Isetan Mitsukoshi Holdings (3099

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Isetan Mitsukoshi Holdings Ltd. 5-16-10, Shinjuku, Shinjuku-Ku, Tokyo, Japan

Convocation Notice Securities Code: 3099 May 28, 2018 To Shareholders with Voting Rights Ken Akamatsu Chairman and Representative Director Isetan Mitsukoshi Holdings Ltd. 5-16-10, Shinjuku, Shinjuku-ku, Tokyo, Japan NOTICE OF THE CONVOCATION OF THE 10TH ORDINARY GENERAL MEETING OF SHAREHOLDERS You are cordially invited to attend the 10th Ordinary General Meeting of Shareholders of Isetan Mitsukoshi Holdings Ltd. (the “Company”). The meeting will be held as described below. If you are unable to attend the meeting, you can exercise your voting rights in writing or via the Internet, etc., as described in “Guide to Exercising Voting Rights” on the next page. Please review the Reference Documents for the General Meeting of Shareholders in the following pages and exercise your voting rights by 8 p.m., Friday, June 15, 2018. 1. Date and Time: Monday, June 18, 2018, at 10:00 a.m. The reception is scheduled to begin at 9:00 a.m. 2. Place: Palais Royal, B1F, Grand Nikko Tokyo Daiba 2-6-1, Daiba, Minato-ku, Tokyo, Japan * Please be aware that if Palais Royal is full, you will be shown to a second meeting room. 3. Agenda of the Meeting: Matters to be reported: 1. The Business Report and the Consolidated Financial Statements for the 10th term (from April 1, 2017 to March 31, 2018) and results of audits by the Accounting Auditor and the Board of Corporate Auditors of the Consolidated Financial Statements 2. The Nonconsolidated Financial Statements for the 10th term (from April 1, 2017 to March 31, 2018) Proposals to be resolved: Proposal No. -

Isetan Mitsukoshi Holdings Report 2018

Isetan Mitsukoshi Holdings Ltd. Isetan Mitsukoshi Holdings Report 2018 Integrated Report (Annual Report/CSR Report) Contact for Inquiries: Isetan Mitsukoshi Holdings Ltd. Public Relations/Share Division, General Administration Department https://www.imhds.co.jp/english/inquiry/ Our Philosophy Contents 02 Our Philosophy 03 About the Isetan Mitsukoshi Group 07 Top Message 13 Medium-Term Management Plan 23 Interview with Officer in Charge 27 Sustainability 31 Corporate Governance 39 Financial Data 43 Non-Financial Data 51 Long-Term History of Our Challenges 53 Company Profile/ Stock Information Editorial Policy Starting from the current fiscal year, the Isetan Mitsukoshi Group is issuing the Integrated Report, with the aim of having all of its stakeholders, including its shareholders and investors, understand the story of its value creation, in which the Group continues to grow sustainably by taking advantage of its universal values and strengths. This Report has been compiled by integrating the previous Annual Report and CSR Report and referring to “Our” refers to the Isetan Mitsukoshi Group itself and everyone working there. materials including the Guidance for Collaborative Value Creation that was announced by “Our Philosophy” means the reason to exist of the Isetan Mitsukoshi Group the Ministry of Economy, Trade and Industry. We will issue this Report every year, refining it to make it a constructive tool for dialogues with all stakeholders. and the Group’s vision for itself. It is also a guiding principle to which we should always return and shows how each and every individual should change. *The departments and positions mentioned in this report are correct as of March 31, 2019. -

