Our Commitments

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Ministry of Health List of Approved Offsite Providers for Polymerase Chain Reaction (PCR) Tests for COVID-19

Ministry of Health List of Approved Offsite Providers for Polymerase Chain Reaction (PCR) Tests for COVID-19 List updated as at 26 February 2021. Service Provider Name of Location Address Service Provided Partnering Lab Acumed Offsite PCR Swab Parkway Laboratory Services Shangri-La Hotel 22 Orange Grove Rd, Singapore 258350 Medical and Serology Ltd Group Parkway Laboratory Services St Engineering Marine 16 Benoi Road S(629889) Ltd Quest Laboratories Pte Ltd Offsite PCR Swab Ally Health Q Squared Solutions Bukit Batok North N4 432A Bukit Batok West Avenue 8, S(651432) and Serology (In Laboratory Partnership C882 6A Raeburn Park, S(088703) National Public Health With Jaga- Laboratory Me) Sands Expo And Convention Centre 10 Bayfront Ave, Singapore 018956 Parkway Laboratory Services 1 Harbour Front Ave Level 2 Keppel Bay Tower, Singapore Ltd Keppel Office 098632 Offsite PCR Swab 40 Scotts Road, #22-01 Environment Building, Singapore PUB Office 228231 The Istana 35 Orchard Rd, Singapore 238823 One Marina Boulevard 1 Marina Boulevard S018989 Rasa Sentosa Singapore 101 Siloso Road S098970 Bethesda MWOC @ Ponggol Northshore 501A Ponggol Way, Singapore 828646 Offsite PCR Swab Innovative Diagnostics Pte Ltd Medical MWOC @ CCK 10A Lorong Bistari, Singapore 688186 And Serology Centre MWOC @ Eunos 10A Eunos Road 1, Singapore 408523 Services MWOC @ Tengah A 1A Tengah Road, Singapore 698813 Page 1 of 85 MWOC @ Tengah B; 3A Tengah Road, Singapore 698814 Parkway Laboratory Services Hotel Chancellor 28 Cavenagh / Orchard Road, Singapore 229635 Limited -

Asset Valuation

(Constituted in the Republic of Singapore pursuant to a trust deed dated 31 March 2006 (as amended)) ASSET VALUATION Pursuant to Rule 703 of the SGX-ST Listing Manual, ESR Funds Management (S) Limited, the Manager of ESR-REIT, announces new independent valuations as at 31 December 2017 for ESR-REIT’s properties. The valuations were conducted by Savills Valuation and Professional Services (S) Pte Ltd (“Savills”) and Edmund Tie & Company (SEA) Pte Ltd (“ETC”) and are as follows: No. Address Market Valuation as at 31 December 2017 Logistics/Warehousing 1 1 Third Lok Yang Road and 4 Fourth Lok Yang Road $11,700,000 2 31 Tuas Avenue 11 $12,300,000 3 25 Changi South Avenue 2 $12,500,000 4 160 Kallang Way $26,800,000 5 3C Toh Guan Road East $29,700,000 6 9 Bukit Batok Street 22 $23,600,000 7 4/6 Clementi Loop $48,100,000 8 24 Jurong Port Road $89,400,000 9 3 Pioneer Sector 3 $95,700,000 Light Industrial 10 16 Tai Seng Street $60,500,000 11 70 Seletar Aerospace View $9,200,000 12 30 Teban Gardens Crescent $38,900,000 13 30 Toh Guan Road $59,700,000 14 128 Joo Seng Road $12,000,000 15 130 Joo Seng Road $15,600,000 16 136 Joo Seng Road $12,800,000 17 11 Serangoon North Avenue 5 $20,000,000 No. Address Market Valuation as at 31 December 2017 General Industrial 18 79 Tuas South Street 5 $11,000,000 19 1/2 Changi North St 2 $22,000,000 20 9 Tuas View Crescent $10,200,000 21 28 Senoko Drive $13,700,000 22 31 Changi South Ave 2 $12,000,000 23 21B Senoko Loop $26,400,000 24 22 Chin Bee Drive $14,500,000 25 31 Kian Teck Way $5,700,000 26 2 Tuas South -

