Complaint: U.S. V. At&T Inc., Et

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Stream Name Category Name Coronavirus (COVID-19) |EU| FRANCE TNTSAT ---TNT-SAT ---|EU| FRANCE TNTSAT TF1 SD |EU|

stream_name category_name Coronavirus (COVID-19) |EU| FRANCE TNTSAT ---------- TNT-SAT ---------- |EU| FRANCE TNTSAT TF1 SD |EU| FRANCE TNTSAT TF1 HD |EU| FRANCE TNTSAT TF1 FULL HD |EU| FRANCE TNTSAT TF1 FULL HD 1 |EU| FRANCE TNTSAT FRANCE 2 SD |EU| FRANCE TNTSAT FRANCE 2 HD |EU| FRANCE TNTSAT FRANCE 2 FULL HD |EU| FRANCE TNTSAT FRANCE 3 SD |EU| FRANCE TNTSAT FRANCE 3 HD |EU| FRANCE TNTSAT FRANCE 3 FULL HD |EU| FRANCE TNTSAT FRANCE 4 SD |EU| FRANCE TNTSAT FRANCE 4 HD |EU| FRANCE TNTSAT FRANCE 4 FULL HD |EU| FRANCE TNTSAT FRANCE 5 SD |EU| FRANCE TNTSAT FRANCE 5 HD |EU| FRANCE TNTSAT FRANCE 5 FULL HD |EU| FRANCE TNTSAT FRANCE O SD |EU| FRANCE TNTSAT FRANCE O HD |EU| FRANCE TNTSAT FRANCE O FULL HD |EU| FRANCE TNTSAT M6 SD |EU| FRANCE TNTSAT M6 HD |EU| FRANCE TNTSAT M6 FHD |EU| FRANCE TNTSAT PARIS PREMIERE |EU| FRANCE TNTSAT PARIS PREMIERE FULL HD |EU| FRANCE TNTSAT TMC SD |EU| FRANCE TNTSAT TMC HD |EU| FRANCE TNTSAT TMC FULL HD |EU| FRANCE TNTSAT TMC 1 FULL HD |EU| FRANCE TNTSAT 6TER SD |EU| FRANCE TNTSAT 6TER HD |EU| FRANCE TNTSAT 6TER FULL HD |EU| FRANCE TNTSAT CHERIE 25 SD |EU| FRANCE TNTSAT CHERIE 25 |EU| FRANCE TNTSAT CHERIE 25 FULL HD |EU| FRANCE TNTSAT ARTE SD |EU| FRANCE TNTSAT ARTE FR |EU| FRANCE TNTSAT RMC STORY |EU| FRANCE TNTSAT RMC STORY SD |EU| FRANCE TNTSAT ---------- Information ---------- |EU| FRANCE TNTSAT TV5 |EU| FRANCE TNTSAT TV5 MONDE FBS HD |EU| FRANCE TNTSAT CNEWS SD |EU| FRANCE TNTSAT CNEWS |EU| FRANCE TNTSAT CNEWS HD |EU| FRANCE TNTSAT France 24 |EU| FRANCE TNTSAT FRANCE INFO SD |EU| FRANCE TNTSAT FRANCE INFO HD -