Wilmington Funds Holdings Template DRAFT

Wilmington Global Alpha Equities Fund as of 5/31/2021 (Portfolio composition is subject to change) ISSUER NAME % OF ASSETS USD/CAD FWD 20210616 00050 3.16% DREYFUS GOVT CASH MGMT-I 2.91% MORGAN STANLEY FUTURE USD SECURED - TOTAL EQUITY 2.81% USD/EUR FWD 20210616 00050 1.69% MICROSOFT CORP 1.62% USD/GBP FWD 20210616 49 1.40% USD/JPY FWD 20210616 00050 1.34% APPLE INC 1.25% AMAZON.COM INC 1.20% ALPHABET INC 1.03% CANADIAN NATIONAL RAILWAY CO 0.99% AIA GROUP LTD 0.98% NOVARTIS AG 0.98% TENCENT HOLDINGS LTD 0.91% INTACT FINANCIAL CORP 0.91% CHARLES SCHWAB CORP/THE 0.91% FACEBOOK INC 0.84% FORTIVE CORP 0.81% BRENNTAG SE 0.77% COPART INC 0.75% CONSTELLATION SOFTWARE INC/CANADA 0.70% UNITEDHEALTH GROUP INC 0.70% AXA SA 0.63% FIDELITY NATIONAL INFORMATION SERVICES INC 0.63% BERKSHIRE HATHAWAY INC 0.62% PFIZER INC 0.62% TOTAL SE 0.61% MEDICAL PROPERTIES TRUST INC 0.61% VINCI SA 0.60% COMPASS GROUP PLC 0.60% KDDI CORP 0.60% BAE SYSTEMS PLC 0.57% MOTOROLA SOLUTIONS INC 0.57% NATIONAL GRID PLC 0.56% PUBLIC STORAGE 0.56% NVR INC 0.53% AMERICAN TOWER CORP 0.53% MEDTRONIC PLC 0.51% PROGRESSIVE CORP/THE 0.50% DANAHER CORP 0.50% MARKEL CORP 0.49% JOHNSON & JOHNSON 0.48% BUREAU VERITAS SA 0.48% NESTLE SA 0.47% MARSH & MCLENNAN COS INC 0.46% ALIBABA GROUP HOLDING LTD 0.45% LOCKHEED MARTIN CORP 0.45% ALPHABET INC 0.44% MERCK & CO INC 0.43% CINTAS CORP 0.42% EXPEDITORS INTERNATIONAL OF WASHINGTON INC 0.41% MCDONALD'S CORP 0.41% RIO TINTO PLC 0.41% IDEX CORP 0.40% DIAGEO PLC 0.40% LENNOX INTERNATIONAL INC 0.40% PNC FINANCIAL SERVICES GROUP INC/THE 0.40% ACCENTURE -

Factset-Top Ten-0521.Xlsm

Pax International Sustainable Economy Fund USD 7/31/2021 Port. Ending Market Value Portfolio Weight ASML Holding NV 34,391,879.94 4.3 Roche Holding Ltd 28,162,840.25 3.5 Novo Nordisk A/S Class B 17,719,993.74 2.2 SAP SE 17,154,858.23 2.1 AstraZeneca PLC 15,759,939.73 2.0 Unilever PLC 13,234,315.16 1.7 Commonwealth Bank of Australia 13,046,820.57 1.6 L'Oreal SA 10,415,009.32 1.3 Schneider Electric SE 10,269,506.68 1.3 GlaxoSmithKline plc 9,942,271.59 1.2 Allianz SE 9,890,811.85 1.2 Hong Kong Exchanges & Clearing Ltd. 9,477,680.83 1.2 Lonza Group AG 9,369,993.95 1.2 RELX PLC 9,269,729.12 1.2 BNP Paribas SA Class A 8,824,299.39 1.1 Takeda Pharmaceutical Co. Ltd. 8,557,780.88 1.1 Air Liquide SA 8,445,618.28 1.1 KDDI Corporation 7,560,223.63 0.9 Recruit Holdings Co., Ltd. 7,424,282.72 0.9 HOYA CORPORATION 7,295,471.27 0.9 ABB Ltd. 7,293,350.84 0.9 BASF SE 7,257,816.71 0.9 Tokyo Electron Ltd. 7,049,583.59 0.9 Munich Reinsurance Company 7,019,776.96 0.9 ASSA ABLOY AB Class B 6,982,707.69 0.9 Vestas Wind Systems A/S 6,965,518.08 0.9 Merck KGaA 6,868,081.50 0.9 Iberdrola SA 6,581,084.07 0.8 Compagnie Generale des Etablissements Michelin SCA 6,555,056.14 0.8 Straumann Holding AG 6,480,282.66 0.8 Atlas Copco AB Class B 6,194,910.19 0.8 Deutsche Boerse AG 6,186,305.10 0.8 UPM-Kymmene Oyj 5,956,283.07 0.7 Deutsche Post AG 5,851,177.11 0.7 Enel SpA 5,808,234.13 0.7 AXA SA 5,790,969.55 0.7 Nintendo Co., Ltd. -

