Private Equity Investors

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Combining Banking with Private Equity Investing*

Unstable Equity? * Combining Banking with Private Equity Investing First draft: April 14, 2010 This draft: July 30, 2010 Lily Fang INSEAD Victoria Ivashina Harvard University and NBER Josh Lerner Harvard University and NBER Theoretical work suggests that banks can be driven by market mispricing to undertake activity in a highly cyclical manner, accelerating activity during periods when securities can be readily sold to other parties. While financial economists have largely focused on bank lending, banks are active in a variety of arenas, with proprietary trading and investing being particularly controversial. We focus on the role of banks in the private equity market. We show that bank- affiliated private equity groups accounted for a significant share of the private equity activity and the bank’s own capital. We find that banks’ share of activity increases sharply during peaks of the private equity cycles. Deals done by bank-affiliated groups are financed at significantly better terms than other deals when the parent bank is part of the lending syndicate, especially during market peaks. While bank-affiliated investments generally involve targets with better ex-ante characteristics, bank-affiliated investments have slightly worse outcomes than non-affiliated investments. Also consistent with theory, the cyclicality of banks’ engagement in private equity and favorable financing terms are negatively correlated with the amount of capital that banks commit to funding of any particular transaction. * An earlier version of this manuscript was circulated under the title “An Unfair Advantage? Combining Banking with Private Equity Investing.” We thank Anna Kovner, Anthony Saunders, Antoinette Schoar, Morten Sorensen, Per Strömberg, Greg Udell and seminar audiences at Boston University, INSEAD, Maastricht University, Tilburg University, University of Mannheim and Wharton for helpful comments. -

Leadership Newsletter Winter 2020 / 2021

T���������, M���� ��� T����������������� Leadership Newsletter Winter 2020 / 2021 GTCR Firm Update Since the firm’s inception in 1980, GTCR has Technology, Media and Tele- partnered with management teams in more communications than 200 investments to build and transform growth businesses. Over the last twenty years alone, GTCR has invested over $16 billion in approximately 100 platform acquisitions, 30+ 95+ PLATFORMS ADD-ONS including more than 65 companies that have been sold for aggregate enterprise value of over $ $50 billion and another 14 companies that have 25B+ been taken public with aggregate enterprise value PURCHASE of more than $34 billion. In November 2020, PRICE we closed GTCR Fund XIII, the firm’s largest fund to date, with $7.5 billion of limited partner capital commitments. This fund follows GTCR Fund Acquisition Activity Since 2000 XII, which we raised in 2017, with $5.25 billion As of January 15, 2021* of limited partner capital commitments. GTCR currently has 25 active portfolio companies; ten of these companies are within the Technology, Media and Telecommunications (“TMT”) industry. Page 1 / Continues on next page Technology, Media and Telecommunications Group Update Since 2000, GTCR has completed over 30 new platform investments and over 95 add-on acquisitions within the TMT industry, for a total of over 125 transactions with a combined purchase price of over $25 billion. During just the past year, we have realized several of these investments, selling three businesses and completing the partial sale of two additional companies, for a combined enterprise value of over $9 billion. Our TMT franchise includes ten active portfolio companies and one management start-up, which together have completed nearly 30 add-on acquisitions under our ownership, representing approximately $3 billion of GTCR invested capital. -

