Cargills (Ceylon) PLC (CARG.N0000)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Journal of the International Association for Bon Research

THE JOURNAL OF THE INTERNATIONAL ASSOCIATION FOR BON RESEARCH ✴ LA REVUE DE L’ASSOCIATION INTERNATIONALE POUR LA RECHERCHE SUR LE BÖN New Horizons in Bon Studies 3 Inaugural Issue Volume 1 – Issue 1 The International Association for Bon Research L’association pour la recherche sur le Bön c/o Dr J.F. Marc des Jardins Department of Religion, Concordia University 1455 de Maisonneuve Ouest, R205 Montreal, Quebec H3G 1M8 Logo: “Gshen rab mi bo descending to Earth as a Coucou bird” by Agnieszka Helman-Wazny Copyright © 2013 The International Association for Bon Research ISSN: 2291-8663 THE JOURNAL OF THE INTERNATIONAL ASSOCIATION FOR BON RESEARCH – LA REVUE DE L’ASSOCIATION INTERNATIONALE POUR LA RECHERCHE SUR LE BÖN (JIABR-RAIRB) Inaugural Issue – Première parution December 2013 – Décembre 2013 Chief editor: J.F. Marc des Jardins Editor of this issue: Nathan W. Hill Editorial Board: Samten G. Karmay (CNRS); Nathan Hill (SOAS); Charles Ramble (EPHE, CNRS); Tsering Thar (Minzu University of China); J.F. Marc des Jardins (Concordia). Introduction: The JIABR – RAIBR is the yearly publication of the International Association for Bon Research. The IABR is a non-profit organisation registered under the Federal Canadian Registrar (DATE). IABR - AIRB is an association dedicated to the study and the promotion of research on the Tibetan Bön religion. It is an association of dedicated researchers who engage in the critical analysis and research on Bön according to commonly accepted scientific criteria in scientific institutes. The fields of studies represented by our members encompass the different academic disciplines found in Humanities, Social Sciences and other connected specialities. -

Sri Lanka a Handbook for US Fulbright Grantees

Welcome to Sri Lanka A Handbook for US Fulbright Grantees US – SL Fulbright Commission (US-SLFC) 55 Abdul Cafoor Mawatha Colombo 3 Sri Lanka Tel: + 94-11-256-4176 Fax: + 94-11-256-4153 Email: [email protected] Website: www.fulbrightsrilanka.com Contents Map of Sri Lanka Welcome Sri Lanka: General Information Facts Sri Lanka: An Overview Educational System Pre-departure Official Grantee Status Obtaining your Visa Travel Things to Bring Health & Medical Insurance Customs Clearance Use of the Diplomatic pouch Preparing for change Recommended Reading/Resources In Country Arrival Welcome-pack Orientation Jet Lag Coping with the Tropical Climate Map of Colombo What’s Where in Colombo Restaurants Transport Housing Money Matters Banks Communication Shipping goods home Health Senior Scholars with Families Things to Do Life and Work in Sri Lanka The US Scholar in Sri Lanka Midterm and Final Reports Shopping Useful Telephone Numbers Your Feedback Appendix: Domestic Notes for Sri Lanka (Compiled by U.S. Fulbrighters 2008-09) The cover depicts a Sandakadaphana; the intricately curved stone base built into the foot of the entrances to buildings of ancient kingdoms. The stone derives it’s Sinhala name from its resemblance to the shape of a half-moon and each motif symbolises a concept in Buddhism. The oldest and most intricately craved Sandakadaphana belongs to the Anuradhapura Kingdom. 2 “My preparation for this long trip unearthed an assortment of information about Sri Lanka that was hard to synthesize – history, religions, laws, nature and ethnic conflict on the one hand and names, advice, maps and travel tips on the other. -

“Inelastic Proxy for Consumption Growth”