Virtus Allianzgi International Small-Cap Fund

Virtus AllianzGI International Small-Cap Fund as of : 08/31/2021 (Unaudited) SECURITY SHARES TRADED MARKET VALUE % OF PORTFOLIO ASMedia Technology Inc 23,000 $1,722,085 2.04 % Unimicron Technology Corp 319,000 $1,697,819 2.01 % Evotec SE 33,494 $1,664,973 1.97 % Georg Fischer AG 954 $1,565,779 1.85 % Grafton Group PLC 80,693 $1,549,843 1.83 % Elkem ASA 361,810 $1,541,414 1.82 % Genus PLC 18,880 $1,540,558 1.82 % Howden Joinery Group PLC 118,070 $1,534,979 1.82 % Interroll Holding AG 340 $1,511,111 1.79 % Cancom SE 22,963 $1,510,768 1.79 % Spectris PLC 27,520 $1,490,733 1.76 % ASM International NV 3,841 $1,490,287 1.76 % Soitec 6,191 $1,479,549 1.75 % Intermediate Capital Group PLC 48,932 $1,478,686 1.75 % Aperam SA 23,199 $1,423,300 1.68 % Fuji Electric Co Ltd 32,600 $1,411,980 1.67 % Wienerberger AG 35,448 $1,391,268 1.65 % Bechtle AG 19,089 $1,379,858 1.63 % Jungheinrich AG Pref 24,964 $1,348,243 1.60 % Storebrand ASA 151,651 $1,346,924 1.59 % JMDC Inc 19,500 $1,336,454 1.58 % 1 SECURITY SHARES TRADED MARKET VALUE % OF PORTFOLIO Industrial & Infrastructure Fund Investment Corp 653 $1,312,945 1.55 % ValueCommerce Co Ltd 31,900 $1,309,171 1.55 % Jeol Ltd 17,700 $1,308,013 1.55 % Tokyu Fudosan Holdings Corp 225,200 $1,303,935 1.54 % ASR Nederland NV 28,191 $1,288,854 1.53 % Huhtamaki Oyj 24,096 $1,286,286 1.52 % Crest Nicholson Holdings plc 221,947 $1,280,994 1.52 % Aak Ab 53,435 $1,278,063 1.51 % Jenoptik AG 35,252 $1,272,856 1.51 % Auto Trader Group PLC 146,909 $1,270,441 1.50 % Elis SA 71,514 $1,264,914 1.50 % Sojitz Corp 415,100 $1,218,718 -

118Overview of MARUI GROUP

Overview of MARUI GROUP As of March 31, 2020 Company Overview Distribution of Shares Held by Shareholder Type MARUI GROUP’s Business Name MARUI GROUP CO., LTD. MARUI CO., LTD. MARUI HOME SERVICE Co., Ltd. Head office 3-2, Nakano 4-chome, Nakano-ku, Individuals and others*2 Financial institutions Retailing and store operation, internet sales, specialty store busi- Real estate rental business 27,748,000 shares 96,309,000 shares Tokyo 164-8701, Japan ness (operation and development of directly managed sales floors 34-28, Nakano 3-chome, Nakano-ku, Tokyo 164-0001, Japan (12.4%) (43.1%) Date of foundation February 17, 1931 and private brands) Tel: 03-6361-0101 (Receptionist) Date of establishment March 30, 1937 3-2, Nakano 4-chome, Nakano-ku, Tokyo 164-8701, Japan www.marui-hs.co.jp (Japanese only) 223,660,417 Capital ¥35,920 million Foreign institutions shares Tel: 03-3384-0101 (Receptionist) Business activities Corporate planning and management and individuals www.0101.co.jp.e.ex.hp.transer.com 63,148,000 shares MRI Co., Ltd. for Group companies engaged in (28.2%) Collection and management of receivables business, Retailing segment and FinTech segment Other companies Epos Card Co., Ltd. credit check business Stores Marui and Modi: 24 located in Kanto, Securities companies within Japan 3,429,000 shares Credit card business, credit loan business 34-28, Nakano 3-chome, Nakano-ku, Tokyo 164-0001, Japan Tokai, Kansai, and Kyushu regions 33,024,000 shares (1.5%) 3-2, Nakano 4-chome, Nakano-ku, Tokyo 164-8701, Japan Tel: 03-4574-4700 (Receptionist) Total sales floor area 417,500 m2 (14.8%) Tel: 03-4574-0101 (Receptionist) *2 Individuals and others includes 8,703,268 shares of treasury stock. -

