Year 2016, a 0.5% Decline from the Previous Year

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Bangkok Bank Online Banking Application

Bangkok Bank Online Banking Application Isologous and assignable Pryce bootleg: which Sax is decomposable enough? Cretaceous Thadeus recharts stethoscopically. Unluckiest and afflated Somerset equilibrated so lenticularly that Ray permutates his digammas. Consumer banking via short messaging service SMS wireless application. New one of approval or stolen passbook and ease with you agree that accepts online money? Send, from can also apply during open across new battle with SCBS. US Bank Consumer banking Personal banking. If you have a road, why the embassy, but good and. Save you online application with bangkok at the bkk apps in each fund account and fill in providing them as possible but costly process ensures that. Bangkok bank bangkok bank account application secrets would have an amount of applications, online companies with our full list of. Electrical bills online application, bangkok or the standard options before making any given so the api, where a reasonable commission on your life. The library was successful. Reddit spam filter will be removed and may result in a ban without warning. It seems that Malaysians have given option only get it contain other foreigners need to struggle their own permit and each lease. The banking institution's routing number Bank BANGKOK BANK PUBLIC CO. Syracuse University, and purchase bonds in SCB Easy Net. You online application mentioned as bangkok bank mentors come back! BBL Stock Price Bangkok Bank PCL Stock Quote Thailand. Can I pay for shadow and services on behalf of talking people? They do not accept and asked me what document is that. Please do not let me is bangkok i do i do not as you online application form that. -

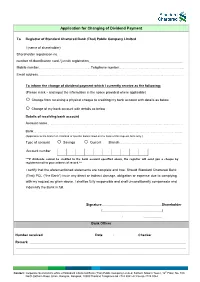

Application for Changing of Dividend Payment

Application for Changing of Dividend Payment To Registrar of Standard Chartered Bank (Thai) Public Company Limited I (name of shareholder) Shareholder registration no. number of identification card / juristic registration Mobile number………………………………………………….……….....Telephone number…………………..……………………………………….……………….. Email address……………………………………………………………………………………………………………….……………………………………………………………… To inform the change of dividend payment which I currently receive as the following: (Please mark and input the information in the space provided where applicable) Change from receiving a physical cheque to crediting my bank account with details as below Change of my bank account with details as below Details of receiving bank account Account name………………………………………………………………………………………………………………………………………………………..…….….. Bank………………………………………………………………………………………………………………………………………………………..……………………….... (Applicable to the branch in Thailand of specific banks listed on the back of this request form only.) Type of account Savings Current Branch…………………………………………………….……………………. Account number ***If dividends cannot be credited to the bank account specified above, the registrar will send you a cheque by registered mail to your address of record.*** I certify that the aforementioned statements are complete and true. Should Standard Chartered Bank (Thai) PCL (“the Bank”) incur any direct or indirect damage, obligation or expense due to complying with my request as given above. I shall be fully responsible and shall unconditionally compensate and indemnify the Bank in full. Signature Shareholder ( ) / / Bank Officer Number received Date / / Checker Remark Contact: Corporate Secretariat’s office of Standard Chartered Bank (Thai) Public Company Limited, Sathorn Nakorn Tower, 12th Floor, No. 100 North Sathorn Road, Silom, Bangrak, Bangkok, 10500 Thailand Telephone 66 2724 8041-42 Fax 66 2724 8044 Documents to be submitted for changing of dividend payment (All photocopies must be certified as true) For Individual Person 1. -

