Deal Drivers: EMEA FY 2020

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

DFA INVESTMENT DIMENSIONS GROUP INC Form NPORT-P Filed 2021-03-25

SECURITIES AND EXCHANGE COMMISSION FORM NPORT-P Filing Date: 2021-03-25 | Period of Report: 2021-01-31 SEC Accession No. 0001752724-21-062357 (HTML Version on secdatabase.com) FILER DFA INVESTMENT DIMENSIONS GROUP INC Mailing Address Business Address 6300 BEE CAVE ROAD 6300 BEE CAVE ROAD CIK:355437| IRS No.: 363129984 | State of Incorp.:MD | Fiscal Year End: 1031 BUILDING ONE BUILDING ONE Type: NPORT-P | Act: 40 | File No.: 811-03258 | Film No.: 21771544 AUSTIN TX 78746 AUSTIN TX 78746 (512) 306-7400 Copyright © 2021 www.secdatabase.com. All Rights Reserved. Please Consider the Environment Before Printing This Document DFA INVESTMENT DIMENSIONS GROUP INC. FORM N-Q REPORT January 31, 2021 (UNAUDITED) Table of Contents DEFINITIONS OF ABBREVIATIONS AND FOOTNOTES T.A. U.S. Core Equity 2 Portfolio Tax-Managed DFA International Value Portfolio T.A. World ex U.S. Core Equity Portfolio VA U.S. Targeted Value Portfolio VA U.S. Large Value Portfolio VA International Value Portfolio VA International Small Portfolio VA Short-Term Fixed Portfolio VA Global Bond Portfolio VIT Inflation-Protected Securities Portfolio VA Global Moderate Allocation Portfolio U.S. Large Cap Growth Portfolio U.S. Small Cap Growth Portfolio International Large Cap Growth Portfolio International Small Cap Growth Portfolio DFA Social Fixed Income Portfolio DFA Diversified Fixed Income Portfolio U.S. High Relative Profitability Portfolio International High Relative Profitability Portfolio VA Equity Allocation Portfolio DFA MN Municipal Bond Portfolio DFA California Municipal Real Return Portfolio DFA Global Core Plus Fixed Income Portfolio Emerging Markets Sustainability Core 1 Portfolio Emerging Markets Targeted Value Portfolio DFA Global Sustainability Fixed Income Portfolio DFA Oregon Municipal Bond Portfolio NOTES TO FINANCIAL STATEMENTS Organization Security Valuation Financial Instruments Federal Tax Cost Recently Issued Accounting Standards Other Subsequent Event Evaluations Table of Contents TABLE OF CONTENTS CONTINUED THE DFA INVESTMENT TRUST COMPANY SCHEDULES OF INVESTMENTS The U.S. -

Software Sector Summary Report

SOFTWARE SECTOR REPORT Q1 2019 GCA: A LEADING INDEPENDENT GLOBAL INVESTMENT BANK Global investment bank providing strategic M&A and capital markets advisory services to growth companies and market leaders LEEDS PARIS FRANKFURT MANCHESTER MUNICH ZURICH NAGOYA TOKYO LONDON SHANGHAI NEW YORK MILAN NEW DELHI OSAKA TEL AVIV FUKUOKA SAN FRANCISCO TAIPEI MUMBAI SINGAPORE HO CHI MINH CITY Global platform: Sector expertise: Exceptional cross- 21 offices in key Experienced team: Expansive coverage border capabilities: markets across Over 400 employees and deep Over a third of all America, Asia and across the globe specialization transactions Europe Broad spectrum Diversified Strong reputation of clients: business model: and track record: Leading Geographically High number of conglomerates, top balanced, synergistic repeat clients and private equity firms and complementary referrals and emerging high- focus areas growth companies 2 GCA operates as GCA in America and Asia, and GCA Altium in Europe GCA OVERVIEW The GCA Software Team US Team Paul DiNardo Daniel Avrutsky Rupert Sadler Josh Wepman Managing Director Managing Director Managing Director Managing Director Software HCM Software Software, Travel & Telematics Software & Digital Media [email protected] [email protected] [email protected] [email protected] James Orozco Clark Callander Chris Gough Kevin Walsh Managing Director Managing Director Managing Director Managing Director Financial Sponsors Technology Real Estate Tech Software & Digital Media [email protected] [email protected] -

