Transcript: National Symposium for Future Electricity Networks 19 Th January 2011

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

What's up with Woodford?

BUSINESS WITH PERSONALITY RUNNERS AND WHAT’S UP WITH WOODFORD? RIDERS WILL THE FORMER STAR’S FUND FROZEN NEXT PM BE PRO- AFTER CLIENTS PULL OUT P3 OR ANTI-HS2? P15 TUESDAY 4 JUNE 2019 ISSUE 3,384 CITYAM.COM FREE DOWNTOBUSINESS TRUMP AND MAY SET FOR BREAKFAST TRADE DEAL ON THE MENU... MEETING WITH 10 LEADING BOSSES BUT CHINA FEUD HITS MARKETS OWEN BENNETT the US – will break bread at St James’s chairman Sir Roger Carr, is expected to The business breakfast comes as One touched down in Stansted. @owenjbennett Palace alongside Trump, outgoing say the UK-US trade relationship “is a global markets continue to take fright at Khan hit back, releasing a video Prime Minister Theresa May and Prince great partnership, but one I believe we Trump’s escalating trade war, with the strongly criticising Trump. He said: BUSINESS leaders will sit down for Andrew, the Duke of York. can make greater still”. S&P 500 down more than 200 points “President Trump, if you are watching breakfast with US President Donald Chief executive officers and senior rep- She will say the two countries should (seven per cent) in the last month. this, your values, and what you stand Trump this morning as part of a bid to resentatives from BAE Systems, Glaxo- work together on “keeping markets Trump arrived in the UK yesterday for, are the opposite of London’s values strengthen transatlantic relations, as smithkline, National Grid, Barclays, free, fair and open, and keeping our morning and immediately sparked a and the values of this country.” fears over an impending global trade Reckitt Benckiser, JP Morgan, Lockheed industries competitive,” calling for a war of words with London mayor Sadiq Large protests are expected in central war continue to mount. -

THE 422 Mps WHO BACKED the MOTION Conservative 1. Bim

THE 422 MPs WHO BACKED THE MOTION Conservative 1. Bim Afolami 2. Peter Aldous 3. Edward Argar 4. Victoria Atkins 5. Harriett Baldwin 6. Steve Barclay 7. Henry Bellingham 8. Guto Bebb 9. Richard Benyon 10. Paul Beresford 11. Peter Bottomley 12. Andrew Bowie 13. Karen Bradley 14. Steve Brine 15. James Brokenshire 16. Robert Buckland 17. Alex Burghart 18. Alistair Burt 19. Alun Cairns 20. James Cartlidge 21. Alex Chalk 22. Jo Churchill 23. Greg Clark 24. Colin Clark 25. Ken Clarke 26. James Cleverly 27. Thérèse Coffey 28. Alberto Costa 29. Glyn Davies 30. Jonathan Djanogly 31. Leo Docherty 32. Oliver Dowden 33. David Duguid 34. Alan Duncan 35. Philip Dunne 36. Michael Ellis 37. Tobias Ellwood 38. Mark Field 39. Vicky Ford 40. Kevin Foster 41. Lucy Frazer 42. George Freeman 43. Mike Freer 44. Mark Garnier 45. David Gauke 46. Nick Gibb 47. John Glen 48. Robert Goodwill 49. Michael Gove 50. Luke Graham 51. Richard Graham 52. Bill Grant 53. Helen Grant 54. Damian Green 55. Justine Greening 56. Dominic Grieve 57. Sam Gyimah 58. Kirstene Hair 59. Luke Hall 60. Philip Hammond 61. Stephen Hammond 62. Matt Hancock 63. Richard Harrington 64. Simon Hart 65. Oliver Heald 66. Peter Heaton-Jones 67. Damian Hinds 68. Simon Hoare 69. George Hollingbery 70. Kevin Hollinrake 71. Nigel Huddleston 72. Jeremy Hunt 73. Nick Hurd 74. Alister Jack (Teller) 75. Margot James 76. Sajid Javid 77. Robert Jenrick 78. Jo Johnson 79. Andrew Jones 80. Gillian Keegan 81. Seema Kennedy 82. Stephen Kerr 83. Mark Lancaster 84. -

