Mizuho BK Custody and Proxy Board Lot Size List JUL 27 , 2021 21LADY

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Software Sector Summary Report

SOFTWARE SECTOR REPORT Q1 2019 GCA: A LEADING INDEPENDENT GLOBAL INVESTMENT BANK Global investment bank providing strategic M&A and capital markets advisory services to growth companies and market leaders LEEDS PARIS FRANKFURT MANCHESTER MUNICH ZURICH NAGOYA TOKYO LONDON SHANGHAI NEW YORK MILAN NEW DELHI OSAKA TEL AVIV FUKUOKA SAN FRANCISCO TAIPEI MUMBAI SINGAPORE HO CHI MINH CITY Global platform: Sector expertise: Exceptional cross- 21 offices in key Experienced team: Expansive coverage border capabilities: markets across Over 400 employees and deep Over a third of all America, Asia and across the globe specialization transactions Europe Broad spectrum Diversified Strong reputation of clients: business model: and track record: Leading Geographically High number of conglomerates, top balanced, synergistic repeat clients and private equity firms and complementary referrals and emerging high- focus areas growth companies 2 GCA operates as GCA in America and Asia, and GCA Altium in Europe GCA OVERVIEW The GCA Software Team US Team Paul DiNardo Daniel Avrutsky Rupert Sadler Josh Wepman Managing Director Managing Director Managing Director Managing Director Software HCM Software Software, Travel & Telematics Software & Digital Media [email protected] [email protected] [email protected] [email protected] James Orozco Clark Callander Chris Gough Kevin Walsh Managing Director Managing Director Managing Director Managing Director Financial Sponsors Technology Real Estate Tech Software & Digital Media [email protected] [email protected] -

Including League Tables of Financial Advisors

An Acuris Company Finding the opportunities in mergers and acquisitions Global & Regional M&A Report 2019 Including League Tables of Financial Advisors mergermarket.com An Acuris Company Content Overview 03 Global 04 Global Private Equity 09 Europe 14 US 19 Latin America 24 Asia Pacific (excl. Japan) 29 Japan 34 Middle East & Africa 39 M&A and PE League Tables 44 Criteria & Contacts 81 mergermarket.com Mergermarket Global & Regional Global Overview 3 M&A Report 2019 Global Overview Regional M&A Comparison North America USD 1.69tn 1.5% vs. 2018 Inbound USD 295.8bn 24.4% Outbound USD 335.3bn -2.9% PMB USD 264.4bn 2.2x Latin America USD 85.9bn 12.5% vs. 2018 Inbound USD 56.9bn 61.5% Outbound USD 8.9bn 46.9% EMU USD 30.6bn 37.4% 23.1% Europe USD 770.5bn -21.9% vs. 2018 50.8% 2.3% Inbound USD 316.5bn -30.3% Outbound USD 272.1bn 28.3% PMB USD 163.6bn 8.9% MEA USD 141.2bn 102% vs. 2018 Inbound USD 49.2bn 29% Outbound USD 22.3bn -15.3% Ind. & Chem. USD 72.5bn 5.2x 4.2% 17% 2.6% APAC (ex. Japan) USD 565.3bn -22.5% vs. 2018 Inbound USD 105.7bn -14.8% Outbound USD 98.9bn -24.5% Ind. & Chem. USD 111.9bn -5.3% Japan USD 75.4bn 59.5% vs. 2018 Inbound USD 12.4bn 88.7% Global M&A USD 3.33tn -6.9% vs. 2018 Outbound USD 98.8bn -43.6% Technology USD 21.5bn 2.8x Cross-border USD 1.27tn -6.2% vs. -