Not Mitt Romney's Bain Capital: Boston Investment Firm Home To

Not Mitt Romney’s Bain Capital: Boston investment firm home to diverse political views - Business - The Boston Globe Interested in documentaries? Click here to view our latest free screening. TEXT SIZE MANAGE ACCOUNT LOG OUT NEWS BusinessMETRO MARKETS TECHNOLOGY ARTS BUSINESS BETABOSTON SPORTS OPINION Red Sox Live 3 8 POLITICS LIFESTYLE Final MAGAZINE INSIDERS AtTODAY'S Bain, PAPER a broad range of viewpoints is the new reality E-MAIL FACEBOOK TWITTER GOOGLE+ LINKEDIN 57 http://www.bostonglobe.com/...romney-bain-capital-boston-investment-firm-home-diverse-political-views/gAGQyqkSROIoVubvsCXJxM/story.html[5/23/2015 10:37:45 PM] Not Mitt Romney’s Bain Capital: Boston investment firm home to diverse political views - Business - The Boston Globe SUZANNE KREITER/GLOBE STAFF Former Governor Deval Patrick, a Democrat, is joining Bain Capital — an investment firm founded by his predecessor on Beacon Hill, Republican Mitt Romney. By Beth Healy and Matt Rocheleau GLOBE STAFF APRIL 16, 2015 There are two chestnuts that drive Bain Capital partners crazy: First, the notion that they are ruthless capitalists who enjoy firing people. Second, that they are all card-carrying Republicans. Fifteen long years since Mitt Romney left the Boston investment firm he founded, those old impressions still rankle. Enter Deval Patrick, former Massachusetts governor and a Democrat closely aligned with President Obama, named this week a Bain managing director who will focus on “social impact” investing. The newest Bain employee — and the public spirit implied by his new job — would seem to contradict the firm’s old image. But current and former partners, and close observers of the firm say Bain Capital is more of a big tent than many might think. -

Private Equity;

MICHAEL MORTELL Senior Managing Director Digital Media; Mergers & Acquisitions; Private Equity; Restructuring; Strategy 485 Lexington Avenue, 10th Michael Mortell is a Senior Managing Director at Ankura Capital Advisors, Floor New York, NY 10017 based in New York. Mike has extensive experience advising entrepreneurs +1.212.818.1555 Main and companies on mergers, acquisitions, strategic and business planning, +1.646.291.8597 Direct restructuring, and capital raising alternatives. Over a career in investment banking and consulting, he has cultivated expertise in the digital media and [email protected] private equity industries and developed strong relationships within them. Mike has a proven record of identifying young, high-potential companies, and providing the strategical and tactical counsel that supports growth EDUCATION objectives and positions them for future success. He also has advised MBA, University or Chicago owners/shareholders of established companies on strategic growth and Booth School of Business liquidity options. In addition to his work in digital media, he has significant BS, Finance Fairfield University experience in the e-commerce, software, retail, specialty manufacturing, and business services sectors. Prior to joining Ankura, Mike was a senior advisor at GP Bullhound, a CERTIFICATIONS boutique investment bank that acquired AdMedia Partners, the M&A FINRA Series 24, 7, 79 and 63 advisory firm where he served as a managing director. He previously ran the Private Equity Financing Group of Prudential Securities and worked for Zolfo, Cooper and Company where he was a consultant to troubled companies and their creditors. Mike also co-founded and managed Grandwood Capital LLC, an investment bank and advisory firm focused on middle-market companies. -

Private Equity and Value Creation in Frontier Markets: the Need for an Operational Approach

WhatResearch a CAIA Member Review Should Know Investment Strategies CAIAInvestmentCAIA Member Member Strategies Contribution Contribution Private Equity and Value Creation in Frontier Markets: The Need for an Operational Approach Stephen J. Mezias Afzal Amijee Professor of Entrepreneurship and Family Enterprise Founder and CEO of Vimodi, a novel visual discussion with INSEAD, based at the Abu Dhabi campus application and Entrepreneur in Residence at INSEAD 42 Alternative Investment Analyst Review Private Equity and Value Creation in Frontier Markets Private Equity and Value Creation in Frontier Markets What a CAIA Member Should Know Investment Strategies 1. Introduction ership stakes, earning returns for themselves and the Nowhere else is the operational value creation approach LPs who invested with them. While this clarifies that more in demand than in the Middle East North Africa capturing premiums through ownership transactions is (MENA) region. Advocating and building operational a primary goal for GPs, it does not completely address capabilities requires active investment in business pro- the question of what GPs need to do to make the stakes cesses, human capital, and a long-term horizon. Devel- more valuable before selling the companies in question. oping the capabilities of managers to deliver value from There are many ways that the GPs can manage their in- operations will not only result in building capacity for vestments to increase value, ranging from bringing in great companies, but will also raise the bar for human functional expertise, e.g., sound financial management, talent and organizational capability in the region. In the to bringing in specific sector operational expertise, e.g., long term, direct support and nurturing of the new gen- superior logistics capabilities. -