The Global State of Sustainable Insurance Understanding and Integrating Environmental, Social and Governance Factors in Insurance

www.unep.org United Nations Environment Programme P.O. Box 30552 Nairobi, Kenya Tel.: ++254-(0)20-62 1234 Fax: ++254-(0)20-62 3927 E-mail: [email protected] United Nations Environment Programme Finance Initiative (UNEP FI) UNEP FI is a strategic public-private partnership between UNEP and the global financial sector. UNEP works with over 180 banks, insurers and investment firms, and a range of partner organisations, to understand the impacts of environmental, social The global and governance factors on financial performance and sustainable development. state of Through a comprehensive work programme encompassing research, sustainable training, events and regional activities, UNEP FI carries out its mission to identify, promote and insurance realise the adoption of best environmental and sustainability practice at all levels of financial Understanding and integrating ROGRAMME institution operations. P environmental, social and governance factors in insurance A report by the Insurance Working Group of the NVIRONMENT E United Nations Environment Programme Finance Initiative Based on the IWG’s pioneering 2009 global survey International Environment House on ESG factors and insurance underwriting 15 Chemin des Anémones ATIONS and product development 1219 Chatelaine, Geneva, Switzerland N Tel: (41) 22 917 8178 Fax: (41) 22 796 9240 [email protected] NITED www.unepfi.org U UNEP job n° DTI/1207/GE The global state of sustainable insurance Understanding and integrating environmental, social and governance factors in insurance A report by the Insurance Working Group of the United Nations Environment Programme Finance Initiative Based on the IWG’s pioneering 2009 global survey on ESG factors and insurance underwriting and product development October 2009 Disclaimer notice The information contained in the report is meant for informational purposes only and is subject to change without notice. -

Including League Tables of Financial Advisors

An Acuris Company Finding the opportunities in mergers and acquisitions Global & Regional M&A Report 2019 Including League Tables of Financial Advisors mergermarket.com An Acuris Company Content Overview 03 Global 04 Global Private Equity 09 Europe 14 US 19 Latin America 24 Asia Pacific (excl. Japan) 29 Japan 34 Middle East & Africa 39 M&A and PE League Tables 44 Criteria & Contacts 81 mergermarket.com Mergermarket Global & Regional Global Overview 3 M&A Report 2019 Global Overview Regional M&A Comparison North America USD 1.69tn 1.5% vs. 2018 Inbound USD 295.8bn 24.4% Outbound USD 335.3bn -2.9% PMB USD 264.4bn 2.2x Latin America USD 85.9bn 12.5% vs. 2018 Inbound USD 56.9bn 61.5% Outbound USD 8.9bn 46.9% EMU USD 30.6bn 37.4% 23.1% Europe USD 770.5bn -21.9% vs. 2018 50.8% 2.3% Inbound USD 316.5bn -30.3% Outbound USD 272.1bn 28.3% PMB USD 163.6bn 8.9% MEA USD 141.2bn 102% vs. 2018 Inbound USD 49.2bn 29% Outbound USD 22.3bn -15.3% Ind. & Chem. USD 72.5bn 5.2x 4.2% 17% 2.6% APAC (ex. Japan) USD 565.3bn -22.5% vs. 2018 Inbound USD 105.7bn -14.8% Outbound USD 98.9bn -24.5% Ind. & Chem. USD 111.9bn -5.3% Japan USD 75.4bn 59.5% vs. 2018 Inbound USD 12.4bn 88.7% Global M&A USD 3.33tn -6.9% vs. 2018 Outbound USD 98.8bn -43.6% Technology USD 21.5bn 2.8x Cross-border USD 1.27tn -6.2% vs. -