Software Sector Summary Report

Software COMPANYSector PRESENTATION Summary Week of October 2, 2017 1 DEAL DASHBOARD Software $35.9 Billion 470 $29.1 Billion 76 Financing Volume YTD (1)(2) Financing Transactions YTD (1)(2) M&A Volume YTD (3) M&A Transactions YTD (3) Select Financing Transactions Quarterly Financing Volume (1)(2) Quarterly M&A Volume (3) Select M&A Transactions (4) $Bn $Bn (61)% Company Amount ($MM) 43% Target Acquirer EV ($MM) $14 $50 $270 $12 $41 $3,903 $10 $11 $9 $6 $6 $24 $250 $6 $5 $1,125 $16 $15 $12 ( ) $12 $6 $5 $70 $834 ( ) Q3'15 Q4'15 Q1'16 Q2'16Q3'16 Q4'16 Q1'17 Q2'17 Q3'17 Q3'15 Q4'15 Q1'16 Q2'16 Q3'16 Q4'16 Q1'17 Q2'17 Q3'17 $45 Quarterly Financing Deal Count (1)(2) Quarterly M&A Deal Count (3) $614 36% $35 9% $531 156 160 154 127 118 123 103 111 $35 94 29 29 29 29 $382 24 24 26 21 $32 14 $344 $26 $270 Q3'15 Q4'15 Q1'16 Q2'16Q3'16 Q4'16 Q1'17 Q2'17 Q3'17 Q3'15 Q4'15 Q1'16 Q2'16 Q3'16 Q4'16 Q1'17 Q2'17 Q3'17 Last 12 Months Software Price Performance vs. S&P 500 (5) M&A EV/ NTM Rev. Over Time (6) 35.0% SPX IGV All Buyers Strategic Buyers PE Buyers 30.0% 30% 6 ` 5.3x Financing Activity by Quarter 4.7x 4.9x 5 4.5x 4.6x 25.0% 4.2x 4.3x 4.0x 4.1x 3.9x 3.9x 3.7x 20.0% 4 3.6x 3.1x 16% 2.7x 2.9x 2.9x 15.0% 3 2.5x 2.5x 2.5x 2.2x 10.0% 2 5.0% 1 0.0% 0 Sep-16 Oct-16 Nov-16 Dec-16 Jan-17 Feb-17 Mar-17 Apr-17 May-17 Jun-17 Jul-17 Aug-17 2011 2012 2013 2014 2015 2016 2017 (5.0%) (10.0%) Notes: Source: Capital IQ, PitchBook, and Dow Jones VentureSource. -

Including League Tables of Financial Advisors

An Acuris Company Finding the opportunities in mergers and acquisitions Global & Regional M&A Report 2019 Including League Tables of Financial Advisors mergermarket.com An Acuris Company Content Overview 03 Global 04 Global Private Equity 09 Europe 14 US 19 Latin America 24 Asia Pacific (excl. Japan) 29 Japan 34 Middle East & Africa 39 M&A and PE League Tables 44 Criteria & Contacts 81 mergermarket.com Mergermarket Global & Regional Global Overview 3 M&A Report 2019 Global Overview Regional M&A Comparison North America USD 1.69tn 1.5% vs. 2018 Inbound USD 295.8bn 24.4% Outbound USD 335.3bn -2.9% PMB USD 264.4bn 2.2x Latin America USD 85.9bn 12.5% vs. 2018 Inbound USD 56.9bn 61.5% Outbound USD 8.9bn 46.9% EMU USD 30.6bn 37.4% 23.1% Europe USD 770.5bn -21.9% vs. 2018 50.8% 2.3% Inbound USD 316.5bn -30.3% Outbound USD 272.1bn 28.3% PMB USD 163.6bn 8.9% MEA USD 141.2bn 102% vs. 2018 Inbound USD 49.2bn 29% Outbound USD 22.3bn -15.3% Ind. & Chem. USD 72.5bn 5.2x 4.2% 17% 2.6% APAC (ex. Japan) USD 565.3bn -22.5% vs. 2018 Inbound USD 105.7bn -14.8% Outbound USD 98.9bn -24.5% Ind. & Chem. USD 111.9bn -5.3% Japan USD 75.4bn 59.5% vs. 2018 Inbound USD 12.4bn 88.7% Global M&A USD 3.33tn -6.9% vs. 2018 Outbound USD 98.8bn -43.6% Technology USD 21.5bn 2.8x Cross-border USD 1.27tn -6.2% vs. -

