Boston Office Market Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Directory of Massachusetts LOBBYISTS 617.646.1000 - BOSTON - WASHINGTON DC GREG M

Directory of Massachusetts LOBBYISTS 617.646.1000 - www.oneillandassoc.com BOSTON - WASHINGTON DC GREG M. PETER J. VICTORIA E. MARK K. MATTHEW P. D’AGOSTINO D’AGOSTINO IRETON MOLLOY MCKENNA Lobbying & Public Aairs Providing comprehensive state and municipal advocacy. PRACTICE AREAS: TRANSPORTATION | HEALTH CARE PUBLIC SAFETY | REGULATIONS | ENERGY ENVIRONMENT | CANNABIS FINANCIAL SERVICES | EMERGING INDUSTRIES 12 POST OFFICE SQUARE, 6TH FLOOR | BOSTON, MA 02109 | 6175743399 WWW.TENAXSTRATEGIES.COM David Albright Oamshri Amarasingham Cynthia Arcate Jewish Alliance for Law and Social Action American Civil Liberties PowerOptions, Inc. A 18 Tremont Street, Suite 320 Union of Massachusetts 129 South Street, 5th Floor Boston, MA 02108 211 Congress Street Boston, MA 02111 Anthony Arthur Abdelahad (617) 227-3000 Boston, MA 02110 (617) 428-4258 Ventry Associates LLP (617) 482-3170 1 Walnut Street Walter Alcorn Luz A. Arevalo Boston, MA 02108 Consumer Technology Association Robert J. Ambrogi Greater Boston, Legal Services (617) 423-0028 1919 South Eads Street Law Office of Robert Ambrogi 197 Friend Street Arlington, VA 22202 128 Main Street Boston, MA 02114 Tate Abdols (571)239-5209 Gloucester, MA 01930 (617) 603-1569 Onex Partners Advisor, Inc. (978) 317-0972 161 Bay Street Theodore J. Alexio Jr. Derek Armstrong Toronto, ON M5J 2S1 Essential Strategies Inc. Shannon Ames Bank of America, N.A. (416) 362-7711 One State Street, Suite 1100 Low Impact Hydropower Institute 100 Federal Street Boston, MA 02109 329 Massachusetts Avenue, Suite 6 Boston, MA 02110 Brendan Scott Abel (617) 227-6666 Lexington, MA 02420 (617) 434-8613 Massachusetts Medical Society (781) 538-4266 860 Winter Street Waltham, MA 02451 Daniel Allegretti Gabriel Amo Kristina Ragosta Arnoux (781) 434-7682 Exelon Generation Company, LLC Magellan Health 1 Essex Drive The Home Depot 8621 Robert Fulton Drive Bow, NH 03304 166 Valley Street, 6M222 Columbia, MD 21046 Lisa C. -

Boston Office Market Report

BOSTON OFFICE MARKET REPORT THIRD QUARTER 2017 FLAT ABSORPTION AMIDST MOVING PIECES As the nation’s 10th largest metro and population growth exceeding San Francisco, New York and Los Angeles, Boston has cemented its status as one of the premier Global Markets as a “must have” location. Not surprisingly, rumors surrounding Amazon’s HQ2 are running rampant with many local professionals thinking the Hub stands an excellent chance to land the second behemoth headquarters for the booming Amazon. In addition to the buzz surrounding the potential Amazon expansion, the local market remained extremely active with several large chips announcing relocations this quarter. Rental rents have responded favorably with the average rate eclipsing $55.26 per square foot. With a combined vacancy rate at 7.0% across Downtown’s eight distinct submarkets, the overall market has remained at its lowest levels since the dot-com boom of the early 2000’s. Firmly rooted in education, technology and life sciences, the region’s diverse economic base has submitted strong job growth through increased recruitment and skilled labor retention from the area’s leading universities and institutions. Looking forward, expect sound market conditions and a diversified economy to guide the greater Boston commercial real estate market to a strong performance over the next several years. # 4.2% # 4.4% # 2.9% 4th AUGUST AUGUST ANNUAL HIGHEST GDP MASSACHUSETTS NATIONAL WAGE GROWTH PER CAPITA UNEMPLOYMENT UNEMPLOYMENT NATIONALLY MARKET TRENDS CLASS A - ASKING RATE BOSTON 10TH LARGEST -

