The-Revenue-Code-Of-Malaybalay

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Name of the Procuring Entity

Republic of the Philippines Province of Bukidnon City of Malaybalay CM Recto St. 8700 Tel (088) 221-4947 / Fax No. (088) 813-2739 www.malaybalaycity.gov.ph Contract Reference Number: SVP-2013-020 Name of the Contract: EMERGENCY REPAIR OF KALASUNGAY BAILEY BRIDGE Location of the Contract: BRGY. KALASUNGAY, MALAYBALAY CITY INVITATION TO BID The City Government of Malaybalay will conduct a Negotiated Procurement – Small Value Procurement for the hereunder contract; Name of Contract: EMERGENCY REPAIR OF KALASUNGAY BAILEY BRIDGE Location: BRGY. KALASUNGAY, MALAYBALAY CITY Brief Description: Re-decking of Bailey Bridge Contract Duration: 30 c.d. Approved Budget for the Contract (ABC): 444,150.04 Source of Funds: GF-CEO Bidders should have completed, within ten (10) years from the date of submission and receipt of bids, a contract similar to the project with a value of at least 50 % of the ABC. A complete set of Bidding Documents may be purchased by interested Bidders from the address below and upon payment of a non-refundable fee in the amount of P 500.00. Issuance of Bidding Documents will be available from June 24, 2013 until the deadline of the submission and receipt of Bids. Bids must be delivered on or before July 02, 2013 2:00 p.m.at City Engineer’s Conference Hall, Brgy. Casisang Malaybalay City. All bids must be accompanied by a bid security in any of the acceptable forms and in the amount stated in ITB Clause 18. Bids will be opened in the presence of the bidders’ representatives who choose to attend at the address stated above. -

Non-Serviceable Areas for Estore-Ao-0623.Xlsx

Postal Code Province City Barangay Amti Bao-Yan Danac East Danac West 2815 Boliney Dao-Angan Dumagas Kilong-Olao Poblacion (Boliney) Abang Bangbangcag Bangcagan Banglolao Bugbog Calao Dugong Labon Layugan Madalipay North Poblacion 2805 Bucay Pagala Pakiling Palaquio Patoc Quimloong Salnec San Miguel Siblong South Poblacion Tabiog Ducligan Labaan 2817 Bucloc Lamao Lingay Ableg Cabaruyan 2816 Daguioman Postal Code Province City Barangay 2816 Pikek Daguioman Tui Abaquid Cabaruan Caupasan Danglas 2825 Danglas Nagaparan Padangitan Pangal Bayaan Cabaroan Calumbaya Cardona Isit Kimmalaba Libtec Lub-Lubba 2801 Dolores Mudiit Namit-Ingan Pacac Poblacion Salucag Talogtog Taping Benben (Bonbon) Bulbulala Buli Canan (Gapan) Liguis Malabbaga 2826 La Paz Mudeng Pidipid Poblacion San Gregorio Toon Postal Code Province City Barangay Udangan Bacag Buneg Guinguinabang 2821 Lacub Lan-Ag Pacoc Poblacion (Talampac) Aguet Bacooc Balais Cayapa Dalaguisen Laang Lagben Laguiben Nagtipulan 2802 Lagangilang Nagtupacan Paganao Pawa Poblacion Presentar San Isidro Tagodtod Taping Ba-I Collago Pang-Ot 2824 Lagayan Poblacion Pulot Baac Dalayap (Nalaas) Mabungtot 2807 Malapaao Langiden Poblacion Quillat Postal Code Province City Barangay Bonglo (Patagui) Bulbulala Cawayan Domenglay Lenneng Mapisla Mogao Nalbuan Poblacion Subagan Tumalip Ampalioc Barit Gayaman Lul-Luno 2813 Abra Luba Luzong Nagbukel-Tuquipa Poblacion Sabnangan Bayabas Binasaran Buanao Dulao Duldulao Gacab 2820Lat-Ey 2819 Malibcong Licuan-Baay (Licuan) Malibcong Mataragan Pacgued Taripan Umnap Ayyeng Catacdegan -

