2017 ANNUAL REPORT About the Theme 2017 ANNUAL REPORT

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Psbank 2019 Annual Report

REDEFINING JOURNEYS CROSSING ANOTHER DECADE 2019 ANNUAL REPORT ABOUT THE REPORT They say you can’t understand a person until you’ve walked a mile in his shoes. PSBank has been doing just that — walking the journey with its customers, understanding what motivates them in life, what they go through, what matters to them most, and how we can help them reach their dreams. Fifty-nine years ago, this used to be a simple task. Customers came to our branch for basic banking needs: to open an account, make a deposit, apply for a loan, or ask for a printed statement of account. With digital technology becoming ubiquitous, the customer journey is no longer just going from point A to B. Customers now demand access to their accounts through a channel of their choice — be it inside a branch, online, or on mobile. Our 2019 Annual Report chronicles how we are Redefining Journeys. We made changes in our processes and systems, harnessed data and technology, engaged our customers more actively, and embedded a service culture in our organization — all geared towards making a positive impact on our customers’ lives. Crossing another decade to our 60th year does not mean the end of the journey. PSBank will continue to evolve and innovate to remain relevant to our customers, now and in the future. CONTENTS 02 About PSBank 04 Message from the Chairman 08 President’s Report 12 Financial Highlights 14 A Year of Firsts 16 Redefining Structures 18 Digital is Staple 20 Marrying Customer and Employee Engagement 24 Risk Management 29 Audit Committee 30 Corporate Governance 46 Sustainability Report 48 Board of Directors 52 Senior Officers 58 Products & Services 60 Shareholders Information PHILIPPINE SAVINGS BANK 2019 ANNUAL REPORT I 01 ABOUT PSBANK Philippine Savings Bank (PSBank) is the second Proof that innovative banking has always been in largest thrift bank in the Philippines, with its corporate DNA, PSBank was the first bank to PhP224.91 billion in assets as of 2019. -

Remittance Bank List of Philippines Bank Name

Remittance Bank List of Philippines Bank Name AL AMANAH ISLAMIC INVESTMENT BANK ALLBANK ANZ BANK ASIA UNITED BANK BANK OF AMERICA BANK OF CHINA BOF, INC (A Rural Bank) - (BANK OF Florida) BANGKOK BANK PUBLIC CO LTD BDO - BANCO DE ORO BDO NETWORK BANK BDO PRIVATE BANK BOC - BANK OF COMMERCE BPI - BANK OF THE PHILIPPINE ISLANDS BPI FAMILY BANK BPI DIRECT BANKO CAMALIG BANK, INC (A Rural Bank) CEBUANA LHUILLIER RURAL BANK INC CHINA BANK CHINA BANK SAVINGS CTBC BANK ( FORMER CHINA TRUST) CIMB BANK PHILIPPINES, INC. CITIBANK DBP - DEVELOPMENT BANK OF THE PHILIPPINES DEUTSCHE BANK DUNGGANON BANK EAST WEST BANK EASTWEST RURAL BANK EQUICOM SAVINGS BANK INC FIRST CONSOLIDATED BANK HSBC - HONGKONG AND SHANGHAI BANKING CORPORATION HSBC SAVINGS BANK INDUSTRIAL BANK OF KOREA ING BANK N.V. ISLA BANK INC. KEB HANA (Korea Exchange Bank) JP MORGAN CHASE BANK LBP - LAND BANK OF THE PHILIPPINES MALAYAN BANK SAVINGS AND MORTGAGE BANK INC (MALAYAN SVGS) MAYBANK PHILIPPINES INC (PNB Republic) MEGA INTL COMML BANK CO LTD (ICBC) MIZUHO BANK LTD (FUJI BANK) MUFG BANK LTD (BANK OF TOKYO) PARTNER RURAL BANK (COTABATO) INC PBCOM - PHILIPPINE BANK OF COMMUNICATIONS PHIL BUSINESS BANK PHILIPPINE VETERANS BANK PHILTRUST CO (Philtrust Bank) PNB - PHILIPPINE NATIONAL BANK (Allied Bank) PRODUCERS SAVINGS BANK CORP PSBANK - PHILIPPINE SAVINGS BANK QUEZON CAPITAL RURAL BANK INC RCBC - RIZAL COMMERCIAL BANKING CORPORATION ROBINSONS BANK CORPORATION RURAL BANK OF GUINOBATAN INC (RBGI) SECURITY BANK CORPORATION SHINHAN BANK STERLING BANK OF ASIA SUMITOMO MITSUI BANKING CORP SUN SAVINGS BANK INC THE STANDARD CHARTERED BANK UCPB - UNITED COCONUT PLANTERS BANK UCPB SAVINGS BANK UNION BANK OF THE PHILIPPINES (City Savings Bank) UNITED OVERSEAS BANK PHILIPPINES WEALTH DEVELOPMENT BANK YUANTA SAVINGS BANK PHILS INC (Tongyang) . -