FDN-274688 Disclosure

FDN-274688 Disclosure MP Total Adam Afriyie 5 Adam Holloway 4 Adrian Bailey 7 Alan Campbell 3 Alan Duncan 2 Alan Haselhurst 5 Alan Johnson 5 Alan Meale 2 Alan Whitehead 1 Alasdair McDonnell 1 Albert Owen 5 Alberto Costa 7 Alec Shelbrooke 3 Alex Chalk 6 Alex Cunningham 1 Alex Salmond 2 Alison McGovern 2 Alison Thewliss 1 Alistair Burt 6 Alistair Carmichael 1 Alok Sharma 4 Alun Cairns 3 Amanda Solloway 1 Amber Rudd 10 Andrea Jenkyns 9 Andrea Leadsom 3 Andrew Bingham 6 Andrew Bridgen 1 Andrew Griffiths 4 Andrew Gwynne 2 Andrew Jones 1 Andrew Mitchell 9 Andrew Murrison 4 Andrew Percy 4 Andrew Rosindell 4 Andrew Selous 10 Andrew Smith 5 Andrew Stephenson 4 Andrew Turner 3 Andrew Tyrie 8 Andy Burnham 1 Andy McDonald 2 Andy Slaughter 8 FDN-274688 Disclosure Angela Crawley 3 Angela Eagle 3 Angela Rayner 7 Angela Smith 3 Angela Watkinson 1 Angus MacNeil 1 Ann Clwyd 3 Ann Coffey 5 Anna Soubry 1 Anna Turley 6 Anne Main 4 Anne McLaughlin 3 Anne Milton 4 Anne-Marie Morris 1 Anne-Marie Trevelyan 3 Antoinette Sandbach 1 Barry Gardiner 9 Barry Sheerman 3 Ben Bradshaw 6 Ben Gummer 3 Ben Howlett 2 Ben Wallace 8 Bernard Jenkin 45 Bill Wiggin 4 Bob Blackman 3 Bob Stewart 4 Boris Johnson 5 Brandon Lewis 1 Brendan O'Hara 5 Bridget Phillipson 2 Byron Davies 1 Callum McCaig 6 Calum Kerr 3 Carol Monaghan 6 Caroline Ansell 4 Caroline Dinenage 4 Caroline Flint 2 Caroline Johnson 4 Caroline Lucas 7 Caroline Nokes 2 Caroline Spelman 3 Carolyn Harris 3 Cat Smith 4 Catherine McKinnell 1 FDN-274688 Disclosure Catherine West 7 Charles Walker 8 Charlie Elphicke 7 Charlotte -

Download (9MB)

A University of Sussex PhD thesis Available online via Sussex Research Online: http://sro.sussex.ac.uk/ This thesis is protected by copyright which belongs to the author. This thesis cannot be reproduced or quoted extensively from without first obtaining permission in writing from the Author The content must not be changed in any way or sold commercially in any format or medium without the formal permission of the Author When referring to this work, full bibliographic details including the author, title, awarding institution and date of the thesis must be given Please visit Sussex Research Online for more information and further details 2018 Behavioural Models for Identifying Authenticity in the Twitter Feeds of UK Members of Parliament A CONTENT ANALYSIS OF UK MPS’ TWEETS BETWEEN 2011 AND 2012; A LONGITUDINAL STUDY MARK MARGARETTEN Mark Stuart Margaretten Submitted for the degree of Doctor of PhilosoPhy at the University of Sussex June 2018 1 Table of Contents TABLE OF CONTENTS ........................................................................................................................ 1 DECLARATION .................................................................................................................................. 4 ACKNOWLEDGMENTS ...................................................................................................................... 5 FIGURES ........................................................................................................................................... 6 TABLES ............................................................................................................................................ -