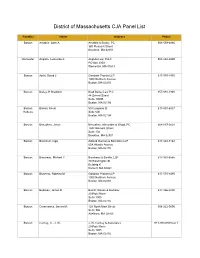

CJA Panel List 020717

District of Massachusetts CJA Panel List Panel(s) Name Address Phone Boston John A Amabile 380 Pleasant St. 508-559-6966 Brockton, MA 02301 Worcester Leonardo A. Angiulo PO Box 2903 508-868-0899 Worcester, MA 01613 Boston David J Apfel Goodwin Procter LLP 617-570-1970 Exchange Place 53 States Street Boston, MA 02109 Boston R Bradford Bailey Brad Bailey Law P.C. 857-991-1945 10 Winthrop Square 4th Floor Boston, MA 02110 Boston Kevin L Barron 5 Lexington Street 617-407-6837 Habeas No 3 Charlestown, MA 02129 Boston Janice Bassil Bassil & Budreau LLP 617-366-2200 20 Park Place Suite 1005 Boston, MA 02116 Boston Inga Bernstein Zalkind Duncan & Bernstein LLP 617-742-6020 65A Atlantic Avenue Boston, MA 02110 Springfield Alan J Black 48 Round Hill Road 413-732-5381 Habeas Suite 1 Northampton, MA 01060 Boston Victoria M Bonilla-Argudo Bourbeau & Bonilla, LLP 617-350-6868 80 Washington St. Building K Norwell, MA 02061 Boston Michael C Bourbeau 80 Washington St. 617-350-6565 Building K Norwell, MA 02061 Boston Roberto M Braceras Goodwin Procter LLP 617-570-1895 Exchange Place 53 State Streeet Boston, MA 02109 Tuesday, February 07, 2017 Page 1 of 12 Boston Henry Brennan, Jr. 20 Park Plaza Ste. 400 617-201-5977 Boston, MA 02116 Worcester Brian J Buckley Fletcher, Tilton & Whipple, P.C. 508-459-8017 370 Main Street Suite 1200 Worcester, MA 01608 Boston James H Budreau 20 Park Plaza 617-366-2200 Suite 1005 Boston, MA 02116 Boston James M. Caramanica 8 North Main Street 508-222-0096 Suite 403 Attelboro, MA 02703 Boston J. -

District of Massachusetts CJA Panel List

District of Massachusetts CJA Panel List Panel(s) Name Address Phone Email Boston Amabile, John A Amabile & Burkly, PC 508-559-6966 [email protected] 380 Pleasant Street Brockton, MA 02301 Worcester Angiulo, Leonardo A. Angiulo Law, PLLC 508-868-0899 [email protected] PO Box 2903 Worcester, MA 01613 Boston Apfel, David J Goodwin Procter LLP 617-570-1970 [email protected] 1000 Northern Avenue Boston, MA 02210 Boston Bailey, R Bradford Brad Bailey Law P.C. 857-991-1945 [email protected] 44 School Street Suite 1000B Boston, MA 02108 Boston Barron, Kevin 50 Congress St 617-407-6837 [email protected] Habeas Sutie 600 Boston, MA 02109 Boston Benzaken, Jason Benzaken, Alexander & Wood, PC 508-897-0001 [email protected] 1342 Belmont Street Suite 102 Brockton, MA 02301 Boston Bernstein, Inga Zalkind Duncan & Bernstein LLP 617-820-5168 [email protected] 65A Atlantic Avenue Boston, MA 02110 Boston Bourbeau, Michael C Bourbeau & Bonilla, LLP 617-350-6565 [email protected] 80 Washington St Building K Norwell, MA 02061 District of Massachusetts CJA Panel List Panel(s) Name Address Phone Email Boston Braceras, Roberto M Goodwin Procter LLP 617-570-1895 [email protected] 1000 Northern Avenue Boston, MA 02210 Boston Budreau, James H Bassil & Budreau 617-276-7385 [email protected] 20 Park Place Suite 1005 Boston, MA 02116 Boston Caramanica, James M. 120 North Main Street 508-222-0096 [email protected] Suite 306 Attelboro, MA 02703 Boston Carney, Jr., J. W. J. W. Carney & Associates -

