Monetary Policy in Postwar Years

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

On the Classification of Economic Fluctuations

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Explorations in Economic Research, Volume 2, number 2 Volume Author/Editor: NBER Volume Publisher: NBER Volume URL: http://www.nber.org/books/moor75-2 Publication Date: 1975 Chapter Title: On the Classification of Economic Fluctuations Chapter Author: John R. Meyer, Daniel H. Weinberg Chapter URL: http://www.nber.org/chapters/c7408 Chapter pages in book: (p. 43 - 78) Moo5 2 'fl the 'if at fir JOHN R. MEYER National Bureau of Economic on, Research and Harvard (Jriiversity drawfi 'Ces DANIEL H. WEINBERG National Bureau of Economic iliOns Research and'ale University 'Clical Ihit onth Economic orith On the Classification of 1975 0 Fluctuations and ABSTRACT:Attempts to classify economic fluctuations havehistori- cally focused mainly on the identification of turning points,that is, so-called peaks and troughs. In this paper we report on anexperimen- tal use of multivariate discriminant analysis to determine afour-phase classification of the business cycle, using quarterly andmonthly U.S. economic data for 1947-1973. Specifically, weattempted to discrimi- nate between phases of (1) recession, (2) recovery, (3)demand-pull, and (4) stagflation. Using these techniques, we wereable to identify two complete four-phase cycles in the p'stwarperiod: 1949 through 1953 and 1960 through 1969. ¶ As a furher test,extrapolations were made to periods occurring before February 1947 andalter September 1973. Using annual data for the period 1926 -1951, a"backcasting" to the prewar U.S. economy suggests that the n.ajordifference between prewar and postwar business cycles isthe onii:sion of the stagflation phase in the former. -

Information to Users

INFORMATION TO USERS This manuscript has been reproduced from the microfilm master. UMI films the text directly from the original or copy submitted. Thus, som e thesis and dissertation copies are in typewriter face, while others may be from any type of computer printer. The quality of this reproduction is dependent upon the quality of the copy submitted. Broken or indistinct print, colored or poor quality illustrations and photographs, print bleedthrough, substandard margins, and improper alignment can adversely affect reproduction. In the unlikely event that the author did not send UMI a complete manuscript and there are missing pages, these will be noted. Also, if unauthorized copyright material had to be removed, a note will indicate the deletion. Oversize materials (e.g., maps, drawings, charts) are reproduced by sectioning the original, beginning at the upper left-hand corner and continuing from left to right in equal sections with small overlaps. Photographs included in the original manuscript have been reproduced xerographically in this copy. Higher quality 6” x 9” black and white photographic prints are available for any photographs or illustrations appearing in this copy for an additional charge. Contact UMI directly to order. ProQuest Information and Learning 300 North Zeeb Road, Ann Arbor, Ml 48106-1346 USA 800-521-0600 ____ ® UMI BEFORE THE GREAT SOCIETY: LIBERALISM, DEINDUSTRIALIZATION AND AREA REDEVELOPMENT IN THE UNITED STATES, 1933 - 1965 DISSERTATION Presented in Partial Fulfillment of the Requirements for the Degree Doctor of Philosophy in the Graduate School of The Ohio State University By Gregory S. Wilson, M.A. ***** The Ohio State University 2001 Dissertation Committee: Approved by Professor William R. -

Down Market Battle Plan

The Shape of Recovery: What’s Next? Panelists Leon LaBrecque Matt Pullar JD, CPA, CFP®, CFA Vice President, Private Client Chief Growth Officer Services 248.918.5905 216.774.1192 [email protected] [email protected] 2 As an independent financial services firm, our About Sequoia salaried, non-commission professionals have Financial Group access to a variety of solutions and resources and our recommendations are based solely on what works best for you, not us. 3 1. What are we monitoring? 2. What are we hearing from our Financial investment partners? Market Update 3. What are we recommending? 4 COVID-19: U.S. Confirmed Cases and Fatalities S o urce: Johns Hopkins CSSE, J.P. Morgan Asset Management. Guide to the Markets – U.S. Data are as of June 30, 2020. 5 Consumer Sentiment Index S o urce: CONSSENT Index (University of Michigan Consumer Sentiment Index) Copyright 2020 Bloomberg Finance L.P. 17-Jul-2020 6 COVID-19: Fatalities S o urce – New York Times https://static01.nyt.com/images/2020/0 7/20/multimedia/20-MORNING- 7DAYDEATHS/20-MORNING- 7DAYDEATHS-articleLarge.png 7 High-Frequency Economic Activity S o urce: Apple Inc., FlightRadar24, Mortgage Bankers Association (MBA), OpenTable, STR, Transportation Security Administration (TSA), J.P. Morgan Asset Management. *Driving directions and total global flights are 7- day moving averages and are compared to a pre-pandemic baseline. Guide to the Markets – U.S. Data are as of June 30, 2020. 8 S&P 500 Index at Inflection Points S o urce: Compustat, FactSet, Federal Reserve, Standard & Poor’s, J.P. -

