Audit Report on the Accounts of Tehsil Municipal Administrations Sahiwal

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Power Distribution Enhancement Investment Program – Tranche 4

Resettlement Plan Due Diligence June 2013 MFF 0021-PAK: Power Distribution Enhancement Investment Program – Tranche 4 Prepared by Multan Electric Power Company for the Asian Development Bank. This is a document of the borrower. The views expressed herein do not necessarily represent those of ADB's Board of Directors, Management, or staff, and may be preliminary in nature. Due Diligence Document Document Stage: Final Project Number: M1-M64 {June 2013} Islamic Republic of Pakistan: Multitranche Financing Facility (MFF) For Power Distribution Enhancement Investment Program Tranche-IV: Power Transformer’s Extension & Augmentation Subprojects Prepared by: Environment & Social Safeguards Section Project Management Unit (PMU) MEPCO, Pakistan i Table of contents ABBREVIATIONS ........................................................................................................................................................ iii EXECUTIVE SUMMARY .............................................................................................................................................. iv 1. Project Overview ................................................................................................................................................. 1 1.1 Project Background ...................................................................................................................................... 1 2. Scope of Land Acquisition and Resettlement ................................................................................................. -

List of Branches Authorized for Overnight Clearing (Annexure - II) Branch Sr

List of Branches Authorized for Overnight Clearing (Annexure - II) Branch Sr. # Branch Name City Name Branch Address Code Show Room No. 1, Business & Finance Centre, Plot No. 7/3, Sheet No. S.R. 1, Serai 1 0001 Karachi Main Branch Karachi Quarters, I.I. Chundrigar Road, Karachi 2 0002 Jodia Bazar Karachi Karachi Jodia Bazar, Waqar Centre, Rambharti Street, Karachi 3 0003 Zaibunnisa Street Karachi Karachi Zaibunnisa Street, Near Singer Show Room, Karachi 4 0004 Saddar Karachi Karachi Near English Boot House, Main Zaib un Nisa Street, Saddar, Karachi 5 0005 S.I.T.E. Karachi Karachi Shop No. 48-50, SITE Area, Karachi 6 0006 Timber Market Karachi Karachi Timber Market, Siddique Wahab Road, Old Haji Camp, Karachi 7 0007 New Challi Karachi Karachi Rehmani Chamber, New Challi, Altaf Hussain Road, Karachi 8 0008 Plaza Quarters Karachi Karachi 1-Rehman Court, Greigh Street, Plaza Quarters, Karachi 9 0009 New Naham Road Karachi Karachi B.R. 641, New Naham Road, Karachi 10 0010 Pakistan Chowk Karachi Karachi Pakistan Chowk, Dr. Ziauddin Ahmed Road, Karachi 11 0011 Mithadar Karachi Karachi Sarafa Bazar, Mithadar, Karachi Shop No. G-3, Ground Floor, Plot No. RB-3/1-CIII-A-18, Shiveram Bhatia Building, 12 0013 Burns Road Karachi Karachi Opposite Fresco Chowk, Rambagh Quarters, Karachi 13 0014 Tariq Road Karachi Karachi 124-P, Block-2, P.E.C.H.S. Tariq Road, Karachi 14 0015 North Napier Road Karachi Karachi 34-C, Kassam Chamber's, North Napier Road, Karachi 15 0016 Eid Gah Karachi Karachi Eid Gah, Opp. Khaliq Dina Hall, M.A. -

Unraveling Health Risk and Speciation of Arsenic from Groundwater in Rural Areas of Punjab, Pakistan