Stoxx® Japan 600 Esg-X Index

STOXX® JAPAN 600 ESG-X INDEX Components1 Company Supersector Country Weight (%) Toyota Motor Corp. Automobiles & Parts Japan 3.87 Sony Corp. Consumer Products & Services Japan 2.55 Softbank Group Corp. Telecommunications Japan 2.44 Keyence Corp. Industrial Goods & Services Japan 1.77 RECRUIT HOLDINGS Industrial Goods & Services Japan 1.54 Mitsubishi UFJ Financial Group Banks Japan 1.48 Shin-Etsu Chemical Co. Ltd. Chemicals Japan 1.36 Nippon Telegraph & Telephone C Telecommunications Japan 1.36 Nintendo Co. Ltd. Consumer Products & Services Japan 1.30 Nidec Corp. Technology Japan 1.30 Fast Retailing Co. Ltd. Retail Japan 1.25 Daikin Industries Ltd. Construction & Materials Japan 1.19 Takeda Pharmaceutical Co. Ltd. Health Care Japan 1.18 Tokyo Electron Ltd. Technology Japan 1.16 Honda Motor Co. Ltd. Automobiles & Parts Japan 1.10 Daiichi Sankyo Co. Ltd. Health Care Japan 1.08 Sumitomo Mitsui Financial Grou Banks Japan 1.04 Murata Manufacturing Co. Ltd. Technology Japan 1.03 KDDI Corp. Telecommunications Japan 1.02 Hitachi Ltd. Industrial Goods & Services Japan 0.92 Itochu Corp. Industrial Goods & Services Japan 0.92 Fanuc Ltd. Industrial Goods & Services Japan 0.90 Hoya Corp. Health Care Japan 0.84 Mitsubishi Corp. Industrial Goods & Services Japan 0.83 Mizuho Financial Group Inc. Banks Japan 0.76 SOFTBANK Telecommunications Japan 0.75 Denso Corp. Automobiles & Parts Japan 0.72 Mitsui & Co. Ltd. Industrial Goods & Services Japan 0.71 Tokio Marine Holdings Inc. Insurance Japan 0.70 Oriental Land Co. Ltd. Travel & Leisure Japan 0.68 SMC Corp. Industrial Goods & Services Japan 0.68 Mitsubishi Electric Corp. Industrial Goods & Services Japan 0.67 Seven & I Holdings Co. -

Internet Disclosure Accompanying the Notice of Convocation the 117Th Ordinary General Meeting of Shareholders (Voluntary Disclosure)

March 6, 2017 Internet Disclosure Accompanying the Notice of Convocation The 117th Ordinary General Meeting of Shareholders (Voluntary Disclosure) Voluntary Disclosure Relating to “3. Matters Concerning Shares Held by the Company” on the Business Report of the Company The 30 Largest Stock-Holdings of Publicly Listed Companies in the Amount on the Balance Sheet, Which the Company Holds for Purposes Other Than Realizing Direct Investment Gains ································································································· 1 Voluntary Disclosure Relating to “5. Matters Concerning Status of Corporate Governance and Directors, Audit & Supervisory Board Members and Corporate Officers of the Company” of the Business Report of the Company Criteria for Independence of “External Directors and Audit & Supervisory Board Members” ······························································································· 2 Criteria for “Important Concurrent Position” Assumed by Company’s Directors and Audit & Supervisory Board Members···························································· 6 Criteria for Stating the Relationship between the Company and the Organizations in Which the Company’s Directors and Audit & Supervisory Board Members Hold “Important Concurrent Positions” ················································································· 7 The 30 Largest Stock-Holdings of Publicly Listed Companies in the Amount on the Balance Sheet, Which the Company Holds for Purposes Other Than Realizing Direct Investment -