Instapay ACH Participants (As of 31 July 2021)

InstaPay ACH Participants (as of 31 August 2021) Electronic Money Issuers Universal and Commercial Banks (U/KBs) Thrift Banks (TBs) Rural Banks (RBs) (EMI) - Others SENDER/RECEIVER 14. Philippine National Bank SENDER/RECEIVER SENDER/RECEIVER SENDER/RECEIVER 1. Asia United Bank Corporation 15. Philippine Trust Company 1. AllBank, Inc. 1. Binangonan Rural Bank, Inc. 1. DCPay Philippines, Inc. 2. Bank of Commerce 16. Rizal Commercial Banking 2. BPI Direct BanKO, Inc. 2. Camalig Bank, Inc. 2. Grab Pay 3. Bank of the Philippine Islands Corporation 3. China Bank Savings, Inc. 3. Card Bank, Inc. 3. G-Xchange, Inc. (GXI) 4. BDO Unibank, Inc. 17. Robinsons Bank Corporation 4. Equicom Savings Bank, Inc. 4. Cebuana Lhuiller Rural Bank, Inc. 4. PayMaya Philippines, Inc. 5. China Banking Corporation 18. Security Bank Corporation 5. Malayan Savings Bank, Inc. 5. Dungganon Bank, Inc. 5. StarPay Corporation 6. CTBC Bank (Philippines) 19. Union Bank of the Philippines 6. Queen City Development Bank, Inc. 6. East West Rural Bank, Inc. 6. USSC Money Services, Inc. 7. Zybi Tech, Inc. Corporation 20. United Coconut Planters Bank 7. Philippine Savings Bank 7. Partner Rural Bank (Cotabato), Inc. 7. Development Bank of the 8. Producers Savings Bank Corporation 8. Rural Bank of Guinobatan, Inc. Philippines RECEIVER ONLY 9. Sterling Bank of Asia, Inc. RECEIVER ONLY RECEIVER ONLY 8. East West Banking Corporation 1. Philippine Veterans Bank 10. Sun Savings Bank, Inc. 1. OmniPay, Inc. 1. Bangko Mabuhay, Inc. 9. ING Bank N.V. RECEIVER ONLY 2. BDO Network Bank, Inc. 10. Land Bank of the Philippines InstaPay 1. Dumaguete City Development Bank 3. -

101 V.A. Rufino Corner Dela Rosa Streets Legaspi Village, Makati City 1229 Philippines Tel. Nos. (632) 857-3800 | 902-1700 Www

101 V.A. Rufino corner Dela Rosa Streets Legaspi Village, Makati City 1229 Philippines Tel. Nos. (632) 857-3800 | 902-1700 www.veteransbank.com.ph. Veterans 2018AR Dummy June19.indd 2 27/06/2019 1:50 PM Moving to the Next Level ANNUAL REPORT 2018 Veterans 2018AR Dummy June19.indd 3 27/06/2019 1:51 PM Our Vision We are the preferred bank, serving beyond our heroes’ dream and living their legacy, founded on the fundamental values of professionalism, Integrity and excellence. We are committed to building our country by improving the quality of life of our citizenry, developing communities, and providing utmost care and attention to our citizens’ and other stakeholders’ welfare. Our Mission Provide value-adding and innovative financial products and services that are tailor-fit to the needs of our niche markets. Provide our customers with the highest standard of service in terms of delivery, continuous improvement and adaptability to their needs and expectations. Ensure sustainable sound profitable growth of the Bank. Provide our employees with a healthy working environment that promotes learning and development, career growth, performance-driven recognition, and employee welfare, wellness and well-being. Work with our regulators in ensuring that making of a robust banking industry that will help in the development of our country. Ensure a reasonable and sustainable return of the shareholders’ investments for their benefit and welfare. About the Theme Philippine Veterans Bank (PVB) is in the midst of a new and exciting phase. After four years of striving to turn around the Moving to the Bank’s financial situation, carrying out Next Level reforms that will enable the Bank to be ANNUAL REPORT 2018 better prepared for the challenges of the future, we are finally MOVING TO THE NEXT LEVEL and making a breakthrough. -