“Inelastic Proxy for Consumption Growth” Liquor Sector in Sri Lanka March 2016 Analyst- Hiruni Perera [email protected] 011 5889809 LOLC Securities Limited (An LOLC Group Company) Contents Investment Case Industry Dynamics Liquor industry to reap benefits from expected increase in GDP Inelastic demand for Arrack consumption Arrack Consumption to maintain a modest growth of 1.7% Inelastic demand for malt liquor (Beer) consumption Beer consumption growth to slow with recent excise duty hike Excise duty for 1% of alc. strength of Beer > Excise duty paid for 1% of alc. strength of Arrack However demand growth for Beer to outpace growth for Arrack in mid-long term We estimate 4% growth in total recorded liquor consumption for 2016 Growth in tourism can be a key catalyst for the growth in the liquor sector LOLC Securities Limited | Sector Research 2 Contents contd. Industry Dynamics contd. A gradual reduction in the illicit and illegal liquor consumption Budget 2016 is trending positive for big players Excise duty on liquor to play an important role in the Gvt. Fiscal revenue Less likelihood of a complete ban of liquor in Sri Lanka However certain countries exists in the world with prohibition of liquor Tight regulations to govern the liquor industry in Sri Lanka Cultural and demographic factors to influence liquor consumption We estimate liquor consumers to represent 25% of population Key Players in the industry Appendices LOLC Securities Limited | Sector Research 3 Investment Case LOLC Securities Limited | Sector Research 4 Investment Case Inelastic proxy for consumption growth……. Liquor consumption in Sri Lanka is expected to be supported from the increase in GDP per capita income due to its strong positive correlation between total liquor consumption and GDP. -

Puttalam Lagoon System an Environmental and Fisheries Profile

REGIONAL FISHERIES LIVELIHOODS PROGRAMME FOR SOUTH AND SOUTHEAST ASIA (RFLP) --------------------------------------------------------- An Environmental and Fisheries Profile of the Puttalam Lagoon System (Activity 1.4.1 : Consolidate and finalize reports on physio-chemical, geo-morphological, socio-economic, fisheries, environmental and land use associated with the Puttalam lagoon ecosystem) For the Regional Fisheries Livelihoods Programme for South and Southeast Asia Prepared by Sriyanie Miththapala (compiler) IUCN, International Union for Conservation of Nature, Sri Lanka Country Office October 2011 REGIONAL FISHERIES LIVELIHOODS PROGRAMME FOR SOUTH AND SOUTHEAST ASIA (RFLP) – SRI LANKA An Environmental and Fisheries Profile of the Puttalam Lagoon System (Activity 1.4.1- Consolidate and finalize reports on physio-chemical, geo-morphological, socio-economic, fisheries, environment and land use associated with Puttalam lagoon ecosystem) For the Regional Fisheries Livelihoods Programme for South and Southeast Asia Prepared by Sriyanie Miththapala (compiler) IUCN, International Union for Conservation of Nature, Sri Lanka Country Office October 2011 i Disclaimer and copyright text This publication has been made with the financial support of the Spanish Agency of International Cooperation for Development (AECID) through an FAO trust-fund project, the Regional Fisheries Livelihoods Programme (RFLP) for South and Southeast Asia. The content of this publication does not necessarily reflect the opinion of FAO, AECID, or RFLP. All rights reserved. Reproduction and dissemination of material in this information product for educational and other non-commercial purposes are authorized without any prior written permission from the copyright holders provided the source is fully acknowledged. Reproduction of material in this information product for resale or other commercial purposes is prohibited without written permission of the copyright holders. -

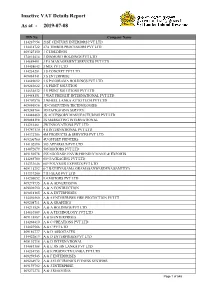

Inactive VAT Details Report As at - 2019-07-08

Inactive VAT Details Report As at - 2019-07-08 TIN No Company Name 114287954 21ST CENTURY INTERIORS PVT LTD 114418722 27A TIMBER PROCESSORS PVT LTD 409327150 3 C HOLDINGS 174814414 3 DIAMOND HOLDINGS PVT LTD 114689491 3 FA MANAGEMENT SERVICES PVT LTD 114458643 3 MIX PVT LTD 114234281 3 S CONCEPT PVT LTD 409084141 3 S ENTERPRISE 114689092 3 S PANORAMA HOLDINGS PVT LTD 409243622 3 S PRINT SOLUTION 114634832 3 S PRINT SOLUTIONS PVT LTD 114488151 3 WAY FREIGHT INTERNATIONAL PVT LTD 114707570 3 WHEEL LANKA AUTO TECH PVT LTD 409086896 3D COMPUTING TECHNOLOGIES 409248764 3D PACKAGING SERVICE 114448460 3S ACCESSORY MANUFACTURING PVT LTD 409088198 3S MARKETING INTERNATIONAL 114251461 3W INNOVATIONS PVT LTD 114747130 4 S INTERNATIONAL PVT LTD 114372706 4M PRODUCTS & SERVICES PVT LTD 409206760 4U OFFSET PRINTERS 114102890 505 APPAREL'S PVT LTD 114072079 505 MOTORS PVT LTD 409150578 555 EGODAGE ENVIR;FRENDLY MANU;& EXPORTS 114265780 609 PACKAGING PVT LTD 114333646 609 POLYMER EXPORTS PVT LTD 409115292 6-7 BATHIYAGAMA GRAMASANWARDENA SAMITIYA 114337200 7TH GEAR PVT LTD 114205052 9.4.MOTORS PVT LTD 409274935 A & A ADVERTISING 409096590 A & A CONTRUCTION 409018165 A & A ENTERPRISES 114456560 A & A ENTERPRISES FIRE PROTECTION PVT LT 409208711 A & A GRAPHICS 114211524 A & A HOLDINGS PVT LTD 114610569 A & A TECHNOLOGY PVT LTD 409118887 A & B ENTERPRISES 114268410 A & C CREATIONS PVT LTD 114023566 A & C PVT LTD 409186777 A & D ASSOCIATES 114422819 A & D ENTERPRISES PVT LTD 409192718 A & D INTERNATIONAL 114081388 A & E JIN JIN LANKA PVT LTD 114234753 A & -