B Oston Inner Harbor

93 30 Cambridge St Charlestown Msgr. O’Brien Chelsea St Hy Bridge Hampshire St Co Route 3 mm erc ial To Logan St t International 35 S t B s S Airport e 39 l r Broadway e o r v a t o h S n s Commercial Av C a d t Main St r H o on o f d M 31 i ar n Ch n a Longfellow a w ss t Ne a Cambridge St S ch Bridge u n I C se i C o n t h o d 22 t St a u St n s r State A r 16 w t St 7 A l t 29 e e o 33 S 34 l v a r r s B t n e n t v S o 38 i c H i t Harvard Bridge R m S e a s r n 4 2 e Boston T to r rl g 20 b Memorial Drive a Common in 44 o h Berkeley St sh 3 24 r C a 9 36 14 19 N W l o Public 8 10 41 e rth Beacon St er Garden 26 Beach S 37 n n Clarendon St t n A a v Dartmouth17 St 23Arlington St 42 C 25 43 S 15 21 h o 1 6 tuart S n 5 t r C gr 18 e e Commonwealth Av t t Su ss Commonwealth Av s n m S 46 e i m t 45 h e 40 c o r Boylston St r P 28 o Beacon St 90 t 27 D r 11 o Sobin 12 F Park 32 0 1/4 1/2 mi E Berkeley St 93 Boylston St 13 D St Huntington Av Brookline Av Reserved Channel Columbus Av Tremont St Representative Boston Office Landlord Projects 1 10 St. -

85 Devonshire Street Boston, Ma

85 DEVONSHIRE STREET BOSTON, MA RETAIL SPACE FOR LEASE 85 DEVONSHIRE STREET STREET FLOOR MEZZANINE BOSTON, MA 3,665 SF 855 SF – OPEN TO BELOW + 2,900 SF LOWE LEVEL 85 Devonshire Street provides hard corner visibility to a very busy vehicular and pedestrian intersection. Ideally positioned in the center of Downtown Crossing, adjacent to the MBTA - State Street entrance, with access to the Orange and Blue lines. Directly across from Congress Square which is occupied by: • 284,600 SF office including the 200,000 SF joint headquarters for DigitasLBi and Publicis.Sapient • A 165-key, 85,700 SF Hyatt Centric boutique hotel • 51,350 SF of residential space including 35 condominiums • 36,650 SF of retail Densely surrounded by office, hotel, and residential towers new and old, making this is an opportunity for strong seven-day customer counts and maximum brand visibility. 855 SF Dw WATER STREET WATER 3,665 SF OPEN TO BELOW +2,900 SF LOWER LEVEL DEVONSHIRE STREET PROPERTY FEATURES • 4,520 SF street-level retail/restaurant space and 2,900 SF lower-level space available • Corner location adjacent to MBTA entrance, across from Congress Square development, and steps from Freedom Trail and core Financial District • Approximately 55' of dramatic window line frontage along Devonshire Street, and 60’ of floor to ceiling window line along Water Street, allowing for prominent signage and branding visibility • Retail and restaurant neighbors include Dig Inn, HomeGoods, Love Art Sushi, Marshalls, Old Navy, Primark, Roche Bros., Shake Shack, Sweetgreen and T.J.Maxx -