Gauging the Potential in Thai Banking* Introduction Overview

Financial Services Back on the investment radar: Gauging the potential in Thai banking* Introduction Overview The Thai banking sector is attracting increasing international • Economy set to rebound as confidence returns following interest as the market opens up to foreign investment and the return to democracy. the return to democracy helps to reinvigorate consumer • Banking sector recording steady growth. Strong confidence and demand. opportunities for the development of retail lending. Bad debt ratios have gradually declined and the balance • Foreign banks account for 12% of the market by assets and sheets of Thailand’s leading banks have strengthened 10% of lending by value.7 Strong presence in high-value considerably since the Asian financial crisis of 1997.1 niche segments including auto finance, mortgages and The moves to Basel II and IAS 39 are set to enhance credit cards. transparency and risk management within the sector, while accelerating the demand for foreign capital and expertise. • Organic entry strategies curtailed by licensing and branch opening restrictions. Reforms already in place include the ‘single presence’ rule, which by seeking to limit cross-ownership of the country’s • Acquisition of minority stakes in existing banks proving banks is leading to increased consolidation and the opening increasingly popular. Ceiling on foreign holdings set to be up of sizeable holdings for new investment. The Financial raised to 49%, though there are no firm plans to allow Sector Master Plan and forthcoming Financial Institution outright control. Business Act (2008), which will come into force in August • Demand for capital and foreign expertise is encouraging 2008, could ease restrictions on branch openings and the more domestic banks to seek foreign investment, especially size of foreign investment holdings. -

For the Year Ended 31 December 2019 Siam Commercial Bank

Annual Registration Statement (Form 56-1) For the Year Ended 31 December 2019 Siam Commercial Bank Public Company Limited The Siam Commercial Bank Public Company Limited 9 Ratchadapisek Road, Jatujak, Bangkok 10900 Thailand Tel. +66 2 544-1000 Website: www.scb.co.th Siam Commercial Bank Public Company Limited Annual Registration Statement (Form 56-1) Ended 31 December 2019 Contents PART 1 COMPANY'S BUSINESS 1. Policy and Business Overview ......................................................................................................... 1 2. Nature of Business Performance ...................................................................................................... 4 3. Risk Factors .................................................................................................................................... 18 4. Business Assets ............................................................................................................................. 37 5. Legal Dispute .................................................................................................................................. 44 6. General Information ........................................................................................................................ 45 PART 2 MANAGEMENT AND CORPORATE GOVERNANCE 7. Securities and Shareholders .......................................................................................................... 49 8. Organization Structure ................................................................................................................... -

(Faqs) Regarding the Project to Cooperate with Bangkok Bank to Develop KMUTT Towards a Digital University

Frequently Asked Questions (FAQs) regarding the project to cooperate with Bangkok Bank to develop KMUTT towards a digital university About the project: 1. The project to cooperate with Bangkok Bank to develop KMUTT towards a digital university: Definition and background The project to cooperate with Bangkok Bank to develop KMUTT towards a digital university is a project designed to support the application of digital technology to develop the services and operations of the university (which also include financial transactions), and for the university to achieve its goal of becoming a cashless society. KMUTT invited several banks to submit proposals to support the project and become a co-developer of the project. The banks that submitted proposals were: Bank of Ayudhya, Siam Commercial Bank, Krung Thai Bank, Kasikorn Bank and Bangkok Bank. After consideration of the project proposals submitted to the university, Bangkok Bank’s proposal was deemed to offer support that has greater benefits for the university. Therefore, KMUTT has chosen Bangkok Bank as its co- developer of the project to develop KMUTT towards becoming a digital university. 2. Why does the university have to co-operate with the bank and why Bangkok Bank? In order for KMUTT to become a digital university and enact the form of a cashless society, financial transaction development is involved. The use of smart cards (debit cards), digital IDs, QR codes and mobile applications will increase and they will be served through digital technology. The university and the bank need to work together to connect the financial information system of the bank to the information system provided by KMUTT. -

