Report for the Period Ended 30 September 2017

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

New Board and Job Announcements August 2017

New Board and Job Announcements August 2017 Louise Adamany has started a role as Independent Director at Wood Group PLC Irene Chang Britt has started a role as Independent Director at Brighthouse Financial, Inc. http://investor.brighthousefinancial.com/corporate-governance/board-of-directors Carmen Bowser will become an Independent Director at Peapack Gladstone Financial and Peapack Gladstone Bank on September 28. http://philadelphia.citybizlist.com/article/436644/peapack-gladstone-financial-corp-appoints- carmen-m-bowser-director Leslie Anne Coolidge has started a role as Independent Director at Power Solutions International, a leader in the design, engineer and manufacture of emissions-certified, alternative-fuel power systems. http://investors.psiengines.com/releasedetail.cfm?ReleaseID=1033699 Tanuja Majumdar Dehne has started a role as Independent Director of Advanced Disposal Services, the fourth largest solid waste company in the U.S. http://www.advanceddisposal.com/news/2017/advanced-disposal-announces-that-tanuja- dehne-has-been-elected-to-its-board-of-directors.aspx Carol Eicher has changed roles from President/CEO to Chairman at Innocor, Inc. Ambassador April H. Foley has changed role from Independent Director to Lead Independent Director of Vista Outdoor, Inc., a designer, manufacturer, and marketer of outdoor sports and recreation products. https://vistaoutdoor.com/investors-information/corporate-governance/board-of-directors/ Andrea Funk has joined the board of Crown Holdings, Inc., supplier of packaging products to consumer marketing companies. https://www.crowncork.com/news/press-room/crown-holdings-inc-elects-andrea-j-funk-its-board- directors Elizabeth Noël Harwerth has started a role as NED at Charter Court Financial Services Group Ltd, one of the fastest growing specialty mortgage banks in the UK. -

Avg Rtg Corporate Bonds Redeemable Pfd Stock Government

TORCHMARK CORPORATION Bond Exposures $50M and Over From All Operations (Millions of $) December 31, 2014 Amortized Cost ($ millions) Asset- Avg Corporate Redeemable Government Backed Rtg Bonds Pfd Stock & GSE Municipals Securities Total Fair Value BERKSHIRE HATHAWAY INC A 197 - - - - 197 239 GENERAL ELECTRIC CO AA- 113 - - - - 113 148 TENN VALLEY AUTHORITY AAA - - 108 - - 108 107 DUKE ENERGY CORP BBB+ 108 - - - - 108 142 NATIONAL GRID PLC A- 106 - - - - 106 117 FANNIE MAE AAA - - 101 - - 101 107 SOUTHERN CO/THE A 97 - - - - 97 108 EXELON CORP BBB+ 79 17 - - - 97 120 DOW CHEMICAL CO/THE BBB 87 - - - - 87 93 CARGILL INC A 85 - - - - 85 104 CSX CORP BBB+ 85 - - - - 85 101 METLIFE INC BBB+ 70 15 - - - 85 99 JOHNSON CONTROLS INC BBB 83 - - - - 83 96 UNION PACIFIC CORP A- 82 - - - - 82 89 EATON CORP PLC BBB+ 81 - - - - 81 79 COOPERATIEVE CENTRALE RAIFFEIS AA- 81 - - - - 81 96 UNITED TECHNOLOGIES CORP A 81 - - - - 81 84 ENTERPRISE PRODUCTS PARTNERS L BBB+ 80 - - - - 80 91 ATMOS ENERGY CORP A- 79 - - - - 79 88 AGL RESOURCES INC BBB+ 79 - - - - 79 93 NORFOLK SOUTHERN CORP BBB+ 79 - - - - 79 79 DOMINION RESOURCES INC/VA BBB+ 72 6 - - - 79 81 NAVIENT CORP BB 75 - - - - 75 66 FREDDIE MAC AAA - - 74 - - 74 76 US TREASURY AAA - - 74 - - 74 73 GLENCORE PLC BBB 74 - - - - 74 82 NEWMONT MINING CORP BBB 73 - - - - 73 74 AMERICAN INTERNATIONAL GROUP I BBB 71 - - - - 71 80 AT&T INC A- 70 - - - - 70 77 TRAVELERS COS INC/THE BBB+ 25 45 - - - 70 82 LINCOLN NATIONAL CORP BBB+ 69 - - - - 69 83 AMERICAN UNITED MUTUAL INSURAN A- 69 - - - - 69 73 MOSAIC CO/THE BBB -

