Highlights of Major General Construction Companies' Financial

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Published on July 21, 2021 1. Changes in Constituents 2

Results of the Periodic Review and Component Stocks of Tokyo Stock Exchange Dividend Focus 100 Index (Effective July 30, 2021) Published on July 21, 2021 1. Changes in Constituents Addition(18) Deletion(18) CodeName Code Name 1414SHO-BOND Holdings Co.,Ltd. 1801 TAISEI CORPORATION 2154BeNext-Yumeshin Group Co. 1802 OBAYASHI CORPORATION 3191JOYFUL HONDA CO.,LTD. 1812 KAJIMA CORPORATION 4452Kao Corporation 2502 Asahi Group Holdings,Ltd. 5401NIPPON STEEL CORPORATION 4004 Showa Denko K.K. 5713Sumitomo Metal Mining Co.,Ltd. 4183 Mitsui Chemicals,Inc. 5802Sumitomo Electric Industries,Ltd. 4204 Sekisui Chemical Co.,Ltd. 5851RYOBI LIMITED 4324 DENTSU GROUP INC. 6028TechnoPro Holdings,Inc. 4768 OTSUKA CORPORATION 6502TOSHIBA CORPORATION 4927 POLA ORBIS HOLDINGS INC. 6503Mitsubishi Electric Corporation 5105 Toyo Tire Corporation 6988NITTO DENKO CORPORATION 5301 TOKAI CARBON CO.,LTD. 7011Mitsubishi Heavy Industries,Ltd. 6269 MODEC,INC. 7202ISUZU MOTORS LIMITED 6448 BROTHER INDUSTRIES,LTD. 7267HONDA MOTOR CO.,LTD. 6501 Hitachi,Ltd. 7956PIGEON CORPORATION 7270 SUBARU CORPORATION 9062NIPPON EXPRESS CO.,LTD. 8015 TOYOTA TSUSHO CORPORATION 9101Nippon Yusen Kabushiki Kaisha 8473 SBI Holdings,Inc. 2.Dividend yield (estimated) 3.50% 3. Constituent Issues (sort by local code) No. local code name 1 1414 SHO-BOND Holdings Co.,Ltd. 2 1605 INPEX CORPORATION 3 1878 DAITO TRUST CONSTRUCTION CO.,LTD. 4 1911 Sumitomo Forestry Co.,Ltd. 5 1925 DAIWA HOUSE INDUSTRY CO.,LTD. 6 1954 Nippon Koei Co.,Ltd. 7 2154 BeNext-Yumeshin Group Co. 8 2503 Kirin Holdings Company,Limited 9 2579 Coca-Cola Bottlers Japan Holdings Inc. 10 2914 JAPAN TOBACCO INC. 11 3003 Hulic Co.,Ltd. 12 3105 Nisshinbo Holdings Inc. 13 3191 JOYFUL HONDA CO.,LTD. -

List of Exhibitors (As of May 18, 2015)

List of Exhibitors (As of May 18, 2015) Corporation/Organization Names (by alphabetical order) Central Japan Railway Company CTI Engineering Co., Ltd. DENSO CORPORATION East Japan Railway Company East Nippon Expressway Company Limited Central Nippon Expressway Company Limited West Nippon Expressway Company Limited Foundation of River &Basin Integrated Communications, JAPAN FUJITSU LIMITED Hanshin Expressway Hokkaido Railway Company Honda Motor Co., Ltd. Honshu-Shikoku Bridge Expressway Co., Ltd. Idemitsu Kosan Co.,Ltd. IHI Corporation ISHIDA CO.,LTD. ISUZU MOTORS LIMITED Japan Commission on Large Dams Japan Construction Information Center Japan Science and Technology Agency (JST) KAJIMA CORPORATION Kawasaki Heavy Industries,Ltd. Kyushu Railway Company Metropolitan Expressway Company Limited MITSUBISHI HEAVY INDUSTRIES, LTD. National Research and Development Agency, Public Works Research Institute (PWRI) NEC Corporation NEDO(New Energy and Industrial Technology Development Organization) NEWJEC Inc. NICHICON CORPORATION NIPPON KOEI CO,LTD. Nissan Motor Corporation NORITAKE CO.,LIMITED OBAYASHI CORPORATION OOIRI Co.,Ltd. Oriental Consultants Co., Ltd./Oriental Consultants Global Co., Ltd. OYO Corporation PACIFIC CONSULTANTS CO.,LTD. PanaHome Corporation Panasonic Production Engineering Co., Ltd PASCO CORPORATION SAMCO Inc. SHIMIZU CORPORATION TAISEI CORPORATION The Jiangsu Institution of Engineers The River Foundation Tohoku Regional Development Association Tokyo Metro Co., Ltd. TOYO CONSTRUCTION CO.,LTD Toyota Motor Corporation Water Resources Environment Center West Japan Railway Company List of Exhibitors (As of May 18, 2015) <"The Monodzukuri Nippon Grand Award" Category> Corporation/Organization Names (by alphabetical order) DENSO CORPORATION FUJI KIHAN CO.,LTD GIKEN LTD. KTX Corporation MITAKA KOHKI CO., LTD. Nippon Steel & Sumikin Stainless Steel Corporation O.N. INDUSTRIES LTD ZEROONE PRODUCTS, INC.. -

