Bank Muscat Online Account Statement

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Introduction Bank Muscat Is the Largest Bank of Sultanate of Oman. It Is a Joint Stock Company That Typically Offers Wide Variet

Introduction Bank Muscat is the largest bank of Sultanate of Oman. It is a joint stock Company that typically offers wide variety of financial and banking products and services to individuals and organizations. The banking services offered typically include a variety of retail, private, investment banking and numerous other services. In addition, Bank Muscat is also known to offer asset management, treasury and capital market products to different individuals and business customers in Sultanate of Oman. Bank Muscat is headquartered in Ruwi, Oman. The overall aim of the report is to carry out the SWOT analysis of the Bank Muscat and analyzes as how strength' weakness, opportunity and threats will influence the growth in revenue of Bank Muscat. Eventually report justifies and recommends whether Bank Muscat corporate goal should be to increase sales revenue by approximate 10% every year for the 5 years. Discussion and Analysis Bank Muscat enjoys a reputable status in Oman with the largest customer base. In Bank Muscat, market has been segmented depending upon on the people that have diverse banking needs and accordingly bank targets Individuals and Businesses. Below is performed SWOT analysis of the Bank Muscat SAOG. This comprehensive SWOT analysis of the Bank Muscat provides thorough information about company’s strengths, weaknesses, opportunities and threats. Next couples of paragraphs review these in detail. Strengths – The biggest strength of Bank Muscat is the already established network. It already has a network of 130 branches, 400 ATMs, 140+ CDMs and 4500 PoS terminals. In fact, it is the largest bank in Oman and that’s its USP. -

Review of U.S. Treasury Department's License to Convert Iranian Assets

United States Senate PERMANENT SUBCOMMITTEE ON INVESTIGATIONS Committee on Homeland Security and Governmental Affairs Rob Portman, Chairman Review of U.S. Treasury Department’s License to Convert Iranian Assets Using the U.S. Financial System MAJORITY REPORT PERMANENT SUBCOMMITTEE ON INVESTIGATIONS UNITED STATES SENATE REVIEW OF U.S. TREASURY DEPARTMENT’S LICENSE TO CONVERT IRANIAN ASSETS USING THE U.S. FINANCIAL SYSTEM TABLE OF CONTENTS I. EXECUTIVE SUMMARY ....................................................................................... 1 II. FINDINGS OF FACTS AND RECOMMENDATIONS ......................................... 5 III. BACKGROUND ...................................................................................................... 8 A. United States’ Sanctions Against Iran ............................................................ 8 1. The Joint Plan of Action ...................................................................................... 9 2. The Joint Comprehensive Plan of Action .......................................................... 10 B. United States Sanctions Enforcement ........................................................... 12 1. The United States Treasury Department ......................................................... 12 a. OFAC can Authorize Otherwise Prohibited Transactions using General Licenses and Specific Licenses ................................................................................. 14 2. The United States Department of State .......................................................... -

Global Finance: Euromoney: CPI Financial: Banker

About bank muscat With assets worth over USD 22 billion, bank muscat is the leading financial services provider in Oman. The bank has a strong presence in Corporate Banking, Retail Banking, Investment Banking, Islamic Banking, Treasury, as well as Private Banking and Asset Management. The bank’s biggest footprint and presence across the Sultanate and world class products and services are helping to make the vital differentiation, with the focus on its ‘Let’s Do More’ vision. The bank has the largest network in Oman consisting of 148 branches, 622 ATMs/CDMs and more than 11,000 PoS terminals. The international operations consist of a branch each in Riyadh (Kingdom of Saudi Arabia), Kuwait and a Representative Office each in Dubai (UAE) and Singapore. bank muscat currently owns 97% stake in Muscat Capital LLC, a brokerage and investment banking entity in Saudi Arabia. Main awards received by bank muscat Global Finance: Best Bank, Oman (2015,2014, 2013, 2011, 2010, 2009, 2008, 2007, 2006, 2005, 2004, 2003, 2002) Safest Bank in Oman (2015, 2014) Best Forex Bank and Provider, Oman (2015, 2014, 2013, 2012, 2011, 2010, 2009, 2008, 2007, 2006, 2005, 2004) Best Trade Finance Bank and Provider, Oman (2015, 2014, 2013, 2012, 2011, 2010, 2009, 2008, 2007, 2006, 2005, 2004) Best Consumer Internet Bank, Oman (2013, 2012, 2011, 2010, 2009, 2007, 2006, 2005, 2004) Best Investment Bank, Oman (2015, 2014, 2013, 2012, 2011, 2010, 2009) Best Islamic Financial Institution (2015, 2014, 2013) for Meethaq Euromoney: Best Bank, Oman (2015, 2014, 2013, 2012, 2011, -

