Comprehensive Annual Financial Report for the Year Ended June 30, 2017

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Game Info 2018-19 South Carolina Men's Basketball

2018-19 SOUTH CAROLINA MEN’S BASKETBALL DIRECTOR OF ATHLETICS COMMUNICATIONS & PUBLIC RELATIONS: EMILY MILES // [email protected] CELL: 803-727-3284 // TWITTER: @EMILYMILES_SID GAMECOCK MEN’S BASKETBALL SOCIAL MEDIA: #GAMECOCKS TWITTER AND INSTAGRAM: @GAMECOCKMBB // FACEBOOK: /GAMECOCKMBB GAMECOCK ATHLETICS ON THE WEB: GAMECOCKSONLINE.COM GAME INFO ARENA: Colonial Life Arena (18,000) BROADCAST: SEC Network PLAY-BY-PLAY: Richard Cross ANAYLYST: Debbie Antonelli 2018-19 SCHEDULE OVERALL: 7-7 | SEC: 2-0 RADIO: Gamecock Radio Network IN COLUMBIA: 107.5 The Game : 5-4 | : 1-2 | : 1-1 HOME AWAY NEUTRAL PLAY-BY-PLAY: Derek Scott ANALYST: Casey Manning OCTOBER VS MISSOURI SIRIUS: 105 | XM: 190 26 Augusta + L, 77-72 GAMECOCKS (7-7, 2-0 SEC) (9-4, 0-1 SEC) WATCH: ESPN App NOVEMBER LIVE STATS: GamecocksOnline.com HEAD COACH: Frank Martin (FIU, ’93) HEAD COACH: Cuonzo Martin (Purdue, ’00) 6 USC Upstate W, 65-52 TICKETS: GamecocksOnline.com/1- 9 Stony Brook ^ L, 83-81 AT CAROLINA: 120-97 (7th season) AT MIZZOU: 29-17 (2nd season) 800-4SC-FANS/Colonial Life Arena 13 Norfolk State ^ W, 81-64 CAREER: 237-151 (12th season) CAREER: 215-138 (11th season) Box Office 17 vs. Providence # L, 76-67 VS. MIZZOU: 10-9 VS. CAROLINA: 4-0 18 George Washington # W, 90-55 TOP SCORER: Silva (12.8) TOP SCORER: Geist (13.8) SERIES: Mizzou leads, 5-4 26 Wofford L, 81-61 TOP REBOUNDER: Silva (7.1) TOP REBOUNDER: Tilmon (6.2) IN COLUMBIA: Tied, 2-2 30 Coastal Carolina W, 85-79 TOP ASSIST MAKER: Lawson (3.1) TOP ASSIST MAKER: Geist (2.9) TREND: The teams have split the last COMMUNICATIONS/PR: Emily Miles MEDIA RELATIONS: R.J. -

PHPP Brochure.Indd

the ArtS If you’re looking for Welcome to Palmetto Health culture, Columbia has it. Several and Columbia, SC art and history museums house nationally recognized collections. A variety of theatrical, dance and musical offerings can be experienced at The Koger Center for the Arts, Colonial Life Arena, Township Auditorium and the nearby Newberry Opera House. Music fans most likely SportS Sports fans can take in any number of spectator sports already know that Columbia in Columbia. A member of the Southeastern Conference, the is the home and starting place University of South Carolina hosts men’s and women’s basketball for the popular band, Hootie and the Blowfish. And unique to teams in its 12,401-seat Colonial Life Arena. The 72,400-seat South Carolina are a number of hometown festivals which celebrate Williams-Brice Stadium is home to USC’s football team. And just 90 traditions, seasons and landmarks. miles away in nearby Charlotte, N.C., Columbians can cheer on the Carolina Panthers, Charlotte Bobcats and Charlotte Sting, respective For additional information, please visit Central Carolina Association members of the NFL, NBA and WNBA. of Realtors at centralcarolinarealtors.com. Palmetto Health Baptist Palmetto Health Richland Palmetto Health Heart Hospital 803-296-7300 | palmettohealth.org/physicianpractices Palmetto Health Parkridge Palmetto Health Children’s Hospital Below are several websites that will allow you to gather additional information according to your interests and needs. Greater Columbia Chamber of Commerce | columbiachamber.com -