Conveying Our Feelings and Connecting Them to the Future

The Denka Gunbai No. Column 08 TheDenkaWay Summer Way 2021 Vol.08 Photo provided by Minamisanriku-cho Summer Denka Big Swan Stadium, a building that resembles a swan spreading its wings Breathing new life into Niigata’s sports culture 2021 A Stadium Bearing Vol.08 the Denka Name Nihonbashi Mitsui Tower, 2-1-1 Nihonbashi-muromachi, Chuo-ku, Tokyo 103-0022 Tokyo Chuo-ku, 2-1-1 Nihonbashi-muromachi, Tower, Nihonbashi Mitsui Satoshi Fukuoka / / Editor-in-chief: Ltd. Denka Co., Corporate Communications Dept., 2021/ Publisher: 1, July. Published: Have you heard of Niigata Stadium, also known as “Denka Big Swan Stadium,” located on the banks of the Toyanogata Lake in Niigata Prefecture? Constructed as one of the 2002 FIFA World Cup venues, Niigata Stadium celebrates its 20th anniversary this year. It has been recognized under the name of “Denka” since 2014, when Denka acquired the naming rights. Its distinctive design resembles a swan spreading its wings as if to take off. With a capacity of 40,000 people, it is also used as a home stadium for Albirex Niigata, a local soccer team in the J2 league. It has also been awarded the J league Best Pitch Award six times for its well-maintained pitch. Using this stadium as a base, Denka has been actively spons oring sporting events such as the Denka Athletics Challenge Cup*1, which has been held every year since 2019. Denka decided to acquire the naming rights due to its strong connection with Niigata Prefecture. Currently, around 2,000 employees, or one third of the entire Denka Group, work in Niigata prefecture. -