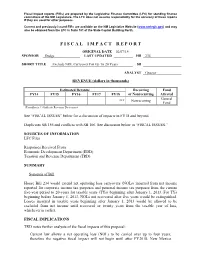

F I S C a L I M P a C T R E P O

Fiscal impact reports (FIRs) are prepared by the Legislative Finance Committee (LFC) for standing finance committees of the NM Legislature. The LFC does not assume responsibility for the accuracy of these reports if they are used for other purposes. Current and previously issued FIRs are available on the NM Legislative Website (www.nmlegis.gov) and may also be obtained from the LFC in Suite 101 of the State Capitol Building North. F I S C A L I M P A C T R E P O R T ORIGINAL DATE 02/07/14 SPONSOR Dodge LAST UPDATED HB 234 SHORT TITLE Exclude NOL Carryover For Up To 20 Years SB ANALYST Graeser REVENUE (dollars in thousands) Estimated Revenue Recurring Fund FY14 FY15 FY16 FY17 FY18 or Nonrecurring Affected General *** Nonrecurring Fund (Parenthesis ( ) Indicate Revenue Decreases) See “FISCAL ISSUES” below for a discussion of impacts in FY18 and beyond. Duplicates SB 156 and conflicts with SB 106. See discussion below in “FISCAL ISSUES.” SOURCES OF INFORMATION LFC Files Responses Received From Economic Development Department (EDD) Taxation and Revenue Department (TRD) SUMMARY Synopsis of Bill House Bill 234 would extend net operating loss carryovers (NOLs) incurred from net income reported for corporate income tax purposes and personal income tax purposes from the current five-year period to 20-years for taxable years (TYs) beginning after January 1, 2013. For TYs beginning before January 1, 2013, NOLs not recovered after five years would be extinguished. Losses incurred in taxable years beginning after January 1, 2013 would be allowed to be excluded from net income until recovered or twenty years from the taxable year of loss, whichever is earlier. -

Simon Kuznets and the Empirical Tradition in Economics

This PDF is a selection from a published volume from the National Bureau of Economic Research Volume Title: Political Arithmetic: Simon Kuznets and the Empirical Tradition in Economics Volume Author/Editor: Robert William Fogel, Enid M. Fogel, Mark Guglielmo, and Nathaniel Grotte Volume Publisher: University of Chicago Press Volume ISBN: 0-226-25661-8, 978-0-226-25661-0 (cloth) Volume URL: http://www.nber.org/books/foge12-1 Conference Date: n/a Publication Date: March 2013 Chapter Title: The Emergence of National Income Accounting as a Tool of Economic Policy Chapter Author(s): Robert William Fogel, Enid M. Fogel, Mark Guglielmo, Nathaniel Grotte Chapter URL: http://www.nber.org/chapters/c12915 Chapter pages in book: (p. 49 - 64) 3 :: The Emergence of National Income Accounting as a Tool of Economic Policy Herbert Hoover was sworn in as president at the end of a decade of generally vigorous economic growth, marred by the deep but short recession of 1920–21. By March 1929, the economy was near the top of a vigorous boom. In his inaugural address, Hoover was lyrical in his vision of American prosperity: “Ours is a land rich in resources; stimulating in its glorious beauty; fi lled with millions of happy homes; blessed with comforts and opportunity. In no nation are the institu- tions of progress more advanced. In no nation are the fruits of accom- plishment more secure. In no nation is the government more worthy of respect. No country is more loved by its people. I have an abiding faith in their capacity, integrity, and high purpose. -