University of South Carolina

PRELIMINARY OFFICIAL STATEMENT DATED FEBRUARY 8, 2017 NEW ISSUE RATING: Moody’s: “Aa3” BOOK-ENTRY-ONLY (See “Rating” herein) In the opinion of McNair Law Firm, P.A., Bond Counsel, assuming continuing compliance by the University with certain covenants, interest on the Series 2017A Bonds is excludable from gross income for federal income tax purposes under existing statutes, regulations and judicial decisions. Interest on the Series 2017A Bonds is not an item of tax preference for purposes of the federal alternative minimum tax imposed on individuals or corporations. However, interest on the Series 2017A Bonds is included in the computation of adjusted current earnings for purposes of the alternative minimum tax for corporations. See “FEDERAL TAX EXEMPTION AND OTHER TAX MATTERS” for a brief description of certain other federal income tax consequences to certain recipients of interest on the Series 2017A Bonds. The Series 2017A Bonds and the interest thereon will also be exempt from all State, county, municipal and school district and other taxes or assessments imposed within the State of South Carolina, except estate, transfer and certain franchise taxes. See “FEDERAL TAX EXEMPTION AND OTHER TAX MATTERS.” $40,000,000* UNIVERSITY OF SOUTH CAROLINA ATHLETIC FACILITIES REVENUE BONDS SERIES 2017A Dated: March 1, 2017 Due: May 1, As Shown On Inside Cover The $40,000,000* Athletic Facilities Revenue Bonds, Series 2017A (the “Series 2017A Bonds”), of the University of South Carolina (the “University”) are being issued (i) to acquire, construct and equip the Football Operations Facility (as defined herein), and (ii) to pay the costs of issuance of the Series 2017A Bonds. -

The Daily Gamecock, MONDAY, JANUARY 14, 2013

University of South Carolina Scholar Commons January 2013 1-14-2013 The aiD ly Gamecock, MONDAY, JANUARY 14, 2013 University of South Carolina, Office oftude S nt Media Follow this and additional works at: https://scholarcommons.sc.edu/gamecock_2013_jan Recommended Citation University of South Carolina, Office of Student Media, "The aiD ly Gamecock, MONDAY, JANUARY 14, 2013" (2013). January. 13. https://scholarcommons.sc.edu/gamecock_2013_jan/13 This Newspaper is brought to you by the 2013 at Scholar Commons. It has been accepted for inclusion in January by an authorized administrator of Scholar Commons. For more information, please contact [email protected]. Game Changer January 14, 2013 Jeffrey Davis / The Link A2 Monday, January 14, 2013 Comedians top Carolina Communications VP to leave Productions spring calendar university this semester home to the West” to consider possible Shows, performers that wasn’t the typical lecture,” Lawrence to take in an internal email interim appointments total nearly $100,000 Telford said. “It’s a show that a lot job at UC Davis to top administrators this week and expects of campuses in the North do, so in late March Thursday. Lawrence USC will conduct a Sarah Ellis we thought we’d take a chance and came to USC after nationwide search [email protected] see how it would work down here.” Thad Moore six years as the vice for her permanent Other acts appearing on the [email protected] president for university replacement. Two big-na me net work spring calendar include: advancement at He also said his comedians are heading up — Bugsy Calhoun, a local poet, USC’s first-ever Oregon State considerations would Carolina Productions’ nearly at a spoken word event Feb. -

You're at AU, Now What?

You’re at AU, now what? PEER-TO-PEER GRADUATE LIFESTYLE AND SUCCESS GUIDE Disclaimer The information provided in this guide is designed to provide helpful information to (new) Augusta University students from their graduate student peers. This guide is not meant to be used, nor should it be used, as an official source of information. Students should refer to official Augusta University handbooks/guides/manual and website and their official program hand books for official policies, procedures and student information. Information provided is for informational purposes only and does not constitute endorsement of any people, places or resources. The views and opinions expressed in this guide are those of the authors and do not necessarily reflect the official policy or position of Augusta University and/or of all graduate students. The content included has been compiled from a variety of sources and is subject to change without notice. Reasonable efforts have been taken to ensure the accuracy and integrity of all information, but we are not responsible for misprints, out-of-date information or errors. Table of Contents Foreword and Acknowledgements Pages 4 - 5 Getting Started Pages 6 - 9 Augusta University Campuses Defined: Summerville and Health Sciences - Parking & Transportation Intra- and inter-campus transit Public Safety Email/Student Account - POUNCE - Financial Aid - Social Media Student Resources Pages 10 - 19 Student Services On Campus Dining Get Fit: The Wellness Center Services Provided by The Graduate School TGS Traditions Student Organizations From Student’s Perspectives: Graduate Programs at Augusta University Pages 20 - 41 Q&A with Current Graduate Students Choosing the Right Mentor for You: What Makes a Good Advisor? Additional Opportunities for Ph.D. -