Annex 1: Parker Review Survey Results As at 2 November 2020

Annex 1: Parker Review survey results as at 2 November 2020 The data included in this table is a representation of the survey results as at 2 November 2020, which were self-declared by the FTSE 100 companies. As at March 2021, a further seven FTSE 100 companies have appointed directors from a minority ethnic group, effective in the early months of this year. These companies have been identified through an * in the table below. 3 3 4 4 2 2 Company Company 1 1 (source: BoardEx) Met Not Met Did Not Submit Data Respond Not Did Met Not Met Did Not Submit Data Respond Not Did 1 Admiral Group PLC a 27 Hargreaves Lansdown PLC a 2 Anglo American PLC a 28 Hikma Pharmaceuticals PLC a 3 Antofagasta PLC a 29 HSBC Holdings PLC a InterContinental Hotels 30 a 4 AstraZeneca PLC a Group PLC 5 Avast PLC a 31 Intermediate Capital Group PLC a 6 Aveva PLC a 32 Intertek Group PLC a 7 B&M European Value Retail S.A. a 33 J Sainsbury PLC a 8 Barclays PLC a 34 Johnson Matthey PLC a 9 Barratt Developments PLC a 35 Kingfisher PLC a 10 Berkeley Group Holdings PLC a 36 Legal & General Group PLC a 11 BHP Group PLC a 37 Lloyds Banking Group PLC a 12 BP PLC a 38 Melrose Industries PLC a 13 British American Tobacco PLC a 39 Mondi PLC a 14 British Land Company PLC a 40 National Grid PLC a 15 BT Group PLC a 41 NatWest Group PLC a 16 Bunzl PLC a 42 Ocado Group PLC a 17 Burberry Group PLC a 43 Pearson PLC a 18 Coca-Cola HBC AG a 44 Pennon Group PLC a 19 Compass Group PLC a 45 Phoenix Group Holdings PLC a 20 Diageo PLC a 46 Polymetal International PLC a 21 Experian PLC a 47 -

Rio Tinto BHP, Tesco, Sainsbury, Arcelormittal, National Grid

Quarterly Engagement Rio Tinto Report July-September BHP, Tesco, 2020 Sainsbury, ArcelorMittal, National Grid 2 LAPFF QUARTERLY ENGAGEMENT REPORT | JULY-SEPTEMBER 2020 lapfforum.org CLIMATE EMERGENCY Puutu Kunti Kurrama and Pinikura Aboriginal Corporation Rio Tinto under pressure from investors over Juukan Gorge As LAPFF has been learning more about “My interaction with Mr. Rio Tinto’s involvement in the destruc- Thompson, in his roles as Chair tion of the historically significant caves of both Rio Tinto and 3i, has been at Juukan Gorge in Western Australia, there have been increasing concerns positive thus far. However, I sense about the company’s corporate govern- that investors are losing confidence ance practices. Consequently, the Forum in his leadership and in his board at – along with other investor groups, most Rio Tinto. It will be a long road back What happened at prominently the Australasian Centre for for the company.” Juukan Gorge? Corporate Responsibility (ACCR) - has been pushing the company to review its Cllr Doug McMurdo In May, Rio Tinto destroyed 46,000-year- corporate governance arrangements. old Aboriginal caves in the Juukan One of the main strategies in this Gorge region of Western Australia. The engagement has been to issue press responding to information issued by explosions were part of a government releases citing LAPFF’s concerns as vari- Australian Parliamentary inquiries into sanctioned mining exploration in ous details of Rio Tinto’s practices were this matter. There appears to be increas- the region. The caves are of cultural revealed through a range of investiga- ing evidence of corporate governance fail- significance to the Puutu Kunti tions. -