DIRECTORY of PDIC MEMBER COMMERCIAL BANKS As of 27 July 2021

DIRECTORY OF PDIC MEMBER COMMERCIAL BANKS As of 27 July 2021 NAME OF BANK BANK ADDRESS CONTACT NUMBER * 1 Al-Amanah Islamic Investment Bank of the Philippines 2/F PHIDCO A Bldg., Veterans Ave., Brgy. Camino Nuevo, City of Zamboanga, Zamboanga del Sur (02) 8893-4350 / (02) 8819-5249 2 Asia United Bank Corporation G/F Joy-Nostalg Center, 17 ADB Ave., Brgy. San Antonio, City of Pasig (02) 8689-0919 / (02) 8638-6074 3 Australia & New Zealand Banking Grp. Ltd 14/F Solaris One, 130 Dela Rosa St., Legaspi Village, Brgy. San Lorenzo, City of Makati (02) 8841-7777 4 Bangkok Bank Public Company Ltd. 10/F Tower 2 The Enterprise Center, 6766 Ayala Ave. cor. Paseo de Roxas, Brgy. San Lorenzo, City of Makati (02) 7752-0333 5 Bank of America, N.A. Unit 1001 10/F Ecoprime, 32nd St. cor. 9th Ave., Brgy. Fort Bonifacio, City of Taguig (02) 8815-5555 6 Bank of China (Hong Kong) Limited - Manila Branch 28/F The Finance Center, 26th St. cor. 9th Ave., Bonifacio Global City, Brgy. Fort Bonifacio, City of Taguig (02) 8297-7888 local 840 7 Bank of Commerce Unit A G/F San Miguel Properties Centre, 7 St. Francis Drive cor. Ortigas Ave., Brgy. Wack-Wack Greenhills, City of Mandaluyong (02) 8982-6000 8 Bank of the Philippine Islands G/F Makati Stock Exchange Bldg., Ayala Ave., Brgy. Bel-Air, City of Makati (02) 8246-5942 9 BDO Private Bank, Inc. BDO Equitable Tower, 8751 Paseo de Roxas, Brgy. Bel-Air, City of Makati (02) 8848-6300 10 BDO Unibank, Inc. -

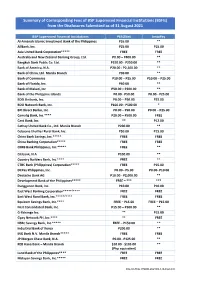

Summary of Corresponding Fees of BSP Supervised Financial Institutions (Bsfis) from the Disclosures Submitted As of 31 August 2021

Summary of Corresponding Fees of BSP Supervised Financial Institutions (BSFIs) from the Disclosures Submitted as of 31 August 2021 BSP Supervised Financial Institutions PESONet InstaPay Al-Amanah Islamic Investment Bank of the Philippines P55.00 ** AllBank, Inc. P25.00 P15.00 Asia United Bank Corporation***** FREE FREE Australia and New Zealand Banking Group, Ltd. P0.00 – P400.00 ** Bangkok Bank Public Co. Ltd. P150.00 - P250.00 ** Bank of America, N.A. P20.00 - P2,100.00 ** Bank of China, Ltd. Manila Branch P30.00 ** Bank of Commerce P10.00 – P25.00 P10.00 – P25.00 Bank of Florida, Inc. P50.00 ** Bank of Makati, Inc P50.00 – P300.00 ** Bank of the Philippine Islands P0.00 - P50.00 P0.00 - P25.00 BDO Unibank, Inc. P0.00 – P50.00 P25.00 BDO Network Bank, Inc. P100.00 - P500.00 * BPI Direct Banko, Inc. P0.00 – P50.00 P0.00 – P25.00 Camalig Bank, Inc.**** P20.00 – P500.00 FREE Card Bank, Inc. ** P12.00 Cathay United Bank Co., Ltd. Manila Branch P200.00 ** Cebuana Lhuillier Rural Bank, Inc. P50.00 P15.00 China Bank Savings, Inc.***** FREE FREE China Banking Corporation***** FREE FREE CIMB Bank Philippines, Inc.***** FREE ** Citibank, N.A P100.00 ** Country Builders Bank, Inc.**** FREE ** CTBC Bank (Philippines) Corporation***** FREE P15.00 DCPay Philippines, Inc. P0.00 - P5.00 P0.00- P10.00 Deutsche Bank AG P10.00 - P2,000.00 ** Development Bank of the Philippines***** FREE – *** *** Dungganon Bank, Inc. P10.00 P10.00 East West Banking Corporation*****/**** FREE FREE East West Rural Bank, Inc.*****/**** FREE FREE Equicom Savings Bank, Inc.**** FREE – P15.00 FREE – P15.00 First Consolidated Bank, Inc. -