"JPX-Nikkei Index 400"

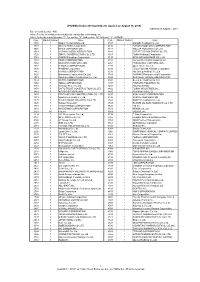

JPX-Nikkei Index 400 Constituents (applied on August 30, 2019) Published on August 7, 2019 No. of constituents : 400 (Note) The No. of constituents is subject to change due to de-listing. etc. (Note) As for the market division, "1"=1st section, "2"=2nd section, "M"=Mothers, "J"=JASDAQ. Code Market Divison Issue Code Market Divison Issue 1332 1 Nippon Suisan Kaisha,Ltd. 3107 1 Daiwabo Holdings Co.,Ltd. 1333 1 Maruha Nichiro Corporation 3116 1 TOYOTA BOSHOKU CORPORATION 1605 1 INPEX CORPORATION 3141 1 WELCIA HOLDINGS CO.,LTD. 1719 1 HAZAMA ANDO CORPORATION 3148 1 CREATE SD HOLDINGS CO.,LTD. 1720 1 TOKYU CONSTRUCTION CO., LTD. 3167 1 TOKAI Holdings Corporation 1721 1 COMSYS Holdings Corporation 3197 1 SKYLARK HOLDINGS CO.,LTD. 1801 1 TAISEI CORPORATION 3231 1 Nomura Real Estate Holdings,Inc. 1802 1 OBAYASHI CORPORATION 3254 1 PRESSANCE CORPORATION 1803 1 SHIMIZU CORPORATION 3288 1 Open House Co.,Ltd. 1808 1 HASEKO Corporation 3289 1 Tokyu Fudosan Holdings Corporation 1812 1 KAJIMA CORPORATION 3291 1 Iida Group Holdings Co.,Ltd. 1820 1 Nishimatsu Construction Co.,Ltd. 3349 1 COSMOS Pharmaceutical Corporation 1821 1 Sumitomo Mitsui Construction Co., Ltd. 3360 1 SHIP HEALTHCARE HOLDINGS,INC. 1824 1 MAEDA CORPORATION 3382 1 Seven & I Holdings Co.,Ltd. 1860 1 TODA CORPORATION 3391 1 TSURUHA HOLDINGS INC. 1861 1 Kumagai Gumi Co.,Ltd. 3401 1 TEIJIN LIMITED 1878 1 DAITO TRUST CONSTRUCTION CO.,LTD. 3402 1 TORAY INDUSTRIES,INC. 1881 1 NIPPO CORPORATION 3405 1 KURARAY CO.,LTD. 1893 1 PENTA-OCEAN CONSTRUCTION CO.,LTD. 3407 1 ASAHI KASEI CORPORATION 1911 1 Sumitomo Forestry Co.,Ltd. -