Sri Lankan Spring Supper

SRI LANKAN SPRING SUPPER Butternut squash, green kale & raw green mango patty empanadas, tamarind mayo Black pepper pulled pork shoulder, kithul and elderflower caramel Aubergine and jaggery moju Northern turmeric dahl, tempered onion & black mustard seeds Burnt pork crackling coconut pol sambol Smoked coconut yoghurt Green tea and jasmine cucumber, chilli capsicum, Spanish black & daikon radish pickles Roast paan bread, seeni sambol butter Muthu Samba rice – Arrack, cinnamon & coconut kiri-bath rice pudding, candied pistachios Fresh Sri Lankan ginger beer Sri Lankan Spring Supper by Hōtal Paradise 4. When you are ready for your main course, empty the pork into a saucepan and place over a medium heat. Add 20ml of water 35 minutes A fiery, modern riff on the traditional to loosen the meat. Cook for 10-15 minutes, stirring occasionally. Dutch-Burgher Lamprais. Serves 2 5. Empty the dahl into a small saucepan, add a splash of water and warm over a medium heat for 5-7 minutes. Halfway through, add the onion and black mustard seed temper and stir to combine. In the Box Give the instructions a read through to familiarise yourself with the process before you start. Moju 6. Place the paan bread under the grill and lightly toast on both sides. Cut into slices and plate with the seeni sambol butter . Muthu samba rice Remove aubergine moju and seeni sambol butter Empanadas from the fridge to allow to come to room temperature. 7. The aubergine moju can either be enjoyed at room temperature or heated in the microwave for 90 seconds according to preference. -

Annual Report 2014/15

Annual Report 2014/15 | ReportAnnual 2014/15 Lion Brewery (Ceylon) PLC Lion Brewery Annual ReportAnnual 2014/15 END OF THE BEGINNING Lion Brewery (Ceylon) PLC Read the Lion Brewery (Ceylon) PLC Annual Report 2014/15 online 1 Annual Report 2014/15 END OF THE BEGINNING Lion Brewery was incorporated in 1996 as a joint venture between Ceylon Brewery (now known as Ceylon Beverage Holdings PLC) and the global brewing giant Carlsberg. Today its portfolio includes a trio of Lion brands, widely acclaimed as Sri Lanka’s finest beers and Carlsberg & Carlsberg Special Brew, which are brewed and marketed under license. Both the Lion and Carlsberg claim to heritage of over a century in brewing excellence and market leadership. Recently Lion Brewery acquired the Three Coins and Sando portfolio and with it a range of brands that have served Sri Lankan consumers for well over 5 decades. In its formative years, Lion has built a strong foundation to grasp the opportunities that lie ahead. It has remained true to its rich heritage of brewing excellence but has nevertheless modernised to remain relevant to the 21st century. Lion has an aggressive and creative corporate culture that is driven by consumer needs and supported by a truly state of the art manufacturing facility and supply chain excellence. It may operate in the most regulated industry in the Country, but this is a challenge its talented team thrives on as they strive to exceed stakeholder expectations. At Lion the journey is never ending. Perfection is said to be unattainable but it doesn’t stop us from seeking it. -