Charges VAT Amount OMR Inclusive in OMR in OMR of VAT

Bank Muscat. Better Everyday. Total Amount in Sr No. Charge Type Charge Particulars Bank Charges VAT Amount OMR inclusive in OMR in OMR of VAT Bank Charges F062 Version: 1.7 / August / 2021 - 1 - Bank Muscat. Better Everyday. Total Amount in Sr No. Charge Type Charge Particulars Bank Charges VAT Amount OMR inclusive in OMR in OMR of VAT 1 Savings Account Per month (if balance falls 0.500 0.025 0.525 below OMR 100) Salary below OMR 500 per Nil Nil Nil 1.1 Ledger Fees month Account purpose to receive Nil Nil Nil pension or other social support allowance being granted by the Government 1.2 Foreign currency Per month, if balance falls 0.500 0.025 0.525 Account Ledger fees below to equivalent of 100 OMR Eligibility & minimum balance 1.3 Interest* OMR 100. Paid on semi annual 0.50% N/A 0.50% basis 2 Current Account Per month (if balance falls 0.500 0.025 0.525 below OMR 200) Salary below OMR 500 per Nil Nil Nil 2.1 Ledger Fees month Account purpose to receive Nil Nil Nil pension and other social support allowance being granted by the Government 2.2 Foreign currency Per month, if balance falls 0.500 0.025 0.525 Account Ledger fees below to equivalent of 200 OMR 10 leaves 1.000 0.050 1.050 2.3 Cheque Book 25 leaves 2.000 0.100 2.100 Charges 50 leaves 3.000 0.150 3.150 100 leaves 5.000 0.250 5.250 Returned for lack of funds 15.000 0.750 15.750 2.4 Cheque Return Charges Returned for other reasons 10.000 0.500 10.500 2.5 Stop Payment Per instruction (Single or Bunch 5.000 0.250 5.250 of cheques) for a day Handling or post Dated 5.000 0.250 5.250 2.6 Post Dated Cheques Cheques (Per/ Cheque) Individual 10.000 0.500 10.500 2.7 Removing Name from Caution List Corporate 20.000 1.000 21.000 3 Call Account If balance falls below Monthly 3.1 Call Accounts Ledger Fees OMR 1,000 2.000 0.100 2.100 F062 Version: 1.7 / August / 2021 - 1 - Bank Muscat. -

Bank Muscat (SAOG) NOTES to the CONSOLIDATED FINANCIAL STATEMENTS YEAR ENDED 31 DECEMBER 2012

Bank Muscat (SAOG) NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS YEAR ENDED 31 DECEMBER 2012 1 LEGAL STATUS AND PRINCIPAL ACTIVITIES Bank Muscat (SAOG) (the Bank or the Parent Company) is a joint stock company incorporated in the Sultanate of Oman and is engaged in commercial and investment banking activities through a network of a hundred and thirty six branches within the Sultanate of Oman and one branch in Riyadh, Kingdom of Saudi Arabia and one in Kuwait. The Bank has representative offices in Dubai, United Arab Emirates and in Singapore. The Bank (Parent Company) has a 96.25% owned subsidiary in Riyadh, Kingdom of Saudi Arabia. The Bank operates in Oman under a banking licence issued by the Central Bank of Oman and is covered by its deposit insurance scheme. The Bank has its primary listing on the Muscat Securities Market. The Bank has recently obtained licence for its Islamic Banking window and has opened its first Islamic Banking branch on 20 January 2013. The Bank and its subsidiary (together, the Group) operate in Five countries (2011 -Four countries) and employed 3,210 employees as of 31 December 2012 (2011: 3,024). 2 BASIS OF PREPARATION 2.1 Statement of compliance The consolidated financial statements have been prepared in accordance with International Financial Reporting Standards (IFRS), the applicable regulations of the Central Bank of Oman, the requirements of the Commercial Companies Law of 1974, as amended and disclosure requirements of the Capital Market Authority of the Sultanate of Oman. The preparation of financial statements in conformity with IFRS requires management to make judgments, estimates and assumptions that affect the application of policies and reported amounts of assets and liabilities, income and expenses. -