Int. J. Environ. Res. Public Health 2015, 12, 12371-12390; doi:10.3390/ijerph121012371 OPEN ACCESS International Journal of Environmental Research and Public Health ISSN 1660-4601 www.mdpi.com/journal/ijerph Article Unraveling Health Risk and Speciation of Arsenic from Groundwater in Rural Areas of Punjab, Pakistan Muhammad Bilal Shakoor 1, Nabeel Khan Niazi 1,2,*, Irshad Bibi 1,2, Mohammad Mahmudur Rahman 3,4,5, Ravi Naidu 4,5, Zhaomin Dong 4,5, Muhammad Shahid 6 and Muhammad Arshad 1 1 Institute of Soil and Environmental Sciences, University of Agriculture Faisalabad, Faisalabad 38040, Pakistan; E-Mails: [email protected] (M.B.S.); [email protected] (I.B.); [email protected] (M.A.) 2 Southern Cross GeoScience, Southern Cross University, Lismore 2480, NSW, Australia 3 Centre for Environmental Risk Assessment and Remediation (CERAR), Mawson Lakes Campus, University of South Australia, SA 5095, Australia; E-Mail: [email protected] 4 Global Centre for Environmental Remediation (GCER), Faculty of Science and Information Technology, The University of Newcastle, University Drive, Callaghan, NSW 2308, Australia; E-Mails: [email protected] (R.N.); [email protected] (Z.D.) 5 Cooperative Research Centre for Contamination Assessment and Remediation of the Environment (CRC CARE), P.O. Box 486, Salisbury South, SA 5106, Australia 6 Department of Environmental Sciences, COMSATS Institute of Information Technology, Vehari 61100, Pakistan; E-Mail: [email protected] * Author to whom correspondence should be addressed; E-Mail: [email protected] or [email protected]; Tel.: +92-41-920-1089; Fax: +92-41-240-9585. -

Field Appraisal Report Tma Renala Khurd

FIELD APPRAISAL REPORT TMA RENALA KHURD Prepared by; Punjab Municipal Development Fund Company December-2008 TABLE OF CONTENTS 1. INSTITUTIONAL DEVELOPMENT 1.1 BACKGROUND 2 1.2 METHODOLOGY 2 1.3 DISTRICT PROFILE 2 1.3.1 History 2 1.3.2 Location 2 1.3.3 Area/Demography 2 1.4 TMA/TOWN PROFILE 3 1.4.1 Municipal Status 3 1.4.2 Location 3 1.4.3 Area / Demography 3 1.5 TMA STAFF PROFILE 4 1.6 INSTITUTIONAL ASSESSMENT 4 1.6.1 Tehsil Nazim 4 1.6.2 Office of Tehsil Municipal Officer 5 1.7 TEHSIL OFFICER (Planning) OFFICE 8 1.8 TEHSIL OFFICER (Regulation) OFFICE 11 1.9 TEHSIL OFFICER (Finance) OFFICE 12 1.10 TEHSIL OFFICER (Infrastructure & Services) OFFICE 16 2. INFRASTRUCTURE DEVELOPMENT 2.1 ROAD NETWORK & STREET LIGHTS 19 2.2 WATER SUPPLY 19 2.3 SEWERAGE 20 2.4 SOLID WASTE MANAGEMENT 21 2.5 PARKS 22 2.6 FIRE FIGHTING 22 3. PROCUREMENT & ENVIRONMENT 3.1 ENVIRONMENT & SOCIAL CONDITIONS 23 3.2 PROCUREMENT CAPACITY 23 1 1. INSTITUTIONAL DEVELOPMENT 1.1 BACKGROUND TMA Renala Khurd has applied for funding under PMSIP. After initial desk appraisal, PMDFC field team visited the TMA for assessing its institutional and engineering capacity. 1.2 METHODOLOGY Appraisal is based on interviews with TMA staff, open-ended and close-ended questionnaires and agency record. Debriefing sessions and discussions were held with Tehsil Nazim, TMO, TOs and other TMA staff. 1.3 DISTRICT PROFILE 1.3.1 History The district Okara derived its name from a tree known as “OKAAN” which was standing on the embankment of a water-tank, being maintained by a person known as “RANA”. -