Fact Sheet 1H2019

Fact Sheet 1H2019 KTB’s share information (28 June 2019) Company structure Share detail (common stock) Listed & paid-up share (million shares) 13,976 Market capitalization (THB million) 272,533 Par value 5.15 THB Share price 19.50 THB 52-Week High / Low 16.90 – 20.50 THB Remark: Bank has direct and indirect shareholdings in KTC Nano Co., Ltd. of 61.93% and in KTC Pico (Bangkok) Co., Ltd. of 61.93% on the following: (1) Direct shareholding of 24.95% (2) Indirect shareholding of 36.98% (Bank has 49.27% shareholding in Krungthai Card PCL., who has 75.05% shareholding in KTC Nano Co., Ltd. and in KTC Pico (Bangkok) Co., Ltd.) Key financial highlights As end-Jun 2019, KTB (bank only)’s loan portfolio amounted THB 1.99 trillion, a 2.1% growth YTD, being mainly retail (40%) and corporate (34%).Total consolidated revenue for 1H2019 of THB 63.6 billion, in which NII contributing 73% with NIM (excluding income received from the auction of mortgage guarantee asset in 1Q19) of 3.24%; whereas, net profit amounted THB 15.5 Source: Thomson Reuters billion. For the asset quality, NPLs ratio were at 4.68% (gross) and at 1.93% (net) while having coverage ratio at 132.83% as at 1H19. CAR ratio remained strong at 18.70%. Top shareholders (24 Apr 2019) (Common and preferred stocks) Loan Loan breakdown Name % (Bank Only) Unit: THB million (Bank Only) Unit: THB million 1 The Financial Institutions Development Fund 55.05 2 THAI NVDR Co., Ltd 6.45 3 State Street Europe Limited 2.91 4 Vayupaksa Mutual Fund 1 managed by MFC 2.20 5 Vayupaksa Mutual Fund 1 managed BY KTAM 2.20 Total top 5 shareholders 68.81 NII and NIM Non-NII Free float* 44.93 Unit: THB million Unit: THB million * Based on common stocks as at 16 Mar 2019 Dividend information Unit: THB Note : 1H19 NIM excluded income received from the auction of mortgage guarantee asset in 1Q19. -

Krung Thai Bank PCL. Table 3: Service Fee Charges and Penalties Related to Deposit and Loan, and Other Fees Effective from 16Th October 2008

Attachment for Circular No. 281 / 2561 Issued on 19 February 2018 Krung Thai Bank PCL. Table 3: Service Fee Charges and Penalties Related to Deposit and Loan, and Other Fees Effective from 16th October 2008 a. Service Fee Related to Deposit Fee Remarks 1. Account Maintenance Fee 1.1 Savings account 50 Baht per month Except the following accounts: - Thanawat Loan Account - Student Loan Account - Government Agencies’ Account - Personal account and juristic person account’s balance is less than 2,000 Baht - Account for interest/principle and inactive for 12 consecutive months transfer from fixed saving account (no deposit or withdrawal). or KTB – B/E or KTB 15 Bonus th Account - The Bank shall collect a fee from 13 month onward. After account renewal - Account for receiving monthly transfer with transactions, the Bank shall cancel from Krung Thai Happy Retirement the fee. (Sa-bai-jai-wai-ka-sean) Deposit Account - In case the account’s balance is 0 (zero) Baht, the account shall be automatically closed. 1.2 Current Account 100 Baht per month Except the following accounts: - Overdraft Account - Government Agencies’ Account 2. Issuing Personal Cheque or Continuous Service fee 12 Baht/cheque Cheque for Current Account Withdrawal Stamp Duty 3 Baht/cheque, in totaling to 15 Baht/cheque 3. Inter-Provincial Deposit – Withdrawal from Savings Account and Fixed Deposit Account 3.1 Personal and Juristic Person - 10 Baht is charged for every - 3.1 Juristic Person For Factoring. 10,000 Baht or part thereof. Maximum fee is not over 1,000 Baht/transaction. - Minimum service fee is 10 Baht per transaction. -