Whole Day Download the Hansard

Monday Volume 663 8 July 2019 No. 326 HOUSE OF COMMONS OFFICIAL REPORT PARLIAMENTARY DEBATES (HANSARD) Monday 8 July 2019 © Parliamentary Copyright House of Commons 2019 This publication may be reproduced under the terms of the Open Parliament licence, which is published at www.parliament.uk/site-information/copyright/. HER MAJESTY’S GOVERNMENT MEMBERS OF THE CABINET (FORMED BY THE RT HON. THERESA MAY, MP, JUNE 2017) PRIME MINISTER,FIRST LORD OF THE TREASURY AND MINISTER FOR THE CIVIL SERVICE—The Rt Hon. Theresa May, MP CHANCELLOR OF THE DUCHY OF LANCASTER AND MINISTER FOR THE CABINET OFFICE—The Rt Hon. David Lidington, MP CHANCELLOR OF THE EXCHEQUER—The Rt Hon. Philip Hammond, MP SECRETARY OF STATE FOR THE HOME DEPARTMENT—The Rt Hon. Sajid Javid, MP SECRETARY OF STATE FOR FOREIGN AND COMMONWEALTH AFFAIRS—The Rt. Hon Jeremy Hunt, MP SECRETARY OF STATE FOR EXITING THE EUROPEAN UNION—The Rt Hon. Stephen Barclay, MP SECRETARY OF STATE FOR DEFENCE AND MINISTER FOR WOMEN AND EQUALITIES—The Rt Hon. Penny Mordaunt, MP LORD CHANCELLOR AND SECRETARY OF STATE FOR JUSTICE—The Rt Hon. David Gauke, MP SECRETARY OF STATE FOR HEALTH AND SOCIAL CARE—The Rt Hon. Matt Hancock, MP SECRETARY OF STATE FOR BUSINESS,ENERGY AND INDUSTRIAL STRATEGY—The Rt Hon. Greg Clark, MP SECRETARY OF STATE FOR INTERNATIONAL TRADE AND PRESIDENT OF THE BOARD OF TRADE—The Rt Hon. Liam Fox, MP SECRETARY OF STATE FOR WORK AND PENSIONS—The Rt Hon. Amber Rudd, MP SECRETARY OF STATE FOR EDUCATION—The Rt Hon. Damian Hinds, MP SECRETARY OF STATE FOR ENVIRONMENT,FOOD AND RURAL AFFAIRS—The Rt Hon. -

Public Forum, G&R Scrutiny Commission 6-1-21 PDF 650 KB

Public Document Pack Growth and Regeneration Scrutiny Commission Supplementary Information Date: Wednesday, 6 January 2021 Time: 3.00 pm Venue: Virtual Meeting - Zoom Committee Meeting with Public Access via YouTube 4. Public Forum Up to 30 minutes is allowed for this item. (Pages 3 - 21) I Issued by: Dan Berlin City Hall, Bristol, BS1 9NE Tel: 0117 90 36898 E-mail: [email protected] Date: Wednesday, 06 January 2021 Agenda Item 4 Growth & Regeneration Scrutiny Commission 2020 Public Forum 3 spe Growth & Regeneration Scrutiny Commission 6th January 2021 Public Forum Questions Ref Name Page No. David Redgewell, South West Transport Network and Railfuture Q 1 & 2 2 Severnside. Q3 Councillor Huw James, North Somerset Council 3 Q4 & 5 Councillor Clive Stevens 3-4 Q6, 7, & 8 Councillor Paula O’Rourke 4-5 Statements Ref Name Page No. David Redgewell, South West Transport Network and Railfuture S1 6 Severnside. S2 Lucy Travis, Somerset Catch the Bus Campaign 8 S3 Gordon Richardson, Chair, Bristol Disabled Equalities Forum 10 S4 Christina Biggs, Friends of Suburban Bristol Railways 11 S5 Councillor Jerome Thomas 14 S6 Martin Garrett, Transport for Greater Bristol 15 S7 Dick Daniel, Bath Area Trams Association 18 1 Page 2 Growth & Regeneration Scrutiny Commission 2020 Public Forum Questions Q1: David Redgewell What progress has been made in discussions with secretary of state for local government, Robert Jenrick MP and ministers for local government, Luke Hall MP on a second Devolution deal to allow North Somerset Council to join -