Of All the Police Stations Sahiwal District Okara

POLICE DEPARTMENT SAHIWAL REGION REQEUST FOR PHYSICAL ADDRESSES/CONTACTS NO/EMAIL ID/ OF ALL THE POLICE STATIONS SAHIWAL DISTRICT S. Name of Police Contact No/ Address of Police Station E-Mail Remarks No. Station Fax 1 PS City Sahiwal Near Municipal Committee Sahiwal 040-9200360 - - 2 PS Civil Line Near Tehsil Office, Sahiwal 040-9200359 - - Near Grain Market Ghalla Mandi, 3 PS Ghalla Mandi 040-9200358 - - Sahiwal 4 PS Fateh Sher Near T.V Boaster, Sahiwal 040-9200235 - - 5 PS Farid Town Near Market Farid Town 040-9200353 - - 6 PS Yousafwala G.T Road Chak No. 84/5-L 040-4301140 - - 7 PS Noor Shah Qasba Noor Shah 040-4469303 - - 8 PS Bahadar Shah Qutab Shahana Road - - - 9 PS Harappa Harappa Town 040-4468817 - - 10 PS Dera Rahim Chak Dera Rahim - - - 11 PS Kamir Sahiwal Arifwala Road 040-4306010 - - Burnt. Presently functioning 12 PS City Chichawatni G.T Road Chichawatni 040-5486237 - in the building of PS Sadar Chichawatni PS Sadar 13 Faisalabad G.T Road 040-5486236 - - Chichawatni Qasba Kassowal-Lahore Multan 14 PS Kassowal 040-5410506 - - G.T Road 15 PS Ghaziabad Chichawatni - Burewala G.T Road - - - Iqbal Nagar-Burwala Road Near 16 PS Shah Kot 040-5435465 - - Adda 90 Morr OKARA DISTRICT S. Name of Police Contact No/ Address of Police Station E-Mail Remarks No. Station Fax Faisalabad Road Porani Ketchehry 1 A-Division 0449200096 - CIA Chowk Okara - Sirki Mohallah Road Near City Stop 2 B-Division 0449200329 - Okara - Near PSO Pump Al Jihad Check 3 Cantt. Okara 0442880510 - Post Multan road Okara - 4 Shahbore Chak No.27/4.L Shahbore 044021103 -

List of Adult Vaccination Centres

LIST OF ADULT VACCINATION CENTRES Province District Tehsil AVC Name Address Timings AJK Muzaffarabad Naseraabad THQ Patikka Town Committee Pattika District Muzaffarabad 9 AM - 3:30 PM AJK Muzaffarabad Muzaffarabad AIMS Muzaffarabad Abbas Institute of Medical Sciences, Ambore District Muzaffarabad 9 AM - 3:30 PM AJK Muzaffarabad Muzaffarabad CMH Muzaffarabad SKBZ CMH Hospital Mir Waiz Road Muzaffarabad 9 AM - 3:30 PM Tehsil Headquarter Hospital Kel near Main Bazar Kel District AJK Neelum Sharda THQ Kel 9 AM - 3:30 PM Neeelum AJK Neelum Athmaqam DHQ Neelum District Headquarter Hospital Athmaqam Neelum 9 AM - 3:30 PM AJK Jhelum Valley Hattian Ballan DHQ Hattian DHQ Hospital near SSP Office Town Committee Hattian 9 AM - 3:30 PM AJK Bagh Bagh DHQ Bagh DHQ Hospital Bagh 9 AM - 3:30 PM AJK Bagh Dhirkot THQ Dhirkot THQ Hospital Dhirkot Tehsil Dhirkot District Bagh 9 AM - 3:30 PM AJK Poonch Rawalakot CMH Rawalakot SKBZ Hospital Rawalakot District Poonch 9 AM - 3:30 PM AJK Poonch Hajeera THQ Hajeera Tehsil headquarter Hospital Hajeera District poonch 9 AM - 3:30 PM AJK Sudhnoti Trarkhal THQ Trarkhel Tehsil Headquarter Hospital Trarkhel District Sudhnoti 9 AM - 3:30 PM AJK Sudhnoti Pallandri DHQ Pallandri District Headquarter Hospital Pallandri District Sudhnoti 9 AM - 3:30 PM AJK Haveli Haveli DHQ Haveli DHQ Hospital Forward kahota District Haveli 9 AM - 3:30 PM AJK Mirpur Mirpur Teaching Hospital New City Sector A New City Mirpur Azad Kashmir 9 AM - 3:30 PM AJK Mirpur Mirpur DHO Office Mirpur Allama Iqbal Road DHO Office Mirpur 9 AM - 3:30 PM -