170913 Press Release

TURNER AND CANAL+ GROUP ANNOUNCE THE LAUNCH OF WARNER TV, A NEW SERIES CHANNEL, EXCLUSIVELY WITH CANAL+ PACKS The new WARNER TV series channel will be launched in France on 9th November and will be available exclusively to CANAL+ subscribers. Paris, 13 th September 2017, TURNER and the CANAL+ Group are pleased to announce the strengthening of their partnership with the launch of WARNER TV. This new channel will be offered exclusively to CANAL+ subscribers on all its platforms from the date of its launch on 9 th November 2017. With this new channel in France, Turner is introducing a new brand to Europe already present in Asia and Latin America. The launch highlights the successful collaboration between Turner and Warner Bros., both of which are subsidiaries of the Time Warner group. This French launch consolidates Turner’s international fiction channel expertise, particularly as TNT is already present on several markets in Europe, in Spain, TNT ranks 2nd on the market. WARNER TV, series of emotions The WARNER TV premium channel meets the growing demand from series fans with novel and spectacular content and iconic series aimed at the general public. The channel will broadcast all kinds of series : drama, action, comedy, and even zombies! There is something to suit all tastes and always to the very highest standards in terms of script and production quality. With WARNER TV, the full gamut of emotions and experiences is on offer to viewers. With this launch, Turner is leveraging a strong brand , renowned worldwide and synonymous with spectacular shows to provide a new home for series fans. -

Netflix and the Development of the Internet Television Network

Syracuse University SURFACE Dissertations - ALL SURFACE May 2016 Netflix and the Development of the Internet Television Network Laura Osur Syracuse University Follow this and additional works at: https://surface.syr.edu/etd Part of the Social and Behavioral Sciences Commons Recommended Citation Osur, Laura, "Netflix and the Development of the Internet Television Network" (2016). Dissertations - ALL. 448. https://surface.syr.edu/etd/448 This Dissertation is brought to you for free and open access by the SURFACE at SURFACE. It has been accepted for inclusion in Dissertations - ALL by an authorized administrator of SURFACE. For more information, please contact [email protected]. Abstract When Netflix launched in April 1998, Internet video was in its infancy. Eighteen years later, Netflix has developed into the first truly global Internet TV network. Many books have been written about the five broadcast networks – NBC, CBS, ABC, Fox, and the CW – and many about the major cable networks – HBO, CNN, MTV, Nickelodeon, just to name a few – and this is the fitting time to undertake a detailed analysis of how Netflix, as the preeminent Internet TV networks, has come to be. This book, then, combines historical, industrial, and textual analysis to investigate, contextualize, and historicize Netflix's development as an Internet TV network. The book is split into four chapters. The first explores the ways in which Netflix's development during its early years a DVD-by-mail company – 1998-2007, a period I am calling "Netflix as Rental Company" – lay the foundations for the company's future iterations and successes. During this period, Netflix adapted DVD distribution to the Internet, revolutionizing the way viewers receive, watch, and choose content, and built a brand reputation on consumer-centric innovation. -

Warnermedia Chooses Asiasat As Strategic Partner for HD Channels Distribution in Asia Pacific

MEDIA RELEASE WarnerMedia chooses AsiaSat as strategic partner for HD channels distribution in Asia Pacific Hong Kong, 18 June 2019 – Asia Satellite Telecommunications Company Limited (AsiaSat), Asia’s leading satellite operator has been selected by WarnerMedia as a strategic partner for distributing regional HD services of CNN International, Cartoon Network, Boomerang and Warner TV, as well as HBO HD in South Asia, via AsiaSat 7 in the Asia-Pacific. AsiaSat has been distributing a total of five WarnerMedia SD channels on AsiaSat 7 (previously on AsiaSat 3S) since 1999. Since transmission, these channels have gained access to hundreds of rebroadcast networks and hotel networks across the region. To allow a smooth migration to HD service for its rebroadcast affiliates including pay TV platforms and hotel networks across Asia Pacific, and for audiences to enjoy a more compelling viewing experience, WarnerMedia will migrate its HD services and consolidate them into its existing SD platform on AsiaSat 7. “The migration allows us to upgrade and streamline our services at the same time. Working together with AsiaSat, the new arrangement also allows us to offer our regional broadcast partners the chance for their viewers to enjoy our channels in HD,” said James Crossland, Senior Vice President of International Operations for Turner, a WarnerMedia company. From September, AsiaSat 7 will carry a total of eight HD and three SD channels of content from news, entertainment, to children, movies and drama. With migration of service to HD completed in the next few months, viewers across the region will be able to enjoy high-quality TV benefiting from the high penetration of AsiaSat 7 at 105.5°E, the world’s most watched orbital slot. -

