A Guide to the Capital Budget

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

2018-2019 Voter Analysis Report

20182019 VOTER ANALYSIS REPORT APRIL 2019 NEW YORK CITY CAMPAIGN FINANCE BOARD Board Chair Frederick P. Schaffer Board Members Gregory T. Camp Richard J. Davis Marianne Spraggins Naomi B. Zauderer Amy M. Loprest Executive Director Roberta Maria Baldini Assistant Executive Director for Campaign Finance Administration Kitty Chan Chief of Staff Daniel Cho Assistant Executive Director for Candidate Guidance and Policy Eric Friedman Assistant Executive Director for Public Affairs Hillary Weisman General Counsel THE VOTER ASSISTANCE ADVISORY COMMITTEE VAAC Chair Naomi B. Zauderer Members Daniele Gerard Joan P. Gibbs Okwudiri Onyedum Arnaldo Segarra Mazeda Akter Uddin Jumaane Williams New York City Public Advocate (Ex-Officio) Michael Ryan Executive Director, New York City Board of Elections (Ex-Officio) The VAAC advises the CFB on voter engagement and recommends legislative and administrative changes to improve NYC elections. 2018–2019 VOTER ANALYSIS REPORT TEAM Lead Editor Gina Chung, Production Editor Lead Writer and Data Analyst Katherine Garrity, Policy and Data Research Analyst Design and Layout Winnie Ng, Art Director Jennifer Sepso, Designer Maps Jaime Anno, Data Manager WELCOME FROM THE VOTER ASSISTANCE ADVISORY COMMITTEE In this report, we take a look back at the past year and the accomplishments and challenges we experienced in our efforts to engage New Yorkers in their elections. Most excitingly, voter turnout and registration rates among New Yorkers rose significantly in 2018 for the first time since 2002, with voters turning out in record- breaking numbers for one of the most dramatic midterm elections in recent memory. Below is a list of our top findings, which we discuss in detail in this report: 1. -

The City Record

1993 VOLUME CXLVIII NUMBER 47 THURSDAY, MARCH 11, 2021 Price: $4.00 Design and Construction . 1998 District Attorney - New York County �������� 1998 THE CITY RECORD TABLE OF CONTENTS Procurement and Contract BILL DE BLASIO Mayor Management. 1998 PUBLIC HEARINGS AND MEETINGS LISETTE CAMILO Education ���������������������������������������������������� 1999 Borough President - Brooklyn . 1993 Commissioner, Department of Citywide Contracts and Purchasing . 1999 Administrative Services City Planning Commission ������������������������ 1994 Housing Authority �������������������������������������� 1999 JANAE C. FERREIRA Community Boards . 1995 Procurement ���������������������������������������������� 1999 Editor, The City Record Housing Authority �������������������������������������� 1995 Information Technology and Published Monday through Friday except legal Housing Preservation and Development . 1996 holidays by the New York City Department of Telecommunications . 2000 Citywide Administrative Services under Authority Independent Budget Office ������������������������ 1996 Infrastructure �������������������������������������������� 2000 of Section 1066 of the New York City Charter. Landmarks Preservation Commission . 1996 Parks and Recreation . 2000 Subscription $500 a year, $4.00 daily ($5.00 by mail). Periodicals Postage Paid at New York, NY PROPERTY DISPOSITION Revenue and Concessions . 2000 POSTMASTER: Send address changes to THE CITY RECORD, 1 Centre Street, Citywide Administrative Services . 1997 Small Business Services ���������������������������� -

Local Government Primer

LOCAL GOVERNMENT PRIMER Alaska Municipal League Alaskan Local Government Primer Alaska Municipal League The Alaska Municipal League (AML) is a voluntary, Table of Contents nonprofit, nonpartisan, statewide organization of 163 cities, boroughs, and unified municipalities, Purpose of Primer............ Page 3 representing over 97 percent of Alaska's residents. Originally organized in 1950, the League of Alaska Cities............................Pages 4-5 Cities became the Alaska Municipal League in 1962 when boroughs joined the League. Boroughs......................Pages 6-9 The mission of the Alaska Municipal League is to: Senior Tax Exemption......Page 10 1. Represent the unified voice of Alaska's local Revenue Sharing.............Page 11 governments to successfully influence state and federal decision making. 2. Build consensus and partnerships to address Alaska's Challenges, and Important Local Government Facts: 3. Provide training and joint services to strengthen ♦ Mill rates are calculated by directing the Alaska's local governments. governing body to determine the budget requirements and identifying all revenue sources. Alaska Conference of Mayors After the budget amount is reduced by subtracting revenue sources, the residual is the amount ACoM is the parent organization of the Alaska Mu- required to be raised by the property tax.That nicipal League. The ACoM and AML work together amount is divided by the total assessed value and to form a municipal consensus on statewide and the result is identified as a “mill rate”. A “mill” is federal issues facing Alaskan local governments. 1/1000 of a dollar, so the mill rate simply states the amount of tax to be charged per $1,000 of The purpose of the Alaska Conference of Mayors assessed value. -