Updated on 3 October. 2016 Date Issue Code 20160930 Nippon

JPX-Nikkei Index 400 Component Stocks Weight and FFW Ratio Following Cap-adjustment Updated on 3 October. 2016 FFW Ratio Compornent Weight Date Issue Code Following Cap- (JPX-Nikkei Index 400) 20160930 Nippon Suisan Kaisha,Ltd. 1332 0.75000 0.0427% 20160930 INPEX CORPORATION 1605 0.65000 0.3699% 20160930 HAZAMA ANDO CORPORATION 1719 0.65000 0.0315% 20160930 TOKYU CONSTRUCTION CO., LTD. 1720 0.55000 0.0253% 20160930 COMSYS Holdings Corporation 1721 0.55000 0.0593% 20160930 TAISEI CORPORATION 1801 0.80000 0.3028% 20160930 OBAYASHI CORPORATION 1802 0.75000 0.2309% 20160930 SHIMIZU CORPORATION 1803 0.70000 0.2126% 20160930 HASEKO Corporation 1808 0.70000 0.0870% 20160930 KAJIMA CORPORATION 1812 0.80000 0.2549% 20160930 Sumitomo Mitsui Construction Co., Ltd. 1821 0.85000 0.0281% 20160930 Kumagai Gumi Co.,Ltd. 1861 0.70000 0.0294% 20160930 DAITO TRUST CONSTRUCTION CO.,LTD. 1878 0.85000 0.4596% 20160930 NIPPO CORPORATION 1881 0.35000 0.0342% 20160930 MAEDA ROAD CONSTRUCTION CO.,LTD. 1883 0.60000 0.0436% 20160930 Sumitomo Forestry Co.,Ltd. 1911 0.70000 0.0715% 20160930 DAIWA HOUSE INDUSTRY CO.,LTD. 1925 0.80000 0.6287% 20160930 Sekisui House,Ltd. 1928 0.85000 0.4418% 20160930 KYOWA EXEO CORPORATION 1951 0.60000 0.0434% 20160930 KYUDENKO CORPORATION 1959 0.50000 0.0531% 20160930 JGC CORPORATION 1963 0.70000 0.1355% 20160930 Nihon M&A Center Inc. 2127 0.65000 0.0701% 20160930 Temp Holdings Co.,Ltd. 2181 0.50000 0.0891% 20160930 Cookpad Inc. 2193 0.35000 0.0155% 20160930 EZAKI GLICO CO.,LTD. 2206 0.60000 0.1091% 20160930 CALBEE,Inc. -

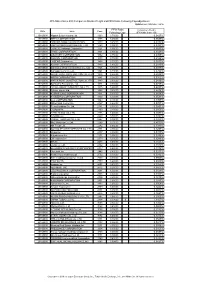

JPX-Nikkei Index 400 Constituents (Applied on August 31, 2021) Published on August 6, 2021 No

JPX-Nikkei Index 400 Constituents (applied on August 31, 2021) Published on August 6, 2021 No. of constituents : 400 (Note) The No. of constituents is subject to change due to de-listing. etc. (Note) As for the market division, "1"=1st section, "2"=2nd section, "M"=Mothers, "J"=JASDAQ. Code Market Divison Issue Code Market Divison Issue 1332 1 Nippon Suisan Kaisha,Ltd. 3048 1 BIC CAMERA INC. 1417 1 MIRAIT Holdings Corporation 3064 1 MonotaRO Co.,Ltd. 1605 1 INPEX CORPORATION 3088 1 Matsumotokiyoshi Holdings Co.,Ltd. 1719 1 HAZAMA ANDO CORPORATION 3092 1 ZOZO,Inc. 1720 1 TOKYU CONSTRUCTION CO., LTD. 3107 1 Daiwabo Holdings Co.,Ltd. 1721 1 COMSYS Holdings Corporation 3116 1 TOYOTA BOSHOKU CORPORATION 1766 1 TOKEN CORPORATION 3141 1 WELCIA HOLDINGS CO.,LTD. 1801 1 TAISEI CORPORATION 3148 1 CREATE SD HOLDINGS CO.,LTD. 1802 1 OBAYASHI CORPORATION 3167 1 TOKAI Holdings Corporation 1803 1 SHIMIZU CORPORATION 3231 1 Nomura Real Estate Holdings,Inc. 1808 1 HASEKO Corporation 3244 1 Samty Co.,Ltd. 1812 1 KAJIMA CORPORATION 3254 1 PRESSANCE CORPORATION 1820 1 Nishimatsu Construction Co.,Ltd. 3288 1 Open House Co.,Ltd. 1821 1 Sumitomo Mitsui Construction Co., Ltd. 3289 1 Tokyu Fudosan Holdings Corporation 1824 1 MAEDA CORPORATION 3291 1 Iida Group Holdings Co.,Ltd. 1860 1 TODA CORPORATION 3349 1 COSMOS Pharmaceutical Corporation 1861 1 Kumagai Gumi Co.,Ltd. 3360 1 SHIP HEALTHCARE HOLDINGS,INC. 1878 1 DAITO TRUST CONSTRUCTION CO.,LTD. 3382 1 Seven & I Holdings Co.,Ltd. 1881 1 NIPPO CORPORATION 3391 1 TSURUHA HOLDINGS INC. 1893 1 PENTA-OCEAN CONSTRUCTION CO.,LTD. -