Lebanon This Week

Issue 594 | July 29 - August 3, 2019 Economic Research & Analysis Department LEBANON THIS WEEK In This Issue Charts of the Week Economic Indicators...........................1 Capital Markets..................................1 Performance of Arab Stock Markets in First Seven Months of 2019 (% change)* Lebanon in the News..........................2 Budget law forecasts deficit of 7.6% of GDP in 2019 Lebanon's population to reach 6.4 million at the end of 2025 Ministry of Finance clarifies operations of offshore companies Fiscal deficit narrows by 18% to $2.4bn in first five months of 2019 Net foreign assets of financial sector down by $204m in June 2019 Payment cards reach 2.81 million at end- March 2019, ATMs total 2,014 Lebanon ranks 77th globally, seventh among Arab countries in terms of readiness for change Lebanon launches campaign to support in- dustrial sector Performance of the Beirut Stock Exchange* Lebanon and Iraq sign healthcare coopera- tion agreement Construction activity remains subdued in first quarter of 2019 Corporate Highlights .........................8 Byblos Bank's net profits at $60m in first half of 2019, foreign currency liquidity at 15.6% of deposits Stock market index down 14% in first seven months of 2019 Kafalat loan guarantees down 85% to $4.3m in first half of 2019 -XO $XJ 6HS 2FW 1RY 'HF -DQ )HE 0D U $SU 0D \ -XQ -XO Aggregate net profits of five listed banks *Capital Markets Authority Value Weighted Index down 5.5% to $570m in first half of 2019 Source: Local Stock Markets, Capital Markets Authority, S&P Dow Jones Indices, Byblos Bank Assurex's net earnings at $2.8m in 2018 Quote to Note Banking sector assets at $256bn at end-June 2019 ''We would like it to be an opportunity to go much farther in the implementation of re- forms.'' Ratio Highlights................................11 Risk Outlook ....................................11 H.E. -

Lebanon This Week

Issue 182 September 6-18, 2010 Economic Research & Analysis Department LEBANON THIS WEEK In This Issue Charts of the Week Economic Indicators.....................1 Total Insurance Penetration in Arab Countries at end-2009 (% of GDP) Capital Markets............................1 3.5 3.1 3.0 2.8 Lebanon in the News....................2 2.5 Lebanon ranks 112th globally, 13th in 2.5 2.3 2.2 Arab region in credit ratings 2.0 2.0 Political tensions to affect growth, short- term challenge is to rollover maturing 1.5 1.2 Eurobonds 1.0 0.9 1.0 0.8 Draft budget for 2011 projects fiscal 0.6 0.5 deficit at 27% of expenditures and 8.6% 0.5 of GDP 0.0 Balance of payments posts surplus of $2.3bn in first 7 months of 2010 UAE Egypt Qatar Jordan Oman Kuwait Coincident Indicator up 13.4% year-on- Lebanon Morocco Bahrain Tunisia Algeria year in July 2010 Saudi Arabia Lebanon ranks 92nd globally, 12th Total Insurance Penetration in Lebanon (% of GDP) among Arab countries in global competi- 3.5 tiveness Lebanese banks to comply with new sanctions on Iran 3.04 3.11 3.0 Lebanon ranks 9th in Arab world in con- 2.86 nectivity 2.92 2.94 Construction permits up 48% in first 7 months of 2010 2.63 2.5 2.56 Launch of Lebanese-Mexican Business Council Net public debt at $44.3bn at end-July 2010 2.0 Airport passengers up 11% in first 8 2003 2004 2005 2006 2007 2008 2009 months of 2010 Source: Swiss Re, Byblos Reserach Corporate Highlights ...................6 MEA's IPO indefinitely postponed Quote to Note BLC Bank acquires 10% stake in USB Bank "The current rapid growth, -