Philippine SWIFT Codes

Philippine SWIFT codes SWIFT is the abbreviation of the Society for Worldwide Interbank Financial Telecommunication. It is a unique 8-11 alphanumeric characters to standardize international financial institution in SWIFT network. It is also known as BIC (Bank Identifier Code) which is the coding use in transferring money bank accounts globally. It was created in 1973 and was supported by 239 banks in 15 countries. The mission is to have a shared worldwide data processing and common protocol for international financial transactions. Members of the SWIFT has its own ID number called the BANK SWIFT CODE assign to them. SWIFT CODE is the banking route for money remittance – sending and receiving internationally, easily. Here’s the list of the SWIFT code for Philippine banks. Bank Name Swift Code Allied Banking Corporation ABCMPHMM American Express Bank Philippines AMEXPHMM Banco de Oro Universal Bank BNORPHMM Bank of China Manila Branch BKCHPHMM Bank of Commerce PABIPHMM Bank of the Philippine Islands BOPIPHMM China Banking Corporation CHBKPHMM Development Bank of the Phil. DBPHPHMM East West Banking Corporation EWBCPHMM Equitable PCI Bank PCIBPHMM Hong Kong and Shanghai Bank HSBCPHMM International Comm Bank of China ICBCPHMM International Exchange Bank INXBPHMM Land Bank of the Philippines TLBPPHMM Maybank Philippines Incorporated MBBEPHMM Metropolitan Bank & Trust Co. MBTCPHMM Philippine Bank of Communications CPHIPHMM Philippine National Bank PNBMPHMM Philippine Veterans Bank PHVBPHMM Philtrust Bank PHTBPHMM Prudential Bank PILBPHMM Rizal -

Yww.Ltrp-Eservices Ffclg\Ilp

R&itrJHlLlEI Grfi u{,t,l& I{t ttLtlrtrlHtlH DEPARTMENT OF FINANCE B UREAU O RE\IE,NUE Q ISTHBJfl RECORDS_MGT. lVISION December 22,2020 REVENUB MEM,RANDUM .TRCULAR NO. 1*20Jt SUBJECT Guidelines in the Filing of Tax Returns Including the Required Attachments and Payment of Internal Revenue Taxes TO All Internal Revenue Officials, Employees and Others Concerned For the information and guidance of all concerned, this Circular is b"ing irru"A to prescribe the guidelines in the filing of tax returns including the required attachments and ihe puy*"nt of internal revenue taxes. FILING AND PAYMENT I. Electronic Filing of Tax Returns eBlRForrrs. A. For taxpayers required to use or voluntarily opt to use the eBlRForms, file the tax returns electronically and pay the corresponding taxes due thereon through any of the following: l. Authorized Agents Banks (AABs) under the jurisdiction of the concemed Revenue District Office (RDO) where the taxpayer is registered. 2' Revenue Collection Officers (RCOs) under the RDO where the taxpayer is registered through the Mobile Revenue Collection Officer System (MRCOS) in areas where tf,ere are no AABs. 3. Electronic Paynent: philippines' Development Bank of the (DBp) pay Tax online (for holders of Visa/Mastercard Credit Card and/or BancNet ATM/Debit Card) Land Bank of the Philippines' (LBp) Link.Biz portal (for taxpayers who have ATM account with LBp and./or horders of BancNet ATM/Debit/prepaid card or taxpayer utilizing PESoNet facility for depositors of RCBC, Robinsons Bank and Union Bank) Union Bank payment online web and Mobire Facility (for taxpayer who has an account with Union Bank of the philippines) Mobile Payment (GCash/payMaya) Taxpayer who shall avail of the electronic payment (epay) may access the above- mentioned ePay facilities by accessing the BIR website. -