OBAYASHI CORPORATION Summary of the Second Quarter (Cumulative) Financial Results for FY2015 Ending March 2016

OBAYASHI CORPORATION Summary of the Second Quarter (cumulative) Financial Results for FY2015 Ending March 2016 Disclaimer: This financial information, a digest of Obayashi Corporation's "Summary of the Second Quarter (cumulative) Financial Results for FY2015 ending March 2016" ("Kessan Tanshin") disclosed at the Tokyo Stock Exchange on November 10, 2015 was translated into English and presented solely for the convenience of non-Japanese speaking users. If there is any discrepancy between Japanese "Kessan Tanshin" and this document, Japanese "Kessan Tanshin" will prevail. This document includes forward-looking statements based on the information available at the time of the release of Japanese "Kessan Tanshin". Due to various factors, the actual results may vary from the forward-looking statements contained herein. Obayashi Corporation (non-consolidated) is called the "Company" hereinafter. (Rounded down to the nearest million yen) 1. Summary of the Second Quarter (cumulative) Results for FY2015 ending March 2016 (April 1, 2015 - September 30, 2015) (1) Consolidated Business Results (cumulative) (% shows the increase (decrease) from the results of the same quarter of the previous FY.) Profit attributable to Net Sales Operating Income Ordinary Income owners of parent (Unit: million yen) % (Unit: million yen) % (Unit: million yen) % (Unit: million yen) % 2nd Quarter of FY2015 834,626 2.9 42,538 152.7 45,537 104.6 27,886 96.7 2nd Quarter of FY2014 810,786 12.0 16,831 100.1 22,257 85.4 14,179 124.7 (Note) Comprehensive income: [2Q/FY2015] -1,231 -

Fukushima Dai-Ichi

Fukushima Dai-ichi Short overview of 11 March 2011 accidents and considerations Marco Sangiorgi - ENEA 3rd EMUG Meeting – ENEA Bologna 11-12 April 2011 NPPs affected by Earthquake NPPs affected by Earthquake Tōkai Nuclear Power Plant The Tōkai Nuclear Power Plant (東海発電所 Tōkai hatsudensho , Tōkai NPP) was Japan's first nuclear power plant. It was built in the early 1960s to the British Magnox design, and generated power from 1966 until it was decommissioned in 1998. A second nuclear plant, built at the site in the 1970s, was the first in Japan to produce over 1000 MW of electricity, and still produces power as of 2009. The site is located in Tokai in the Naka District in Ibaraki Prefecture, Japan and is operated by the Japan Atomic Power Company . Unit Type Average electric Capacity Construction Construction First criticality Closure power started completed Tōkai I Magnox (GCR) 159 MW 166 MW March 1, 1961 November 10, July 25, 1966 March 31, 1965 1988 Tōkai II BWR/5 1060 MW 1100 MW October 3, 1973 March 13, 1978 November 28, 1978 NPPs affected by Earthquake Onagawa Nuclear Power Plant The Onagawa Nuclear Power Plant (女川原子力発電所 Onagawa genshiryoku hatsudensho , Onagawa NPP) is a nuclear power plant in Onagawa in the Oshika District and Ishinomaki city, Miyagi Prefecture, Japan. It is managed by the Tohoku Electric Power Company . It was the most quickly constructed nuclear power plant in the world. The Onagawa-3 unit was the most modern reactor in all of Japan at the time of its construction. It was used as a prototype for the Higashidori Nuclear Power Plant. -

Joint Company Information Session in Civil Engineering for International Students

Joint Company Information Session in Civil Engineering for International Students ------------------------------------------------------------------------------------------------------------------------------------------- Date & Time : 6th of July, 2013 (Sat) 13:00-17:00 Venue : Japan Society of Civil Engineers (JSCE) Yotsuya 1chome, Shinjyuku-ku, Tokyo Participant companies : JFE Engineering Corporation, Katahira & Engineers Inc., Obayashi Corporation, Shimizu Corporation, Chodai Co., Ltd., Eight-Japan Engineering Consultants Inc., Nippon Koei Co., Ltd., Obayashi Road Corporation, Oriental Consultants Co., Ltd., East Nippon Expressway Company Limited, NEXCO-East Engineering Company Limited, Nippon Road Co., Toda Corporation Organizer : International Students Network Group, International Activities Centre, JSCE ------------------------------------------------------------------------------------------------------------------------------------------- International Students Network Group, JSCE, held a Joint Company Information Session in Civil Engineering for International Students at the JSCE headquarter in Tokyo on 6th July. It aimed to provide international students with information on Japanese construction companies and job opportunities. 13 construction companies participated and 8 out of them gave a presentation to introduce their business activities. Also, those companies set up their booths to meet the international students. Total 55 international students Opening Session attended mainly from universities in the Kanto region (area -