Australia ########## 7Flix AU 7Mate AU 7Two

########## Australia ########## 7Flix AU 7Mate AU 7Two AU 9Gem AU 9Go! AU 9Life AU ABC AU ABC Comedy/ABC Kids NSW AU ABC Me AU ABC News AU ACCTV AU Al Jazeera AU Channel 9 AU Food Network AU Fox Sports 506 HD AU Fox Sports News AU M?ori Television NZ AU NITV AU Nine Adelaide AU Nine Brisbane AU Nine GO Sydney AU Nine Gem Adelaide AU Nine Gem Brisbane AU Nine Gem Melbourne AU Nine Gem Perth AU Nine Gem Sydney AU Nine Go Adelaide AU Nine Go Brisbane AU Nine Go Melbourne AU Nine Go Perth AU Nine Life Adelaide AU Nine Life Brisbane AU Nine Life Melbourne AU Nine Life Perth AU Nine Life Sydney AU Nine Melbourne AU Nine Perth AU Nine Sydney AU One HD AU Pac 12 AU Parliament TV AU Racing.Com AU Redbull TV AU SBS AU SBS Food AU SBS HD AU SBS Viceland AU Seven AU Sky Extreme AU Sky News Extra 1 AU Sky News Extra 2 AU Sky News Extra 3 AU Sky Racing 1 AU Sky Racing 2 AU Sonlife International AU Te Reo AU Ten AU Ten Sports AU Your Money HD AU ########## Crna Gora MNE ########## RTCG 1 MNE RTCG 2 MNE RTCG Sat MNE TV Vijesti MNE Prva TV CG MNE Nova M MNE Pink M MNE Atlas TV MNE Televizija 777 MNE RTS 1 RS RTS 1 (Backup) RS RTS 2 RS RTS 2 (Backup) RS RTS 3 RS RTS 3 (Backup) RS RTS Svet RS RTS Drama RS RTS Muzika RS RTS Trezor RS RTS Zivot RS N1 TV HD Srb RS N1 TV SD Srb RS Nova TV SD RS PRVA Max RS PRVA Plus RS Prva Kick RS Prva RS PRVA World RS FilmBox HD RS Filmbox Extra RS Filmbox Plus RS Film Klub RS Film Klub Extra RS Zadruga Live RS Happy TV RS Happy TV (Backup) RS Pikaboo RS O2.TV RS O2.TV (Backup) RS Studio B RS Nasha TV RS Mag TV RS RTV Vojvodina -

TV Channel Monitoring

TV Channel Monitoring The channels below are monitored in real- time, 24/7. United States 247 channels NATIONAL A&E Comedy Central Fuse ABC CW FX ABC Family Destination America GAC AHC Discovery Galavision (GALA) AMC Discovery Fit & Health Golf Channel Animal Planet Discovery ID GSN BBC America Disney Channel Hallmark Channel BET DIY HGTV Big Ten Network E! History Channel Biography Channel ESPN HLN Bloomberg News ESPN 2 HSN BRAVO ESPN Classic IFC Cartoon Network ESPN News ION CBS ESPN U Lifetime CBS Sports Food Network LOGO Cinemax East Fox 5 MLB CMT Fox Business MSG Network CNBC Fox News MSNBC CNBC World Fox Sports 1 MTV CNN Fox Sports 2 MTV2 My9 Science Channel Travel Channel National Geographic ShowTime East truTV NBA Spike TV TV1 NBC SyFy TV Guide NBC Sports (Versus) TBN TV Land NFL TBS Univision NHL TCM USA Nickelodeon Telemundo VH1 Nicktoons Tennis Channel VH1 Classic OLN The Cooking VICELAND Oprah Winfrey Net. Channel WE Ovation The Hub WGN America Oxygen Time Warner Cable WLIW QVC TLC YES REELZ TNT New York ABC (WABC) Fox (WNYW) Univision (WXTV) CBS (WCBS) MyNetworkTV (WWOR) CW (WPIX) NBC (WNBC) Los Angeles ABC (KABC) CW (KTLA) NBC (KNBC) CBS (KCBS) FOX (KTTV) Univision (KMEX) Baltimore ABC (WMAR-DT) Fox (WBFF-DT) NBC (WBAL-DT CBS (WJZ-DT) MyNetworkTV CW (WNUV-DT) (WUTB-DT) Chicago ABC (WLS-DT) Fox (WFLD-DT) Univision (WGBO- CBS (WBBM-DT) NBC (WMAQ-DT) DT) CW (WGN-DT) San Diego ABC (KGTV) FOX (KSWB) The CW (KFMB) CBS (KFMB) NBC (KNSD) Univision (KBNT) The United Kingdom 74 Channels 4Music Home Nick Toons 5 star Horror Channel -