Sindarius Thornwell 6-5 206 So

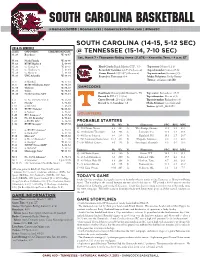

south carolina basketball @GamecockMBB | #Gamecocks | GamecocksOnline.com | #HereSC SOUTH CAROLINA (14-15, 5-12 SEC) 2014-15 schedule DATE OPPONENT TIME/BROADCAST @ TENNESSEE (15-14, 7-10 SEC) O. 26 Benedict + W, 92-47 Sat., March 7 • Thompson-Boling Arena (21,678) • Knoxville, Tenn. • 4 p.m. ET N. 14 North Florida W, 81-56 N. 18 RV/RV Baylor $ L, 69-65 N. 20 vs. Cornell % W, 69-45 Head Coach: Frank Martin (FIU, ’93) Top scorer: Notice (11.4) N. 21 vs. Charlotte % L, 65-63 Record At Carolina: 42-53 (3rd season) Top rebounder: Carrera (5.6) N. 23 vs. Akron % L, 68-63 Career Record: 159-107 (8th season) Top assist maker: Stroman (3.5) N. 26 UNC Asheville W, 89-75 Record vs. Tennessee: 0-4 Media Relations: Emily Feeney Twitter: @GamecockMBB D. 1 at Marshall W, 77-59 D. 6 RV/RV Oklahoma State ! W, 75-49 D. 19 Clemson W, 68-45 GAMECOCKS D. 21 Coker W, 78-52 D. 30 North Carolina A&T W, 91-54 Head Coach: Donnie Tyndall (Morehead St., ’93) Top scorer: Richardson (15.7) Record At UT: 15-14 (1st) Top rebounder: Moore (6.9) J. 3 vs. No. 9/9 Iowa State & W, 64-60 Career Record: 215-121 (10th) Top assist maker: Richardson (3.6) J. 7 Florida* L, 72-68 Record vs. S. Carolina: 1-0 Media Relations: Tom Satkowiak J. 10 at Ole Miss* L, 65-49 Twitter: @VOL_HOOPS J. 13 RV/RV Alabama* W, 68-66 J. 17 at Auburn* L, 71-68 J. -

NEPC Pastoral Profile.Indd

FFROMROM TTHEHE SSEARCHEARCH CCOMMITTEEOMMITTEE Northeast Presbyterian is a community of believers who connect people to God and each other through Christ by gathering, growing, and going. We celebrate through worship as we share life together. In God’s Spirit, we live out God’s Word and seek to disciple and grow mature believers. Our hearts are committed to refl ecting Christ’s love to our neighbors while sharing the gospel locally and globally. We invite you to explore the following pages, discovering Northeast Presbyterian’s 40-year history, built on the trustworthy foundations of God’s inerrant Word, faithful servant-leadership, and a Body of believers who ardently seek and follow Christ. We understand our fundamental weakness in light of God’s perfect strength, trusting Him to accomplish His great kingdom purposes through our frail human framework. Our committee is prayerfully expectant for the next season of our church. We are humbly grateful for the opportunity to serve our church in this holy calling to reveal the next Senior Pastor of NEPC. Please read and review windows into NEPC through our overviews and snapshots. Any questions may be directed to Dr. Charles McGowan. If you are interested in pursuing this opportunity, you may submit materials confi dentially to [email protected]. We are praying as you consider whether the Lord may be calling you to Northeast Presbyterian Church as our next Senior Pastor. 1 NNEPCEPC – MMEMBERSHIPEMBERSHIP aandnd BBUDGETUDGET IINFONFO 2 NNEPCEPC – OOURUR BBELIEFSELIEFS Northeast Presbyterian Church is a member of the Presbyterian Church in America (PCA), a denomination whose identifying statement is “Faithful to the Scriptures, True to the Reformed Faith, and Obedient to the Great Commission of Jesus Christ.” We believe those doctrines are formally expressed in the Westminster Confession of Faith together with its Larger and Shorter Catechisms. -