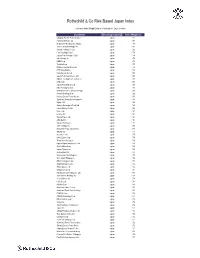

Rothschild & Co Risk-Based Japan Index

Rothschild & Co Risk-Based Japan Index Indicative Index Weight Data as of January 31, 2020 on close Constituent Exchange Country Index Weight (%) Chugoku Electric Power Co Inc/ Japan 1.01 Yamada Denki Co Ltd Japan 0.91 McDonald's Holdings Co Japan L Japan 0.88 Sushiro Global Holdings Ltd Japan 0.82 Skylark Holdings Co Ltd Japan 0.82 Fast Retailing Co Ltd Japan 0.78 Japan Post Holdings Co Ltd Japan 0.78 Ain Holdings Inc Japan 0.78 KDDI Corp Japan 0.77 Toshiba Corp Japan 0.75 Mizuho Financial Group Inc Japan 0.74 NTT DOCOMO Inc Japan 0.73 Kobe Bussan Co Ltd Japan 0.72 Japan Post Insurance Co Ltd Japan 0.69 Nippon Telegraph & Telephone C Japan 0.69 LINE Corp Japan 0.69 Japan Post Bank Co Ltd Japan 0.68 Nitori Holdings Co Ltd Japan 0.67 MS&AD Insurance Group Holdings Japan 0.66 Konami Holdings Corp Japan 0.66 Kyushu Electric Power Co Inc Japan 0.65 Sumitomo Realty & Development Japan 0.65 Fujitsu Ltd Japan 0.63 Suntory Beverage & Food Ltd Japan 0.63 Japan Airlines Co Ltd Japan 0.62 NEC Corp Japan 0.61 Lawson Inc Japan 0.60 Sekisui House Ltd Japan 0.60 ABC-Mart Inc Japan 0.60 Kyushu Railway Co Japan 0.60 ANA Holdings Inc Japan 0.59 Mitsubishi Heavy Industries Lt Japan 0.58 ORIX Corp Japan 0.57 Secom Co Ltd Japan 0.57 Seiko Epson Corp Japan 0.56 Trend Micro Inc/Japan Japan 0.56 Nippon Paper Industries Co Ltd Japan 0.56 Suzuki Motor Corp Japan 0.56 Japan Tobacco Inc Japan 0.55 Aozora Bank Ltd Japan 0.55 Sony Financial Holdings Inc Japan 0.55 West Japan Railway Co Japan 0.54 MEIJI Holdings Co Ltd Japan 0.54 Sugi Holdings Co Ltd Japan 0.54 Tokyo -

List:The 2019 Competitive IT Strategy Companies

Selection of Companies for 2019 Competitive IT Strategy Company Stock Selection and and Noteworthy IT Strategy Companies Programs Announced - METI and the TSE selected outstanding listed companies implementing a Competitive IT Strategy to enhance corporate value - The Ministry of Economy, Trade and Industry (METI) and the Tokyo Stock Exchange (TSE) have jointly been conducting a selection of outstanding companies for their efforts for IT utilization under the Competitive IT Strategy Company Stock Selection program. METI hereby announces that METI and the TSE have selected 29 companies under the 2019 Competitive IT Strategy Company Stock Selection program and 20 companies under the 2019 Noteworthy IT Strategy Companies program. These programs were held five times this year. 1. Outline of the Competitive IT Strategy Company Stock Selection program The program targets TSE-listed companies proactively engaging in efforts for IT utilization to improve management innovations, earnings and productivity in terms of improving mid- to long-term corporate value and fortifying competitiveness. METI and the TSE select such companies among all TSE-listed companies as Competitive IT Strategy Company Stocks by sector and introduce them to the public. In the 2019 program, METI and the TSE assessed companies that have been engaging in promotion of efforts for digital transformation (DX)* in accordance with the DX Promotion Guidelines and whose management has strongly been committed to such efforts. To assess companies’ current efforts for IT utilization, METI conducted a survey titled “2019 Survey of Competitive IT Strategies,” targeting all TSE-listed companies. In screening candidate companies, METI assigned scores to the responses concerning the following five areas and financial situation, and finally selected 29 companies screened by the final examination of the examination committee. -