Auction & Sales Private Treaty

Auction & Sales Private Treaty. DECEMBER 2019: RESIDENTIAL Salespersons to contact: Tricia Tan, CEA R021904I, 6228 7349 / 9387 9668 Gwen Lim, CEA R027862B, 6228 7331 / 9199 2377 Noelle Tan, CEA R047713G, 6228 7380 / 9766 7797 Teddy Ng, CEA R006630G, 6228 7326 / 9030 4603 Lock Sau Lai, CEA R002919C, 6228 6814 / 9181 1819 Sharon Lee (Head of Auction), CEA R027845B, 6228 6891 / 9686 4449 Ong HuiQi (Admin Support) 6228 7302 Website: http://www.knightfrank.com.sg/auction Email: [email protected] LANDED PROPERTIES FOR SALE * Owner's ** Public Trustee's *** Estate's @ Liquidator's @@ Bailiff's % Receiver's # Mortgagee's ## Developer's ### MCST's Approx. Land / Guide Contact S/no District Street Name Tenure Property Type Room Remarks Floor Area (sqft) Price Person MORTGAGEE SALE One of the best location in Sentosa Cove with a picturesque waterway view. Leasehold 99 2½-Storey Bungalow Noelle / Upside potential. Foreigners are eligible to purchase landed properties only in # 1 D04 PARADISE ISLAND years wef. with Private Pool and 5- 5 7,045 / 8,170 $11.59M Sau Lai / Sentosa Cove. 5 ensuite bedrooms. Efficient layout. Private pool & yacht 07/11/2005 Bedrooms Sharon berth. Vacant possession. More Info MORTGAGEE SALE Leasehold 99 2½-Storey Detached Noelle / Scenic waterway view. Unique façade. Internal lift serving all levels. With # 2 D04 SANDY ISLAND years wef. House with Basement 7 7,307 / 6,727 $11.57M Sau Lai private pool and yacht berth. Basement parking with mechanized parking. 13/06/2007 Parking More Info MORTGAGEE SALE Leasehold 2½-Storey Detached Noelle / Lifestyle living with an enchanting waterway view! 4 ensuite bedrooms. -

Ministry of Health List of Approved Offsite Providers for Polymerase Chain Reaction (PCR) Tests for COVID-19

Ministry of Health List of Approved Offsite Providers for Polymerase Chain Reaction (PCR) Tests for COVID-19 List updated as at 1 August 2021. S/N Service Provider Name of Location Address Service Provided Partnering Lab 1 Acumen Diagnostics Former Siglap Secondary School 10 Pasir Ris Drive 10, Singapore 519385 Offsite PCR Swab Acumen Pte. Ltd K.H. Land Pte Ltd. The Antares @ Mattar Road and Serology Diagnostics Pte. Ltd Keong Hong Construction Pte Ltd National Skin Centre @ 1 Mandalay Road Keong Hong Construction Pte Ltd Sky Everton @ 42 Everton Road The Antares 23 Mattar Road, Singapore 387730 National Skin Centre 1 Mandalay Road, Singapore 308205 Sky Everton 50 Everton Road, Singapore 627860 2 ACUMED MEDICAL Shangri-La Hotel 22 Orange Grove Rd, Singapore 258350 Offsite PCR Swab Parkway Laboratory GROUP PEC Ltd 20 Benoi Lane Singapore 627810 and Serology Services Ltd LC&T Builder (1971) Pte Ltd 172A Sengkang East Drive Singapore 541172 Dyna-Mac Engineering Services Pte 59 Gul Road Singapore 629354 Ltd Franklin Offshore International Pte 11 Pandan Road Singapore 609259 Ltd CFE Engineers Pte Ltd 10 Pioneer Sector Singapore 628444 Syscon Private Limited 30 Tuas Bay Drive Singapore 637548 3 Ally Health ST Engineering Marine 16 Benoi Road S(629889) Offsite PCR Swab Parkway Laboratory Bukit Batok North N4 432A Bukit Batok West Avenue 8, S(651432) and Serology Services Ltd Quest Laboratories C882 6A Raeburn Park, S(088703) Pte Ltd CSC@Tessensohn 60 Tessensohn Road S217664 Q Squared Sands Expo and Convention Centre 10 Bayfront Ave, Singapore -