St. Michael No. 53Cdr.Cdr

9 2 . l Apr - Sep p e e a S h 2011 c The Archangel y i a M Newsletter of D . t t s S The St. Michael's College, Batticaloa, Alumni Association (Colombo Branch) a e Published Quarterly For Private Circulation. No. 53 F Michaelites Shine here and abroad First bishop from SMC Rev. John Jegasothy - An Dhiloraj Ranjit Canagasabey Outstanding Australian Helping Refugees Rev. John Daniel Jegasothy B.Th.Hon., B.D., M.Th., J.P. was ordained as is 15th Bishop of Colombo Minister of the Methodist Church in 1977. After serving in Colombo he Venerable Dhiloraj Ranjit Canagasabey B.Th., B.Div., the first ever past moved during the height of the Eelam war to Trincomalee as Circuit pupil of SMC to become bishop, was consecrated and installed as the Superintendent (1981-1983). 15th Bishop of Colombo of the Church of Sri Lanka by 8 Anglican Bishops, In Trinco he headed the Human Rights Group and in association with the local and foreign, at a festive trilingual service at the Cathedral of Christ Rotary Club of Trincomalee, the YMCA, the Tricomalee Welfare the Living Saviour, Colombo, on May 14, 2011. Bishop Dhilo Association, Ghandiam and his church he took up the cause of the displaced Canagasabey succeeds Rt Rev. Duleep de Chickera and is the second and otherwise affected people and demanded justice. It did not take long Tamil after Rt Rev.J.J.Gnanapragasam (1987 - 1992). for him to come under the adverse notice of the security establishment and Among the over 5,000 well wishers present to greet the new Bishop were he sensed danger. -

Lion Brewery (Ceylon) PLC

Lion Brewery (Ceylon) PLC Annual Report 2015/16 CONTENTS Financial Highlights 1 Chairman’s Message 2 - 3 Chief Executive’s Review 4 - 11 Profiles of Directors 12 - 13 Senior Management Team 14 - 16 Annual Report of the Board of Directors on the Affairs of the Company 17 - 24 Audit Committee Report 25 - 26 Report of the Related Party Transactions Review Committee 27 Financial Calendar 28 Independent Auditors’ Report 29 Statement of Financial Position 30 - 31 Statement of Profit or Loss and Other Comprehensive Income 32 Statement of Changes In Equity 33 - 34 Cash Flow Statement 35 - 36 Notes to the Financial Statements 37 - 74 Value Added Statement 75 Five Year Summary 76 - 77 Statement of Profit or Loss and Other Comprehensive Income - US$ 78 Statement of Financial Position - US$ 79 Notes to the Financial Statements - US$ 80 Five Year Summary - US$ 81 Information to Shareholders & Investors 82 - 83 Glossary of Financial Terms 84 Notice of Meeting 85 Form of Proxy 87 - 88 Corporate Information IBC FINANCIAL HIGHLIGHTS In Rs.’000 2016 2015 Change % Revenue 35,526,379 32,350,375 9.8 Profit before finance cost 3,877,479 2,984,420 29.9 Profit before taxation 2,958,357 2,386,367 24.0 Profit after taxation 2,080,545 1,330,320 56.4 Dividends per share (Rs.) 3.00 4.00 (25.0) Shareholders’ funds 9,986,134 7,926,582 26.0 Total assets 28,040,272 26,521,313 5.7 Earnings per ordinary share (Rs.) 26.01 16.63 56.4 Net assets per ordinary share (Rs.) 124.83 99.08 26.0 Market capitalisation 36,720,000 48,000,000 (23.5) Annual Report 2015/16 Lion Brewery (Ceylon) PLC 1 CHAIRMAN’S MESSAGE The increase in turnover was entirely driven by price increases necessitated consequent to stiff rises in excise duty. -

SELECTED PAPERS of SIBA- MCU INTERNATIONAL BUDDHIST CONFERENCE 2013 on International Exchange of Buddhism in the Global Context