Stephen Kinnock MP Aberav

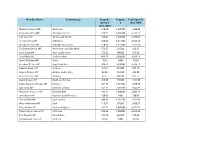

Member Name Constituency Bespoke Postage Total Spend £ Spend £ £ (Incl. VAT) (Incl. VAT) Stephen Kinnock MP Aberavon 318.43 1,220.00 1,538.43 Kirsty Blackman MP Aberdeen North 328.11 6,405.00 6,733.11 Neil Gray MP Airdrie and Shotts 436.97 1,670.00 2,106.97 Leo Docherty MP Aldershot 348.25 3,214.50 3,562.75 Wendy Morton MP Aldridge-Brownhills 220.33 1,535.00 1,755.33 Sir Graham Brady MP Altrincham and Sale West 173.37 225.00 398.37 Mark Tami MP Alyn and Deeside 176.28 700.00 876.28 Nigel Mills MP Amber Valley 489.19 3,050.00 3,539.19 Hywel Williams MP Arfon 18.84 0.00 18.84 Brendan O'Hara MP Argyll and Bute 834.12 5,930.00 6,764.12 Damian Green MP Ashford 32.18 525.00 557.18 Angela Rayner MP Ashton-under-Lyne 82.38 152.50 234.88 Victoria Prentis MP Banbury 67.17 805.00 872.17 David Duguid MP Banff and Buchan 279.65 915.00 1,194.65 Dame Margaret Hodge MP Barking 251.79 1,677.50 1,929.29 Dan Jarvis MP Barnsley Central 542.31 7,102.50 7,644.81 Stephanie Peacock MP Barnsley East 132.14 1,900.00 2,032.14 John Baron MP Basildon and Billericay 130.03 0.00 130.03 Maria Miller MP Basingstoke 209.83 1,187.50 1,397.33 Wera Hobhouse MP Bath 113.57 976.00 1,089.57 Tracy Brabin MP Batley and Spen 262.72 3,050.00 3,312.72 Marsha De Cordova MP Battersea 763.95 7,850.00 8,613.95 Bob Stewart MP Beckenham 157.19 562.50 719.69 Mohammad Yasin MP Bedford 43.34 0.00 43.34 Gavin Robinson MP Belfast East 0.00 0.00 0.00 Paul Maskey MP Belfast West 0.00 0.00 0.00 Neil Coyle MP Bermondsey and Old Southwark 1,114.18 7,622.50 8,736.68 John Lamont MP Berwickshire Roxburgh -

Equality Bill Committee Stage Report Bill No 131 of 2008-09 RESEARCH PAPER 09/83 13 November 2009

Equality Bill Committee Stage Report Bill No 131 of 2008-09 RESEARCH PAPER 09/83 13 November 2009 This is a report on the House of Commons Committee Stage of the Equality Bill. It complements and may be read in conjunction with the Library research paper RP 09/42 on the Bill which was prepared for Second Reading in Commons. The Bill was introduced into the House of Commons on 24 April 2009. It had its Second Reading in the House of Commons on 11 May 2009. The Bill was amended in Committee and new clauses were added, in particular a clause providing for “dual discrimination” based on a combination of two of the protected characteristics covered by the Bill. The amendments made were largely technical, such as to correct drafting errors and omissions. Legislation to outlaw discrimination has existed for over 40 years. Typically, new Acts have had as their focus one area of policy, for example, pay, equal treatment of women, race discrimination etc. Almost inevitably, the body of current law, introduced piece meal over such a long period, has developed inconsistencies of both content and approach. As well as introducing new requirements one of the main aims of this Bill is to harmonise existing law into a more coherent whole. Vincent Keter Recent Research Papers 09/73 Constitutional Reform and Governance Bill [Bill 142 of 2008-09] 06.10.09 09/74 Economic indicators, October 2009 07.10.09 09/75 The Treaty of Lisbon after the Second Irish Referendum 08.10.09 09/76 Social Indicators 15.10.09 09/77 Unemployment by Constituency, September 2009 -

(A) Ex-Officio Members

Ex-Officio Members of Court (A) EX-OFFICIO MEMBERS (i) The Chancellor His Royal Highness The Earl of Wessex (ii) The Pro-Chancellors Sir Julian Horn-Smith Mr Peter Troughton Mr Roger Whorrod (iii) The Vice-Chancellor Professor Dame Glynis Breakwell (iv) The Treasurer Mr John Preston (v) The Deputy Vice-Chancellor and Pro-Vice-Chancellors Professor Bernie Morley, Deputy Vice-Chancellor & Provost Professor Jeremy Bradshaw, Pro-Vice-Chancellor (International & Doctoral) Professor Jonathan Knight, Pro-Vice-Chancellor (Research) Professor Peter Lambert, Pro-Vice-Chancellor (Learning & Teaching) (vi) The Heads of Schools Professor Veronica Hope Hailey, Dean and Head of the School of Management Professor Nick Brook, Dean of the Faculty of Science Professor David Galbreath, Dean of the Faculty of Humanities and Social Sciences Professor Gary Hawley, Dean of the Faculty of Engineering and Design (vii) The Chair of the Academic Assembly Dr Aki Salo (viii) The holders of such offices in the University not exceeding five in all as may from time to time be prescribed by the Ordinances Mr Mark Humphriss, University Secretary Ms Kate Robinson, University Librarian Mr Martin Williams, Director of Finance Ex-Officio Members of Court Mr Martyn Whalley, Director of Estates (ix) The President of the Students' Union and such other officers of the Students' Union as may from time to time be prescribed in the Ordinances Mr Ben Davies, Students' Union President Ms Chloe Page, Education Officer Ms Kimberley Pickett, Activities Officer Mr Will Galloway, Sports -