Software Sector Summary Report

Software COMPANYSector PRESENTATION Summary Week of October 2, 2017 1 DEAL DASHBOARD Software $35.9 Billion 470 $29.1 Billion 76 Financing Volume YTD (1)(2) Financing Transactions YTD (1)(2) M&A Volume YTD (3) M&A Transactions YTD (3) Select Financing Transactions Quarterly Financing Volume (1)(2) Quarterly M&A Volume (3) Select M&A Transactions (4) $Bn $Bn (61)% Company Amount ($MM) 43% Target Acquirer EV ($MM) $14 $50 $270 $12 $41 $3,903 $10 $11 $9 $6 $6 $24 $250 $6 $5 $1,125 $16 $15 $12 ( ) $12 $6 $5 $70 $834 ( ) Q3'15 Q4'15 Q1'16 Q2'16Q3'16 Q4'16 Q1'17 Q2'17 Q3'17 Q3'15 Q4'15 Q1'16 Q2'16 Q3'16 Q4'16 Q1'17 Q2'17 Q3'17 $45 Quarterly Financing Deal Count (1)(2) Quarterly M&A Deal Count (3) $614 36% $35 9% $531 156 160 154 127 118 123 103 111 $35 94 29 29 29 29 $382 24 24 26 21 $32 14 $344 $26 $270 Q3'15 Q4'15 Q1'16 Q2'16Q3'16 Q4'16 Q1'17 Q2'17 Q3'17 Q3'15 Q4'15 Q1'16 Q2'16 Q3'16 Q4'16 Q1'17 Q2'17 Q3'17 Last 12 Months Software Price Performance vs. S&P 500 (5) M&A EV/ NTM Rev. Over Time (6) 35.0% SPX IGV All Buyers Strategic Buyers PE Buyers 30.0% 30% 6 ` 5.3x Financing Activity by Quarter 4.7x 4.9x 5 4.5x 4.6x 25.0% 4.2x 4.3x 4.0x 4.1x 3.9x 3.9x 3.7x 20.0% 4 3.6x 3.1x 16% 2.7x 2.9x 2.9x 15.0% 3 2.5x 2.5x 2.5x 2.2x 10.0% 2 5.0% 1 0.0% 0 Sep-16 Oct-16 Nov-16 Dec-16 Jan-17 Feb-17 Mar-17 Apr-17 May-17 Jun-17 Jul-17 Aug-17 2011 2012 2013 2014 2015 2016 2017 (5.0%) (10.0%) Notes: Source: Capital IQ, PitchBook, and Dow Jones VentureSource. -

Scheme Document

THIS DOCUMENT IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION. PART II (EXPLANATORY STATEMENT) OF THIS DOCUMENT COMPRISES AN EXPLANATORY STATEMENT IN COMPLIANCE WITH SECTION 897 OF THE COMPANIES ACT 2006. This Document contains a proposal which, if implemented, will result in the cancellation of the listing of RSA Shares on the Official List and of trading of RSA Shares on the London Stock Exchange. If you are in any doubt as to the contents of this Document or the action you should take, you are recommended to seek your own financial advice immediately from your stockbroker, bank manager, accountant or other independent financial adviser authorised under the Financial Services and Markets Act 2000, if you are in the United Kingdom, or from another appropriately authorised independent financial adviser if you are taking advice in a territory outside the United Kingdom. If you sell or have sold or otherwise transferred all of your RSA Shares or RSA ADSs, please send this Document together with the accompanying documents (other than documents or forms personal to you) at once to the purchaser or transferee, or to the stockbroker, bank or other agent through whom the sale or transfer was effected, for transmission to the purchaser or transferee. However, such documents should not be forwarded or transmitted in or into or from any jurisdiction in which such act would constitute a violation of the relevant laws of such jurisdiction. If you sell or have sold or otherwise transferred only part of your holding of RSA Shares or RSA ADSs, you should retain these documents and contact the bank, stockbroker or other agent through whom the sale or transfer was effected. -