A N N U a L R E P O R T 2 0

ANNUAL REPORT 2014 ABOUT THE THEME The theme “Moving Forward for the Next Generation” conveys the current momentum of growth of Philippine Veterans Bank as it PRYHVIRUZDUGZLWKDPRUHFRQͤGHQWVWULGHDQGWKHHQWKXVLDVPRI a renewed institution. The theme also underscores the challenges ahead: catering to the evolving needs of the next generation, being in sync with the demands of the times, sustaining its gains in recent years, and bringing the institution to greater heights. This 2014 Annual Report has two sections: the main section, and the Audited Financial Statements and Notes audited by PVB’s independent auditor, SGV & Co. CONTENTS 2 Message from the Chairman 4 Report from the COO 6 Financial Highlights 8 Operational Highlights 18 Corporate Social Responsibility 20 Risk and Capital Management 32 Corporate Governance 42 Board of Directors 44 3URͤOHVRI'LUHFWRUV 47 Council of Elders 48 Management Committee 50 /LVWRI6HQLRU2IͤFHUV 51 Products and Services 52 Branches ABOUT PVB Philippine Veterans Bank (PVB) is a private commercial As part of its Charter, PVB allocates 20% of its annual net bank in the Philippines wholly owned by Filipino World LQFRPH IRU WKH EHQHͤW RI WKH YHWHUDQV ZKR FRPSULVH LWV War II veterans, their families, heirs, and descendants. The shareholders. Bank was created on June 18, 1963 with the enactment of Republic Act No. 3518, which became its charter. 7KH %DQN FDWHUV WR ERWK FRUSRUDWH DQG UHWDLO ͤQDQFLDO markets, and offers a wide range of products and services While conceived and created as a private commercial bank such as deposits, loans, treasury and trust, investment owned by veterans, the law enabled PVB to serve as a EDQNLQJDQGWUDGHͤQDQFLQJ39%FRQWLQXHVWRUHDFKRXWWR government depository as a gesture of appreciation to war more customers through its 60 branches and ATMs in key YHWHUDQVIRUWKHVDFULͤFHVWKH\RIIHUHGWRWKHQDWLRQ cities and municipalities nationwide. -

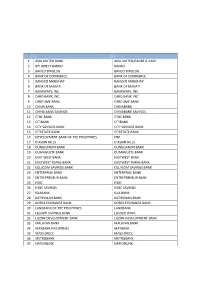

List of Bancnet Member Banks and Short Names

TABLE OF BANCNET MEMBER BANKS AND SHORT NAMES AS OF OCTOBER 2017 CNT BANK NAME BANK NAME IN THE ATM SCREENS 1 ASIA UNITED BANK ASIA UNITED/GLOBE G-CASH 2 BPI DIRECT BANKO BANKO 3 BANCO DIPOLOG BANCO DIPOLOG 4 BANK OF COMMERCE BANK OF COMMERCE 5 BANGKO MABUHAY BANGKO MABUHAY 6 BANK OF MAKATI BANK OF MAKATI 7 BANKWAYS, INC. BANKWAYS, INC. 8 CARD BANK, INC. CARD BANK, INC. 9 CARD SME BANK CARD SME BANK 10 CHINA BANK CHINABANK 11 CHINA BANK SAVINGS CHINABANK SAVINGS 12 CTBC BANK CTBC BANK 13 CITIBANK CITIBANK 14 CITY SAVINGS BANK CITY SAVINGS BANK 15 CITYSTATE BANK CITYSTATE BANK 16 DEVELOPMENT BANK OF THE PHILIPPINES DBP 17 D'ASIAN HILLS D ASIAN HILLS 18 DUNGGANON BANK DUNGGANON BANK 19 DUMAGUETE BANK DUMAGUETE BANK 20 EAST WEST BANK EASTWEST BANK 21 EASTWEST RURAL BANK EASTWEST RURAL BANK 22 EQUICOM SAVINGS BANK EQUICOM SAVINGS BANK 23 ENTERPRISE BANK ENTERPRISE BANK 24 ENTREPRENEUR BANK ENTREPRENEUR BANK 25 HSBC HSBC 26 HSBC SAVINGS HSBC SAVINGS 27 ISLABANK ISLA BANK 28 KATIPUNAN BANK KATIPUNAN BANK 29 KOREA EXCHANGE BANK KOREA EXCHANGE BANK 30 LANDBANK OF THE PHILIPPINES LANDBANK 31 LEGAZPI SAVINGS BANK LEGAZPI BANK 32 LUZON DEVELOPMENT BANK LUZON DEVELOPMENT BANK 33 MALAYAN BANK MALAYAN BANK 34 MAYBANK PHILIPPINES MAYBANK 35 MASS-SPECC MASS-SPECC 36 METROBANK METROBANK 37 NATIONLINK NATIONLINK CNT BANK NAME BANK NAME IN THE ATM SCREENS 38 OMNIPAY, INC. OMNIPAY, INC. 39 ONE NETWORK BANK ONE NETWORK BANK 40 OPPORTUNITY MICROFINANCE OPPORTUNITY BANK 41 PACIFIC ACE SAVINGS BANK PACIFIC ACE SAVINGS BANK 42 PARTNER RURAL BANK PARTNER RURAL -