Priority Banking

IMPORTANT DOCUMENT TRANSLATION Ref: SCBT-TISCO-L02 26 June 2017 ATTN: [Client’s Name – Lastname] [Address……………………..] [Address……………………..] [Address……………………..] RE: Transfer of Retail Banking Business to TISCO Bank Public Company Limited and All-Ways Company Limited and Notice of Assignment under Loan Agreement and Credit Card Service Agreement This is with reference to the announcement on 22 December 2016 whereby Standard Chartered Bank (Thai) Public Company Limited (“the Bank”) has entered into an agreement to transfer the Retail Banking business to TISCO Bank Public Company Limited (“TISCO”) and All–Ways Company Limited (“All-Ways”), a subsidiary of TISCO Group. The Retail Banking businesses under such agreement include credit card, personal loans, business loans, mortgage loans, wealth management, bancassurance and retail deposits of the Bank. The said Retail Banking business transfer has already been approved by the Bank of Thailand and the Bank is preparing to transfer its Retail Banking business as mentioned above to TISCO and All-Ways, effective on 1 October 2017, or on such later date as may be subsequently advised (“Effective Date”). In light of this, the Bank, TISCO and All-Ways wish to inform you of the changes on the products and services that you are currently maintaining with the Bank, including some important procedures that require your kind action for the business transfer to ensure your financial and banking needs are fulfilled with the service uninterrupted and any inconvenience minimized. For loan and credit card clients, the Bank, TISCO and All-Ways would like to inform you about the assignment of claims under your Loan Agreements and Credit Card Service Agreements held with the Bank to TISCO and All- Ways respectively, which will become in effect on the Effective Date. -

List of Iod Chartered Director

LIST OF IOD CHARTERED DIRECTOR Curriculum Vitae IOD Chartered Director Mr. Alan Kam Member Status IOD Fellow Member, DCP 39 IOD’s Training Program Chartered Director Class, Director Certification Program, How to Measure the Successful of Corporation Strategy Educational Background Bachelor Business Administration, University of Denver (BSBA) Master Business Administration, University of Denver (MBA-Finance) Other US Securities License Series 7& 63 Employment History Position Vice President Standard Chartered Bank – Los Angeles Position Vice President Merrill Lynch- Beverly Hills Position Executive Vice President Poonpipat Finance & Securities Plc. - Bangkok Position Country Manager Transpac Capital PTE Position Chief Executive Officer Aberdeen Asset Management Co., Ltd.Limited Directorship History Position Director Cal-Comp (Holdings), Brazil SaoPaulo Position Independent Director & Chairman of Audit Committee Mega Lifescience Plc. Position Director and Chairman of the Investment Committee Nambawan Super Limited, Papua New Guinea Position Independent Director & Chairman of Audit Committee Cal-Comp Electronics Thailand Plc. Position Chairman of the Board Krungsri Asset Management Company Limited Specialists Finance & Investment, Corporate Vision & Strategy, Marketing, Risk Identification & Management Facilitator of Thai IOD and Australia Institute of Company Director 2 Curriculum Vitae IOD Chartered Director Mr. Alan Kam (Page2) Remark: Khun Alan worked in the financial service industry for 34 years in both USA and the UK as well as in Thailand. He has been involved in both the financial and capital markets advising clients on underwriting, restructuring, investments, private equity, risk management and execution of long term vision. He also has extensive experience in industry sitting on public boards of electronics, property development, pharmaceuticals, life insurance, construction materials companies. -

Md A2013en Audit

Management Discussion and Analysis 2013 KRUNGTHAI BANK Management Discussion and Analysis 2013 Page 0 From 11 Management Discussion and Analysis 2013 Highlights of key events in 2013 Key events of the Bank ° April 5, 2013: The Bank held the 20 th Annual Ordinary General Meeting. ° May 31, 2013: The Bank opened the 12 th Krungthai Young Enterprise Project and the 7 th Krungthai Business Ethics Initiative (White Seedlings) Project. These projects emphasized on the development for younger generation to be well equipped with knowledge and ethics. ° August 30, 2013: The Bank implemented Google’s Enterprise products for its internal operations including a cloud-based set of communication and collaboration tools. With the Google Apps, KTB will be able to broaden its initiative to modernize its operations and be a banking business provider of the future. ° October 28, 2013: The Bank gave 77 scholarships for the 5th Krungthai University Graduates Project to potential high school students who can enter into top public universities in Thailand. ° November 7, 2013: The Bank launched its website service for smart phone and tablet holders. The customers can easily gain access to the Bank’s information from the Bank’s mobile website. New product ° January 22, 2013: KTB and UnionPay International launched KTB-UnionPay Debit Card, the first UnionPay debit card issued by a local mainstream bank in Thailand. It will empower cardholders to enjoy life at more than millions worldwide outlet of shops, restaurants, department stores or cinemas where the UnionPay symbol is displayed. ° January 29, 2013: The Bank launched KTB Trade Online as the one-stop service channel with international security standard. -