Nominal GDP Targeting for a Speedier Economic Recovery

Munich Personal RePEc Archive Nominal GDP targeting for a speedier economic recovery Eagle, David M. Eastern Washington University 8 March 2012 Online at https://mpra.ub.uni-muenchen.de/39821/ MPRA Paper No. 39821, posted 04 Jul 2012 12:20 UTC Nominal GDP Targeting for a Speedier Economic Recovery By David Eagle Associate Professor of Finance Eastern Washington University Email: [email protected] Phone: (509) 828-1228 Abstract: For U.S. recessions since 1948, we study paneled time series of (i) ExUR, the excess of the unemployment rate over the prerecession rate, and (ii) NGAP, the percent deviation of nominal GDP from its prerecession trend. Excluding the 1969-70 and 1973-75 recessions, a regression of ExUR on current and past values of NGAP has an R2 of 75%. Simulations indicate that NGDP targeting could have eliminated 84% of the average ExUR during the period from 1.5 years and 4 years after the recessions began. The maximum effect of NGAP on unemployment occurs with a lag of 2 to 3 quarters. Revised: March 8, 2012 © Copyright 2012, by David Eagle. All rights reserved. Nominal GDP Targeting for a Speedier Economic Recovery By David Eagle “Major institution change occurs only at times of crisis. … I hope no crises will occur that will necessitate a drastic change in domestic monetary institutions. … Yet, it would be burying one’s head in the sand to fail to recognize that such a development is a real possibility. … If it does, the best way to cut it short, to minimize the harm it would do, is to be ready not with Band-Aids but with a real cure for the basic illness.” Milton Friedman, 1984 Figure 1. -

Karl Brunner and Allan Meltzer

Karl Brunner and Allan Meltzer: From Monetary Policy to Monetary History to Monetary Rules* Prepared for the Conference “Karl Brunner and Monetarism” Swiss National Bank, Zurich, Switzerland, October 29-30, 2018 Michael D Bordo Rutgers University, Hoover Institution, and NBER Economics Working Paper 19104 HOOVER INSTITUTION 434 GALVEZ MALL STANFORD UNIVERSITY STANFORD, CA 94305-6010 March 1, 2019 Karl Brunner and Allan Meltzer were pioneer monetarists whose work in the 1960s and 1970s challenged the prevailing Keynesian orthodoxy. A major part of their work was a critique of the Federal Reserve System’s monetary policy strategy from the 50s leading to the Great inflation. This paper explores the nexus between Brunner and Meltzer’s earlier work in a report prepared for the US congress in 1964 on the System’s discretionary counter cyclical policy in its first fifty years of existence, and Allan Meltzer’s monumental two volume A History of the Federal Reserve (2003, 2009). Many of the themes in the early report reappeared in A History. A key theme in the 1964 monograph was a critique of the Fed’s use of the Net Free Reserves doctrine which had evolved in the 1950s from the earlier Burgess Rieffler Strong doctrine which guided Fed policy in the 1920s and 1930s. which the authors argued explained the Fed’s policy mistakes leading to the Great Contraction. They posit the case that their monetarist approach based on the money supply, monetary base and money multiplier could have greatly improved the Fed’s performance from the 1920s to the 1960s.The 1964 monograph was a key building block for their later work in monetary theory and policy including their critique of Keynes, the importance of policy uncertainty and the case for a monetary base rule. -

University Microfilms, Inc., Ann Arbor, Michigan an APPRAISAL of a NATIONAL POLICY