Including League Tables of Financial Advisors

An Acuris Company Finding the opportunities in mergers and acquisitions Global & Regional M&A Report 2019 Including League Tables of Financial Advisors mergermarket.com An Acuris Company Content Overview 03 Global 04 Global Private Equity 09 Europe 14 US 19 Latin America 24 Asia Pacific (excl. Japan) 29 Japan 34 Middle East & Africa 39 M&A and PE League Tables 44 Criteria & Contacts 81 mergermarket.com Mergermarket Global & Regional Global Overview 3 M&A Report 2019 Global Overview Regional M&A Comparison North America USD 1.69tn 1.5% vs. 2018 Inbound USD 295.8bn 24.4% Outbound USD 335.3bn -2.9% PMB USD 264.4bn 2.2x Latin America USD 85.9bn 12.5% vs. 2018 Inbound USD 56.9bn 61.5% Outbound USD 8.9bn 46.9% EMU USD 30.6bn 37.4% 23.1% Europe USD 770.5bn -21.9% vs. 2018 50.8% 2.3% Inbound USD 316.5bn -30.3% Outbound USD 272.1bn 28.3% PMB USD 163.6bn 8.9% MEA USD 141.2bn 102% vs. 2018 Inbound USD 49.2bn 29% Outbound USD 22.3bn -15.3% Ind. & Chem. USD 72.5bn 5.2x 4.2% 17% 2.6% APAC (ex. Japan) USD 565.3bn -22.5% vs. 2018 Inbound USD 105.7bn -14.8% Outbound USD 98.9bn -24.5% Ind. & Chem. USD 111.9bn -5.3% Japan USD 75.4bn 59.5% vs. 2018 Inbound USD 12.4bn 88.7% Global M&A USD 3.33tn -6.9% vs. 2018 Outbound USD 98.8bn -43.6% Technology USD 21.5bn 2.8x Cross-border USD 1.27tn -6.2% vs. -

Canada Rothschild/Soros Clan Lost Huge Investment in China's Ouster of Bo Xilai More Below Bilderber Timeline, Rothsch / China

NewsFollowUp.com Obama / CIA Franklin Scandal Omaha pictorial Index sitemap home Canada North American Union? ... Secret agenda is to dissolve the United States of America into the North Your browser does not support inline frames or American Union. ... is currently configured not to display inline controlled by frames. corporations ... no accountability. go to Immigration page WMR: Bilderberg Rothschild/Soros clan lost huge Timeline, Rothschild Canada investment in / China Your browser does not China's ouster of support inline frames or is currently configured not to Bo Xilai more display inline frames. below America for sale, How does this tie into NAU? North American Union Politics Resources related topics related topics related topics Environment Economics De-regulation Indigenous Rights Immigration Pharmaceuticals Labor Latin America Taxes War Global Collectivism PROGRESSIVE REFERENCE CONSERVATIVE* Americas American Society of International Law, see also Accenture formerly Andersen Consulting, see Amnesty International ECOSOC on North American Union. Enron, Kenneth Lay, Jeffrey Skilling, Bush from Canadians.org Deep Integration of U.S. and Center for North American Studies, American Accuracy in Media portrays NAU as a left-wing Canadian economies regulation, standards University, Professor Robert Pastor, said to be conspiracy ..."AIM has previously documented governing health, food safety, father of NAU, and his book "Towards a North that Pastor's campaign for a North American wages. Harmonization process a demand -

Distribution Strategies in Insurance Understanding the Customer View DISTRIBUTION STRATEGIES in INSURANCE

Distribution Strategies in Insurance Understanding the Customer View DISTRIBUTION STRATEGIES IN INSURANCE Executive Insurers are, by their very nature, cautious. As a result, they will often focus more on the risks of summary new developments as much as the potential opportunities. The evolution of the insurance as likely to use instant messaging or sales process however, and the web chats as they are face-to-face widespread adoption of digital meetings (5%) when communicating channels in every walk of life, has with their insurer. made insurers sit up and take note. Most now realise that they must The survey cautions against making interact with their customers – at simplistic assumptions, however. least to some extent – whenever, Respondents most comfortable with however and through whichever technology were not the youngest channel their customer desires. We group, as you might expect, but have commissioned this research those aged 35-44. In fact, surprisingly, to better understand consumers’ the youngest respondents were most expectations and gauge how well likely to interact face-to-face than any insurers currently measure up. other age group. The survey, based on the responses A key aspect of the findings is clear: of more than 2,000 working age insurers need both compelling adults in the UK, highlights that traditional and digital channels. It consumers are becoming more savvy is on the latter, however, that they when purchasing their insurance. seem most at risk of falling short. The For example, consumers are almost research found that more than one in as likely to prioritise the ease of three consumers find buying or obtaining a quote (36%) as much as renewing a policy online “very the brand of the insurer (42%). -