S.R.O. No.---/2011.In Exercise Of

PART II] THE GAZETTE OF PAKISTAN, EXTRA., JANUARY 9, 2021 39 S.R.O. No.-----------/2011.In exercise of powers conferred under sub-section (3) of Section 4 of the PEMRA Ordinance 2002 (Xlll of 2002), the Pakistan Electronic Media Regulatory Authority is pleased to make and promulgate the following service regulations for appointment, promotion, termination and other terms and conditions of employment of its staff, experts, consultants, advisors etc. ISLAMABAD SATURDAY, JANUARY 9, 2021 PART II Statutory Notifications (S. R. O.) GOVERNMENT OF PAKISTAN MINISTRY OF NATIONAL FOOD SECURITY AND RESEARCH NOTIFICATION Islamabad, the 6th January, 2021 S. R. O. (17) (I)/2021.—In exercise of the powers conferred by section 15 of the Agricultural Pesticides Ordinance, 1971 (II of 1971), and in supersession of its Notifications No. S.R.O. 947(I)/2002, dated the 23rd December, 2002, S.R.O. 1251 (I)2005, dated the 15th December, 2005, S.R.O. 697(I)/2005, dated the 28th June, 2006, S.R.O. 604(I)/2007, dated the 12th June, 2007, S.R.O. 84(I)/2008, dated the 21st January, 2008, S.R.O. 02(I)/2009, dated the 1st January, 2009, S.R.O. 125(I)/2010, dated the 1st March, 2010 and S.R.O. 1096(I), dated the 2nd November, 2010. The Federal Government is pleased to appoint the following officers specified in column (2) of the Table below of Agriculture Department, Government of the Punjab, to be inspectors within the local limits specified against each in column (3) of the said Table, namely:— (39) Price: Rs. -

Determinants of Female Employment Status in Pakistan: a Case of Sahiwal District

A Service of Leibniz-Informationszentrum econstor Wirtschaft Leibniz Information Centre Make Your Publications Visible. zbw for Economics Shaheen, Ruqia; Shabir, Ghulam; Faridi, Muhammad Zahir; Yasmin, Fouzia Article Determinants of female employment status in Pakistan: A case of Sahiwal District Pakistan Journal of Commerce and Social Sciences (PJCSS) Provided in Cooperation with: Johar Education Society, Pakistan (JESPK) Suggested Citation: Shaheen, Ruqia; Shabir, Ghulam; Faridi, Muhammad Zahir; Yasmin, Fouzia (2015) : Determinants of female employment status in Pakistan: A case of Sahiwal District, Pakistan Journal of Commerce and Social Sciences (PJCSS), ISSN 2309-8619, Johar Education Society, Pakistan (JESPK), Lahore, Vol. 9, Iss. 2, pp. 418-437 This Version is available at: http://hdl.handle.net/10419/188204 Standard-Nutzungsbedingungen: Terms of use: Die Dokumente auf EconStor dürfen zu eigenen wissenschaftlichen Documents in EconStor may be saved and copied for your Zwecken und zum Privatgebrauch gespeichert und kopiert werden. personal and scholarly purposes. Sie dürfen die Dokumente nicht für öffentliche oder kommerzielle You are not to copy documents for public or commercial Zwecke vervielfältigen, öffentlich ausstellen, öffentlich zugänglich purposes, to exhibit the documents publicly, to make them machen, vertreiben oder anderweitig nutzen. publicly available on the internet, or to distribute or otherwise use the documents in public. Sofern die Verfasser die Dokumente unter Open-Content-Lizenzen (insbesondere CC-Lizenzen) zur Verfügung gestellt haben sollten, If the documents have been made available under an Open gelten abweichend von diesen Nutzungsbedingungen die in der dort Content Licence (especially Creative Commons Licences), you genannten Lizenz gewährten Nutzungsrechte. may exercise further usage rights as specified in the indicated licence. -