AN APPRAISAL OF A NATIONAL POLICY: THE EMPLOYMENT ACT OF 1946 Item Type text; Dissertation-Reproduction (electronic) Authors Lansdowne, Jerry W. Publisher The University of Arizona. Rights Copyright © is held by the author. Digital access to this material is made possible by the University Libraries, University of Arizona. Further transmission, reproduction or presentation (such as public display or performance) of protected items is prohibited except with permission of the author. Download date 04/10/2021 12:36:28 Link to Item http://hdl.handle.net/10150/290209 This dissertation has been microfilmed exactly as received 68-13,547 LANSDOWNE, Jerry Wayman, 1931- AN APPRAISAL OF A NATIONAL POLICY: THE EMPLOYMENT ACT OF 1946. University of Arizona, Ph.D„ 1968 Political Science, general University Microfilms, Inc., Ann Arbor, Michigan AN APPRAISAL OF A NATIONAL POLICY: THE EMPLOYMENT ACT OF 1946 by Jerry Waymati Lansdowne A Dissertation Submitted to the Faculty of the DEPARTMENT OF GOVERNMENT In Partial Fulfillment of the Requirements For the Degree of DOCTOR OF PHILOSOPHY v. In the Graduate College THE UNIVERSITY OF ARIZONA 1968 THE UNIVERSITY OF ARIZONA GRADUATE COLLEGE I hereby recommend that this dissertation prepared under my direction by Jerry Wayman Lansdowne entitled An Appraisal of a National Policy. The Employment Act of 19^6 be accepted as fulfilling the dissertation requirement of the degree of Doctor of Philosophy * | VJ i- - <—<>_ Cp & Dissertation Director Date After inspection of the final copy of the dissertation, the following members of the Final Examination Committee concur in its approval and recommend its acceptance:'" 3 - V &' 3 -c y s? - O 1 •6,^ (o & This approval and acceptance is contingent on the candidate's adequate performance and defense of this dissertation at the final oral examination. -

The Making of Global Capitalism

Contents Preface vii INTRODUCTION 1 PART I: PRELUDE TO THE NEW AMERICAN EMPIRE . The DNA of American Capitalism 25 The Dynamic Economy 26 The Active State 31 Internationalizing the American State 35 . American State Capacities: From Great War to New Deal 45 From Wilson to Hoover: Isolationism Not 46 The Great Depression and the New Deal State 53 From New Deal to Grand Truce with Capital 59 PART II: THE PROJECT FOR A GLOBAL CAPITALISM . Planning the New American Empire 67 Internationalizing the New Deal 69 The Path to Bretton Woods 72 Laying the Domestic Foundations 80 . Launching Global Capitalism 89 Evolving the Marshall Plan 91 The American Rescue of European Capitalism 96 “The Rest of the World” 102 PART III: THE TRANSITION TO GLOBAL CAPITALISM . The Contradictions of Success 111 Internationalizing Production 112 Internationalizing Finance 117 Detaching from Bretton Woods 122 . Structural Power Through Crisis 133 Class, Profi ts, and Crisis 135 Transition through Crisis 144 Facing the Crisis Together 152 PART IV: THE REALIZATION OF GLOBAL CAPITALISM . Renewing Imperial Capacity 163 The Path to Discipline 164 The New Age of Finance 172 The Material Base of Empire 183 . Integrating Global Capitalism 195 Integrating Europe 196 Japan’s Contradictions of Success 203 The Rest of the World (Literally) 211 PART V: THE RULE OF GLOBAL CAPITALISM . Rules of Law: Governing Globalization 223 The Laws of Free Trade 224 Global Investment, American Rules 230 Disciplinary Internationalism 234 . The New Imperial Challenge: Managing Crises 247 Firefi ghter in Chief 248 The Asian Contagion 254 Failure Containment 261 PART VI: THE GLOBAL CAPITALIST MILLENNIUM . -

Joint Economic Report

81sT CONGRESS SENATE {NREPORT JOINT ECONOMIC REPORT REPORT OF THE JOINT COMMITTEE ON THE ECONOMIC REPORT ON THE JANUARY 1950 ECONOMIC REPORT OF THE PRESIDENT TOGETHER WITH THE MINORITY VIEWS JuNE 16 (legislative day, JuNE 7), 1950.-Ordered to be printed, with illustrations UNITED STATES GOVERNMENT PRINTING OFFICE 68366 WASHINGTON : 1950 JOINT COMMITTEE ON THE ECONOMIC REPORT (Created pursuant to see. 5 (a) of Public Law 304, 79th Cong.) SENATE HOUSE OF REPRESENTATIVES JOSEPH C. O'MAHONEY, Wyoming, Chairman EDWARD J. HART, New Jersey, Vice Chairman FRANCIS J. MYERS, Pennsylvania WRIGHT PATMAN, Texas JOHN SPARKMAN, Alabama WALTER B. HUBER, Ohio PAUL H. DOUGLAS, Illinois FRANK BUCHANAN, Pennsylvania ROBERT A. TAFT, Ohio JESSE P. WOLCOTT, Michigan RALPH E. FLANDERS, Vermont ROBERT F. RICH, Pennsylvania ARTHUR V. WATKINS, Utah CHRISTIAN A. HERTER, Massachusetts TREODORE J. KREPS, Staff Director GROVER W. ENSLEY, Associate Staff Director JOHN W. LEIRMAN, Clerk 11 CONTENTS I. COMMITTEE FINDINGS Page The fundamental problem - _ ------------------------ 4 The basic solution: Private capital investment -__-___-__-__-____-__ 5 A positive program to strengthen the system of private property -10 Unity in the Congress - 11 Unity in the programs of business, labor, and agriculture -12 Recommendations -13 Comments on the President's legislative'recommendations -15 Comments on subcommittee reports and recommendations -18 Supplementary statement of Senator Douglas - 22 II. VIEWS OF THE MINORITY Appraisal of philosophy of President's report--------------------------- -