Smart Grid Demonstration in Commercial Areas in Albuquerque, NM

Smart Grid Demonstration in Commercial Areas in Albuquerque, NM Atsushi Denda Shimizu Institute of Technology (SIT) Shimizu Corporation September, 2010 Profile of Shimizu Corporation •Founded in 1804 in Edo (present-day Tokyo) •Capital US$ 797,141 thousand in FY2009 •Employees 11,369 (As of April, 2010) •Consolidated net sales US$ 17.0 billion in FY2009 •Main business Project planning, designing and construction Facility management, maintenance and renovation http://www.shimz.co.jp/english/index.html Shimizu Institute of Technology (SIT) •193 researchers and 64 staffs •Total R&D budgets in 2010 US$ 82.4 Million Breakdown of researchers Physics, Geology, Social Eng., etc 20% Architectural Chemistry 4% Engineering Mechanical 46% Engineering 4% Electronics 8% Civil Engineering 18% History of Shimizu Smart Grid 2006 Urban Micro Grid (Japan) 2008 PV Micro Grid (China) 2011Smart Grid (United States) Microgrid system in SIT Microgrid control system Exhaust heat utilization Exhaust heat recovery Gas engine gen. 350kW 排熱回収Absorption water heater-chiller Gas engine gen. 90kW Nickelmetalhydritebattery 40kW x 10hrs Thermal energy storage Electricdoublelayercapacitor Heat pump 100kW x ±2 sec chiller Solar photovoltaics 10kW Heat storage tank Purchased power Laboratory buildings Chilled/hot water Electric power flow Thermal energy flow Microgrid control results in SIT ) 800 kW Total Load of Labs Parallel Mode ( 600 400 Purchased Power from the Utility 200 Gas Engine NiMH 0 Effective Power Control Start EDLC Islanded Mode -100 0 500 1000 1500 2000 Time 300 0.6 Frequency [Hz] 250 0.5 (sec) 200 0.4 Cascade Control 150 ( ) 0.3 Analog Communication 100 Event Rate 0.2 50 0.1 Effective [kW] Power 0 -500 100 200 300 400 500 600 0 49 49.249.449.649.8 50 50.250.450.650.8 51 Time [sec] 300 0.3 50±0.2 [Hz] Gas engine gen. -

Construction in Japan Frans Van Gassel

Modern Construction in Japan Frans van Gassel Technische Universiteit Eindhoven April 2007 Construction in Japan – Culture – Architecture - Housing ENJOY YOUR STAY – Construction Systems – Robotics BUT – Construction Site PLEASE FOLLOW THE – Building Systems RULES 1 Future cities Sky City, Mega City 2 Construction systems Mechanised construction system A construction system is a technical installation, assembling building parts into a building. An installation is a collection of equipment, computers, telecommunication devices and people working alone or together. Delftse Poort Rotterdam Types of construction systems Construction tasks Three kinds of tasks: Type of Physical Cognitive tasks Control tasks construction tasks system 1. Physical tasks Traditional •People •People •People Performed by: •Equipment Workers Mechanised •Equipment •People •People Equipment 2. Cognitive tasks Computers and Mechatronised •Equipment •Computers •People software •Telecommunication Means of devices communication Automated •Equipment •Computers •Computers •Telecommunication •Telecommunication devices devices 3. Control tasks 3 AUTOMATED CONSTRUCTION SYSTEMS Structure Type of Plant System Company The aims to use construction systems are: SRC Fixed Plant Pushed-up AMURAD Kajima BIG CANOPY Obayashi • All weather construction site: no wind, sun and rain. Outer Mast RC Lifted-up NEW SMART Shimizu • Safe work conditions. Plant Mast on Column SHUTTRISE Kajima • Reduction of manpower. Inner Mast SMART Shimizu • Shorten construction period by modularization -