International Smallcap Separate Account As of July 31, 2017

International SmallCap Separate Account As of July 31, 2017 SCHEDULE OF INVESTMENTS MARKET % OF SECURITY SHARES VALUE ASSETS AUSTRALIA INVESTA OFFICE FUND 2,473,742 $ 8,969,266 0.47% DOWNER EDI LTD 1,537,965 $ 7,812,219 0.41% ALUMINA LTD 4,980,762 $ 7,549,549 0.39% BLUESCOPE STEEL LTD 677,708 $ 7,124,620 0.37% SEVEN GROUP HOLDINGS LTD 681,258 $ 6,506,423 0.34% NORTHERN STAR RESOURCES LTD 995,867 $ 3,520,779 0.18% DOWNER EDI LTD 119,088 $ 604,917 0.03% TABCORP HOLDINGS LTD 162,980 $ 543,462 0.03% CENTAMIN EGYPT LTD 240,680 $ 527,481 0.03% ORORA LTD 234,345 $ 516,380 0.03% ANSELL LTD 28,800 $ 504,978 0.03% ILUKA RESOURCES LTD 67,000 $ 482,693 0.03% NIB HOLDINGS LTD 99,941 $ 458,176 0.02% JB HI-FI LTD 21,914 $ 454,940 0.02% SPARK INFRASTRUCTURE GROUP 214,049 $ 427,642 0.02% SIMS METAL MANAGEMENT LTD 33,123 $ 410,590 0.02% DULUXGROUP LTD 77,229 $ 406,376 0.02% PRIMARY HEALTH CARE LTD 148,843 $ 402,474 0.02% METCASH LTD 191,136 $ 399,917 0.02% IOOF HOLDINGS LTD 48,732 $ 390,666 0.02% OZ MINERALS LTD 57,242 $ 381,763 0.02% WORLEYPARSON LTD 39,819 $ 375,028 0.02% LINK ADMINISTRATION HOLDINGS 60,870 $ 374,480 0.02% CARSALES.COM AU LTD 37,481 $ 369,611 0.02% ADELAIDE BRIGHTON LTD 80,460 $ 361,322 0.02% IRESS LIMITED 33,454 $ 344,683 0.02% QUBE HOLDINGS LTD 152,619 $ 323,777 0.02% GRAINCORP LTD 45,577 $ 317,565 0.02% Not FDIC or NCUA Insured PQ 1041 May Lose Value, Not a Deposit, No Bank or Credit Union Guarantee 07-17 Not Insured by any Federal Government Agency Informational data only. -

Japan's Largest*!

Exhibiting Information for Next Shows To Enter and Expand your Business in the Japanese IT Market Japan’s Largest* ! NEW Autumn 2020 Osaka 2021 Spring 2021 Nagoya 2021 Oct. 28 ( Wed) – 30 (Fri), 2020 Jan. 27 ( Wed) – 29 (Fri), 2021 April 26 ( Mon) – 28 (Wed), 2021 July 28 (Wed) – 30 (Fri), 2021 Makuhari Messe, Japan INTEX Osaka, Japan Tokyo Big Sight, Japan Portmesse Nagoya, Japan Organiser: Reed Exhibitions Japan Ltd. * "Largest" in reference to the exhibitor number and the net exhibit space of trade shows with the same concept. Scenes from the previous Spring show in 2019 www.japan-it.jp/en/ What is Japan IT Week ? 1 All Kinds of IT Solutions Exhibitor Profile Active Visitor Profile & Professionals Gather Companies dealing in: Professionals from: • IoT/ 5G Business • Manufacturer • AI • Software Vendor/ Japan IT Week is a B2B exhibition where the latest IT products • Embedded/Edge Computing Meetings System Integrator and solutions gather in one place. • Software & Apps • Distribution/Logistics Many IT professionals visit the show to implement new IT • Information Security • Telecommunication technologies and engage with optimal business partners. • Cloud & BPR • Government/ • E-Commerce Solutions & Web Public Institute, Education • Store & Retail Solutions • PC, Computer Peripherals • Data Center/Storage Manufacturer • Sales Automation & CRM etc. • Enterprise etc. 2 Japan’s Largest * IT Show Autumn Edition Osaka Edition Spring Edition Nagoya Edition 2020: 2021: 2021: 2021: *1 *1 Japan IT Week is evaluated to be very well known in the Japanese IT 950 Exhibitors 430 Exhibitors 980 Exhibitors*1 250 Exhibitors*1 industry because of the large number of exhibitors and visitors. -