An Historical Perspective

How the American Free Enterprise System Creates Jobs and Prosperity Lesson 1 – An Historical Perspective How the American Free Enterprise System Creates Jobs and Prosperity is a nine lesson (with Prologue) mini-course of study designed to provide students with a big picture understanding about how the American free enterprise system works and the importance of entrepreneurship and innovation in the context of the global economy. This course is offered by Entrepreneurial Engagement Ohio, which is 501(c)(3) non-profit with the mission of promoting entrepreneurial, economic, business, and scientific literacy of students. © - 2016 John Klipfell and Entrepreneurial Engagement Ohio Lesson One - A Historical Perspective Key Points To Take Away: 1. The American free enterprise system has created jobs and prosperity despite all the challenges it has faced. 2. Generations of innovators & entrepreneurs before us have created the jobs and prosperity we enjoy today. 3. Few countries in the world enjoy a standard of living that approaches that of the USA. Recession Name Peak Unemployment Rate Understanding Great depression (1929-33) 24.9% Recessions Recession of 1937-38 19.0% Recession of 1945 5.2% Recession of 1949 7.9% Recession of 1953 6.1% Recession of 1958 7.5% Recession of 1960-61 7.1% Recession of 1969-70 6.1% Recession of 1973-75 9.0% Recession of 1980 7.8% Early 1980’s recession 10.8% Early 1990’s recession 7.8% Early 2000’s recession 6.3% Great recession 2007-2009 10.0% Source: Wikipedia Source: US Census Bureau Percentage of US Labor Force Employed In Agriculture 100 75 % of Labor Force 50 25 0 1980 2000 1920 1940 1960 1870 1900 Year Source: US Census Bureau & US Bureau of Labor Statistics Total US Civilian Labor Force 160 Civilian Labor Force (millions) CivilianLabor Force 120 80 40 0 1960 1980 2000 2010 1870 1900 1920 1940 Year Lesson One - A Historical Perspective Can our economic system continue to create the millions of jobs needed to continue American prosperity? Yes, but only if people understand how our economic system works. -

Jones, the Falling Rate of Profit and the Great Recession Final Corrected

The Falling Rate of Profit and the Great Recession Peter Jones November 2014 1 A thesis submitted for the degree of Doctor of Philosophy of the Australian National University 2 I declare that the material contained in this thesis is entirely my own work, except where due and accurate acknowledgment of another source has been made. Peter Jones 3 Acknowledgements All writing is a collaborative effort to some extent, even the somewhat individualistic task of writing a PhD thesis. Rick Kuhn’s help, advice, comments and example have been the most important contributions of any individual and deserve the most credit. An email debate with Bob McKee, Guglielmo Carchedi, Alan Freeman and Andrew Kliman also helped clarify some of the key concepts used in the thesis, and their work developing and applying Marx’s value theory was the most important inspiration and intellectual reference point for the thesis as a whole. My aunt Lyn Rainforest and my mother Cathy Jones also generously helped with editing some of the chapters. I have also been challenged to sharpen my analysis by discussions with many comrades in Australia. The thesis would not have been possible without the support and encouragement of my partner Amanda Zivcic and of course my family and friends, in particular my mother and my sister, Laura Jones. I also cannot also help thinking of my late father Robert Jones and what he would have made of it all; no doubt he would have disagreed with a great deal but would also have been very supportive. 4 Abstract This thesis develops a new, temporalist interpretation of Marx’s value theory.