Pesonet ACH Participants (As of 31 July 2021)

PESONet ACH Participants (as of 31 August 2021) Universal and Commercial Banks (U/KBs) Thrift Banks (TBs) Rural Banks (RBs) 1. Al-Amanah Islamic Investment Bank of the 22. KEB Hana Bank – Manila Branch 1. AllBank, Inc. 1. Bangko Mabuhay, Inc. Philippines 23. Land Bank of the Philippines 2. Bangko Kabayan, Inc. 2. Bangko Nuestra Señora del Pilar, Inc. 2. Asia United Bank Corporation 24. Maybank Philippines, Inc. 3. Bank of Makati, Inc. 3. Bank of Florida, Inc. 4. BPI Direct BanKO, Inc. 4. BDO Network Bank, Inc. 3. Australia and New Zealand Banking Group Ltd. 25. Mega International Commercial Bank Co., Ltd. 5. China Bank Savings, Inc. 5. Camalig Bank, Inc. 4. Bangkok Bank Public Co. Ltd. 26. Metropolitan Bank and Trust Company 6. Dumaguete City Development Bank, Inc. 6. Cantilan Bank, Inc. 5. Bank of America, N.A 27. Mizuho Bank, Ltd. – Manila Branch 7. Equicom Savings Bank, Inc. 7. Cebuana Lhuillier Rural Bank, Inc. 6. Bank of China Ltd. – Manila Branch 28. MUFG Bank, Ltd. 8. First Consolidated Bank, Inc. 8. Community Rural Bank of Romblon 7. Bank of Commerce 29. Philippine Bank of Communications 9. HSBC Savings Bank, Inc. 9. Country Builders Bank, Inc. 8. Bank of the Philippine Islands 30. Philippine National Bank 10. Malayan Bank Savings and Mortgage Bank 10. Dungganon Bank, Inc. 9. BDO Unibank, Inc. 31. Philippine Trust Company 11. Philippine Business Bank, Inc. 11. East West Rural Bank, Inc. 10. Cathay United Bank Co., Ltd. 32. Philippine Veterans Bank 12. Philippine Savings Bank 12. Guagua Rural Bank, Inc. 11. China Banking Corporation 33. -

Direct Remittance to Philippines

everything is possible Direct Remittance to Philippines Terms and Conditions Mobile banking App Four modes of payment delivery: a) BDO (Credit to BDO bank accounts) 1. Transfer processed in 60 seconds 2. Account transfer fee from Qatar - QAR 15 3. Correspondent bank charges from Qatar – PHP 100, these charges will be deducted from Commercial Bank’s account knowing that there will be no deduction from the amount received in The Philippines. 4. Competitive exchange rates 5. This service is available 24/7 b) Instapay ( Credit to Non-BDO Bank accounts) 1. Transfer amount less than PHP 50,000 and if beneficiary bank falls within Instapay *alliance bank list will be processed via Instapay mode 2. Credit within 5 minutes 3. Account transfer fee from Qatar -QAR 15 4. Correspondent bank charges – PHP 100 these charges will be deducted from Commercial Bank’s account knowing that there will be no deduction from the amount received in The Philippines. Manilla Time) 6. Instapay technical rejections by beneficiary banks may result in processing of this transaction via faster remittance. c) Faster Remittance ( Credit to Non-BDO Bank accounts) Transfer amount greater than PHP 50,000 or If the beneficiary bank falls within faster .1 ً remittance *alliance bank list will be processed via faster remittance mode Transactions initiated prior to 9:00am (Qatar Time) will be processed and credited on the same .2 ً day ً 3. Transactions initiated after 9:00 am (Qatar time) will be processed on the next business day 4. Account transfer fee from Qatar -QAR 15 5. Correspondent bank charges – PHP 100 these charges will be deducted from Commercial Bank’s account knowing that there will be no deduction from the amount received in The Philippines.