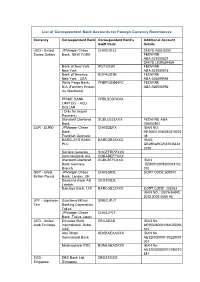

List of Correspondent Bank Accounts for Foreign Currency Remittances

List of Correspondent Bank Accounts for Foreign Currency Remittances Currency Correspondent Bank Correspondent Bank's Additional Account Swift Code Details USD - United JPMorgan Chase CHASUS33 CHIPS ABA:0002 States DoLLars Bank, NEW YORK FEDWIRE ABA:021000021 CHIPS UID#354459 Bank of New York, IRVTUS3N FEDWIRE New York ABA:021000018 Bank of America, BOFAUS3N FEDWIRE New York , USA. ABA:026009593 WeLLs Fargo Bank, PNBPUS3NNYC FEDWIRE N.A.(FormerLy Known ABA:026005092 As Wachovia) PRIME BANK PRBLBDDHXXX LIMITED - ACU DOLLAR ( OnLy for Import Payment) Standard Chartered SCBLUS33XXX FEDWIRE ABA: Bank 026002561 EUR - EURO JPMorgan Chase CHASDEFX IBAN NO: Bank, DE265011080062316023 Frankfurt,Germany 08 BARCLAYS BANK BARCGB22XXX IBAN: PLC GB28BARC2032536444 2255 Societe GeneraLe SOGEFRPPXXX Commerzbank AG COBADEFFXXX Standard Chartered SCBLDEFXXXX IBAN Bank Germany :DE50512305000018102 Branch 010 GBP - Great JPMorgan Chase CHASGB2L SORT CODE:609242 Britain Pound Bank, London, UK Deutsche Bank AG DEUTGB2L London BarcLays Bank, U.K. BARCGB22XXX SORT CODE: 203253 IBAN NO.: GB76 BARC 2032 5333 6065 46 JPY - Japanese Sumitomo Mitsui SMBCJPJT Yen Banking Corporation, Tokyo JPMorgan Chase CHASJPJT Bank, Tokyo,Japan AED - United Emirates Bank EBILAEAD IBAN No. Arab Emirates InternationaL, Dubai, AE950260001261025056 UAE 501 Abu Dhabi ADCBAEAAXXX IBAN No. CommerciaL Bank AE320030000100228001 001 Mashreqbank PSC. BOMLAEADXXX IBAN No. AE320330000010195510 887 SGD - DBS Bank Ltd, DBSSSGSG Singapore Singapore DoLLars SGD - Singapore DoLLars J P Morgan Chase CHASSGSGXXX Bank, N.A. SAR-Saudi NationaL CommerciaL NCBKSAJEXXX IBAN No. Arabian RiyaL Bank SA141000008834422300 0104 Saudi HoLLandi Bank, AAALSARI IBAN No. Riyadh SA415000000003100260 5275 AUD-AustraLian ANZ MeLbourne, ANZBAU3M BSB Code : 013024 DoLLars AustraLia JP MORGAN CHASE CHASAU2XXXX BSB Code : 212200 BANK, N.A. -

The Republic of Lebanon

THE REPUBLIC OF LEBANON The World Bank Group THIRD QUARTER 2003 A Quarterly Publication of the Lebanon Country Office Public Disclosure Authorized Public Disclosure Authorized In this edition Page · Editorial: Moving Together on the Portfolio 3 Public Disclosure Authorized · Privatization: From Panacea to Pr econditions 4 · Bank Group Operations 8 · Recent Economic Developments 10 · Fundamental Transitions for the Region’s Greatest Challenge 18 · News, Recent and Upcoming Activities 23 Public Disclosure Authorized · Recent World Bank Publications 25 Republic of Lebanon Update World Bank Contacts – Washington Joseph Saba, Country Director Shaha Riza, Acting Manager Tel. (202) 473-2992 - Fax (202) 477-1482 External Relations and Outreach E-mail: [email protected] Tel. (202) 458 1592 - Fax (202) 522 0006 Email: [email protected] Osman Ahmed, Lead Operations Officer Tel. (202) 473-7063 - Fax (202) 477-1482 Sabah Moussa, Executive Assistant E-mail: [email protected] Tel. (202) 473-9019 - Fax (202) 477-1482 E-mail: [email protected] Carlos Silva-Jauregui, Senior Economist Tel. (202) 473-1859 - Fax (202) 477-0432 Sereen Juma, Communications Associate E-mail: [email protected] Tel. (202) 473-7199 - Fax (202) 522-0003 E-mail: [email protected] Sophie Warlop, Operations Analyst Tel. (202) 473-7255 - Fax. (202) 477-1482 www.worldbank.org E-mail: [email protected] To Order World Bank Publications: World Bank Address: http://publications.worldbank.org/ecommerce 1818 H Street, NW Washington, DC 20433 For Information on World Bank Programs in Lebanon: www.worldbank.org/mna/lebanon World Bank Contacts – Beirut Omar Razzaz, Country Manager Hadia Samaha Karam, Operations Officer Tel. Ext. -