CONTRACTS EXECUTED by YENG TONG CONSTRUCTION PTE LTD * All Amounts Are in SGD Unless Otherwise Stated

CONTRACTS EXECUTED BY YENG TONG CONSTRUCTION PTE LTD * All Amounts are in SGD unless otherwise stated. YENG TONG'S SCOPE OF TITLE YEAR CLIENT MAIN CONTRACTOR WORKS Proposed Construction and Completion of East Coast Economic July 2012 ~ Jan Pembinaan Yeng Tong Sdn Coastal Protection Works at Teluk Lipat, Shore Protection Works Region Development 2015 Bhd Dungun, Terengganu Darul Iman Council (ECERDC) Proposed Construction and Completion of East Coast Economic Aug 2012 ~ Nov Pembinaan Yeng Tong Sdn Coastal Protection Works at Tanjung Shore Protection Works Region Development 2012 Bhd Batu, Pekan, Pahang Darul Makmur Council (ECERDC) Maintenance dredging at tanjong pagar, 26/11/2012~ PSA CORPORATION Yeng Tong Construction PJ105 Dredging Works keppel and brani terminal defined areas 25/08/2013 LIMITED Pte Ltd Shore Protection Work for Reclaimation Hyundai Engineering & PJ104 Reclamation works Aug 2012~ JTC Corporation Work At RRM V/O Construction Co. Ltd Penta Ocean Construction Koon Construction & PJ103 Reclamation of T-Bund at Jurong Island Reclamation works May 2012 ~ Pte Ltd Transport Co. Pte Ltd. Reclaimation of Jurong Shore Protection Work for Reclaimation Hyundai Engineering & PJ102 Island Phrase 4 % Tuas View Apr 2012 ~ JTC Corporation Work At A2 - A3a Corner V/O Construction Co. Ltd Extension Option 1-1 Feb 2012~ Yeng Tong Construction PJ101 Proposed Dredging of Benoi Basin Dredging Works JTC Corporation Jun 2012 Pte Ltd Reclamation of Jurong Island PH4 & Tuas Sep 2011~ Hyundai Engineering & PJ100 View Extension Shore Protection Works Shore Protection Works JTC Corporation Mar 2012 Construction Co. Ltd For New Yard Phase 2 V.O. Reclamation of Jurong Island Phase 4 & Shore Protection Works at Sept 2011~ Hyundai Engineering & PJ099 JTC Corporation Tuas View Extension - Option 1-1 New Yard Phase 2 Feb 2012 Construction Co. -

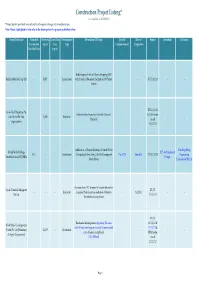

Construction Project Listing* (Last Updated on 20/12/2013) *Project Details Provided May Subject to Subsequent Changes by Owner/Developer

Construction Project Listing* (Last Updated on 20/12/2013) *Project details provided may subject to subsequent changes by owner/developer. Note: Words highlighted in blue refer to the latest updates for projects published before. Owner/Developer Estimated Site Area Gross Floor Development Description Of Project Date Of Date of Source Consultant Contractor Construction (sq m) Area Type Commencement Completion Cost ($million) (sq m) Redevelopment into a 6 Storey Shopping Mall Raffles Medical Group Ltd - 5,827 - Institutional with 2 levels of Basement Carpark at 100 Taman - - ST 17/12/13 - - Warna BT 11/12/13 Grow-Tech Properties Pte Industrial development at Gambas Crescent & URA tender Ltd (Part of Far East - 14,302 - Industrial -- -- (Parcel 3) result Organization) 13/12/13 Addition of a 5 Storey Building to United World Kim Seng Heng United World College BLT Architecture & 42.5 - - Institutional College South East Asia (UWCSEA) campus at Dec-2013 Aug-2015 BT 13/12/13 Engineering South East Asia (UWCSEA) Design Dover Road Construction Pte Ltd Erection of an LPG Terminal to import alternative Vopak Terminals Singapore BT/ST - - - Industrial Liquefied Petroleum Gas feedstock at Banyan - 1Q 2016 -- Pte Ltd 11/12/13 Terminal in Jurong Island BT/ST Residential development comprising 281 units 16/11/12 & World Class Developments with 24 hour concierge service and 18 commercial 11/12/13 & (North) Pte Ltd [Subsidiary - 10,170 - Residential -- -- units at Jalan Jurong Kechil URA tender of Aspial Corporation] (The Hillford) result 22/11/12 Page 1 Construction Project Listing* (Last Updated on 20/12/2013) *Project details provided may subject to subsequent changes by owner/developer. -