CJA Panel List All Alpha.Xlsx

District of Massachusetts CJA Panel List Panel(s) Name Address Phone Boston Amabile, John A Amabile & Burkly, PC 508-559-6966 380 Pleasant Street Brockton, MA 02301 Worcester Angiulo, Leonardo A. Angiulo Law, PLLC 508-868-0899 PO Box 2903 Worcester, MA 01613 Boston Apfel, David J Goodwin Procter LLP 617-570-1970 1000 Northern Avenue Boston, MA 02210 Boston Bailey, R Bradford Brad Bailey Law P.C. 857-991-1945 44 School Street Suite 1000B Boston, MA 02108 Boston Barron, Kevin 50 Congress St 617-407-6837 Habeas Sutie 600 Boston, MA 02109 Boston Benzaken, Jason Benzaken, Alexander & Wood, PC 508-897-0001 1342 Belmont Street Suite 102 Brockton, MA 02301 Boston Bernstein, Inga Zalkind Duncan & Bernstein LLP 617-820-5168 65A Atlantic Avenue Boston, MA 02110 Boston Bourbeau, Michael C Bourbeau & Bonilla, LLP 617-350-6565 80 Washington St Building K Norwell, MA 02061 Boston Braceras, Roberto M Goodwin Procter LLP 617-570-1895 1000 Northern Avenue Boston, MA 02210 Boston Budreau, James H Bassil, Klovee & Budreau 617-366-2200 20 Park Place Suite 1005 Boston, MA 02116 Boston Caramanica, James M. 120 North Main Street 508-222-0096 Suite 306 Attelboro, MA 02703 Boston Carney, Jr., J. W. J. W. Carney & Associates 617-933-0350 ext 1 20 Park Place Suite 1405 Boston, MA 02116 District of Massachusetts CJA Panel List Panel(s) Name Address Phone Boston Christofferson, Eric DLA Piper LLP (US) 617-406-6089 33 Arch Street Boston, MA 02210 Habeas Church, Susan Demissie & Church 617-354-3944 929 Massachusetts Avenue Cambridge, MA 02139 Boston Cipoletta, James J 385 Broadway 781-289-7777 Suite 307 Revere, MA 02151 Boston Cloherty, Daniel J Todd & Weld LLP 617-624-4774 One Federal Street Boston, MA 02110 Boston Connolly, William H 20 Park Plaza 617-542-0200 Suite 1000 Boston, MA 02116 Boston Cunha, John Cunha & Holcomb, P.C. -

Lawyers Clearinghouse on Affordable Housing And

2018 - 2019 LAWYERS CLEARINGHOUSE BOARD OF DIRECTORS President Emily F. Hodge, Esq. Kathleen M. Phelps, Esq. Choate Hall & Stewart Morgan Lewis & Bockius LLP Christopher H. Lindstrom, Esq. Two International Place One Federal Street Nutter McClennen & Fish LLP Boston, MA 02110 Boston, MA 02110-1726 Seaport West 617 248-4075 617 951-8481 155 Seaport Boulevard [email protected] [email protected] Boston, MA 02210 Residence: Boston Residence: Needham 617 439-2698 Term Ends: 9/2019 Term Ends: 9/2020 [email protected] Member Since: 2013 Member Since: 2008 Residence: Wayland Term Ends: 9/2019 Kurt A. James, Esq. Cindy A. Rowe, Esq. Member Since: 2013 KJP Partners LLP JALSA 175 Federal Street, Suite 1440 18 Tremont Street, Suite 320 Vice President Boston, MA 02110 Boston, MA 02108 Elizabeth Lintz, Esq. 617 409-5398 617 227-3000 Goulston & Storrs, PC [email protected] [email protected] 400 Atlantic Avenue Residence: Marblehead Residence: Brookline Boston, MA 02110-3333 Term Ends: 9/2019 Term Ends: 9/2019 617 574-6495 Member Since: 2001 Member Since: 1992 [email protected] Residence: Jamaica Plain Jessica R. Lisak, Esq. Jeffrey W. Sacks, Esq. Term Ends: 9/2018 WilmerHale Nixon Peabody LLP Member Since: 2012 60 State Street 100 Summer Street Boston, MA 02109 Boston, MA 02110 Treasurer 617 526-6003 617 345-1056 [email protected] [email protected] Kathleen McGrath, Esq. Residence: Boston Residence: Newton Liberty Mutual Group Term Ends: 9/2021 Term Ends: 9/2018 175 Berkeley Street, Member Since: 2018 Member Since: 1997 Mail Stop M-06 E-284 Boston, MA 02116 Josephine A. -