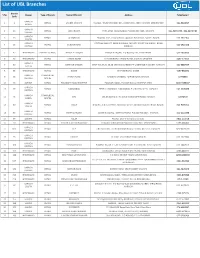

To Download UBL Branch List

List of UBL Branches Branch S No Region Type of Branch Name Of Branch Address Telephone # Code KARACHI 1 2 RETAIL LANDHI KARACHI H-G/9-D, TRUST CERAMIC IND., LANDHI IND. AREA KARACHI (EPZ) EXPORT 021-5018697 NORTH KARACHI 2 19 RETAIL JODIA BAZAR PARA LANE, JODIA BAZAR, P.O.BOX NO.4627, KARACHI. 021-32434679 , 021-32439484 CENTRAL KARACHI 3 23 RETAIL AL-HAROON Shop No. 39/1, Ground Floor, Opposite BVS School, Sadder, Karachi 021-2727106 SOUTH KARACHI CENTRAL BANK OF INDIA BUILDING, OPP CITY COURT,MA JINNAH ROAD 4 25 RETAIL BUNDER ROAD 021-2623128 CENTRAL KARACHI. 5 47 HYDERABAD AMEEN - ISLAMIC PRINCE ALLY ROAD PRINCE ALI ROAD, P.O.BOX NO.131, HYDERABAD. 022-2633606 6 46 HYDERABAD RETAIL TANDO ADAM STATION ROAD TANDO ADAM, DISTRICT SANGHAR. 0235-574313 KARACHI 7 52 RETAIL DEFENCE GARDEN SHOP NO.29,30, 35,36 DEFENCE GARDEN PH-1 DEFENCE H.SOCIETY KARACHI 021-5888434 SOUTH 8 55 HYDERABAD RETAIL BADIN STATION ROAD, BADIN. 0297-861871 KARACHI COMMERCIAL 9 65 NAPIER ROAD KASSIM CHAMBERS, NAPIER ROAD,KARACHI. 32775993 CENTRAL CENTRE 10 66 SUKKUR RETAIL FOUJDARY ROAD KHAIRPUR FOAJDARI ROAD, P.O.BOX NO.14, KHAIRPUR MIRS. 0243-9280047 KARACHI 11 69 RETAIL NAZIMABAD FIRST CHOWRANGI, NAZIMABAD, P.O.BOX NO.2135, KARACHI. 021-6608288 CENTRAL KARACHI COMMERCIAL 12 71 SITE UBL BUILDING S.I.T.E.AREA MANGHOPIR ROAD, KARACHI 32570719 NORTH CENTRE KARACHI 13 80 RETAIL VAULT Shop No. 2, Ground Floor, Nonwhite Center Abdullah Harpoon Road, Karachi. 021-9205312 SOUTH KARACHI 14 85 RETAIL MARRIOT ROAD GILANI BUILDING, MARRIOT ROAD, P.O.BOX NO.5037, KARACHI. -

Sr # Outlet Name Location Address 1 Super Shaheen Umerkot Umerkot 2

Sr # Outlet Name Location Address 1 Super Shaheen Umerkot Umerkot 2 Mukhi Thana Bola Khan Thana Bola Khan 3 A Rahim Sethio Tando Muhammad Khan Sijawal Road Tando Muhammad Khan 4 Bilal Tando Jan Muhammad Tando Jan Muhammad 5 Huziafa Tando Haider Tando Haider 6 Sattar Tando Allahyar Tando Allahyar 7 Imran Tando Adam Tando Adam 8 Habib Sehwan Indus Highway Sehwan 9 PSO S/S 09 Sanghar Tando Adam Road Sanghar 10 Dahri Sakrand Sakrand 11 Jam P/S Qazi Ahmed Qazi Ahmed 12 Qarni Odero Lal Odero Lal 13 Nawabshah Nawabshah Sakrand Road Nawabshah 14 Nasir Mujeeb Nawabshah Sanghar Road Nawabshah 15 Razi Shah Naukot Naukot 16 H Misri Shah Nasarpur Tando Allahyar Roead Nasarpur 17 Jamali Moro Moro 18 Malani Mithi Mithi 19 Shaikh Mirpurkhas Mirpurkhas 20 Nadir Mehar Indus Highway Mehar 21 Shaheed Ismail Matli Badin Road Matli 22 Al Ahmed Matiari NHW Matiari 23 New Abideen Kunri Kunri 24 Diaram Kot Ghulam Muhammad Kot Ghulam Muhammad 25 Nathan Shah KN Shah Indus Highway KN Shah 26 Samo F/S Khyber NHW Khyber 27 Baloch Khorwah Khorwah 28 Mehran Khipro Khipro 29 Al Amin Khanot Indus Highway Khanot 30 Jamali Johi Johi 31 New Razi Shah Islamkot Islamkot 32 Golden Taj Hyderabad Old Sabzi Mandi Hyderabad 33 Platinum Hyderabad Old NHW Hyderabad 34 Hala Hala Hala 35 Gharib Nawaz Daur Daur 36 Carwan e Afandi Dadu Dadu 37 Sikander Dadu Dadu 38 Paras Chachro Chachro 39 Amir Birmani Bhan Syedabad Indus Highway Bhan Syedabad 40 Sadat Badin Badin 41 Shahbaz 1 PS Sukkur Main Bus Stand Sukkur 42 AWT SS Sukkur Ayub Gate Sukkur 43 Rohri PS Rohri Main National Highway, Rohri -