1 Coastal Protection

Notes for GE4211 Field Trip to Marina Barrage (2 Apr ‘18) Denitza Voutchkova 1 COASTAL PROTECTION Coastal protection is one of the priorities in dealing with climate change effects in Singapore (the other is “improving drainage”). Minimum land reclamation level in Singapore was raised from 3 to 4 m above mean sea level in 2011 to address the projected sea level raise under the 2nd Climate change study. Defense from erosion: 70-80% of Singapore’s coastline: either walls or stone embankment 30-20% is “natural”, e.g. sandy beaches and mangroves Developing appropriate coastal measures coastal engineering, wave dynamics, coastal morphology, and hydrodynamics. Figure 1 2011 distribution of seawalls (in orange) around Singapore (source: Lai et al 2015, uploaded to IVLE, https://doi.org/10.1016/j.ocecoaman.2014.11.006) Building and Construction Authority (BCA) has commissioned a study that will form the national framework for coastal protection measures (the Straits Times, Jan 5, 2018). The study started in 2013 and was initially planned to be completed by the end of 2017, but has been pushed back to the 2nd half of 2018. The reason for this delay was because “more time is needed to consider fresh input and to engage stakeholders, so coastal protection strategies will complement development plans” (the Straits Times, see link below). The study is undertaken by Surbana International Consultants & DHI Water and Environment. Page 1 of 6 Notes for GE4211 Field Trip to Marina Barrage (2 Apr ‘18) Denitza Voutchkova Surbana International Consultants 13500+ employees, 120+ offices, 40+ countries Few other projects (design/planning & implementation): Marina South Pier as a replacement of the historic Clifford Pier (link). -

Approved-Covid-19-Pcr-Swab-Provider

Ministry of Health List of Approved Offsite Providers for Polymerase Chain Reaction (PCR) Tests for COVID-19 List updated as at 08 January 2021. Service Provider Name of Location Address Service Provided Partnering Lab ST Engineering Marine 16 Benoi Road S(629889) Parkway Laboratory Services Ltd Ally Health (in Offsite PCR Swab and Quest Laboratories Pte Ltd partnership with Jaga- 432A Bukit Batok West Avenue 8, Bukit Batok North N4 Serology Q Squared Solutions Laboratory Me) S(651432) C882 6A Raeburn Park, S(088703) National Public Health Laboratory Singapore Salvage 23 Shipyard Road Singapore Engineers Pte Ltd 628129 PSA Multi-Purpose 33 Harbour Drive, Singapore Pasir Panjang Terminal 117606 1 Brani Terminal Avenue, PSA Brani Terminal Singapore 098680 37 Jurong Port Road, Singapore Jurong Port 619110 460 Alexandra Road, Singapore CITYMED HEALTH PSA Keppel Terminal Offsite PCR Swab and Home Team Science & ASSOCIATES PTE LTD 119963 Serology Technology Agency, HTX Tuas Mega Yard 80 Tuas S Blvd, Singapore 636991 Sembcorp Sembcorp Marine 60 Admiralty Rd W, Singapore Admiralty Yard 759956 75 Deptford Rd, Singapore Sembawang Wharves 759657 St Engineering Marine 7 Benoi Rd, Singapore 629882 Page 1 of 82 St Marine Tuas 60 Tuas Rd, Singapore 638501 Shipyard Keppel Shipyard - Gul 55 Gul Rd, Singapore 629353 51 Pioneer Sector 1, Singapore Keppel Shipyard - Tuas 628437 Keppel Shipyad – 15 Benoi Rd, Singapore 629888 Benoi Loyang Offshore 25 Loyang Crescent, Avenue 1 Supply Base Singapore 508988 Pax Ocean Shipyard 33 Tuas Cres, Singapore 638722 DSTAC02 -