Capitalist Crisis and the Rise of Monetarism

CAPITALIST CRISIS AND THE RISE OF MONETARISM Simon Clarke What is the significance of 'monetarism' for an understanding of the relationship between the economy and the capitalist state? Before we can address the question we have to try to define 'monetarism'. In the strictest sense 'monetarism' refers to the advocacy of the quantity theory of money and a policy preoccupation with the growth of the money supply. In this sense monetarism expresses a pre-Keynesian ortho- doxy, that has been perpetuated by a few cranks and that inexplicably grabbed the hearts and minds of economists and politicians for the best part of a decade, between 1975 and 1985. This is the view that has tended to be taken by economists who remain committed to a Keynesian analysis. For these economists monetarism was a combination of huckstering and collective madness that led to mistaken economic policies. The response to monetarism was to keep faith and wait until normal sanity was resumed. Such a view has apparently now been vindicated by the almost universal abandonment of this kind of monetarist orthodoxy, although elements of its rhetoric remain. This is to take much too narrow a view of monetarism. Although this narrow monetarism has been utterly discredited, and the money supply no longer has the fetishistic significance that it briefly enjoyed, the broader contours of the politics and ideology of monetarism remain with us, and have been assimilated by many of those of a Keynesian persuasion. This politics and ideology relates not so much to the narrow technical issues of monetary policy and the control of the money supply as to the broader questions of the relations between the state and the economy. -

Council-Manager Form of Government

OVERVIEW OF CITY ORGANIZATION COUNCIL-MANAGER FORM OF GOVERNMENT Dallas’ government has changed and grown - from a mayor and six aldermen, to a commission with a mayor and four commissioners elected at-large, to the present council-manager system that has been in place since 1931. Originally, the council was composed of nine members and the mayor, who was elected by council vote. In 1951, the eight council members and mayor were all elected at- large. The structure changed again in 1968 to 10 council members and the mayor, who were all elected at-large, but eight council members represented specific districts. Later, in 1979, eight council members were elected from single-member districts with two council members and the mayor elected at-large. Our current system began in 1991 with 14 council members elected from single-member districts and a mayor elected at-large. The mayor is elected for four years, and council members are elected for two-year terms. Council members can serve up to four consecutive two-year terms. A mayor’s term is limited to two consecutive four-year terms. Council-manager government combines citizen input-through elected council members- with the professional training and experience of a city manager. The City’s organization under this plan is similar to that of a corporation. The mayor and city council serve as the equivalent of a board of directors. They set the public agenda, adopt policy and laws and appoint the city manager, city auditor, city attorney, and city secretary. In Dallas, the manager oversees City operations with an executive team of assistant city managers, each responsible for various departments. -

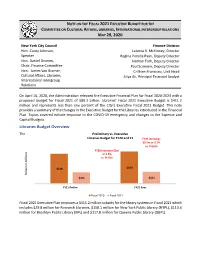

Libraries Budget Overview MAY 29,2020

NOTE ON THE FISCAL 2021 EXECUTIVE BUDGET FOR THE COMMITTEE ON CULTURAL AFFAIRS, LIBRARIES, INTERNATIONAL INTERGROUP RELATIONS MAY 29, 2020 New York City Council Finance Division Hon. Corey Johnson, Latonia R. McKinney, Director Speaker Regina Poreda Ryan, Deputy Director Hon. Daniel Dromm, Nathan Toth, Deputy Director Chair, Finance Committee Paul Scimone, Deputy Director Hon. James Van Bramer, Crilhien Francisco, Unit Head Cultural Affairs, Libraries, Aliya Ali, Principal Financial Analyst International Intergroup Relations On April 16, 2020, the Administration released the Executive Financial Plan for Fiscal 2020-2024 with a proposed budget for Fiscal 2021 of $89.3 billion. Libraries’ Fiscal 2021 Executive Budget is $411.2 million and represents less than one percent of the City’s Executive Fiscal 2021 Budget. This note provides a summary of the changes in the Executive Budget for the Libraries introduced in the Financial Plan. Topics covered include response to the COVID-19 emergency and changes to the Expense and Capital Budgets. Libraries Budget Overview The Preliminary vs. Executive Libraries Budget for FY20 and 21 FY21 increases $0.5m or 0.1% vs. Prelim FY20 increases $2m or 0.5% vs. Prelim $428 $430 Dollars in Millions $411 $411 FY21 Prelim FY21 Exec Fiscal 2020 Fiscal 2021 Fiscal 2021 Executive Plan proposes a $411.2 million subsidy for the library systems in Fiscal 2021 which includes $29.8 million for Research Libraries, $150.1 million for New York Public Library (NYPL), $113.4 million for Brooklyn Public Library (BPL) and $117.8 million for Queens Public Library (QBPL). $410.7 Million Executive Plan $411.2 Million Fiscal 2021 Changes Fiscal 2021 Executive Preliminary • Research Libraries: • New Needs: None • Research Libraries: $30.1M • Other Adjustments: $29.9M • NYPL: $149.6M 458,000 • NYPL: $150.1M • BPL: $113.2M • PEGs: None • BPL: $113.4M • QBPL: $117.8M • QBPL: $117.8M Changes introduced in the Executive Plan increase the Libraries budget for Fiscal 2021 by $500,000. -