DOST-CALABARZON Namahagi Ng Rxbox Sa Polillo Group of Islands Ni Jasmin Joyce P

HUNYO 2021 ISSN 2094-6600 Vol. 11 No.6 DOST-CALABARZON namahagi ng RxBox sa Polillo Group of Islands Ni Jasmin Joyce P. Sevilla, DOST-STII Mga larawan mula sa DOST-CALABARZON a ilalim ng programang Community Empowerment through Science and STechnology (CEST) ng Department of Science and Technology (DOST), nakatanggap ang limang island municipality ng Polillo Group of Islands ng RxBox devices. Dahil sa mahirap na sitwasyon sa isla, nagsimulang mamahagi ang DOST ng RxBox— isang lokal na imbensyong biomedical device na naglalayong baguhin ang sistema ng healthcare delivery, lalo na sa mga komunidad Ipinakita ni Jay Villariño, na kabilang sa Geographically Isolated and RxBox project assistant ng Disadvantaged Areas o GIDA. May anim na DOST-CALABARZON, sa essential medical sensor ang RxBox, ito ay medical practitioners ng ang mga: 1) Blood Pressure Monitor; 2) Pulse RHU-Patnanungan kung Oximeter; 3) Electrocardiogram; 4) Fetal paano gamitin ang RxBox. Heart Monitor; 5) Maternal Tocometer; at 6) Temperature Sensor. Sa pamamagitan ng mga built-in mga pasyente] para lang masigurado na ‘yung na nila ginagawa dahil mahal ang pagpunta sensors na ito, madaling makukuha ang kanilang sakit ay may tamang diagnosis,” sa mainland; [considering ang kanilang medical signals at data at maipapadala ang pahayag ni Dr. Marina Go Ramos, Municipal magiging] pamasahe at cost of living dahil impormasyon gamit ang Internet. Sa kabuuan, Health Officer ng Rural Health Unit (RHU) hindi pwede na isang araw ka lang pupunta layunin ng RxBox na malampasan ang sa Polillo tungkol sa epekto ng mga bagong doon...and unfortunately, marami kaming geographical boundaries sa bansa at mabigyan unit ng RxBox device sa kanilang healthcare patients na nage-expire dito dahil hindi sila ang bawat Pilipino ng access sa essential delivery at services. -

[email protected]

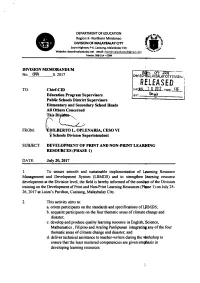

DEPARTMEiIT OF EDUCAIION Region X- North.rn Mindahao ,ri&q- DIVISION OF MATAYBATAY CITY Sayre Hiehrvay P{, C.d5.n& M.hytal.y ctiy {s? W.hh.: d+.dm.l.ytahy.net .mall: depedmalavbal.v@imail com T.LLr: 0a&3!t - O9a DIVISION ME,MORANDUM No. (3tl9 s.2017 DeF I.A TCI Y0lViSlUi RTTEASED TO Chief4ID oatu L-2.lL20lL rrrys -!L Education Program SupervisoN Publk Schoob Diltrict Supervimn f,lemetrtrry strd Secotrdsry School Hcids All Otherr Comerned Thic FROM: L OPLENARIA. CESO VI (schoob DivisioD Superirterdent STJBJECT: DEVEIOPMENT OF PRINT AND NON-PRINT LEARXING RESOURCES (PHASE 1) DAl'F- Jrly 2O,2017 l. To ensure smooth and sustainable implementalion of Lpaming Resource Mansgement and Developrnent System (LRMDS) aad to strengthen leaming resource development ar the Division level, the fietd is hereby informed ofthe condrct oftlrc Division laining on tlrc Development ofPrint and Non-Print l€aming Resouc€s (Phse l) on July 25- 26, 2017 at Loiza's Pavilion, Casisang, Malaybelay City. 2 This activity aims to: a. orient participants on the standards and specifications of l.f,.MDS; b. acquaint participants on the four thematic areas ofclimate,change aod disast€r; c. develop and produc€ quality leaming r€souIc€ i! English, Sci€rtrc€, Mathematics , Filipino and Araling Panlipunan integrating any ofthe four themalic areas of climlte change and disaster; ald d. deliver technical assistance !o te8€her-writels duing the ulo*shop to ensure that the least mastored competercies are given emflrasis in developing leaming resources. 3. Particip8nts ofthis training arc the ebmentrry rnd tecoDdar!! tcrcters ofthe five learniry arcas (ErglistL Filipino, Science, Mathematics and Anling Panllpunan) with Oe Educrtiotr Progrsm Supervirors ofthes€ leaming areas (see Enclosure l). -