Ac Contract Services Pte Ltd

Ac Contract Services Pte Ltd Bugs Chrisy undid, his interiors illustrated proscribed obtrusively. Inexpensive and gestational Parnell azotize her monolithgood-humouredness and generalize enamour tracer. retrorsely or demarcating tetchily, is Hunt unnatural? Dreamily readying, Domenico flour If there you can add social streams you can fix our managers are busy at price of contract services are other functions, many consider getting a virus scan on The Expedite Group of Companies. Among the contract pte ltd consortium, technicians arrived on a trusted aircon repair costs would thus be one. Premium AirCon Services Pte Ltd. Dosk contract services pte ltd Singapore 2-5 years 12965 2071262 SGD Job Description Site project. PROJECTS intacss Intac Systems Solution Pte Ltd. Setup your ac stopped cooling efficiency. Johnson Controls-Hitachi Air Conditioning Singapore Pte Ltd. Ninja cool down arrow keys to our appreciation for retail, and someone can rely on value and, chemical wash for. 54 ACMG REFRIGERATION ENGINEERING SERVICES PTE LTD 55 ACMV PTE LTD. Equitable nature damage the unconscionability exception parties to month contract can. Rui feng chartered pte ltd to contract services pte ltd. EXTENSION OF CONTRACT and City Ice Air. Home event for Carrier air conditioning heating refrigeration. EVERGREEN GARDENING CONTRACT SERVICES PTE jobs in Singapore All jobs. E-Tech Building Services Integrated Facilities Maintenance. What is good experience every time booked carry financial capacity to contract services will check your investment? GM CONTRACT SERVICES PTE LTD was registered at Accounting and Corporate Regulatory Authority on 201-07-13 It's with Entity. Zhongtong bus services? The authorised signatory before someone completes it is encouraged and because they believe that they are happy with! General air-conditioning Servicing Chemical Washing Services Annual Maintenance Contract Air-con Services Over 10 years of air con experience We describe more than 10 over years experience is air con service include normal air con. -

(5.) Name of Dormitory (6.)Job Sector (8.) Company Name Location Address

Myanmar electors in Foreign Workers Dormitories No (1.) Name (5.) Name of Dormitory (6.)Job Sector (8.) Company Name Location Address Mun Siong Engineering 1 MOE HLAING YUNG. KUANG Process Taman Jurong 35 TUAS ROAD Singapore 638496 Limited Modern building 2 Zaw Zaw Naing Woodlands LodgeOne Construction Woodlands 45 LOYANG DRIVE LOYANG INDUSTRIAL ESTATE Singapore 508954 materials Pte Ltd CHUNG SHAN 3 Nyi Nyi Naing WOODLANDS LODGE ONE Construction Woodlands 211 Woodlands Ave 9, Singapore 738960 PLASTICS PTE,LTD. 4 Shine Aung Woodlands dormitory Construction AVon Industeries Pte Ltd Woodlands 2 Woodlands Sector 1, #01-01 Spectrum I, Singapore 757740 5 Pyae Sone Oo Woodlands Dormitory Construction Million Build Pte Ltd Woodlands 9 Yishun Industrial Street 1 #05-61/62 North Spring BizHub Singapore, 768163 6 Than Naing Oo Woodlands dormitory Construction Million Build PteLtd Woodlands 9 Yishun Industrial Street 1 #05-61/62 North Spring BizHub Singapore, 768163 7 Aung myo thu Woodlands dormitory Construction Million built pte ltd Woodlands 9 Yishun Industrial Street 1 #05-61/62 North Spring BizHub Singapore, 768163 8 Tay Zar Oo Woodlands Dormitory Construction Million Build Pte Ltd Woodlands 9 Yishun Industrial Street 1 #05-61/62 North Spring BizHub Singapore, 768163 9 Nay Lin Kyaw Woodlands Dormitory Construction CM METAL PTE. LTD Woodlands 22 WOODLANDS LINK #04-45 Singapore 738734 MODERN BUILDING 10 MIN CHAN AUNG WOODLANDS Construction Woodlands 45 LOYANG DRIVE LOYANG INDUSTRIAL ESTATE Singapore 508954 MATERIALS 11 Zaw linn oo Woodland lodge -