National Grid Plc Anheuser-Busch Inbev SA/NV

Vote Summary Report Reporting Period: 07/01/2020 to 06/30/2021 Location(s): All Locations Institution Account(s): Horizons Enhanced Income International Equity ETF National Grid Plc Meeting Date: 04/22/2021 Country: United Kingdom Primary Security ID: G6S9A7120 Record Date: 03/29/2021 Meeting Type: Special Ticker: NG Shares Voted: 5,593 Proposal Voting Vote Number Proposal Text Proponent Mgmt Rec Policy Rec Instruction Meeting for ADR Holders Mgmt 1 Approve Acquisition of PPL WPD Investments Mgmt For For For Limited 2 Approve Increase in Borrowing Limit Under Mgmt For For For the Company's Articles of Association Anheuser-Busch InBev SA/NV Meeting Date: 04/28/2021 Country: Belgium Primary Security ID: B639CJ108 Record Date: 03/16/2021 Meeting Type: Annual/Special Ticker: ABI Shares Voted: 6,778 Proposal Voting Vote Number Proposal Text Proponent Mgmt Rec Policy Rec Instruction Meeting for ADR Holders Mgmt Special Meeting Agenda Mgmt A1 Authorize Repurchase of Up to 20 Percent of Mgmt For Against Against Issued Share Capital Annual Meeting Agenda Mgmt B2 Receive Directors' Reports (Non-Voting) Mgmt B3 Receive Auditors' Reports (Non-Voting) Mgmt B4 Receive Consolidated Financial Statements Mgmt and Statutory Reports (Non-Voting) B5 Approve Financial Statements, Allocation of Mgmt For For For Income, and Dividends of EUR 0.50 per Share B6 Approve Discharge of Directors Mgmt For For For B7 Approve Discharge of Auditors Mgmt For For For B8.a Reelect Martin J. Barrington as Director Mgmt For Against Against B8.b Reelect William F. Gifford, -

Lessons from FRS17 Disclosures

Is Pension Fund Asset Allocation Really Determined by Fundamentals? Mike Orszag W W W . W A T S O N W Y A T T . C O M Paris, April 2, 2004 Key Question z Do pension funds make asset allocation decisions based on corporate finance risk considerations? z Factors which might matter: – Size of pension scheme relative to company – Size of deficits relative to company – Maturity of scheme Copyright © Watson Wyatt Worldwide. All rights reserved. Data z UK listed companies have had to report pension liabilities on FRS17 basis since late 2001 z Collected roughly 150 data items for FTSE350 on corporate finance from FRS17 disclosures z Matched data to other data on market returns/option price data, betas, etc. Copyright © Watson Wyatt Worldwide. All rights reserved. Accounting Dates z Roughly 48% of FTSE350 (168 companies) use Dec. 31 as end of year, 17% (60 companies) use 31 March, 8% (29 companies) use 30 September, remainder use a variety of dates z Define a panel with two waves: – 2001 Wave = Accounting dates between 30 June 2001 and 29 June 2002 – 2002 Wave = Accounting dates between 30 June 2002 and 29 June 2003 Copyright © Watson Wyatt Worldwide. All rights reserved. Pension Surplus(Deficit)/Pension Liabilities FTSE 350 companies with positive reported pension liabilities 2001 2002 Wave 2002 has 5% -30% -48.1% only 10 10% -24.9% -43.7% companies with 25% -15.2% -34.0% surpluses as 50% -7.7% -27.4% opposed to 81 in 2001. 75% 3.3% -17.3% Among FTSE 90% 15.5% -8.3% 100, wave 2001 95% 21.8% -1.0% has only 4 companies in surplus as N 242 257 opposed to 46 in 2001 Copyright © Watson Wyatt Worldwide. -

Portfolio Investment Report

December 2019 Bristol University Holdings as at 31st December 2019 Please note that the following information is valid as at 31/12/2019. The provision of this information does not constitute a recommendation, investment advice, nor financial promotion. Holdings are subject to change without notice and their accuracy and completeness cannot be guaranteed. No part of this document may be reproduced in any manner without Rathbones prior permission. As per the University’s Investment policy, the portfolio is moving to full fossil fuel divestment and a measurable reduction in the carbon intensity of the investments over time. To date, the only remaining direct position in the Oil & Gas sector is Equinor, representing approximately 0.78% of the portfolio. Direct investment in the Energy sector which is used to measure carbon intensity, includes Orsted, SSE and National Grid. These stocks represent approximately 4.94% of the portfolio. SECURITY NAME SECTOR TREASURY 1 7/8% I/L Stock 22/11/2022 UK Index Linked Government Bonds TREASURY 2 1/2% I/L Stock 17/07/2024 UK Index Linked Government Bonds RABOBANK NEDERLAND 2.25% Snr MTN 23/03/2022 UK Inv Grade Bonds - Higher Quality COVENTRY BUILDING SOCIETY 1.875% Bonds 24/10/2023 UK Inv Grade Bonds - Higher Quality KREDITANST FUR WIE 5.5% MTN 18/6/2025 UK Inv Grade Bonds - Higher Quality EURO INVESTMENT BANK 3.75% MTN 7/12/2027 UK Inv Grade Bonds - Higher Quality A2 DOMINION HOUSING GROUP LTD 3.5% Bonds 15/11/2028 UK Inv Grade Bonds - Higher Quality FIDELITY INTERNATIONAL 6.75% Notes 19/10/2020 UK Investment -

