Development Contributions – Discussion Paper to the Department of Internal Affairs

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

November A&T 2012.Pub

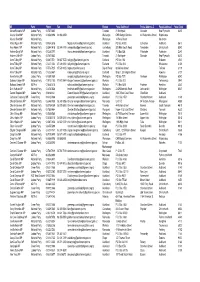

Building Activity On The Rise In Manawatū according to Statistics New Zealand data for October which shows the value of residential building consents in Manawatū is on the increase with residential building consents valued at $25.5 million during the last quarter (end of August) up 13% for the same period last year. Although residential building consents were down 3% in Palmerston North, consents for additions and alterations totalled $2.2 million, which is an increase of 17% compared to the same period last year. Palmerston North Mayor Jono Naylor said that the increase was a sign of recovery in building activity and a big positive for the City and the region. “While the growth in new housing is not happening, residents are choosing to spend money on renovating their homes which is good for local economy.” Graph Source: Manawatu Monthly Economic Update—September 2012 using Stascs NZ data The total Manawatū District residential consent values of $9.4 million in the three months to August, an increase of 45% in the three months to August. Source: Press Release: Palmerston North City Council 2 October 2012 Palmerston North is set to go metropolitan in about five years' time when it is projected to be home to more than 90,000 people. The latest population projections from Statistics New Zealand show the city is the fifth-equal fastest growing area in New Zealand. Mayor Jono Naylor said Palmerston North had already joined Local Government New Zealand (LGNZ's) metropolitan group, as it was already close to the mark at 85,100 and had more issues in common with the major centres than other provincial cities. -

Ms Central Districts Newsletter Nov - Jan 2017

MS CENTRAL DISTRICTS NEWSLETTER NOV - JAN 2017 ANNUAL APPEAL DAY, 2ND SEPTEMBER, 2016 Many thanks to all our collectors and helpers for our Annual Ap- peal Day 2016… with a total of $7,600 of funds raised this was a huge effort! Inside this issue: Our thanks also to these Lions Clubs - Dannevirke, Norsewood, PN Heartland, & Papaioea Rose City who all helped us out this President report 2 year collecting as well! Please see pics on pages of some of our collectors in the region. From the Field Worker’s 3 CHRISTMAS CLOSURE DATES - MSCD Office Annual Appeal Day Pics 4 –5 will be closed from Art Exhibition Pics 6 21st December 2016 - 9th January 2017 MFML Course 7 Multiple Sclerosis Awareness Please find below a link to video 1 of 3 that MSNZ and MS Christmas Message 8 Auckland have been working on over recent months to help show what MS means to people diagnosed. This is the first of 3 videos Maintenance Therapy Pro- 9 which we will be releasing over coming months. - grammes https://youtu.be/-6eraH6mIXI Brain Fog Explained 10 Christmas lunches/dinners 11-12 IMPORTANT DATES TO REMEMBER! Food Together / Joke Cor- 13 ner Regional Christmas Lunches - usual scheduled dates, Notice Board 14 except for Otaki and Levin (see Pg 18) MSCD - The Gathering Xmas Dinner - 19 November Useful Information 15 Levin Ladies Shopping Day - 1st December, 10.00am Subs/Donations Form 16 Recipes 17 DISCLAIMER: THE VIEWS AND EXPRESSED IN THIS NEWSLETTER ARE THOSE OF MSCD Maint. Therapy / 18-19 THE AUTHORS AND NOT NECESSARILY THOSE OF MS CENTRAL DISTRICTS. -

Freshwater Reform 2013 and Beyond 8Apr2013

8 APRIL 2013 LOCAL GOVERNMENT NEW ZEALAND SUBMISSION In the matter of the discussion document: Freshwater reform 2013 and beyond. To the Ministry for the Environment 1 Submission by Local Government New Zealand IN THE MATTER OF: Freshwater reform 2013 and beyond To the Ministry for the Environment 8 APRIL 2013 Introduction 1. Local Government New Zealand (LGNZ) welcomes the opportunity to submit on the Discussion document: Freshwater reform 2013 and beyond. 2. LGNZ wishes to engage further with Minsters and officials on this submission. 3. LGNZ is a member-based organisation representing all 78 local authorities in New Zealand. LGNZ’s governance body is the National Council. The members of the National Council are: . Lawrence Yule, President, Mayor, Hastings District Council . John Forbes, Vice-President, Mayor, Opotiki District Council . John Bain, Zone 1, Deputy Chair, Northland Regional Council . Richard Northey, Zone 1, Councillor, Auckland Council . Meng Foon, Zone 2, Mayor, Gisborne District Council . Jono Naylor, Zone 3, Mayor, Palmerston North City Council . Adrienne Staples, Zone 4, Mayor, South Wairarapa District Council . Maureen Pugh, Zone 5, Mayor, Westland District Council . Tracy Hicks, Zone 6, Mayor, Gore District Council . Len Brown, Metro Sector, Mayor, Auckland Council . Dave Cull, Metro Sector, Mayor, Dunedin City Council . Stuart Crosby, Metro Sector, Mayor, Tauranga City Council . Brendan Duffy, Provincial Sector, Mayor, Horowhenua District Council . Stephen Woodhead, Regional Sector, Chair, Otago Regional Council . Fran Wilde, Regional Sector, Chair, Greater Wellington Regional Council. 4. This submission has been prepared under the direction of the National Council. Councils may choose to make individual submissions. The LGNZ submission does not derogate from these individual submissions. -