Representative Financial Services M&A Transactions

Representative Financial Services M&A Transactions Asset Management • Hellman & Friedman. Representing Hellman & Friedman in connection with its acquisition of Allfunds Bank S.A., a Spanish bank that offers intermediation and investment services to commercial banks, private banking institutions, fund managers, insurance companies and fund supermarkets. • Ramius, LLC. Represented Ramius, LLC, in its sale of Ramius Alternative Solutions to AllianceBernstein. • Landmark Partners. Represented Landmark Partners in the $465 million sale to OM Asset Management, a privately owned asset management holding company. • State Street Bank and Trust Company. Represented State Street Bank and Trust Company in the acquisition of GE Asset Management (GEAM), a privately owned investment manager. • Mitsubishi UFJ Investor Services. Represented Mitsubishi UFJ Investors Services in its acquisition of UBS Global Asset Management’s Alternative Fund Services Business, a company that offers professional services for hedge funds, funds of hedge funds, private equity, and real estate structures. • Mitsubishi UFJ Fund Services Holdings Ltd. Represented Mitsubishi UFJ Fund Services Holdings Ltd., an asset administration company, in its acquisition of Meridian Fund Services Group. • Bain Capital. Represented the global credit affiliate of Bain Capital in its $1.6 billion acquisition of four portfolios of collateralized loan obligations (CLOs) from Regiment Capital. • Wellington Management Company. Represented Wellington Management Company, a privately owned investment manager, in its $85 million PIPE investment in ChinaCache International Holdings Ltd., a provider of content and application delivery services in the People’s Republic of China. • 3i Group. Represented 3i Group in its strategic transaction with Fraser Sullivan, a privately owned investment manager. • Special Committee of Cole Credit Property Trust II Inc. -

How Will Financial Services Private Equity Investments Fare in the Next Recession?

How Will Financial Services Private Equity Investments Fare in the Next Recession? Leading funds are shifting to balance-sheet-light and countercyclical investments. By Tim Cochrane, Justin Miller, Michael Cashman and Mike Smith Tim Cochrane, Justin Miller, Michael Cashman and Mike Smith are partners with Bain & Company’s Financial Services and Private Equity practices. They are based, respectively, in London, New York, Boston and London. Copyright © 2019 Bain & Company, Inc. All rights reserved. How Will Financial Services Private Equity Investments Fare in the Next Recession? At a Glance Financial services deals in private equity have grown on the back of strong returns, including a pooled multiple on invested capital of 2.2x in recent years, higher than all but healthcare and technology deals. With a recession increasingly likely during the next holding period, PE funds need to develop plans to weather any storm and potentially improve their competitive position during and after the downturn. Many leading funds are investing in balance-sheet-light assets enabled by technology and regulatory change. Diligences now should test target companies under stressful economic scenarios and lay out a detailed value-creation plan, including how to mobilize quickly after acquisition. Financial services deals by private equity funds have had a strong run over the past few years, with deal value increasing significantly in Europe and the US(see Figure 1). Returns have been strong as well. Global financial services deals realized a pooled multiple on invested capital of 2.2x from 2009 through 2015, higher than all but healthcare and technology deals (see Figure 2). -