United Kingdom Progress Report 2016-2017

Independent Reporting Mechanism (IRM): United Kingdom Progress Report 2016-2017 Ben Worthy, Birkbeck College, University of London Table of Contents Executive Summary ............................................................................................... 3 I. Introduction ...................................................................................................... 11 II. Context ............................................................................................................. 12 III. Leadership and Multi-stakeholder Process .............................................. 16 IV. Commitments ................................................................................................. 24 1. Beneficial ownership ....................................................................................................................... 26 2. Natural resource transparency .................................................................................................... 30 3. Anti-Corruption Strategy .............................................................................................................. 34 4. Anti-Corruption Innovation Hub ................................................................................................ 39 5. Open contracting ............................................................................................................................ 42 6. Grants data ...................................................................................................................................... -

List of Ministers' Interests

LIST OF MINISTERS’ INTERESTS CABINET OFFICE DECEMBER 2015 CONTENTS Introduction 1 Prime Minister 3 Attorney General’s Office 5 Department for Business, Innovation and Skills 6 Cabinet Office 8 Department for Communities and Local Government 10 Department for Culture, Media and Sport 12 Ministry of Defence 14 Department for Education 16 Department of Energy and Climate Change 18 Department for Environment, Food and Rural Affairs 19 Foreign and Commonwealth Office 20 Department of Health 22 Home Office 24 Department for International Development 26 Ministry of Justice 27 Northern Ireland Office 30 Office of the Advocate General for Scotland 31 Office of the Leader of the House of Commons 32 Office of the Leader of the House of Lords 33 Scotland Office 34 Department for Transport 35 HM Treasury 37 Wales Office 39 Department for Work and Pensions 40 Government Whips – Commons 42 Government Whips – Lords 46 INTRODUCTION Ministerial Code Under the terms of the Ministerial Code, Ministers must ensure that no conflict arises, or could reasonably be perceived to arise, between their Ministerial position and their private interests, financial or otherwise. On appointment to each new office, Ministers must provide their Permanent Secretary with a list in writing of all relevant interests known to them which might be thought to give rise to a conflict. Individual declarations, and a note of any action taken in respect of individual interests, are then passed to the Cabinet Office Propriety and Ethics team and the Independent Adviser on Ministers’ Interests to confirm they are content with the action taken or to provide further advice as appropriate. -

The Penrose Report | Power to the People 0

The Penrose Report | Power To The People 0 The Penrose Report | Power To The People Acknowledgements & Thanks I’d like to thank everyone who has so kindly lent me their time, expertise and – above all – patience as I’ve asked annoying questions during the preparation and drafting of this report. But most of all I’d like to thank my long-suffering secretariat of officials from the Treasury and Department of Business, Energy and Industrial Strategy who have helped to compile and write it with me. 1 The Penrose Report | Power To The People About The Author John Penrose has been MP for Weston-super-Mare since 2005. His campaigns to reboot British capitalism so our economy works for the many, not the few, include the Energy Price Cap; making housing cheaper to own or rent by allowing urban owners and developers to Build Up Not Out; making Britain’s economy more generationally-and-socially-just through a UK Sovereign Wealth Fund; and reforming formerly-nationalised utilities (e.g. energy, telecoms, water, rail) to put customers in charge, rather than politicians, bureaucrats or regulators instead. A successful businessman before he entered politics, John has held a variety of posts since he was elected including PPS to Oliver Letwin, Shadow Business Minister, Tourism & Heritage Minister, Government Whip, Constitution Minister and Northern Ireland Minister. He is currently the Prime Minister’s Anti-Corruption Champion, Chair of the Conservative Policy Forum and sits on the Party’s Policy Board. This is an independent report represented to the Government; it is not a statement of Government or Conservative Party policy.