To the Productivity Commission

11 MARCH 2013 LOCAL GOVERNMENT NEW ZEALAND SUBMISSION Towards Better Local Regulation To the Productivity Commission 1 Submission by Local Government New Zealand IN THE MATTER OF: TOWARDS BETTER LOCAL REGULATION Page 2 of 19 TowardsTo Betterthe Local Productivity Regulation - LGNZ Submission Commission Our ref: EN 21-20 11 MARCH 2013 Table of Contents Introduction ...................................................................................................................................................... 4 Productivity Review Report “Towards better local regulation.” ................................................................... 6 Local government in New Zealand ....................................................................................................... 6 Diversity across local authorities .......................................................................................................... 7 Allocating regulatory responsibilities ................................................................................................... 7 The funding of regulation ..................................................................................................................... 8 Regulation making by local government .............................................................................................. 9 Local government cooperation ........................................................................................................... 10 Local authorities as regulators............................................................................................................11 -

Resource Management Amendment Bill 29Nov2012

29 NOVEMBER 2012 LOCAL GOVERNMENT NEW ZEALAND SUBMISSION In the matter of Resource Management (Restricted Duration of Certain Discharge and Coastal Permits) Amendment Bill . To the Local Government and Environment Select Committee LOCAL GOVERNMENT NEW ZEALAND 1 OF 7 Contents Introduction ....................................................................................................................................................... 3 Executive Summary ........................................................................................................................................... 3 Recommendation .............................................................................................................................................. 4 Our submission .................................................................................................................................................. 4 This Bill is unnecessary ...................................................................................................................................... 5 Page 2 of 7 LGNZ Submission Resource Management (Restricted duration of certain discharge and coastal permits) Amendment Bill – 29 Nov 2012 Our ref: EN21-20-2 Introduction 1. Local Government New Zealand (LGNZ) welcomes the opportunity to submit on the Resource Management (Restricted Duration of Certain Discharge and Coastal Permits) Amendment Bill (the Bill). 2. Local Government New Zealand is a member based organisation representing all 78 local authorities in New -

Newsletter 2016 - April -May Volume 22 No 3 3 June 2016

Palmerston North Boys’ High School Newsletter 2016 - April -May Volume 22 No 3 3 June 2016 John Adams, Guidance Counsellor, Flyover at School ANZAC service Sir John Kirwan encouraging boys to deal with depression retires after 27 years service The German Tour outside Cologne Cathedral Te Ariki Te Puni wins Racial Unity competiton Xavier Hill and others in th the Open 200 Medley The Old Art Block goes as new facility being built The annual Road Race saw Murray come out on top. Ethanpage Helu-Makasini 1 scoring in the victory over Francis Douglas - the first white jersey match A team who worked hard, who believed in themselves and, as Pe- ter Fitzsimons recently wrote, a team “who believed in the virtue From the Rector of team above all.” A team that showed resilience, grit and charac- Mr David Bovey ter. It is said that in January the board told the team and its man- agement they could now afford to buy a couple of big stars; the team said no. We believe in each other, and will continue playing just the way we have. And they did. In 1592 William Shakespeare’s Richard III opened with the famous line “Now is the winter of our discontent, made glorious summer by this sun of York” and while the eponymous character’s soliloquy develops into something much more, it is oft quoted as the weather turns and the gloomy months of winter descend upon us. The arrival of the perennially busy second term, after a wonderful summer and autumn, brings with it the winter sports season, cultural performances and, most importantly, examinations and assessments. -