List of Public Interest Entities

www.pwc.co.uk/transparencyreport List of public interest entities List of public interest entities to accompany Transparency Report Year ended 30 June 2014 2 PricewaterhouseCoopers LLP UK Transparency Report FY14 List of public interest entities Please note – this list includes those 258 audit clients, for whom we issued an audit opinion between 1 July 2013 and 30 June 2014, who have issued transferable securities on a regulated market (as defined in the Statutory Auditors (Transparency) Instrument 2008 (POB 01/2008). 4IMPRINT GROUP PLC BOS (SHARED APPRECIATION MORTGAGES) NO. 1 PLC ABERFORTH GEARED INCOME TRUST PLC BOS (SHARED APPRECIATION MORTGAGES) NO. 2 PLC AFRICAN BARRICK GOLD PLC BOS (SHARED APPRECIATION MORTGAGES) NO.3 PLC AGGREKO PLC BOS (SHARED APPRECIATION MORTGAGES) NO.4 PLC AMLIN PLC BOS (SHARED APPRECIATION MORTGAGES) NO.6 PLC ARKLE MASTER ISSUER PLC BRADFORD & BINGLEY PLC ARM HOLDINGS PLC BRAMMER PLC ASIA RESOURCE MINERALS Plc (formerly BUMI Plc) BRISTOL & WEST PLC ASIAN TOTAL RETURN INVESTMENT COMPANY PLC BRITISH AMERICAN TOBACCO PLC (formerly Henderson Asian Growth Trust Plc) BRITISH TELECOMMUNICATIONS PLC AVIVA PLC BT GROUP PLC AVON RUBBER PLC BURBERRY GROUP PLC BABCOCK INTERNATIONAL GROUP PLC CAIRN ENERGY PLC BAGLAN MOOR HEALTHCARE PLC CAMELLIA PLC BAILLIE GIFFORD JAPAN TRUST PLC CAPITAL & COUNTIES PROPERTIES PLC BAILLIE GIFFORD SHIN NIPPON PLC CAPITAL GEARING TRUST PLC BANK OF SCOTLAND PLC CARNIVAL PLC BARCLAYS BANK PLC CARPETRIGHT PLC BARCLAYS PLC CARR’S MILLING INDUSTRIES PLC BERENDSEN PLC CATLIN UNDERWRITING BIRMINGHAM -

Energy Synthesis FINAL

Public Attitudes, Understanding, and Engagement in relation to Low-Carbon Energy: A selective review of academic and non-academic literatures Report for RCUK Energy Programme Public Attitudes, Understanding, and Engagement in relation to Low-Carbon Energy: A selective review of academic and non-academic literatures Report for RCUK Energy Programme January 2011 Lorraine Whitmarsh1,2 Paul Upham2,3 Wouter Poortinga1,4 Carly McLachlan2,7 Andrew Darnton5 Patrick Devine-Wright6 Christina Demski1 Fionnguala Sherry-Brennan6 1 School of Psychology, Cardiff University 2 Tyndall Centre for Climate Change Research 3 Manchester Business School, University of Manchester 4 Welsh School of Architecture, Cardiff University 5 AD Research and Analysis 6 School of Geography, University of Exeter 7 School of Mechanical, Aerospace and Civil Engineering, University of Manchester 2 Summary and Recommendations 1. Background Purpose of the report This study on public attitudes to, and engagement with, low-carbon energy draws together the results of UK-relevant social research and evidence, as of October 2010, in order to inform the RCUK Energy Programme at both strategic and operational levels. Our sources were identified through a systematic search of bibliographic databases and a formal call for evidence issued to practitioners and academics in order to identify non-academic (‘grey’) sources and forthcoming academic publications. The authors are all active in energy social science research. Overview of the report The report provides an introduction to some of the most relevant social science theory and concepts relating to public engagement (chapter 3), before reviewing findings on attitudes and engagement relating to energy supply, storage and distribution technologies (chapter 4); energy demand attitudes and engagement (chapter 5); and energy systems and research engagement (chapter 6). -