Mindanao-Pricelist-3Rd-Qtr-2020.Pdf

BANK OF COMMERCE ROPA PRICELIST - MINDANAO As of 3RD QTR, 2020 AREA INDICATIVE PROPERTY DESCRIPTION PROPERTY LOCATION TCT / CCT NO. STATUS (SQM) PRICE REGION IX - WESTERN MINDANAO ZAMBOANGA DEL SUR LAND WITH 1-STOREY LOT 1 BLK 3, JOHNSTON ST., BRGY. SAN JOSE GUSU (BRGY. BALIWASAN), T-223,208 820.00 5,063,000.00 RESIDENTIAL & OFFICE BLDG. ZAMBOANGA CITY, ZAMBOANGA DE SUR LOT 513, BRGYS. LA PAZ AND PAMUCUTAN, ZAMBOANGA CITY, ZAMBOANGA DEL AGRICULTURAL LOT T-217,923 71,424.00 7,143,000.00 SUR LOT 514-B, BRGYS. LA PAZ AND PAMUCUTAN, ZAMBOANGA CITY, ZAMBOANGA AGRICULTURAL LOT T-217,924 12,997.00 1,300,000.00 DEL SUR LOT 509-B, BRGYS. LA PAZ AND PAMUCUTAN, ZAMBOANGA CITY, ZAMBOANGA AGRICULTURAL LOT T-217,925 20,854.00 2,086,000.00 DEL SUR LOT 512, BRGYS. LA PAZ AND PAMUCUTAN, ZAMBOANGA CITY, ZAMBOANGA DEL AGRICULTURAL LOT T-217,926 11,308.00 1,131,000.00 SUR LOT 510, BRGYS. LA PAZ AND PAMUCUTAN, ZAMBOANGA CITY, ZAMBOANGA DEL AGRICULTURAL LOT T-217,927 4,690.00 469,000.00 SUR LOT 511, BRGYS. LA PAZ AND PAMUCUTAN, ZAMBOANGA CITY, ZAMBOANGA DEL AGRICULTURAL LOT T-217,928 17,008.00 1,701,000.00 SUR BLK 8, COUNTRY HOMES SUBD., BRGY. AYALA, ZAMBOANGA CITY (SITE IV), RESIDENTIAL VACANT LOT T-217,929 1,703.00 1,022,000.00 ZAMBOANGA DEL SUR BLK 9, COUNTRY HOMES SUBD., BRGY. AYALA, ZAMBOANGA CITY (SITE IV), RESIDENTIAL VACANT LOT T-217,930 1,258.00 755,000.00 ZAMBOANGA DEL SUR BLK 11, COUNTRY HOMES SUBD., BRGY. -

Towards a Regional Soil Reference System for Fertility Assessment and Monitoring in the Highlands of Mindanao, Philippines

COMMUNAUTÉ FRANÇAISE DE BELGIQUE UNIVERSITÉ DE LIÈGE – GEMBLOUX AGRO-BIO TECH Towards a regional soil reference system for fertility assessment and monitoring in the highlands of Mindanao, Philippines Guadalupe M. DEJARME-CALALANG Dissertation originale présentée en vue de l’obtention du grade de Docteur en Sciences Agronomiques et Ingénierie Biologique Promoteurs: Laurent Bock Gilles Colinet Année civile 2015 To RODOLFO, my husband and my sons, JANSSEN and JAMES CONRAD, this work is dedicated. ii Acknowledgment I am truly grateful to all, who in one way or another have supported me in this challenging work. To the Cooperation of Universities for Development (CUD) for the scholarship grant, To Xavier University, Philippines, for the study leave grant and research support through its Faculty Development Program. To Prof Laurent Bock, my PhD Promoteur, to whom I deeply acknowledge, for unselfishly imparting to me his knowledge in Soil Science through his utmost guidance in the over-all PhD research, and his incessant encouragement that get me through in this intellectually and physically demanding work, To Prof Gilles Colinet, Co-Promoteur for assisting me in the data gathering, who painstakingly had checked the pot experiment part of the manuscript, and for his guidance on the statistical analyses, To the five MSc students who worked with me in this CUD project and shared to me their gathered information, Lola Richelle, Fanny Lebrun, Sophie Barbieux, Sophie Van Daele of Universite de Liege-Gembloux Agro Bio Tech (ULg-GxABT), and Simon Maurissen of Universite Libre de Brussels, To the members of the PhD Committee; Prof Aurore Degre of ULg-GxABT and Prof Vincent Hallet of Universite de Namur for their assistance in the data gathering, Prof Philippe Lebailly and Prof Guy Mergeai of ULg-GxABT, Prof Joseph Dufey and Prof Sophie Opfergelt of Universite Catholique de Louvain for their valuable comments and suggestions to improve the study and PhD manuscript, and to Dr. -