August Investor Presentation

APOLLO GLOBAL MANAGEMENT, LLC (NYSE: APO) Apollo Global Management Investor Presentation August 2018 Forward Looking Statements & Other Important Disclosures This presentation may contain forward-looking statements that are within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). These statements include, but are not limited to, discussions related to Apollo Global Management, LLC’s (together with its subsidiaries, “Apollo”,”we”,”us”,”our” and the “Company”) expectations regarding the performance of its business, liquidity and capital resources and the other non-historical statements. These forward looking statements are based on management’s beliefs, as well as assumptions made by, and information currently available to, management. When used in this presentation, the words “believe,” “anticipate,” “estimate,” “expect,” “intend” or future or conditional verbs, such as “will,” “should,” “could,” or “may,” and variations of such words or similar expressions are intended to identify forward-looking statements. Although management believes that the expectations reflected in these forward-looking statements are reasonable, it can give no assurance that these expectations will prove to be correct. These statements are subject to certain risks, uncertainties and assumptions, including risks relating to our dependence on certain key personnel, our ability to raise new private equity, credit or real asset funds, market conditions generally, our ability to manage our growth, fund performance, changes in our regulatory environment and tax status, the variability of our revenues, net income and cash flow, our use of leverage to finance our businesses and investments by funds we manage (“Apollo Funds”) and litigation risks, among others. -

Preqin Special Report: Subscription Credit Facilities

PREQIN June 2019 SPECIAL REPORT: SUBSCRIPTION CREDIT FACILITIES PREQIN SPECIAL REPORT; SUBSCRIPTION CREDIT FACILITIES Contents 3 CEO’s Foreword 4 Subscription Credit Facility Usage in Private Capital 7 Subscription Lines of Credit and LP-GP Alignment: ILPA’s Recommendations - ILPA 8 Are Subscription Facilities Oversubscribed? - Fitch Ratings 10 Subscription Finance Market - McGuireWoods LLP Download the Data Pack All of the data presented in this report is available to download in Excel format: www.preqin.com/SCF19 As with all our reports, we welcome any feedback you may have. To get in touch, please email us at: [email protected] 2 CEO's Foreword Subscription credit facilities: angels or demons? A legitimate and valuable tool for managing liquidity and streamlining transactions in a competitive market, or a cynical ploy for massaging IRRs? The debate continues in private equity and wider private capital circles. As is often the case, historical perspective is helpful. Private capital operates in a dynamic and competitive environment, as GPs and LPs strive to achieve superior net returns, through good times and bad. Completing deals and generating the positive returns that LPs Mark O’Hare expect has never been more challenging than it is CEO, Preqin today, given the availability of capital and the appetite for attractive assets in the market. Innovation and answers: transparent data, combined with thoughtful dynamism have long been an integral aspect of the communication and debate. private capital industry’s arsenal of tools, comprised of alignment of interest; close attention to operational Preqin’s raison d’être is to support and serve the excellence and value add; over-allocation in order to alternative assets industry with the best available data. -

Form 3 FORM 3 UNITED STATES SECURITIES and EXCHANGE COMMISSION Washington, D.C

SEC Form 3 FORM 3 UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 OMB APPROVAL INITIAL STATEMENT OF BENEFICIAL OWNERSHIP OF OMB Number: 3235-0104 Estimated average burden SECURITIES hours per response: 0.5 Filed pursuant to Section 16(a) of the Securities Exchange Act of 1934 or Section 30(h) of the Investment Company Act of 1940 1. Name and Address of Reporting Person* 2. Date of Event 3. Issuer Name and Ticker or Trading Symbol Requiring Statement EASTMAN KODAK CO [ EK ] Chen Herald Y (Month/Day/Year) 09/29/2009 (Last) (First) (Middle) 4. Relationship of Reporting Person(s) to Issuer 5. If Amendment, Date of Original Filed C/O KOHLBERG KRAVIS ROBERTS & (Check all applicable) (Month/Day/Year) CO. L.P. X Director 10% Owner Officer (give title Other (specify 2800 SAND HILL ROAD, SUITE 200 below) below) 6. Individual or Joint/Group Filing (Check Applicable Line) X Form filed by One Reporting Person (Street) MENLO Form filed by More than One CA 94025 Reporting Person PARK (City) (State) (Zip) Table I - Non-Derivative Securities Beneficially Owned 1. Title of Security (Instr. 4) 2. Amount of Securities 3. Ownership 4. Nature of Indirect Beneficial Ownership Beneficially Owned (Instr. 4) Form: Direct (D) (Instr. 5) or Indirect (I) (Instr. 5) Table II - Derivative Securities Beneficially Owned (e.g., puts, calls, warrants, options, convertible securities) 1. Title of Derivative Security (Instr. 4) 2. Date Exercisable and 3. Title and Amount of Securities 4. 5. 6. Nature of Indirect Expiration Date Underlying Derivative Security (Instr. 4) Conversion Ownership Beneficial Ownership (Month/Day/Year) or Exercise Form: (Instr. -