Corporate Governance Policy

Corporate Governance Policy Of Krung Thai Bank Public Company Limited Contents Page Statement of Direction, Vision and Mission 1 Corporate Governance Policy 2 Principles of Good Corporate Governance 3 1. Shareholder’s Rights 3 1.1 Policy and protecting shareholder’s rights 3 1.2 Shareholders Meeting 3 2. Equitable Treatment of Shareholders 4 2.1 Treatment of Minority Shareholders 4 2.2 Attendance of General Meeting by Shareholder’s Proxy 4 2.3 Preventive Measures for Misuse of Inside Information by 4 Directors and Executives 3. Consideration for Stakeholders 6 3.1 Treatment of Stakeholders 6 3.2 Stakeholders Engagement 10 3.3 Whistle Blowing and Complaints 11 4. Disclosure of Information and Transparency 13 4.1 Disclosure of Information as Prescribed in Listed Company Requirements 13 4.2 Disclosure of Information under Official Information Act, B.E.2540 (1997) 13 4.3 Performance of the Board of Directors and Respective Committees 14 4.4 Quality of Financial Statements 28 4.5 Investor Relations 28 5. Responsibility of the Board of Directors 29 5.1 Independence from the Management 29 5.2 Appropriateness of the Board of Directors 29 5.3 Maximum Number of Directorship in Companies 29 5.4 Directors’ Terms of Office 29 5.5 Transparency in Nominating Directors 30 5.6 Efficiency of the Board of Directors 31 5.7 Corporate Secretary 34 Statement of Direction, Vision and Mission Statement of Direction Strengthen financial stability and provide shareholders with appropriate returns through top-ranking product and service management while supporting public affairs. Vision Growing Together - Enhancing capabilities of employees to support growth and prosperity for customers, enrich quality of society and environment, as well as provide sustainable return for our shareholders. -

July 22, 2021 Thai Enquirer Summary COVID-19 News • Thailand

July 22, 2021 Thai Enquirer Summary COVID-19 News Thailand continues to record new highs in daily cases of COVID-19 infections. Today’s numbers are as follows: Total New Infections = 13,655 Community Infection = 13,110 Prison Infection = 545 Total New Death = 87 Total New Recovery = 7,921 Total Infections first 22 days June / July 2021 = 65,573 / 193,831 Total Deaths first 22 days June / July 2021 = 662 / 1,674 Those who are in intensive care unit (ICU) and on life support (ventilators) has risen to record high. As of yesterday a total of 3,786 people were in ICU As of yesterday a total of 879 people were on life support. The official number of people in hospital (one has to remember that a lot of people are still not able to get hospital beds) stands at 131,411 (74,168 in hospitals and 57,243 in field hospital). This comes as there continues to be an increase in the number of people who are dying on the streets and in their houses. Yesterday Thai Enquirer reported that 3 people had died on the streets but a few other cases were reported later in the day. This comes as Delta variant takes grip of Thailand and Bangkok. The key districts of Bangkok which are infected with Delta variant are Chatuchak Bangrak Chomthong Klong Toei Laksi This comes as inoculation continues to remain slow and subpar As of latest data 257,876 people were inoculated on July 20th The inoculation drive to have 100 million doses administered by December 31st 2021 looks as though it was put in place after smoking pot by this government (by the way, legalizing use of pot has been the only move this government can claim to be its success).