Get Shopping!Grab a Retail

BEACON STREET Note: the majority of the businesses listed here are subject to COVID-related restrictions. Please call-ahead as you are making plans. BOSTON COMMON STATE HOUSE/BEACON HILL PARK STREET VISITOR INFO CENTER TH CHURCH GRANARY BURYING THE SHAW 54 REGIMENT MEMORIAL GROUND BEACON STREET AFRICAN-AMERICAN HERITAGE TRAIL Freedom Trail NORMAN THEATERS GNC 343 Washington Street, H3 | 58 Winter Street, F1 CRUMP 450 Washington St., E4 BEANTOWN BEANTOWN GALLERY AMC Loews Cinema 19 175 Tremont Street, B2 Lenscrafters (Macy’s) PUB CAFÉ PUB PAPER SOURCE FENWAY PARK HAMILTON PL. Pearle Vision 100 City Hall Plaza, K1 PUBLIC GARDEN NINE TREMONT Boston Opera House 539 Washington Street, C2 MUSEUM OF FINE ARTS WEN’S FALAFEL MOOYAH ZERO TEMPLE BACK BAY/NEWBURY STREET YUNNAN KING BURGERS HOTEL BRONCORE Modern Theatre 525 Washington Street, C2 Tobias & Battite Hearing Healthcare 16 Temple Place, E1 GLOBAL PACK NOODLES INSOMNIA FITNESS SHIP/FEDEX SUFFOLK UNIVERSITY COOKIES Orpheum Theatre 1 Hamilton Place, F2 Vision Care 2000 48 High Street, G7 DR. PHIL’S COMPUTER SISTERS DISCIPLES LAW SCHOOL BOOKSTORE BETTER SORTS RELIGIOUS GIFTS Paramount Center 545 Washington Street, C2 Wig World 27 Temple Place, E2 REPAIR CENTER SOCIAL CLUB SANTACROSS JADE NAILS DISTINCTIVE SHOE CARBON METRO CREDIT UNION ESCAPE CLOTHING SCHOOL STREET COFFEEHOUSE SALON THREADING PLACE FROM ITALY ODESSA INSTANT BOXAROO ATTRACTIONS HOME FURNISHINGS THE ROOM SHOE REPAIR EMPIRE TASTY BURGER T-MOBILE COURT SQUARE Boston Massacre Site Plaza 208 Washington Street, K3 HomeGoods 350 Washington Street, 3G BEAUTY CAFÉ 26 LADDER DISTRICT 26 COURT STREET COMMONWEALTH SALON ONEGIG BOUTIQUE MONEY BANK Boxaroo 55 Court Street, J1 Macy’s 450 Washington Street, F3 MUSEUM CHAPMAN PLACE 2 Avery Street, B3 DEMOCRACY BREWING OF BOSTON Emerson College Urban Arts Gallery 25 Avery Street, B2 Roche Bobois ORPHEUM THEATRE COLONIAL 17 WEST STREET TRADING CO. -

This Notice Contains Important Information That Is of Interest to the Beneficial Owners of the Subject Securities

Corporate Trust Services One Federal Street, 3rd Floor Boston, MA 02110 THIS NOTICE CONTAINS IMPORTANT INFORMATION THAT IS OF INTEREST TO THE BENEFICIAL OWNERS OF THE SUBJECT SECURITIES. IF APPLICABLE, ALL DEPOSITORIES, CUSTODIANS AND OTHER INTERMEDIARIES RECEIVING THIS NOTICE ARE REQUESTED TO EXPEDITE RE-TRANSMITTAL TO SUCH BENEFICIAL OWNERS IN A TIMELY MANNER. Informational Notice to Holders of Notes (the “Noteholders”) of THE NATIONAL COLLEGIATE STUDENT LOAN TRUST 2005-3 Student Loan Asset Backed Notes (the “Notes”) and the other parties listed on Schedule A (Classes and CUSIPs are listed on Exhibit A attached hereto) Regarding the Scheduled Bankruptcy Court Hearing for Plan Solicitation and Disclosure Statement Matters We refer you to our prior notice dated January 12, 2010 in which we notified you of the filing of the Motion For An Order (A) Approving the Disclosure Statement, (B) Temporarily Allowing Claims For Voting Purposes, (C) Establishing Procedures For Confirmation of the Plan, (D) Establishing Plan Solicitation and Voting Procedures and (E) Approving Forms of Notices and Ballots (the “Motion”). This notice corrects the information previously provided regarding the Bankruptcy Court location for the scheduled hearing on the Motion. NOTICE IS HEREBY given to the Noteholders that a hearing to consider the Motion has been scheduled for February 8, 2010 at 10:00 a.m. (EST) at the Bankruptcy Court located at United States Courthouse, 300 State Street, Springfield, MA 01105 (not in Worcester as stated in the original notice). Objections, if any, to the entry of an Order approving the Motion should (a) be in writing, (b) comply with the Bankruptcy Rules and the Local Bankruptcy Rules of the Court, (c) set forth the name of the objectant, the nature and amount of any claim or interest alleged by such objectant against the estate or the property of the Debtor, (d) state with particularity the legal and factual basis for the objection, (e) be served upon (i) Goodwin Procter LLP, Exchange Place, Boston, MA, Attention: Daniel M. -