Members Offices As at 21 June 2016.Xlsx

MP Party Phone Fax Email Region Postal Address 1 Postal Address 2 Postal Address 3 Postal Code Adrian Rurawhe MP Labour Party 06 757 5662 Taranaki 21 Northgate Strandon New Plymouth 4312 Alastair Scott MP National Party 06 858 8196 06 858 8459 Wairarapa CHB Budget Services 43 Ruataniwha Street Waipukurau Alastair Scott MP National Party Wairarapa 14 Perry Street Masterton Alfred Ngaro MP National Party 09 834 3676 [email protected] Auckland PO Box 83200 Edmonton Auckland 0610 Amy Adams MP National Party 03 344 0418 03 344 0419 [email protected] Canterbury 829 Main South Road Templeton Christchurch 8042 Andrew Bayly MP National Party 09 238 5977 [email protected] Auckland P O Box 528 Pukekohe Pukekohe 2340 Andrew Little MP Labour Party 06 757 5662 Taranaki 21 Northgate Strandon New Plymouth 4312 Anne Tolley MP National Party 06 867 7571 06 867 7572 [email protected] Eastland PO Box 106 Gisborne 4040 Anne Tolley MP National Party 07 307 1254 07 308 0351 [email protected] Eastland P.O. Box 216 Whakatane 3158 Anne Tolley MP National Party 07 573 7125 07 573 9125 [email protected] Bay of Plenty 68 Jellicoe Street Te Puke 3119 Anne Tolley MP National Party 07 323 6487 [email protected] Eastland Shop 1, 35 Islington Street Kawerau 3127 Annette King MP Labour Party 04 389 0989 [email protected] Wellington PO Box 7071 Newtown Wellington 6242 Barbara Kuriger MP National Party 07 870 1005 07 870 3904 [email protected] Waikato P.O. -

Computers in Homes Annual Report 2013

Computers in Homes Annual Report july 2013 Computers in Homes is an initiative of the 2020 Communications Trust. The programme receives support from the Government’s Digital Literacy and Connection Fund (administered by the Department of Internal Affairs) and the Ministry of Education as well as numerous business and community partners. Website: www.computersinhomes.org.nz The 2020 Communications Trust is a registered charitable Trust, established in 1996. Website: www.2020.org.nz Contents Comment from Programme Director. 5 Comment from National Coordinator. 7 Comment from Project Researcher. 8 Case Studies. .20 Far North . .24 Northland. .26 Auckland. 28 Waikato. .30 Bay of Plenty. .32 Hawkes Bay. 34 Taranaki. .36 Wanganui . .38 Manawatu/Horowhenua. .40 Wairarapa. .42 Porirua. 44 Wellington/Lower Hutt. 46 Nelson/Marlborough. 48 Christchurch. .50 West Coast. 52 Dunedin. .54 Refugee Programme. .56 KiwiSkills. 58 Stepping UP. 60 Acknowledgements. 66 Front cover: The Pasifika community in Blenheim turned out in force to support the families graduating from Computers in Homes in May 2013. These Polyfest performers hurried back from their Christchurch competitions the night before, especially to honour their graduate parents. 4 ComPuteRs in Homes gRAduAtes 2012–13: Graduated In Training Dunedin Christchurch West Coast Nelson/Marlborough Wellington/Hutt Porirua Wairarapa Manawatu/Horowhenua Whanganui Taranaki/ Central North Is Hawkes Bay Bay of Plenty Waikato Auckland Northland Far North 0 20 40 60 80 100 120 140 160 180 200 ComPuteRs in Homes -

Parliamentary Scrutiny of Human Rights in New Zealand (Report)

PARLIAMENTARY SCRUTINY OF HUMAN RIGHTS IN NEW ZEALAND: GLASS HALF FULL? Prof. Judy McGregor and Prof. Margaret Wilson AUT UNIVERSITY | UNIVERSITY OF WAIKATO RESEARCH FUNDED BY THE NEW ZEALAND LAW FOUNDATION Table of Contents Introduction ............................................................................................................................... 2 Recent Scholarship ..................................................................................................................... 3 Methodology ............................................................................................................................ 22 Select committee controversy ................................................................................................. 28 Rights-infringing legislation. .................................................................................................... 32 Criminal Records (Expungement of Convictions for Historical Homosexual Offences) Bill. ... 45 Domestic Violence-Victims’ Protection Bill ............................................................................. 60 The Electoral (Integrity) Amendment Bill ................................................................................ 75 Parliamentary scrutiny of human rights in New Zealand: Summary report. .......................... 89 1 Introduction This research is a focused project on one aspect of the parliamentary process. It provides a contextualised account of select committees and their scrutiny of human rights with a particular -