Welcome to Palmetto Health and Columbia, SC

Oh, the Weather! Columbia’s mild winters and ‘Famously Hot’ summers make almost every outdoor activity feasible year-round. While a mild dusting of snow every year or so guarantees a touch of winter, a round of golf in December is still highly possible. (The average annual snowfall is just 1.89 inches.) Whether on weeknights or weekends, Columbia is a melting pot of extracurricular activities. Below are several websites that will allow you to gather additional information according to your Recreation interests and needs. Parks with tennis courts and playgrounds, public and private clubs, and a dozen or so golf courses are available throughout the community. Hunting and fishing are popular in the outlying areas Greater Columbia Chamber of Commerce of the city. Weekend afternoons find families taking in the sounds of columbiachamber.com outdoor concerts in downtown 17-acre Finlay Park or jogging, biking or walking on paths that stretch through nearby Riverfront Park. Columbia, SC Convention and Visitors Bureau Riverbanks Zoo and Botanical Garden, popular among locals and columbiacvb.com out-of-towners alike, is ranked in the Top 10 zoos in the nation. And with several beautiful rivers running through Columbia, and with The State Newspaper Lake Murray nearby, Metropolitan Columbia has been ranked among thestate.com the top 10 canoe towns in the country by Paddler magazine. The University of South Carolina The Water’s Fine! sc.edu Only 10 minutes northwest of our city is the spectacular 50,000- acre manmade Lake Murray. Recognized as one of the nation’s top Richland County School District 1 largemouth bass fishing spots, Lake Murray delights residents and richlandone.org visitors along nearly 526 miles of shoreline. -

The Daily Gamecock, TUESDAY, FEBRUARY 10, 2009

University of South Carolina Scholar Commons February 2009 2-10-2009 The aiD ly Gamecock, TUESDAY, FEBRUARY 10, 2009 University of South Carolina, Office oftude S nt Media Follow this and additional works at: https://scholarcommons.sc.edu/gamecock_2009_feb Recommended Citation University of South Carolina, Office of Student Media, "The aiD ly Gamecock, TUESDAY, FEBRUARY 10, 2009" (2009). February. 14. https://scholarcommons.sc.edu/gamecock_2009_feb/14 This Newspaper is brought to you by the 2009 at Scholar Commons. It has been accepted for inclusion in February by an authorized administrator of Scholar Commons. For more information, please contact [email protected]. dailygamecock.com UNIVERSITY OF SOUTH CAROLINA TUESDAY, FEBRUARY 10, 2009 VOL. 102, NO. 92 ● SINCE 1908 Weather Have questions for your Student Government TODAY Debate nets poor turnout candidates? Send them to The Daily Gamecock HIGH 75° at gamecockeditor@ Two of 12 candidates last week in academics sc.edu to be submitted committee to get teachers for the SG debates discuss platforms, to work more with students Wednesday and TONIGHT on their book lists.” Thursday. Questions LOW 52° argue qualifi cations If elected to student directed to senatorial senate, Kevin Burke , a fi rst- candidates in the Josh Dawsey year undecided student, said College of Arts and STAFF WRITER he would look to implement Sciences, as well TOMORROW a business learning as candidates for HIGH 76° Of the 12 candidates community executive offi ce, running for the business similar to should be submitted school district (district 5) that of the by Tuesday at 5 p.m. of student senate, only two pre-med, Attend the next two Inside showed up to debate the pre-law and debates and if you miss merits of their platform in engineering them, check out our coverage the day after. -

3 Trustees Address 2 School Board Issues

3 trustees address 2 school board issues The Sumter Item talks key topics Contract, finances before with 6 senior school board members school board on Monday SUNDAY, MARCH 24, 2019 $1.75 BY BRUCE MILLS BY BRUCE MILLS ment con- SERVING SOUTH CAROLINA SINCE OCTOBER 15, 1894 [email protected] [email protected] tract with the district’s The scenario of financially investing more into ad- Finances — both in new super- ditional capital assets by the Sumter school board open session and closed intendent, over the quality of its teaching personnel when en- session — headline Sum- Penelope rollment is declining is a major issue many say the ter School District Board MARTIN-KNOX Martin- district’s trustees are facing. of Trustees’ next meet- Knox of Bal- 4 SECTIONS, 24 PAGES | VOL. 124, NO. 111 A second, and related, headline issue is the recent ing set for Monday night. timore response from Shaw Air Force Base leadership that A district spokeswom- County Public Schools. PANORAMA it is “troubled” by the board’s recent actions to re- an distributed the agen- Martin-Knox is sched- open Mayewood Middle School and revert against da for the board’s uled to begin her posi- the previous board’s school consolidation plan that monthly work session on tion with the district on was aimed at alleviating financial challenges in the Friday. July 1. She is replacing district. Shaw is Sumter County’s largest employer The trustees will begin Debbie Hamm, who is in and a key driver of the local economy. Monday at 5 p.m. -