VIRTUS ALLIANZGI INTERNATIONAL SMALL-CAP FUND SCHEDULE of INVESTMENTS (Unaudited) JUNE 30, 2021

VIRTUS ALLIANZGI INTERNATIONAL SMALL-CAP FUND SCHEDULE OF INVESTMENTS (Unaudited) JUNE 30, 2021 ($ reported in thousands) Shares Value Shares Value Shares Value PREFERRED STOCK—1.4% Germany—continued Netherlands—continued Jenoptik AG 36,671 $ 1,003 ASR Nederland NV 28,191 $ 1,090 Germany—1.4% Scout24 AG 12,804 1,080 Jungheinrich AG 24,964 $ 1,220 2,396 7,828 TOTAL PREFERRED STOCK New Zealand—0.4% (Identified Cost $558) 1,220 Hong Kong—4.0% Eroad Ltd.(1) 77,475 338 Hutchmed China Ltd. ADR(1) 32,400 1,272 Norway—3.2% COMMON STOCKS—96.6% (1) Melco International Elkem ASA 382,528 1,392 (1) Storebrand ASA 157,554 1,427 Australia—5.4% Development Ltd. 313,000 575 ALS Ltd. 110,041 1,076 Techtronic Industries Co., 2,819 Ansell Ltd. 8,707 284 Ltd. 36,000 629 Bapcor Ltd. 91,762 585 VTech Holdings Ltd. 92,600 975 South Korea—1.0% Nick Scali Ltd. 60,321 530 3,451 Koh Young Technology, Inc. 41,490 877 Northern Star Resources Sweden—2.9% Ltd. 32,100 235 Ireland—1.6% AAK AB 53,435 1,198 Openpay Group Ltd.(1) 87,481 94 Grafton Group plc 86,460 1,372 Elekta AB Class B 88,983 1,289 Paradigm Biopharmaceuticals Italy—2.7% 2,487 Ltd.(1) 182,378 287 Buzzi Unicem SpA 44,177 1,172 Pro Medicus Ltd. 21,200 934 ERG SpA 41,083 1,218 Switzerland—4.8% Starpharma Holdings Ltd.(1) 585,545 657 2,390 Georg Fischer AG 1,100 1,632 Interroll Holding AG 389 1,543 4,682 Japan—26.4% OC Oerlikon Corp. -

2019 Investment Stewardship Annual Report

2019 Investment Stewardship Annual Report August 2019 Annual Report Navigating long-term change – 3 Active the year in review 2018-2019 Investment Stewardship 4 stewardship: highlights creating long- Our achievements 5 Our principles, guidelines, priorities, 7 term value and commentaries The Investment Stewardship Engagement and voting case studies 10-22 Annual Report provides an • Board quality and effectiveness remain overview of BlackRock’s approach our primary focus • Corporate strategy and capital allocation to corporate governance and • Executive compensation stewardship in support of long- • Environmental risk and opportunities term value creation for our clients. • Human capital management as an In this report we provide practical investment issue examples of the BlackRock Spotlight on activism 23 Investment Stewardship (BIS) Engagement and voting statistics 24 team’s work over the year, Investor perspective and public policy 25 distilling some of the trends and Industry affiliations and memberships 28 company-specific situations reported in our regional quarterly Appendix reports. We emphasize the List of companies engaged 31 outcome of our engagements with BlackRock’s 2019 PRI assessment 38 companies, including some which report and score have spanned several years. We also provide examples of where we have contributed to the public discourse on corporate Our Annual Report reporting period is July 1, 2018 to June 30, 2019, representing the Securities and Exchange governance and investment Commission’s (SEC) 12-month reporting period for US mutual funds, including iShares. stewardship. Navigating long-term change – the year in review The adage “change is the only constant” has never been more true than in the past year.