Management Audit of National Grid Massachusetts D.P.U

Boston Gas Company d/b/a National Grid D.P.U. 20-120 Attachment DPU-53-4 REDACTED Page 1 of 255 March 29, 2021 Management Audit of National Grid Massachusetts D.P.U. 19-117 FINAL REVISION Boston Gas Company d/b/a National Grid D.P.U. 20-120 Attachment DPU-53-4 REDACTED Page 2 of 255 Table of Contents Introduction Introduction .................................................................................................................................................. 1 Consolidated Findings and Recommendations ............................................................................................. 4 Chapter 1: Topic 1 - Examination and Evaluation of Strategic Planning Process History of NGUSA Reorganizations .......................................................................................................... 16 Introduction ........................................................................................................................................ 16 Organizational Charts 2007 to Present .............................................................................................. 18 2007 Global Lines of Business Model ................................................................................................. 21 2011 Jurisdictional Model “US Restructuring Program” .................................................................... 22 2014 “Model 2.0” ............................................................................................................................... 24 2018-2019 “Model 3.0” ..................................................................................................................... -

Cboe UK Utilities Sector Index BUKUTL

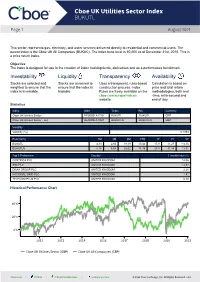

Cboe UK Utilities Sector Index BUKUTL Page 1 August 2021 Cboe Exchange This sector represents gas, electricity, and water services delivered directly to residential and commercial users. The parent index is the Cboe UK All Companies (BUKAC). The index base level is 10,000 as of December 31st, 2010. This is a price return index. Objective The index is designed for use in the creation of index tracking funds, derivatives and as a performance benchmark. Investability Liquidity Transparency Availability Stocks are selected and Stocks are screened to Uses a transparent, rules-based Calculation is based on weighted to ensure that the ensure that the index is construction process. Index price and total return index is investable. tradable. Rules are freely available on the methodologies, both real cboe.com/europe/indices -time, intra-second and website. end of day. Statistics Index ISIN Ticker RIC Currency Cboe UK Utilities Sector DE000SLA1730 BUKUTL .BUKUTL GBP Cboe UK Utilities Sector - net DE000SLA18M1 BUKUTLN .BUKUTLN GBP Volatility Volatility (1y) 0.1733 Returns(%) 1M 3M 6M YTD 1Y 3Y 5Y BUKUTL 4.13 2.66 18.19 10.42 17.9 11.27 -14.36 BUKUTLN 4.18 5.68 22.02 14.45 23.8 31.48 12.51 Top 5 Performers Country 1 month return % CENTRICA PLC UNITED KINGDOM 14.06 SSE PLC UNITED KINGDOM 12.64 DRAX GROUP PLC UNITED KINGDOM 2.28 NATIONAL GRID PLC UNITED KINGDOM 1.91 TELECOM PLUS PLC UNITED KINGDOM 0.39 Historical Performance Chart 40% 20% 0% 2011 2013 2014 2016 2017 2018 2020 2021 Cboe UK Utilities Sector (GBP) Cboe UK All Companies (GBP) Cboe.com | ©Cboe | /CboeGlobalMarkets | /company/cboe © 2021 Cboe Exchange, Inc. -

Sse Plc Annual Report 2020 About This Report

SSE PLC ANNUAL REPORT 2020 ANNUAL REPORT 2020 SSE PLC SSE PLC ANNUAL REPORT For a betterFor energy of world 2020 ABOUT THIS REPORT SSE plc is a UK-listed energy company and this Annual Report 2020 comprises a Strategic Report, a Directors’ Report and Financial Statements for the year ended 31 March 2020. In so far as possible, it also seeks to address trends and factors that could affect the future development, performance and position of SSE’s businesses. This includes taking account of events between 31 March 2020 and 16 June 2020, the date on which the Board of Directors approved this report. That period was dominated by the coronavirus emergency and the Board recognised on 16 June that it was difficult to forecast with accuracy the full extent of the pandemic’s human, social, economic and business impact. AT A GLANCE Operating profit Earnings per share Sale of SSE Energy Adjusted Adjusted Services page 17 SSE completed the sale of its GB £1,488.4m 83.6p household energy supply business. Reported Reported Progress in offshore £963.4m 40.6p wind page 19 SSE was successful in UK auctions for offshore wind capacity contracts. Dividend EBITDA Recommended full-year dividend Adjusted A commitment to decarbonisation page 21 80p £2,191.4m SSE adopted a new target to cut carbon intensity of electricity by 60% by 2030. Alternative Performance Measures Economic contribution SSE assesses the performance of the Group using a UK variety of performance measures. These measures are not all defined under IFRS and are therefore termed “non-GAAP” measures.