The Council of the City of New York Office of Council Member Antonio

The Council of the City of New York Office of Council Member Antonio Reynoso 250 Broadway, Suite 1740 NY, New York 10007 May 10th, 2018 Press Release For Immediate Release Kristina Naplatarski [email protected] (347) 581-2050 (C) (212) 788-7095 (O) Council Member Reynoso, East Brooklyn Congregations, and Metro IAF Call Upon the de Blasio Administration to Build More Affordable Senior Housing on Unutilized NYCHA Land May 10th, 2018 —Bushwick, NY— Today, New York City Council Member Antonio Reynoso in conjunction with East Brooklyn Congregations and Metro IAF called upon the de Blasio administration to build more affordable senior housing on vacant NYCHA land. In Mayor Bill de Blasio’s 2014 “Housing New York” plan, the administration promised to increase the supply of housing for seniors by reaching 15,000 households through a combined effort of new construction and preservation. In 2017, the administration doubled this effort, aiming to serve 30,000 units over an extended 12 year period. The administration has made progress towards this goal; several sites throughout the city, including a vacant lot in NYCHA’s Bushwick II campus, are currently in the RFP process and have stipulations for minimum residential senior units. Community members and elected officials called upon the administration to deliver on its promised targets by utilizing additional vacant NYCHA lots throughout the City. However, they stressed that these lots should be dedicated to the construction of deeply affordable and senior targeted units. In light of our City’s rapidly aging population, it is more crucial than ever that we invest in affordable senior housing. -

New York City Council Districts and Asian Communities (2018)

New York City Council Districts and Asian Communities (2018) 25, which includes Jackson Heights, Queens; District 38 encompassing Sunset Park, Brooklyn; and As our City Council starts this new term with 11 Introduction District 24, which include parts of Jamaica, Queens. new members and 40 returning members, the Asian American Federation has compiled data from Almost three in four Asian New Yorkers are the 2015 American Community Survey (ACS) on the immigrants. Overall, 26 percent of all immigrants Asian populations for each of the City Council citywide are Asians. Council District 20 has the Districts.1 We will highlight the growth in each highest percent of Asian immigrants among all district’s Asian population and highlight the Asian immigrant populations, accounting for 79 percent languages most commonly spoken in each district. of all immigrants in the district. District 1 has the second largest Asian immigrant population, with 66 percent of all immigrants, followed by District 23 at 60 percent; District 19 at 54 percent; District 38 at The Asian population continues to be the fastest Overall Asian Population 51 percent; and District 43 at 48 percent. growing major race and ethnic group in New York City. According to the most recent Census Bureau As Asian immigrants and their families become population estimates, the Asian population in New more established, they have become a growing part York City reached 1.23 million in 2015, accounting of the potential voter base, comprising 11 percent for nearly 15 percent of the city’s population. of the total voting-age citizen population in New York City. -

Washington Heights Community Directory

Washington Heights Community Resource Directory New York State Psychiatric Institute Center of Excellence for Cultural Competence May 2008 Community Profile: Washington Heights and Inwood A survey of New York City residents found that people who report having significant emotional distress are more likely to engage in unhealthy behaviors, such as getting no exercise, binge drinking, smoking, and eating a poor diet. Similarly, New Yorkers with significant emotional distress experience high rates of chronic illness, such as high cholesterol, high blood pressure, obesity, asthma, and diabetes. An added difficulty is that neighborhoods in New York with the lowest incomes often have the highest rates of significant emotional distress, often adding to the burden on these already underserved communities (New York City Department of Health and Mental Hygiene, 2003). The New York City Department of Health and Mental Hygiene (DOHMH) has conducted a number of community health surveys to assess the health and well-being of New Yorkers. Here, we present some of the factors important to the physical and mental health of the communities of Washington Heights and Inwood, to serve as background for the services listed in this directory. Washington Heights and Inwood: The population of Inwood and Washington Heights (I/WH) at the 2000 census was 270,700. More than half of the residents of these communities (51%) were born outside the United States, compared to 36% for New York City as a whole. Figure 1 shows the countries of origin for foreign-born members of Community District 12 (which is made up of Inwood and Washington Heights), while Table 1 lists foreign-born residents by country of origin. -