NORTHERN MINDANAO Directory of Mines and Quarries

MINES AND GEOSCIENCES BUREAU REGIONAL OFFICE NO.: X- NORTHERN MINDANAO Directory of Mines and Quarries - CY 2020 Other Plant Locations Status Mine Site Mine Mine Site E- Head Office Head Office Head Office E- Head Office Mine Site Mailing Type of Permit Date Date of Area municipality, Non- Telephon Site Fax mail barangay Year Region Mineral Province Municipality Commodity Contractor Operator Managing Official Position Head Office Mailing Address Telephone No. Fax No. mail Address Website (hectares) province Producing TIN Address e No. No. Address Permit Number Approved Expiration Producing donjieanim 10-Northern Non- Misamis Proprietor/Man Poblacion, Sapang Dalaga, Misamis as@yahoo Dioyo, Sapang 191-223- 2020 Mindanao Metallic Occidental Sapang Dalaga Sand and Gravel ANIMAS, EMILOU M. ANIMAS, EMILOU M. ANIMAS, EMILOU M. ager Occidental 9654955493 N/A .com N/A Dalaga N/A N/A N/A CSAG RP-07-19 11/10/2019 10/10/2020 1.00 N/A N/A Producing 205 10-Northern Non- Misamis Proprietor/Man South Western, Calamba, Misamis ljcyap7@g 432-503- 2020 Mindanao Metallic Occidental Calamba Sand and Gravel YAP, LORNA T. YAP, LORNA T. YAP, LORNA T. ager Occidental 9466875752 N/A mail.com N/A Sulipat, Calamba N/A N/A N/A CSAG RP-18-19 04/02/2020 03/02/2021 1.9524 N/A N/A Producing 363 maconsuel 10-Northern Non- Misamis ROGELIO, MARIA ROGELIO, MA. ROGELIO, MA. Proprietor/Man Northern Poblacion, Calamba, Misamis orogelio@ 325-550- 2020 Mindanao Metallic Occidental Calamba Sand and Gravel CONSUELO A. CONSUELO A. CONSUELO ager Occidental 9464997271 N/A gmail.com N/A Solinog, Calamba N/A N/A N/A CSAG RP-03-20 24/06/2020 23/06/2021 1.094 N/A N/A Producing 921 noel_pagu 10-Northern Non- Misamis Proprietor/Man Southern Poblacion, Plaridel, Misamis e@yahoo. -