Selected Papers of SIBA-MCU INTERNATIONAL BUDDHIST CONFERENCE 2013 on International Exchange of Buddhism in the Global Context Jointly Organized by The Supreme Sangha of Mahachulalongkornrajavidyalya University Thailand and Sri Lanka International Buddhist Academy held on 20th & 21st August 2556/ 2013 at Sri Lanka International Buddhist Academy Pallekele, Kandy Sri Lanka. ii SELECTED PAPERS OF SIBA- MCU INTERNATIONAL BUDDHIST CONFERENCE 2013 on International Exchange of Buddhism in the Global Context ISSN – 2449-0148 16. 07. 2015 Publisher: Sri Lanka International Buddhist Academy (SIBA) Pallekele, Kundasale 20168, Sri Lanka. iii Advisory Board Dr. Upali M. Sedere Prof. Udaya Meddegama Review Panel Prof. Udaya Meddegama Prof. Ratne Wijetunge Ven. Dr. Medagampitiye Wijitadhamma Ven. Dr. Bhikkhuni W. Suvimalee Dr. Vijita Kumara Mr. A. B. Mediwake Editors Ven. Mahawela Ratanapala Ms. Iromi Ariyaratne Cover page Designers Mr. Udara Kotandeniya Ms. Hasanthi Dahanayake Mr. Thilina Bandara iv Foreword v Foreword This volume is a result of the successful International Conference on ‘Global Exchange of Buddhism’ which was held on August 20, 2013 on the occasion of commemorating the 260th Anniversary of the establishment of the Siyam Maha Nikaya in Sri Lanka. The conference was a joint sponsorship of the Mahachulalongkornrajavidyalaya University (MCU) of Thailand and Sri Lanka International Buddhist Academy at Kundasale, Sri Lanka. The conference was held at the Sri Lanka International Buddhist Academy and was well attended by over 200 foreign delegates from 25 countries and over 500 Sri Lankan participants. The abstract book of all papers presented was published before the conference which was made available to all participants. This has also been published on www.sibacampus.com website and those who wish could download free of charge. -

BANK of CEYLON Many Things to Many People

BANK OF CEYLON Many things to many people. ANNUAL REPORT 2011 Many things to many people. The Bank of Ceylon is many things to many people. We serve over ten million customers islandwide and our commitment to each of them remains steadfast. Our multi-faceted offering is one of our greatest strengths. From the smallest child’s savings account to corporate credit for state and private sector companies, we serve at every level. Where others specialise their portfolios, we expand ours. This is how we stay relevant, supportive and diverse. It is why so many different people come to us and stay with us for generations. Bank of Ceylon. We’re many things to many people. ...it is why so many “different people come to us and stay with us for generations.” CONTENTS Business Highlights 02 Financial Highlights 03 Financial Highlights - Graphical Review 04 Vision & Mission 06 Historical Review 08 Chairman’s Message 15 General Manager’s Review 17 Board of Directors 18 Corporate Management 20 Executive Management Team 24 Management Discussion & Analysis 30 Risk Management 56 Corporate Governance 65 Board & Board Subcommittees 88 Report of Board Subcommittees 89 Sustainability Report 98 GRI Standard Disclosures Index 152 Annual Report of the Directors on the State of Affairs of the Bank of Ceylon 160 Directors’ Interest in Contracts 164 Directors’ Statement on Internal Control 169 Independent Assurance Report 171 Directors Responsibility for Financial Reporting 172 Report of the Auditor General 173 Income Statement 174 Balance Sheet 175 Statement of Changes -

A Study of the Influence of Buddhism on Sinhala Language J.W.R.W.K

A Study of the Influence of Buddhism on Sinhala Language J.W.R.W.K. Jayaweera A Dissertation Submitted in Partial Fulfilment of The Requirement for the Degree of Doctor of Philosophy (Buddhist Studies) International Buddhist Studies College Mahachulalongkornrajavidyalaya University Phra Nakorn Si Ayutthaya, Thailand B.E. 2562 (Copyright by Mahachulalongkornrajavidyalaya University) i A Study of the Influence of Buddhism on Sinhala Language J.W.R.W.K. Jayaweera A Dissertation Submitted in Partial Fulfilment of The Requirement for the Degree of Doctor of Philosophy (Buddhist Studies) International Buddhist Studies College Mahachulalongkornrajavidyalaya University Phra Nakorn Si Ayutthaya, Thailand B.E. 2562 (Copyright by Mahachulalongkornrajavidyalaya University) ii Dissertation Title: A Study of the Influence of Buddhism on Sinhala Language Researcher : J.W.R.W.K. Jayaweera Degree : Doctor of Philosophy (Buddhist Studies) Thesis Supervisory Committee : Ven. Dr. Phramaha Surasak Pajanthaseno : Prof. Udaya Meddegama Date of Graduation: ............................................. Abstract The aim of this dissertation is to study the influence of Buddhism on Sinhala language. Sinhala language has a continual history, which dates back to thousands of years. It seems to be a language with written evidences of great history, which dates at least to the 3rd century B.C. Though several evidences could be presented to confirm that there was a writing practice using Sinhala language (Heḷa Basa) after the arrival of Prince Vijaya in Sri Lanka that tradition developed systematically after the introduction of Buddhism by Venerable Mahinda in 3rd century B.C. He acquainted a Brāhmī alphabet becomingly the Brāhmī scripts in Asoka inscriptions to expand the writing methodology in the island.