Bank Muscat Oryx Fund NAV: OMR 1.811 USD 4.7

To serve you better everyday August 2018 bank muscat Oryx Fund NAV: OMR 1.811 USD 4.7 Objective The Fund’s main objective to achieve long-term capital appreciation by investing in a diversified basket of equities listed on the MENA region stock exchanges. Fund Highlights Commentary Fund Manager Shirish Raut The regional markets were mixed in August with the overall S&P GCC Index Inception Date 05/09/94 dropping 2.5% MoM due to the pressure on index-heavyweight Saudi Banks amidst lower trading activity on account of the longer holidays across the region. Structure Open Ended Mutual Fund Oil prices rallied in the second half of the month, rising +4.3% MoM, as US sanctions on Iranian oil are expected to lead to tighter global crude supplies. Custodian bank muscat SAOG Markets were led by Egypt and Abu Dhabi, up 2.9% and 2.6% MoM, respectively. Strong corporate results have driven investors to reevaluate the Egyptian market Domicile Oman while the rally in Abu Dhabi was primarily driven by the rally in FAB. Oman also recovered 1.9% MoM from year lows while Qatar continues to surprise closing Benchmark S&P GCC Large Cap Index +0.6% MoM and 16.0% YTD. Saudi was the worst performing market, declining 4.2% MoM as foreign investors exited on low liquidity. Dubai continued to Currency OMR/USD decline, falling 3.9% MoM while Kuwait closed the month -0.7% MoM. Overall market liquidity was lower due to the Eid ul Azha holidays with Saudi trading USD Risk Profile High 849 mn on average per day (vs USD 978 mn on average YTD). -

The United States Hails Lebanon's Advanced Banking System

ABL Quarterly Newsletter Issue n° 3–October 2014 ABL’s “Economic Letter” free registration is available here: www.abl.org.lb The United States hails Lebanon’s operating in Lebanon are expected to come advanced banking system under pressure in the face of unfolding developments both in the country and the Lebanon has many advanced features in its region. economy and one of these interesting landmarks is there well-developed baking But S&P stressed that the business system, according to the United States confidence and economic recovery were Department of Commerce's 2014 Country gravelly affected by the political and Commercial Guide for Lebanon (CCG). security events that has plagued the country in recent years. It added that Lebanon's key advantages include a free-market economy, the The agency believes that Lebanon cannot absence of controls on the movement of insulate itself from the rapid and dramatic capital and foreign exchange, a well- in neighboring Syria although the banking developed banking system, a highly- sector, the main pillar of the economy, educated labor force, good quality of life, managed to weather all the major storms and limited restrictions on investors. and even achieved relative growth. This is not the first time the United States It emphasized that if the banking sector and other prominent countries heaped can prosper and grow if the political and praise on the Lebanese banks and the geopolitical risks receded. financial institutions which are seen as the main pillar of the economy. The report S&P insists that Lebanon has all elements expected the business climate to remain of quick economic recovery thanks to the sensitive to domestic and regional political strong financial sector, educated and security developments. -

IFC Mobile Money Scoping Country Report: Lebanon Alaa Abbassi, Andrew Lake, Cherine El Sayed

IFC Mobile Money Scoping Country Report: Lebanon Alaa Abbassi, Andrew Lake, Cherine El Sayed May, 2012 Lebanon Summary Overall readiness rating 4 (Moderately high readiness for Bank Centric Mobile Money deployment in high income segments) 3 (Medium readiness for the mid market, those unable to afford smart phones) Current mobile money solution The banks have begun implementing mobile money – both mobile payments and mobile banking. This is being done by the banks on their own and in conjunction with Mobile payments suppliers within Lebanon. Population 4.14 mil * Mobile Penetration 68% 2010 (High) ** Banked Population 2.5 mil (60%) (Moderately high) *** Remittance % of GDP Outbound $3,737 mil (9.7%) *** Inbound $7,558 mil (19.6%) *** Percent under poverty line 28% * Economically Active population 1,48 mil (36%) * Adult Literacy 87.4% * Main banks Bank Audi, Blom Bank, Byblos Bank, Fransabank, Bankmed, BLF MobileIFC Opportunities Network Operators MTC Touch 1,724,854 (54%) Alfa 1,482,819 (46%) Ease of doing business Ranked 104 in the world, better than Pakistan, worse than Seychelles **** Sources: * https://www.cia.gov/library/publications/the-world-factbook/geos/le.html ** TRA annual report 2010 *** http://elibrary-data.imf.org/DataReport.aspx?c=2529608&d=33060&e=161939 **** http://doingbusiness.org/rankings • Macro-economic Overview • Regulations • Financial Sector • Telecom Sector • Distribution Channel • Mobile Financial Services Landscape Macro-Economic Overview Key Country Statistics Insights • Population: 4.14 mil • Lebanon is a small country, both in terms of population size and geography. • Age distribution: 23% (0 – 14 years) 68% (15 - 64 years) 9% (>65 years) • It has a sophisticated banking industry which serves 60% of the population (2.48 mil • Urban/rural split: 87% urban people, through 900 branches).