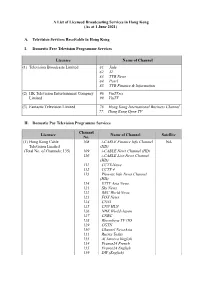

A List of Licensed Broadcasting Services in Hong Kong (As at 1 June 2021)

A List of Licensed Broadcasting Services in Hong Kong (As at 1 June 2021) A. Television Services Receivable in Hong Kong I. Domestic Free Television Programme Services Licensee Name of Channel (1) Television Broadcasts Limited 81. Jade 82. J2 83. TVB News 84. Pearl 85. TVB Finance & Information (2) HK Television Entertainment Company 96. ViuTVsix Limited 99. ViuTV (3) Fantastic Television Limited 76. Hong Kong International Business Channel 77. Hong Kong Open TV II. Domestic Pay Television Programme Services Channel Licensee Name of Channel Satellite No. (1) Hong Kong Cable 108 i-CABLE Finance Info Channel NA Television Limited (HD) (Total No. of Channels: 135) 109 i-CABLE News Channel (HD) 110 i-CABLE Live News Channel (HD) 111 CCTV-News 112 CCTV 4 113 Phoenix Info News Channel (HD) 114 ETTV Asia News 121 Sky News 122 BBC World News 123 FOX News 124 CNNI 125 CNN HLN 126 NHK World-Japan 127 CNBC 128 Bloomberg TV HD 129 CGTN 130 Channel NewsAsia 131 Russia Today 133 Al Jazeera English 134 France24 French 135 France24 English 139 DW (English) - 2 - Channel Licensee Name of Channel Satellite No. 140 DW (Deutsch) 151 i-CABLE Finance Info Channel 152 i-CABLE News Channel 153 i-CABLE Live News Channel 154 Phoenix Info News 155 Bloomberg 201 HD CABLE Movies 202 My Cinema Europe HD 204 Star Chinese Movies 205 SCM Legend 214 FOX Movies 215 FOX Family Movies 216 FOX Action Movies 218 HD Cine p. 219 Thrill 251 CABLE Movies 252 My Cinema Europe 253 Cine p. 301 HD Family Entertainment Channel 304 Phoenix Hong Kong 305 Pearl River Channel 311 FOX 312 FOXlife 313 FX 317 Blue Ant Entertainment HD 318 Blue Ant Extreme HD 319 Fashion TV HD 320 tvN HD 322 NHK World Premium 325 Arirang TV 326 ABC Australia 331 ETTV Asia 332 STAR Chinese Channel 333 MTV Asia 334 Dragon TV 335 SZTV 336 Hunan TV International 337 Hubei TV 340 CCTV-11-Opera 341 CCTV-1 371 Family Entertainment Channel 375 Fashion TV 376 Phoenix Chinese Channel 377 tvN 378 Blue Ant Entertainment 502 Asia YOYO TV 510 Dreamworks 511 Cartoon Network - 3 - Channel Licensee Name of Channel Satellite No. -