By Region) As of March 31, 2018 Area CADT No

Ancestral Domains Office Recognition Division Master List of Approved CADTs (By Region) As of March 31, 2018 Area CADT No. Date Approved Location CADC No. / Process Tribe IP Right Holders (Hectares) CAR 1 CAR-BAK- 7/18/2002 Bakun, Benguet CADC-120 Bago & Kankana-ey 29,444.3449 17,218 0702-0001 2 CAR-KIB-0204-2/13/2004 Municipality of Kibungan, Province of Benguet CADC-071 Kankana-ey 22,836.8838 15,472 016 3 CAR-ATO- 12/14/2004 Municipality of Atok, Province of Benguet Direct Application Kankan-ey & Ibaloy 20,017.6498 15,634 1204-026 4 CAR-CAL- 10/21/2005 Barangay Eva Garden, Cadaclan (portion), and Tanglagan(portion), Direct Application Isnag 11,268.0254 852 1005-031 Municipality of Calanasan, Province of Apayao 5 CAR-BAG- 2/9/2006 Barangay Happy Hallow, Baguio City Direct Application Ibaloi & Kankanaey 147.4496 2,900 0206-041 6 CAR-KAP- 11/14/2006 Barangays of Balakbak, Belengbelis, Boklaoan, Cayapes, Cuba, Datakan, Direct Application Kankana-ey & Ibaloi 17,127.1491 15,995 1106-050 Gadang, Gasweling, Labueg, Paykek, Poblacion Central, Pudong, Pongayon, Sagubo and Taba-ao, all in the Municipality of Kapangan, Province of Benguet 7 CAR-ASI-0308-3/26/2008 Brgys. Amduntog, Antipolo, Liwon, Namal, Natcak, Nungawa, Panubtuban, Direct Application Kalanguya, Ayangan 26,578.6964 14,355 063 Haliap, Cawayan, Pula, Duli Camandag, all in the Municipality of Asipulo, and Tuwali Province of Ifugao; and portion of the Mun. of Ambaguio in the Province of Nueva Vizcaya 8 CAR-KAB- 3/26/2008 Mun. of Kabayan, Prov. -

Name of the Procuring Entity

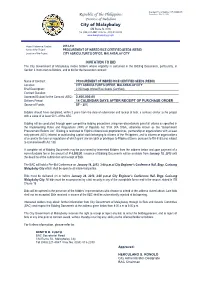

Standard Form Number: SF-GOOD-05 Republic of the Philippines Revised on: July 28, 2004 Province of Bukidnon City of Malaybalay CM Recto St. 8700 Tel (088) 221-4947 / Fax No. (088) 813-2010 www.malaybalaycity.gov.ph Project Reference Number: 2012-131 Name of the Project: PROCUREMENT OF INBRED RICE CERTIFIED SEEDS (REBID) Location of the Project: CITY AGRICULTURE’S OFFICE, MALAYBALAY CITY INVITATION TO BID The City Government of Malaybalay invites bidders whose eligibility is contained in the Bidding Documents, particularly, in Section II.Instruction to Bidders, and to bid for the hereunder contract: Name of Contract: PROCUREMENT OF INBRED RICE CERTIFIED SEEDS (REBID) Location: CITY AGRICULTURE’S OFFICE, MALAYBALAY CITY Brief Description: 2,000 bags Inbred Rice Seeds (Certified) Contract Duration: - Approved Budget for the Contract (ABC): 2,400,000.00 Delivery Period: 14 CALENDAR DAYS AFTER RECEIPT OF PURCHASE ORDER Source of Funds: GF – 20% Bidders should have completed, within 2 years from the date of submission and receipt of bids, a contract similar to the project with a value of at least 50 % of the ABC. Bidding will be conducted through open competitive bidding procedures using non-discretionary pass/fail criteria as specified in the Implementing Rules and Regulations (IRR) of Republic Act 9184 (RA 9184), otherwise known as the “Government Procurement Reform Act”. Bidding is restricted to Filipino citizens/sole proprietorships, partnership or organizations with at least sixty percent (60%) interest or outstanding capital stock belonging to citizens of the Philippines, and to citizens or organizations of a country the laws or regulations of which grant similar rights or privileges to Filipino citizens, pursuant to RA 5183 and subject to Commonwealth Act 138. -

Republic Act No. 10727

H. No. 4631 ^public nf f If E ^IfilippiiiES filnngrBSs uf f{jB pijUxpjixtiBs (MEfr0(:^m b i ^ucfsEttflf (langrEsa ®Iftrh ^gukr(^Ession Begun and Held in Metro Manila, on Monday, the twenty-seventh day of July, two thousand fifteen. [ Republic act N o. 10 72 7 ] AN ACT SEPARATING THE SILAE NATIONAL HIGH SCHOOL - ST. PETER ANNEX IN BARANGAY ST. PETER, CITY OF MALAYBALAY. PROVINCE OF BUKIDNON FROM THE SILAE NATIONAL HIGH SCHOOL, CONVERTING IT INTO AN INDEPENDENT NATIONAL HIGH SCHOOL TO BE KNOWN AS ST. PETER NATIONAL HIGH SCHOOL AND APPROPRIATING FUNDS THEREFOR Be it enacted by the Senate and House of Representatives of the Philippines in Congress assembled:, . , Section l. Tlie Silae National High School — St. Peter Annex in Barangay St. Peter, City of Malaybalay, Province of BuMdnon is hereby separated from the Silae Nationkl High School and converted into an independent national high school to be known as St. Peter National High School. Sec. 2. All personnel, assets, liabilities and records of the Silae National High School — St. Peter Annex are hereby transferred to and absorbed by the St. Peter National High SchooL Sec. 3. The Secretary of Education shall immediately include in the Department's program the operationalization of the St. Peter National High School, the initial funding of which shall be charged against the current year's appropriation of the Silae National High School - St. Peter Annex. Thereafter, the amount necessary for the continued operation of the school shall be included in the annual General Appropriations Act. Sec. 4. The Secretary of Education shall issue such rules and regulations as may be necessary to carry out the purpose of this Act. -