CDEM Group Plan

CIVIL DEFENCE EMERGENCY MANAGEMENT GROUP PLAN 2016 - 2021 VERSION 1.5 JUNE 2020 FOREWORD FROM THE CHAIRMAN This is the fourth generation The Coordinating Executive Group Plan for the Manawatū- Group oversees the coordinated Whanganui Civil Defence Emergency implementation of this Plan and the Management (CDEM) Group. Over Business Plan on behalf of the Group the life of the last Group Plan a with the Joint Standing Committee strong focus was on growing the providing the governance and understanding of the hazards accountability to the community. and risks faced by communities in the Region with much of the This Group Plan is a strategic focus of the regions emergency document that outlines our visions management fraternity being on and goals for CDEM and how we response capability. During that will achieve them, and how we will time an emphasis was placed measure our performance. It seeks on further nurturing the already to: Chairman Bruce Gordon strong relationships developed • Further strengthen the Manawatū-Whanganui Civil Defence across and within the Group at all Emergency Management Group relationships between agencies Joint Standing Committee levels, including the emergency involved in CDEM; management, local government, • Encourage cooperative planning and partner agency sectors – this and action between the various focus will continue under this Group emergency management Plan. The principles of the Group agencies and the community; of consistency, accountability, best • Demonstrate commitment to practice and support, have been, and “Over the life of this deliver more effective CDEM will continue to be the foundation of through an agreed work Group Plan there will the Group. -

Marine Legislation Bill Submission Oct2

OCTOBER 2012 LOCAL GOVERNMENT NEW ZEALAND SUBMISSION In the matter of the Marine Legislation Bill To the Transport and Industrial Relations Select Committee 1 JUNE 2012 Submission by Local Government New Zealand IN THE MATTER OF: The Marine Legislation Bill To the Transport and Industrial Relations Select Committee JULY 2012 Introduction 1. Local Government New Zealand (LGNZ) thanks the Transport and Industrial Relations Select Committee for the opportunity to make this submission in relation to the Marine Legislation Bill. 2. LGNZ wishes to be heard in respect of this submission. LGNZ is a member based organisation representing all 78 local authorities in New Zealand. LGNZ’s governance body is the National Council. The members of the National Council are: Lawrence Yule, President, Mayor, Hastings District Council John Forbes, Vice-President, Mayor, Opotiki District Council John Bain, Zone 1, Deputy Chair, Northland Regional Council Richard Northey, Zone 1, Councillor, Auckland Council Meng Foon, Zone 2, Mayor, Gisborne District Council Jono Naylor, Zone 3, Mayor, Palmerston North City Council Adrienne Staples, Zone 4, Mayor, South Wairarapa District Council Maureen Pugh, Zone 5, Mayor, Westland District Council Tracy Hicks, Zone 6, Mayor, Gore District Council Len Brown, Metro Sector, Mayor, Auckland Council Dave Cull, Metro Sector, Mayor, Dunedin City Council Stuart Crosby, Metro Sector, Mayor, Tauranga City Council Brendan Duffy, Provincial Sector, Mayor, Horowhenua District Council Stephen Woodhead, Regional Sector, Chair, Otago Regional Council Fran Wilde, Regional Sector, Chair, Greater Wellington Regional Council. 3. LGNZ makes this submission on behalf of the National Council, representing the interests of all local authorities of New Zealand. -

MASSEY RESEARCH the Rebirth of Plastic Research, Scholarship and Creativity Evolution at Work September 2009 the Joy of Sects ISSN 1177-2247

MASSEY RESEARCH The rebirth of plastic Research, Scholarship and Creativity Evolution at work September 2009 The joy of sects ISSN 1177-2247 Fire and ice Living with volcanoes MASSEY RESEARCH 1 Why science matters sk Professor Peter Gluckman about how New Zealand’s truth statements from scientists, who themselves are socially powerful, reporting of science stacks up, and he will make no arbitrary, unelected authority figures”. bones about it. “Right now the general quality of science But, let us spare a thought for mainstream media – the MSM, as reporting in New Zealand is terrible by international it is sometimes referred to – which has pressing concerns of its own. Astandards; there is no coherent attempt to explain the issues of the The Trademes and Seeks have run off with its advertisers. Bloggers day or to explore what New Zealand science is delivering,” the and news sites have pilfered its paying readership. The industry has newly appointed Chief Science Adviser told an audience on Massey’s had to cut its suit according to its somewhat shabbier cloth. Struggling Manawatu campus in July of this year. publications have folded and there has been a steady attrition of I agree with him: we are not as well served as we should be by the reporters from the newsrooms. At times such as these, high-mindedly media’s coverage of science, and the lack of serious coverage both calling on the members of the fourth estate to provide critical, fair diminishes the richness of our understanding of the times we live in and comprehensive science reporting will only yield so much.