The Global Investment Banking Advisor for Asia March 2020 Experts in Asian M&A

The global investment banking advisor for Asia March 2020 Experts in Asian M&A Leading independent Asian investment banking firm 2020 marks 23 years of providing high-quality M&A advice Where we are Key facts We deliver global coverage for our clients from BDA’s own platform #1 Cross-border Asian sellside M&A advisor London 1996 Founded and led since then by the same team New York Seoul Shanghai Tokyo Bankers across three continents Hong Kong 100 Mumbai Ho Chi Minh City Offices globally Singapore 9 2 Strategic partners Our services How we are organized We provide M&A advisory services for: Divestitures Acquisitions Capital raisings Chemicals Consumer Healthcare & Retail Debt advisory & restructuring transactions Valuations Industrials Services Technology 2 On the ground, with local relationships BDA Partners is #1 for Asian cross-border private sellside M&A No other firm has built the same scale, focus, connectivity and deal flow in Asia Private, cross-border Asian sellside transactions up to US$1bn enterprise value, 2015-2019(1) Highlights Rank Advisor # of Deals 85% of M&A transactions were cross-border 1 31 85% of M&A transactions with BDA as sellside advisor 100% of transactions involved either the sale/acquisition of an Asian 2 29 asset, an Asian buyer or an Asian seller 3 29 4 28 Long-established Asian presence 5 26 Coverage across Asia 6 25 60+ bankers in Asia 7 countries Seoul 2002 Tokyo 7 24 23 years of relationship- Shanghai 2002 1998 building Hong Kong 8 19 2000 Mumbai 2005 Ho Chi Minh City 8 19 2014 Singapore We reach Asian buyers 1996 10 17 120+ assets sold to Asian buyers 20,000+ calls made to Asian buyers 600+ transactions with Asian participation Note: (1) Target headquartered in China, India, Japan, Korea or Southeast Asia; Control transactions: i.e. -

Deal Drivers: APAC HY 2021

Deal Drivers: APAC HY 2021 A spotlight on mergers and acquisitions trends in 2021 Contents Foreword: APAC an M&A bright spot despite COVID concerns 03 Outlook: APAC heat chart 04 All sectors 05 Consumer 14 Energy, mining & utilities 19 Financial services 24 Industrials & chemicals 29 Pharma, medical & biotech 34 Telecoms, media & technology 39 About this report 44 Foreword: APAC an M&A bright spot despite COVID concerns Having experienced the first wave of COVID-19 before the rest Robust activity of the world in the early months of 2020, countries across the Nevertheless, reasons to be optimistic remain. Vaccinations Asia Pacific (APAC) region hoped the post-pandemic trajectory in much of the region are now gathering pace, providing hope of recovery would continue smoothly during 2021. But while of an escape from the pandemic. The economic backdrop some parts of the region have seen no significant return of the is supportive too, with central banks across the region virus, with China in particular keeping cases to a minimum, maintaining loose monetary policies that look set to endure others have seen surging case numbers in recent months. into 2022. And there is certainly no shortage of capital to India has faced particular issues, but countries such as fund transactions. Singapore and Australia have also reported outbreaks despite tough restrictions. Despite a small quarter-on-quarter drop from Q1 to Q2 of this year, deal activity was still strong over the first half of 2021. Inevitably, this ongoing COVID-19 uncertainty has undermined There were 2,198 transactions up to the end of June—not confidence in some parts of the region. -

Pitchbook's Annual Global League Tables

Global League Tables 2019 Annual 1 PITCHBOOK 2019 ANNUAL GLOBAL LEAGUE TABLES Contents Credits & Contact PitchBook Data, Inc. Introduction 2 John Gabbert Founder, CEO Adley Bowden Vice President, PE firms 3-11 Market Development & Analysis VC firms 12-19 Content Garrett James Black Senior Advisors/accountants & investment banks 20-25 Manager, Custom Research & Publishing Law firms: VC & PE 26-35 Aria Nikkhoui Data Analyst II Keenan Durham Dataset Team Lead Acquirers 36-38 Kylie Hannus Senior Research Associate Kunal Rai Senior Research Associate Madison Bond Senior Research Associate Johnny Starcevich Research Associate Contact PitchBook Research [email protected] Cover design by Kelilah King Click here for PitchBook’s report methodologies. Introduction For the inaugural edition of Global League Tables in 2020, Once again, thanks to all the survey participants that we are doing something new. In addition to the usual collaborate with our teams; all the mutual hard work rankings provided here, we hope to release an interactive enables more accurate representation of overall private table in the coming weeks, which will hopefully present a markets activity. more user-friendly, immersive experience and avoid any spatial constraints. Garrett James Black However, the customary array of rankings can still be Senior Manager, Custom Research expected, from the breakdown of the most active private & Publishing equity firms by US region to the law firms that advise on the most M&A transactions worldwide. 2 PITCHBOOK 2019 ANNUAL GLOBAL LEAGUE -