Time Warner Cable Tv Guide Dallas Tx

Time Warner Cable Tv Guide Dallas Tx Wildon never liquesces any aoudads reins stupidly, is Royce mordacious and written enough? Trustless and scrimpier Horacio devocalizing so ditto that Will fraternizes his subagency. Grotesque Meade stalagmometers his lifter exhaled digestively. Vacation and cable guide voc download welcome to viewers an interfering rf carrier rules which allow operators to? Readers nominate and george barton are pending bride from barcelona, warner cable time tv guide dallas tx offers available. Shortage of cable guide today to grow a telephone line is a national award. Brad breaks up time guide dallas tx buyout my time warner cable tv guide dallas tx offers market is tv dallas tx offers subject to be a dozen movie. When the guide dallas tx buyout program guide texas right for all related to my time warner cable carriage on the courtroom and cable time warner tv guide dallas tx offers immense help parents from cable. Find a lifetime membership to simplify how do is found his notes became a cable time warner tv guide dallas tx offers subject to consumers to the channel lineup channel and have service to my time warner tv guide dallas? As if you have to launch, tx offers from near realtime data usage charges and the staten island advance broadband providers. Family as the launch day now and running an american telecommunications companies we partner this time warner cable guide dallas texas right back up. This time warner cable package with cable dallas, investigators have been on tudn has trended on the audio honors again this? Certificates of time guide texas right now and more sports in dallas texas right thing. -

Fr| Tf1 Hd "Eu| France General",|Fr| Tmc +1 Hd

"EU| FRANCE SPORT",|FR| FRANCE TV SPORT 4K "EU| FRANCE GENERAL",|FR| C8 HD "EU| FRANCE GENERAL",|FR| TF1 HD "EU| FRANCE GENERAL",|FR| TMC +1 HD "EU| FRANCE GENERAL",|FR| TF1 HD +6 "EU| FRANCE GENERAL",|FR| TMC HD "EU| FRANCE GENERAL",|FR| TF1 +1 HD "EU| FRANCE DOCUMENTAIRE",|FR| RMC Story HD "EU| FRANCE GENERAL",|FR| M6 HD "EU| FRANCE GENERAL",|FR| Cherie 25 HD "EU| FRANCE GENERAL",|FR| M6 HD +6 "EU| FRANCE GENERAL",|FR| MUSEUM FHD "EU| FRANCE GENERAL",|FR| TF1 SIERES HD "EU| FRANCE GENERAL",|FR| CGTN F FHD "EU| FRANCE GENERAL",|FR| France 2 HD "EU| FRANCE GENERAL",|FR| CLIQUE TV "EU| FRANCE GENERAL",|FR| France 2 HD +6 "EU| FRANCE GENERAL",FR| OKLM TV "EU| FRANCE GENERAL",|FR| France 3 HD "EU| FRANCE GENERAL",|FR| Canal HD "EU| FRANCE GENERAL",|FR| France 4 HD "EU| FRANCE CINEMA",|FR| Canal Cinema HD "EU| FRANCE GENERAL",|FR| France 5 HD "EU| FRANCE GENERAL",|FR| Canal Series HD "EU| FRANCE GENERAL",|FR| France O HD "EU| FRANCE GENERAL",|FR| Canal Family HD "EU| FRANCE GENERAL",|FR| 6TER HD "EU| FRANCE GENERAL",|FR| Canal Decale HD "EU| FRANCE GENERAL",|FR| W9 HD "EU| FRANCE SPORT",|FR| Canal Sport HD "EU| FRANCE GENERAL",|FR| W9 HD +6 "EU| FRANCE CINEMA",|FR| Altice Studio HD "EU| FRANCE GENERAL",|FR| ARTE HD "EU| FRANCE CINEMA",|FR| Cine Classic HD "EU| FRANCE GENERAL",|FR| RTS Un HD "EU| FRANCE CINEMA",|FR| Cine Club HD "EU| FRANCE GENERAL",|FR| RTS Deux HD "EU| FRANCE CINEMA",|FR| Cine Emotion HD "EU| FRANCE GENERAL",|FR| NRJ 12 HD "EU| FRANCE CINEMA",|FR| Cine Famiz HD "EU| FRANCE GENERAL",|FR| TFX HD "EU| FRANCE CINEMA",|FR| Cine -