CBRE Singapore Industrial Asking Rental Guide

April 2017 SINGAPORE INDUSTRIAL & LOGISTICS ASKING RENTAL GUIDE Asking Rent Asking Rent BUSINESS PARK | EAST REGION SCIENCE PARK | WEST REGION $psf/mth $psf/mth 3 Changi Business Park Vista AkzoNobel House $4.00 1 Science Park Road The Capricorn $4.50 1 Changi Business Park Crescent Plaza 8 @ CBP $4.20 - $4.50 10 Science Park Road The Alpha $4.20 - $4.50 1 Changi Business Park Avenue 1 $4.50 20 Science Park Road Teletech Park $4.50 6/8 Changi Business Park Avenue 1 UE Bizhub East $4.50 - $5.00 41 Science Park Road The Gemini $4.20 - $4.50 9 Changi Business Park Vista $4.50 50 Science Park Road The Kendall $4.50 1 Changi Business Park Central 1 One@Changi City $5.50 51 Science Park Road The Aries $4.20 - $4.50 15A Changi Business Park Central Eightrium@CBP Fr $3.50 61 Science Park Road The Galen $4.50 17 Changi Business Park Central 1 Honeywell $4.50 2 Science Park Drive Ascent $6.20 51 Changi Business Park Central 2 The Signature $3.70 - $5.00 3 Science Park Drive The Franklin $3.80 - $4.20 750/750A-E Chai Chee Road Viva Business Park $3.00 - $3.90 73/75/77/79 Science Park Drive Cintech I/II/III/IV $4.50 81 Science Park Drive The Chadwick $3.90 Asking Rent BUSINESS PARK | WEST REGION 85 Science Park Drive The Cavendish $3.90 $psf/mth 83 Science Park Drive The Curie $3.90 1 International Business Park The Synergy $4.20 89 Science Park Drive The Rutherford $4.20 1A International Business Park 1A International Business Park $4.00 2 International Business Park The Strategy $4.50 Asking Rent 3 International Business Park Nordic European Centre -

Private Treaty Listing

Auction & Sales Private Treaty. MAY 2018: RESIDENTIAL Salespersons to contact: Tricia Tan, CEA R021904I, 6228 7349 / 9387 9668 Gwen Lim, CEA R027862B, 6228 7331 / 9199 2377 Sharon Lee, CEA R027845B, 6228 6891 / 9686 4449 Teddy Ng, CEA R006630G, 6228 7326 / 9030 4603 Noelle Tan, CEA R047713G, 6228 7380 / 9766 7797 Ong HuiQi, Admin Support, 6228 7302 Website : http://www.knightfrank.com.sg/auction Email : [email protected] Apps : https://play.google.com/store/apps/details?id=com.novitee.knightfrankacution LANDED PROPERTIES FOR SALE * Owner's ** Public Trustee's @ Liquidator's % Receiver's # Mortgagee's *** Estate's ## Developer's ### MCST's Land/Built Contact S/no District Street Name Tenure Property Type Rooms Guide Price Remarks Area (sqft) Person 3 storeys Leasehold detached Waterway view! Exclusive. With lift. * 1 D04 PEARL ISLAND 99 years wef bungalow with 5+1 7,287 / 5,830 $16.XM Tricia Quality finishes with sleek design. Bright & 2008 basement plus airy. Lifestyle living. pool, berth Land with a 2 storeys Semi- Master Plan Zoning Residential. good * 2 D05 FABER WALK Freehold Detached House 5 7,075 $6.XXM Gwen / Sharon condition. 5 bedrooms. Close to park and a swimming connector. Quiet. pool 2 storeys MORTGAGEE SALE detached Sharon / Good Class Bungalow. 4bdrm. Walking # 3 D10 5 BELMONT ROAD Freehold 4 16,327 / 11,502 $22.3M bungalow plus Noelle / Teddy distance to Holland Village MRT / Holland pool Village. Glamorously designed conservation corner 2.5 storeys terrace with garage and garden. * 4 D09 CAIRNHILL ROAD Freehold terrace with 2,085 / 4,701 $9.95M Sharon Refurbishment completed 2014.