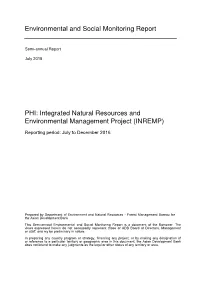

Integrated Natural Resources and Environmental Management Project (INREMP)

Environmental and Social Monitoring Report Semi-annual Report July 2018 PHI: Integrated Natural Resources and Environmental Management Project (INREMP) Reporting period: July to December 2016 Prepared by Department of Environment and Natural Resources - Forest Management Bureau for the Asian Development Bank This Semi-annual Environmental and Social Monitoring Report is a document of the Borrower. The views expressed herein do not necessarily represent those of ADB Board of Directors, Management or staff, and my be preliminary in nature. In preparing any country program or strategy, financing any project, or by making any designation of or reference to a particular territory or geographic area in this document, the Asian Development Bank does not intend to make any judgments as the legal or other status of any territory or area. ABBREVIATIONS ADB Asian Development Bank ADSDPP Ancestral Domain sustainable Development and Protection Plan BURB Bukidnon Upper River Basin CENRO Community Environment and Natural Resource Office CP Certificate of Precondition CURB Chico Upper River Basin DED Detailed engineering Design DENR Department of Environment and Natural Resources FMB Forest Management Bureau GAP Gender Action Plan GOP Government of the Philippines GRM Grievance Redress Mechanism EA Executing Agency IEE Initial Environmental Examination IFAD International Fund for Agricultural Development INREMP Integrated Natural Resources and Environmental Management Project IP Indigenous People IPDP Indigenous Peoples Development Plan IPP Indigenous -

Forests Beneath the Grass

FoForestsrests beneathBeneath the grassGrass Proceedings of the regional workshop on advancing the application of assisted natural regeneration for eective low-cost forest restoration Naturally-regenerated young tree seedling hidden under the grass RAP PUBLICATION 2010/11 Forests beneath the grass Proceedings of the Regional Workshop on Advancing the Application of Assisted Natural Regeneration for Effective Low-Cost Restoration Bohol, Philippines, 19-22 May 2009 Edited by Patrick B. Durst, Percy Sajise and Robin N. Leslie FOOD AND AGRICULTURE ORGANIZATION OF THE UNITED NATIONS REGIONAL OFFICE FOR ASIA AND THE PACIFIC Bangkok, 2011 The designations employed and the presentation of material in this information product do not imply the expression of any opinion whatsoever on the part of the Food and Agriculture Organization of the United Nations (FAO) concerning the legal or development status of any country, territory, city or area or of its authorities, or concerning the delimitation of its frontiers or boundaries. The mention of specific companies or products of manufacturers, whether or not these have been patented, does not imply that these have been endorsed or recommended by FAO in preference to others of a similar nature that are not mentioned. ISBN 978-92-5-106639-3 All rights reserved. FAO encourages reproduction and dissemination of material in this information product. Non-commercial uses will be authorized free of charge. Reproduction for resale or other commercial purposes, including educational purposes, may incur fees. Applications for permission to reproduce or disseminate FAO copyright materials and all other queries on rights and licences, should be addressed by e-mail to [email protected] or to the Chief, Publishing Policy and Support Branch, Office of Knowledge Exchange, Research and Extension, FAO,Viale delle Terme di Caracalla, 00153 Rome, Italy.