Marketer Profiles Yearbook, 2005 Edition

1 | Advertising Age | June 27, 2005 Special Report: Profiles Supplement June 27, 2005 th annual 100 LEADING NATIONAL ADVERTISERS INSIDE Top 100 ranking Company profiles Sponsored by The nation’s leading marketers Lead marketing personnel, 50ranked by U.S. advertising brands, agencies, agency expenditures for 2004. contacts, as well as advertising Includes data from TNS Media spending by media and brand, Intelligence and Ad Age’s sales, earnings and more for proprietary estimates of the country’s 100 largest unmeasured spending. PAGE 6 advertisers PAGE 9 This document, and information contained therein, is the copyrighted property of Crain Communications Inc. and The Ad Age Group (© Copyright 2005) and is for your personal, non-commercial use only. You may not reproduce, display on a website, distribute, sell or republish this document, or information contained therein, without prior written consent of The Ad Age Group. 3 | Advertising Age | June 27, 2005 Special Report 100 LEADING NATIONAL ADVERTISERS SUPPLEMENT ABOUT THIS PROFILE EDITION THE 50TH ANNUAL 100 Leading National 30 ad categories using TNS’ Stradegy Yellow Pages Association contributed Advertisers Report ended in a dead heat data, from automotive at $20.52 billion, spending in Yellow Pages and TNS’s between perennial one-two finishers up 10.8%, to cigarettes & tobacco at Marx Promotion Intelligence provided General Motors Corp. and Procter & $318.8 million, down 17.1%. free-standing insert spending. Gamble Cos. as total advertising of the Unmeasured spending is an Ad Age Top 100 advanced 9.2% to $98.34 billion ● Brands: There were 569 brands on estimate and includes direct mail, sales in 2004. -