Capital City Downtown Community Revitalization Levy – Revised Boundary and Revenue Forecasts

6. 2. That Mayor S. Mandel, on behalf of Capital City City Council, make an application to 2 the Provincial Government Downtown requesting designation of the Capital City Downtown Community Community Revitalization Levy in a regulation. Revitalization Levy Report Revised Boundary and Revenue Forecasts On October 17, 2012, Administration provided a Downtown Arena Update to City Council that included information Recommendations: clarifying the application of a Community Revitalization Levy to fund specific City- 1. That the revised proposed boundary led Catalyst Projects, including the of the Capital City Downtown arena and related infrastructure. Community Revitalization Levy area as shown in Attachment 1 of the Administration indicated that it was not March 5, 2013, Sustainable the intent to dedicate any increase in Development report 2013SHE012, municipal and education property tax be approved. revenue that would accrue naturally 2. That Mayor S. Mandel, on behalf of through the appreciation of already City Council, send a revised existing fully developed property to pay application to the Provincial for Catalyst projects. The presentation Government requesting designation pointed out that the increase in revenue of the Capital City Downtown that is generated by the inflationary Community Revitalization Levy by appreciation of existing properties is way of regulation. essential to the City’s ability to continue to deliver programs and services to the Report Summary entire City. This report provides an update on progress towards completion of the Administration has been engaged in Capital City Downtown Community discussions with the Province about the Revitalization Levy and provides proposed Capital City Downtown direction on the next steps. -

M E M O R a N D

M EMORANDUM To: City Council; City Manager From: Mary A. Winters, City Attorney; Elizabeth Oshel, Associate City Attorney Re: Drawing Voting Districts Date: June 6, 2017 QUESTION What are the legal requirements for drawing voting districts in the city of Bend? ANSWER The City is bound by the U.S. Constitution, federal Voting Rights Act, and Oregon law in determining how to draw any wards or districts for election of city councilors. Cities may set their own rules for electing their city councils, and drawing districts, because Art. XI, § 2 of the Oregon constitution gives the legal voters of every city power to enact and adopt their own charters, through the home rule provisions of the Oregon Constitution. The City must follow the Oregon Secretary of State’s directive in creating or redrawing voting districts. Traditional principles of districting such as equal population, compactness, and contiguity should be the primary considerations. The racial composition of districts should be considered only if necessary to comply with the Voting Rights Act. 1. Principles of Districting and Oregon State Law Traditional districting principles should be used to draw voting districts. First, districts must be drawn with the goal of equal population. An equal population goal “is a background rule” underlying all other considerations in drawing electoral maps. ATTORNEY CLIENT PRIVILEGE Page | 1 Alabama Legislative Black Caucus v. Alabama, __ US __, 125 SCt 1257, 1271 (2015). In addition to equal population, traditional principles of districting include: Compactness, contiguity, respect for political subdivisions or communities defined by actual shared interests, incumbency protection, and political affiliation. -

Inside Money, Business Cycle, and Bank Capital Requirements

Inside Money, Business Cycle, and Bank Capital Requirements Jaevin Park∗y April 13, 2018 Abstract A search theoretical model is constructed to study bank capital requirements in a respect of inside money. In the model bank liabilities, backed by bank assets, are useful for exchange, while bank capital is not. When the supply of bank liabilities is not sufficiently large for the trading demand, banks do not issue bank capital in competitive equilibrium. This equilibrium allocation can be suboptimal when the bank assets are exposed to the aggregate risk. Specifically, a pecuniary externality is generated because banks do not internalize the impact of issuing inside money on the asset prices in general equilibrium. Imposing a pro-cyclical capital requirement can improve the welfare by raising the price of bank assets in both states. Key Words: constrained inefficiency, pecuniary externality, limited commitment JEL Codes: E42, E58 ∗Department of Economics, The University of Mississippi. E-mail: [email protected] yI am greatly indebted to Stephen Williamson for his continuous support and guidance. I am thankful to John Conlon for his dedicated advice on this paper. This paper has also benefited from the comments of Gaetano Antinolfi, Costas Azariadis and participants at Board of Governors of the Federal Reserve System, Korean Development Institute, The University of Mississippi, Washington University in St. Louis, and 2015 Mid-West Macro Conference at Purdue University. All errors are mine. 1 1 Introduction Why do we need to impose capital requirements to banks? If needed, should it be pro- cyclical or counter-cyclical? A conventional rationale for bank capital requirements is based on deposit insurance: Banks tend to take too much risk under this safety net, so bank capital requirements are needed to correct the moral hazard problem created by deposit insurance.