Presidential Politics & Private Equity

Roundtable Presidential Politics & Private Equity Sponsored by Sponsored by 029_MAJOct12 1 9/7/2012 7:07:28 PM Roundtable o explore the impact of the 2012 presidential election on middle- new president, or the existing president, is going to market dealmaking, Mergers & Acquisitions convened a special face. Will taxes go up? Will dividends go up? Will capital gains go up? Will “ObamaCare” get repealed? 5roundtable, held at the Nasdaq exchange and sponsored by Fifth As I’ve canvassed small businesses across the state Street Finance Corp. (Nasdaq: FSC) and Rutan & Tucker LLP. Partici- of Connecticut, I’ve found higher healthcare costs are the number one, two and three things concern pants included four private equity investors, two members of government ing them. I’ve been talking to the 60 or 70 private equity sponsors that we lend to about their portfolio (a Democrat and a Republican), two lenders, an investment banker, an companies, and this is a big issue. So, the question is: attorney and a consultant. Most of the roundtable participants are sup- Does healthcare get repealed? How do you forecast your business, how do you forecast what you want to porting former Governor Mitt Romney (R-Mass.) in the election, which do, and how do you think about deals and lending? This environment creates great uncertainty. underscores the Bain Capital co-founder’s popularity among his private The country is also going to make a choice be equity peers. tween what I call statist and capitalist, not Democrat and Republican. This is a statist president. This is a president who wants a bigger, better government. -

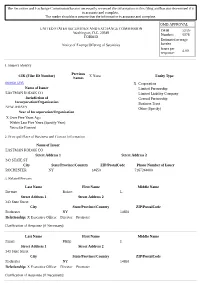

The Securities and Exchange Commission Has Not Necessarily Reviewed the Information in This Filing and Has Not Determined If It Is Accurate and Complete

The Securities and Exchange Commission has not necessarily reviewed the information in this filing and has not determined if it is accurate and complete. The reader should not assume that the information is accurate and complete. OMB APPROVAL UNITED STATES SECURITIES AND EXCHANGE COMMISSION OMB 3235- Washington, D.C. 20549 Number: 0076 FORM D Estimated average Notice of Exempt Offering of Securities burden hours per 4.00 response: 1. Issuer's Identity Previous CIK (Filer ID Number) X None Entity Type Names 0000031235 X Corporation Name of Issuer Limited Partnership EASTMAN KODAK CO Limited Liability Company Jurisdiction of General Partnership Incorporation/Organization Business Trust NEW JERSEY Other (Specify) Year of Incorporation/Organization X Over Five Years Ago Within Last Five Years (Specify Year) Yet to Be Formed 2. Principal Place of Business and Contact Information Name of Issuer EASTMAN KODAK CO Street Address 1 Street Address 2 343 STATE ST City State/Province/Country ZIP/PostalCode Phone Number of Issuer ROCHESTER NY 14650 7167244000 3. Related Persons Last Name First Name Middle Name Berman Robert L. Street Address 1 Street Address 2 343 State Street City State/Province/Country ZIP/PostalCode Rochester NY 14650 Relationship: X Executive Officer Director Promoter Clarification of Response (if Necessary): Last Name First Name Middle Name Faraci Philip J. Street Address 1 Street Address 2 343 State Street City State/Province/Country ZIP/PostalCode Rochester NY 14650 Relationship: X Executive Officer Director Promoter Clarification of Response (if Necessary): Last Name First Name Middle Name Haag Joyce P. Street Address 1 Street Address 2 343 State Street City State/Province/Country ZIP/PostalCode Rochester NY 14650 Relationship: X Executive Officer Director Promoter Clarification of Response (if Necessary): Last Name First Name Middle Name Kruchten Brad W.