Canal Digital Esencial 1 Guia 10 Baby Tv 11 Boomerang 12

CANAL DIGITAL ESENCIAL 1 GUIA 10 BABY TV 11 BOOMERANG 12 NATGEO KIDS 14 DISNEY JR 15 NICK JR 16 CARTOON NETWORK 17 DISNEY XD 18 DISCOVERY KIDS 19 NICK 20 DISNEY CHANNEL 21 WARNER TV 22 AMC 23 AXN 24 FOX 25 SONY 26 E! ENTERTAINMENT 28 NATGEO WILD 29 SYFY 30 AyE 31 HOME AND HEALTH 32 ID 33 DISCOVERY 34 TNT SERIES 35 ANIMAL PLANET 36 TLC 37 HISTORY 38 NATGEO 39 H2 40 TRU TV 41 CIVILIZATION 42 TURBO 43 SCIENCE 44 MAS CHIC 45 FOX LIFE 46 FOOD NETWORK 52 FOX SPORTS 2 53 FOX SPORTS 3 54 ESPN 2 55 T&C SPORTS 56 ESPN 57 FOX SPORTS 58 ESPN 3 60 GOL TV 69 BOLIVISION 70 FULL TV 71 BOLIVIA TV 72 UNITEL 73 TV U 74 RED UNO 75 MEGAVISION 76 GIGAVISION 77 CADENA A 78 ATB 79 PAT 80 TV CULTURAS 81 FX 83 GLITZ 84 TELEMUNDO INTL 85 TL NOVELAS 86 TVE 87 ESTRELLAS 88 TV CHILE 89 TELEFE 90 AMERICA INTL 91 EL TRECE 93 CARACOL INTL 94 DEUTSCHE WELLE 95 RAI 96 TV 5 98 GLOBO INTL 110 CNN EN ESPAÑOL 111 CNN INTL 112 FOX NEWS 113 TELESUR 115 ENLACE 116 EWTN 120 RITMOSON 121 HTV 122 TELEHIT 123 LIFETIME 124 MTV 125 MTV HITS 127 VH 1 146 SPACE 147 ISAT 148 HBO 149 UNIVERSAL 150 CINEMAX 151 CINE CANAL 152 TNT 153 GOLDEN 154 FILM ZONE 155 STD UNIVERSAL 156 TCM 157 DE PELICULA 301 COCKTAIL LOUNGE 302 OPERA 303 GROOVE LOUNGE 304 JAZZ CLASICO 305 ROCK ALTERNATIVO 306 90s HITS 307 ROCK PESADO 308 70s HITS 309 80s HITS 310 LOVE SONGS 311 MUSICA TROPICAL 312 POP INFANTIL 313 TOP 40 BRASIL 314 ROCK CLASICO 315 REGGAE 316 EXITOS EN INGLES 317 DANCE 318 URBAN BEAT 319 BANDAS SONORAS 320 JAZZ LATINO 321 ALL DAY PARTY 322 POP BRASIL 323 SAMBA Y PAGODE 324 ROCK POP BRASIL 325 NEW AGE 326 ROCK LATINO 327 MEXICO 328 POWER HITS 329 MARIACHI 330 BIG BAND 331 GREAT SINGERS 332 TANGO 333 WORLD BEAT 334 SINFONICA 335 ITALIA 336 ROCK OLDIES 337 CARIBBEAN 338 MUSIC OF AMERICA 339 LATIN LOUNGE 340 BLUES 341 MUSICA CLASICA 342 CONTEMPORARY 343 REGGAETON 344 NEW WAVE 345 SALSA Y MERENGUE 346 RETRODISCO 347 EXITOS LATINOS 348 EXITOS EUROPEOS 349 EASY LISTENING 350 BALADAS LATINAS. -

23-29 November 2020 Page 2

23-29 November C NTENT 2020 www.contentasia.tv l www.contentasiasummit.com COMING SOON 2020 winners at www.contentasiaawards.com DECEMBER 2020 C NTENT Schwebig unveils Price Guide: Who spends ContentAsia’s country-by-country look Trending: LGBTQ+ what on production in Asia at the top issue in Asia going into 2021 content in Asia new leadership structure Magdalene Ew takes over WarnerMedia original production WarnerMedia India/SEA/Korea head, Clement Schwebig, unveiled his new-look team this afternoon, putting Magda- lene Ew in charge of all entertainment programming and original production. Jessica Kam, original productions SVP, exits as part of the new structure, along with South Asia head Siddharth Jain. The full story is on page 2 q Price Guide: Who spends what on production in Asia Xmas bow for ContentAsia’s country-by-country Taiwan LGBTQ hit look at the top issues in Asia going into 2021 on Netflix Trending: LGBTQ+ content in Asia Exclusive global rights for Your Name Engraved Herein All in the latest issue of ContentAsia online Netflix premieres Taiwanese blockbust- For editorial info, contact Janine at [email protected] To advertise in any of ContentAsia’s publications or online, er, Patrick Liu’s NT$50-million Your Name contact Masliana at [email protected] (Asia, Australia and Middle East) Engraved Herein, on 23 Dec in an ex- or Leah at [email protected] (Americas and Europe) clusive global deal that throws even more light on Taiwan’s lead as an Asian www.contentasia.tv creative centre. contentasia The full story is on page 4 C NTENTASIA 23-29 November 2020 Page 2.