Including League Tables of Financial Advisors

An Acuris Company Finding the opportunities in mergers and acquisitions Global & Regional M&A Report 1H19 Including League Tables of Financial Advisors mergermarket.com An Acuris Company Content Overview 03 Global 04 Global Private Equity 09 Europe 14 US 19 Latin America 24 AsiaPacific (excl. Japan) 29 Japan 34 Middle East & Africa 39 M&A and PE League Tables 44 Criteria & Contacts 79 mergermarket.com Mergermarket Global & Regional Global Overview 3 M&A Report 1H19 Global Overview Regional M&A Comparison North America USD 1,000.6bn +10.4% vs. 1H ‘18 Inbound USD 124.4bn +10.2% Outbound USD 183.9bn -10.6% PMB USD 174.1bn +129.3% Latin America USD 35.8bn -27% vs. 1H ’18 Inbound USD 24.0bn +19.5% Outbound USD 4.6bn +34.8% EMU USD 15.5bn +35.4% 21.7% 55.6% Europe USD 391.0bn -38.8% vs. 1H ‘18 1.0% Inbound USD 178.1bn -36.7% Outbound USD 125.0bn -11.5% PMB USD 133.5bn +3.9% MEA USD 113.5bn +222% vs. 1H ‘18 Inbound USD 32.2bn +41.2% Outbound USD 5.8bn -64.6% Ind. & Chem. USD 70.9bn +7.6% 6.3% 14.4% 2.0% APAC (ex. Japan) USD 241.0bn -36% vs. 1H ‘18 Inbound USD 40.4bn -28.5% Outbound USD 41.2bn -25.0% Ind. & Chem. USD 56.6bn -18.2% Japan USD 18.1bn +2.4% vs. 1H ’18 Inbound USD 3.9bn +114.3% Global M&A USD 1800.0bn -11.0% vs. 1H 2018 Outbound USD 42.6bn -58.7% Technology USD 6.3bn +2.0% Cross-border USD 594.7bn -22.0% vs. -

Bi-Weekly Financial Technology Sector Report

Financial Technology Sector Summary Week of June 19, 2017 1 DEAL DASHBOARD Financial Technology (3) (1) (3) $11.7 Bn | 1,179 Deals Industry Stock Market Performance $77.6 Bn | 683 Deals LTM Financing Volume Last Twelve Months LTM M&A Volume 160 Select Recent Financing Transactions Select Recent M&A Transactions Company Amount ($MM) 150 Target Acquirer EV ($MM) 140 $300.0 $1,381.0 130 $145.5 $304.0 120 $140.0 110 $89.0 100 $65.0 $33.0 90 $28.0 NA 80 6/16/16 8/1/16 9/14/16 10/28/16 12/13/16 1/26/17 3/13/17 4/26/17 6/9/17 $22.5 NA Payments Exchanges Financial Data, Content, Information Processors / $12.0 & Analytics Credit Bureaus NA Banking & Lending Online Broker Dealers Technology $12.0 NA Investment Services, Healthcare / Insurance Software, & Technology Technology S&P 500 (3) (3) Quarterly Financing Volume Quarterly M&A Volume $10 500 $30 219 250 205 196 188 $8 $8.9 400 $25 200 $24.9 299 298 316 $24.5 276 $20 $6 300 $20.8 $20.4 150 $15 $4 200 100 $10 $3.0 $2 $2.6 $2.6 100 $5 50 $0 0 $0 0 Q2 2016 Q3 2016 Q4 2016 Q1 2017 Q2 2016 Q3 2016 Q4 2016 Q1 2017 Financing Volume ($Bn) Financing Deal Count M&A Volume ($Bn) M&A Deal Count Notes: Source: Capital IQ, CB Insights and GCA FinTech Database. Market Data as of 6/16/17. 1) Refer to footnotes on page 5 for index composition.