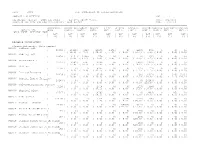

Fall 2009 S.C. COMMISSION on HIGHER EDUCATION PROGRAM : CHES607GDP PAGE: 1 ASSIGNABLE AREA by ROOM USE CODES

Fall 2009 S.C. COMMISSION ON HIGHER EDUCATION PROGRAM : CHES607GDP PAGE: 1 ASSIGNABLE AREA BY ROOM USE CODES (By Site Identifiers) DATE: 05/21/10 FUNCTION USE CODE FOR HOSPITAL EXCLUDED FROM REPORT TIME: 11:03:10 ________________________________________________________________________________________________________________________________ |ASSIGNABLE |CLASS RM|LABORAT |OFFICE |STUDY |SPECIAL |GENERAL |SUPPORT|HEALTH|RESIDENTIL|UNCLAS| INSTITUTION |AREA |FACIL. |FACIL. |FACIL. |FACIL. |FACIL. |FACIL. |FACIL. |FACIL.|FACIL. |FACIL.| BLDG-IDENT BUILDING NAME | ASF | ASF | ASF | ASF | ASF | ASF | ASF | ASF | ASF | ASF | ASF | | (%) | (%) | (%) | (%) | (%) | (%) | (%) | (%) | (%) | (%) | (%) | ________________________________________________________________________________________________________________________________ RESEARCH UNIVERSITIES Clemson University (Main Campus) 000001 Tillman Hall | 53800 | 10445| 4023| 26973| 1971| 0| 9856| 532| 0| 0| 0| ( 19.4) ( 7.4) ( 50.1) ( 3.6) ( 0.0) ( 18.3) ( 0.9) ( 0.0) ( 0.0) ( 0.0) 000003 Godfrey Hall | 28858 | 3161| 24093| 579| 0| 0| 0| 1025| 0| 0| 0| ( 10.9) ( 83.4) ( 2.0) ( 0.0) ( 0.0) ( 0.0) ( 3.5) ( 0.0) ( 0.0) ( 0.0) 000004 Holtzendorf Y | 25723 | 4582| 4781| 8699| 0| 0| 5060| 2601| 0| 0| 0| ( 17.8) ( 18.5) ( 33.8) ( 0.0) ( 0.0) ( 19.6) ( 10.1) ( 0.0) ( 0.0) ( 0.0) 000005 Mell Hall | 5130 | 0| 0| 4747| 0| 0| 272| 111| 0| 0| 0| ( 0.0) ( 0.0) ( 92.5) ( 0.0) ( 0.0) ( 5.3) ( 2.1) ( 0.0) ( 0.0) ( 0.0) 000006 Dillard Building | 16419 | 2622| 0| 3170| 0| 0| 705| 6351| 0| 240| 3331| ( 15.9) ( 0.0) ( -

April 29, 2019

The official minutes of the University of South Carolina Board of Trustees are maintained by the Secretary of the Board. Certified copies of minutes may be requested by contacting the Board of Trustees’ Office at [email protected]. Electronic or other copies of original minutes are not official Board of Trustees' documents. University of South Carolina BOARD OF TRUSTEES Buildings and Grounds Committee April 29, 2019 The Buildings and Grounds Committee of the University of South Carolina Board of Trustees met at 10:00 a.m. on Monday, April 29, 2019, in the Alumni Center’s C. Edward Floyd Boardroom. Members participating were: Mr. Miles Loadholt, Presiding Chairman; Mr. C. Dan Adams; Mr. J. Egerton Burroughs; Ms. Leah B. Moody; Mr. Eugene P. Warr Jr.; Mr. Thad H. Westbrook; Mr. John C. von Lehe Jr., Board Chairman; and Mr. Hubert F. Mobley, Board Vice Chairman; with Mr. Toney J. Lister joining by telephone. Mr. William C. Hubbard was absent. Other Trustees participating were: Mr. Chuck Allen; Mr. Robert F. Dozier Jr.; Mr. A. C. “Bubba” Fennell; Dr. C. Edward Floyd; Mr. Richard A. Jones Jr.; Ms. Rose Buyck Newton; Dr. C. Dorn Smith III; Mr. Mack I. Whittle Jr.; and Mr. Charles H. Williams. Also present were USC Columbia Faculty Senate Chairman Marco Valtorta and USC Columbia Student Government President Luke Rankin. Others present were: President Harris Pastides; Interim President-Elect and USC Upstate Chancellor Brendan Kelly; Secretary J. Cantey Heath Jr.; General Counsel Walter “Terry” H. Parham; Provost Joan Gabel; Chief Operating Officer Edward L. Walton; Vice President for Student Affairs Dennis A.