Retail Brochure

SILVER PANTONE 877 C BLUE PANTONE 8182 C 10 WINTHROP SQUARE 10WINTHROPSQUARE.COM BOSTON, MA 02110 10 WINTHROP SQUARE UNMATCHED VISIBILITY RETAIL OPPORTUNITY 04 — 03 HIGHLY VISIBLE STOREFRONT IN BOSTON JEWEL BOX Located in a quintessential Bostonian office building, two retail opportunities on the ground and basement levels of 10 Winthrop Square have been entirely reconstructed and renewed for the most discerning retail tenant. CENTRAL DOWNTOWN PREMIER DESTINATION An unmatched retail experience with exposed brick and beam interior style and ceiling heights of up to 15ft, 10 Winthrop Square features a highly visible storefront facing Winthrop Square and Boston’s newest 1.8 million square foot luxury rental apartment and office development, Winthrop Center, where all entrances face 06 10 Winthrop Square and are within 200FT. Just steps from Downtown — 07 Crossing’s shopping center and public transportation, 10 Winthrop Square is the ideal location for any type of retail use. 08 — 07 STRATEGICALLY DESIGNED BUILDING SYSTEMS 10 Winthrop has been fully reconstructed with the most modern upgrades for long term use. This turn-of-the-century gem features up to 10FT windows with a highly visible storefront facing Winthrop Square, a brand new rooftop HVAC production system with all infrastructure stubbed to the premises and will be delivered vent- ready, with predetermined venting areas. Located on the ground level, the available space boasts ceiling heights of up to 15FT with an exclusive state-of-the-art first floor retail lobby and entrance. The basement level features ceiling heights of 10FT with its own lobby and entrance, retail lift, bathroom and shower. -

BID-Map-For-Website-20190823.Pdf

HOME FURNISHINGS Grainmaker 91 Summer Street, E5 Good Life 28 Kingston Street, E5 SERVICES DOWNTOWN CROSSING RETAIL MAP HomeGoods 350 Washington Street, 3G Grassroots Café 101 Arch Street, F4 Haley.Henry Wine Bar 45 Province Street, H2 Mattress Firm Downtown Boston 45 Franklin Street, G4 GreCo 1 Milk Street, H3 Hub Pub 18 Province Street, H2 BANKING SERVICES Altour Inc. Foreign Currency Location 155 Federal Street, F7 THEATERS ATTRACTIONS FOOD & DRINK SALONS, SPA & WELLNESS Roche Bobois 2 Avery Street, B3 Herrera’s Mexican Grill 11 Temple Place, E1 J.J. Foley’s Bar & Grille 21 Kingston Street, E5 Macy’s 450 Washington Street, F3 JM Curley 21 Temple Place, E1 Bank of America 100 Federal Street, H6 | 175 Federal Street, HOTELS SHOPPING SERVICES DOWNTOWN PUSHCART VENDOR Love Art Poke 40 Water Street, J3 F7 | 65 Franklin Street, G4 | 79 Summer Street (ATM-only), E5 | 6 Luke’s Lobster 290 Washington Street, I3 Kingston Cuts 25 Kingston Street, E5 JEWELERS The Last Hurrah (Omni Parker House) 60 School Street, H1 Tremont Street, J1 | 315 Washington Street (ATM-only), H3 | 11 FREEDOM TRAIL DOWNTOWN CROSSING PEDESTRIAN ZONE McDonald’s 146 Tremont Street, D1 Winter Street (ATM-only), F2 | 58 Winter Street (ATM-only), F1 Boston Diamond Co. 339 Washington Street, H3 LX Legal Crossing 558 Washington Street, C3 McDonald’s 327 Washington Street, H3 121 Congress St., I5 FREE WIFI ZONE U.S. POST OFFICE PUBLIC PARKING Boston Discount Jewelry Exchange Marliave 10 Bosworth Street, G2 Berkshire Bank Milk Street Café 50 Milk Street, I4 1 Boston Place, J2 365