IEE Study for Development of Punjab Wholesale Market Project Rawalpindi

Second Power Transmission Enhancement Investment Program (RRP PAK 48078-002) Initial Environmental Examination May 2016 PAK: Proposed Multitranche Financing Facility Second Power Transmission Enhancement Investment Program Prepared by National Transmission and Despatch Company Limited for the Asian Development Bank. Power Transmission Enhancement Investment Programme II TA 8818 (PAK) Initial Environmental Examination Extension and Augmentation Subprojects in Sahiwal, Lahore South & Rewat May 2016 Prepared by National Transmission & Despatch Company Limited (NTDC) for the Asian Development Bank (ADB) The Initial Environmental Examination Report is a document of the borrower. The views expressed herein do not necessarily represent those of ADB’s Board of Directors, Management, or staff, and may be preliminary in nature. Your attention is directed to the “terms of use” section of the ADB website. In preparing any country program or strategy, financing any project, or by making any designation of or reference to a particular territory or geographic area in this document, the Asian Development Bank does not intend to make any judgements as to the legal or other status of any territory or area. Acronyms 2 | P a g e CURRENCY EQUIVALENTS th As of 16 April 2016 Currency Unit – Pak Rupees (Pak Rs.) Pak Rs 1.00 = $ 0.009 US$1.00 = Pak Rs. 105.8 Acronyms ADB Asian Development Bank NTDC National Transmission & Despatch Company Limited DGS Distribution Grid Substation SPS Safeguard Policy Statement DoF Department of Forests EA Environmental Assessment -

Province Wise Provisional Results of Census - 2017

PROVINCE WISE PROVISIONAL RESULTS OF CENSUS - 2017 ADMINISTRATIVE UNITS POPULATION 2017 POPULATION 1998 PAKISTAN 207,774,520 132,352,279 KHYBER PAKHTUNKHWA 30,523,371 17,743,645 FATA 5,001,676 3,176,331 PUNJAB 110,012,442 73,621,290 SINDH 47,886,051 30,439,893 BALOCHISTAN 12,344,408 6,565,885 ISLAMABAD 2,006,572 805,235 Note:- 1. Total Population includes all persons residing in the country including Afghans & other Aliens residing with the local population 2. Population does not include Afghan Refugees living in Refugee villages 1 PROVISIONAL CENSUS RESULTS -2017 KHYBER PAKHTUNKHWA District Tehsil POPULATION POPULATION ADMN. UNITS / AREA Sr.No Sr.No 2017 1998 KHYBER PAKHTUNKHWA 30,523,371 17,743,645 MALAKAND DIVISION 7,514,694 4,262,700 1 CHITRAL DISTRICT 447,362 318,689 1 Chitral Tehsil 278,122 184,874 2 Mastuj Tehsil 169,240 133,815 2 UPPER DIR DISTRICT 946,421 514,451 3 Dir Tehsil 439,577 235,324 4 *Shringal Tehsil 185,037 104,058 5 Wari Tehsil 321,807 175,069 3 LOWER DIR DISTRICT 1,435,917 779,056 6 Temergara Tehsil 520,738 290,849 7 *Adenzai Tehsil 317,504 168,830 8 *Lal Qilla Tehsil 219,067 129,305 9 *Samarbagh (Barwa) Tehsil 378,608 190,072 4 BUNER DISTRICT 897,319 506,048 10 Daggar/Buner Tehsil 355,692 197,120 11 *Gagra Tehsil 270,467 151,877 12 *Khado Khel Tehsil 118,185 69,812 13 *Mandanr Tehsil 152,975 87,239 5 SWAT DISTRICT 2,309,570 1,257,602 14 *Babuzai Tehsil (Swat) 599,040 321,995 15 *Bari Kot Tehsil 184,000 99,975 16 *Kabal Tehsil 420,374 244,142 17 Matta Tehsil 465,996 251,368 18 *Khawaza Khela Tehsil 265,571 141,193