Download the ENR Ranking

Overview p. 34 // International Market Analysis p. 34 // Past Decade’s International Contracting Revenue p. 34 // International Region Analysis p. 35 // 2019 Revenue Breakdown p. 35 // 2019 New Contracts p. 35 // Domestic Staff Hiring p. 35 International Staff Hiring p. 35 // Profit-Loss p. 36 // 2019 Backlog p. 36 // Top 10 by Region p. 36 // Top 10 by Market p. 37 Top 20 Non-U.S. International Construction/Program Managers p. 38 // Top 20 Non-U.S. Global Construction/Program Managers p. 38 // Larsen & Toubro Ltd. Installs Massive Fusion Equipment p. 39 // How Contractors Shared the 2019 Market p. 40 // How To Read the Tables p. 40 // Top 250 International Contractors List p. 41 // International Contractors Index p. 46 // Top 250 Global Contractors List p. 47 // Global Contractors Index p. 52 CONNECTIONS China Communications 4 NUMBER Construction Group Ltd. is building the $500-million, 7,887-ft cable-stayed bridge connecting the Pelješac Peninsula with Croatia’s mainland. PHOTO COURTESY OF CHINA COMMUNICATIONS CONSTRUCTION GROUP LTD. GROUP CONSTRUCTION COMMUNICATIONS CHINA OF COURTESY PHOTO International Contractors Struggling With COVID-19 Rocked by the worldwide pandemic and plunging oil prices, the global construction market attempts to cope. By Gary J. Tulacz & Peter Reina enr.com August 17/24, 2020 ENR 33 0824_Top250_Intro_3.indd 33 8/18/20 5:44 PM 31.0% Transportation THE TOP 250 INTERNATIONAL CONTRACTORS $146,582.3 26.1% Buildings $123,456.9 Int’l Market Analysis 15.0% Petroleum $70,934.4 (2019 revenue measured in millions) 10.3% Power $48,556.6 5.6% Other 2.3% 3.4% $26,447.9 1.7% Manufacturing Industrial Telecom $10,822.1 $16,048.1 $7,842.1 % 0.1% 1.7% 2.9 Hazardous Sewer/Waste Water Waste $7,948.7 $13,904.0 $525.0 SOURCE: ENR Comparing the Past Decade’s International $383.7 $453.0 $511.1 $544.0 $521.6 $501.1 $468.1 $482.4 $487.3 $473.1 Contractor Revenue 2010* 2011* 2012 2013 2014 2015 2016 2017 2018 2019 (in $ billions) * Figures for 2010-2011 represent the Top 225 International Contractors before ENR expanded the list to 250. -

Earthquake Protection in Buildings Through Base Isolation

fECH RLC N4TL INST- OF STAND 4 NIST Special Publication 832, Volume 1 A111D3 7aTm7 Earthquake Resistant Construction Using Base Isolation NIST I PUBLICATIONS [Shin kenchiku kozo gijutsu kenkyu iin-kai hokokusho ] Earthquake Protection in Buildings Through Base Isolation United States Department of Commerce Z Technology Administration 832 National Institute of Standards and Technology V.1 1992 7he National Institute of Standards and Technology was established in 1988 by Congress to "assist industry in the development of technology . needed to improve product quality, to modernize manufacturing processes, to ensure product reliability . and to facilitate rapid commercialization ... of products based on new scientific discoveries." NIST, originally founded as the National Bureau of Standards in 1901, works to strengthen U.S. industry's competitiveness; advance science and engineering; and improve public health, safety, and the environment. One of the agency's basic functions is to develop, maintain, and retain custody of the national standards of measurement, and provide the means and methods for comparing standards used in science, engineering, manufacturing, commerce, industry, and education with the standards adopted or recognized by the Federal Government. As an agency of the U.S. Commerce Department's Technology Administration, NIST conducts basic and applied research in the physical sciences and engineering and performs related services. The Institute does generic and precompetitive work on new and advanced technologies. NIST's research