2019 Insurance Fact Book

2019 Insurance Fact Book TO THE READER Imagine a world without insurance. Some might say, “So what?” or “Yes to that!” when reading the sentence above. And that’s understandable, given that often the best experience one can have with insurance is not to receive the benefits of the product at all, after a disaster or other loss. And others—who already have some understanding or even appreciation for insurance—might say it provides protection against financial aspects of a premature death, injury, loss of property, loss of earning power, legal liability or other unexpected expenses. All that is true. We are the financial first responders. But there is so much more. Insurance drives economic growth. It provides stability against risks. It encourages resilience. Recent disasters have demonstrated the vital role the industry plays in recovery—and that without insurance, the impact on individuals, businesses and communities can be devastating. As insurers, we know that even with all that we protect now, the coverage gap is still too big. We want to close that gap. That desire is reflected in changes to this year’s Insurance Information Institute (I.I.I.)Insurance Fact Book. We have added new information on coastal storm surge risk and hail as well as reinsurance and the growing problem of marijuana and impaired driving. We have updated the section on litigiousness to include tort costs and compensation by state, and assignment of benefits litigation, a growing problem in Florida. As always, the book provides valuable information on: • World and U.S. catastrophes • Property/casualty and life/health insurance results and investments • Personal expenditures on auto and homeowners insurance • Major types of insurance losses, including vehicle accidents, homeowners claims, crime and workplace accidents • State auto insurance laws The I.I.I. -

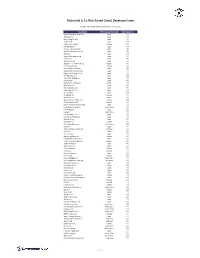

Rothschild & Co Risk-Based Global Developed Index

Rothschild & Co Risk-Based Global Developed Index Indicative Index Weight Data as of January 31, 2020 on close Constituent Exchange Country Index Weight (%) Nippon Telegraph & Telephone C Japan 1.11 Softbank Corp Japan 1.10 Nitori Holdings Co Ltd Japan 0.75 Toshiba Corp Japan 0.67 Kirkland Lake Gold Ltd Canada 0.61 NTT DOCOMO Inc Japan 0.58 Mizuho Financial Group Inc Japan 0.54 Takeda Pharmaceutical Co Ltd Japan 0.50 KDDI Corp Japan 0.49 Japan Post Holdings Co Ltd Japan 0.48 Subaru Corp Japan 0.48 Sekisui House Ltd Japan 0.45 Singapore Telecommunications L Singapore 0.45 Franco-Nevada Corp Canada 0.43 Oriental Land Co Ltd/Japan Japan 0.43 Chugai Pharmaceutical Co Ltd Japan 0.40 Nippon Paint Holdings Co Ltd Japan 0.39 Fast Retailing Co Ltd Japan 0.38 Tokio Marine Holdings Inc Japan 0.38 ITOCHU Corp Japan 0.38 Bandai Namco Holdings Inc Japan 0.37 Bridgestone Corp Japan 0.36 MEIJI Holdings Co Ltd Japan 0.35 Japan Airlines Co Ltd Japan 0.34 Unicharm Corp Japan 0.33 Aroundtown SA Germany 0.33 Ajinomoto Co Inc Japan 0.33 Algonquin Power & Utilities Co Canada 0.32 Deutsche Wohnen SE Germany 0.32 MS&AD Insurance Group Holdings Japan 0.32 Lamb Weston Holdings Inc United States 0.32 ANA Holdings Inc Japan 0.32 Evergy Inc United States 0.32 Kirin Holdings Co Ltd Japan 0.32 Asahi Group Holdings Ltd Japan 0.32 Shiseido Co Ltd Japan 0.32 Wesfarmers Ltd Australia 0.32 Cboe Global Markets Inc United States 0.32 Canon Inc Japan 0.31 Jardine Matheson Holdings Ltd Singapore 0.31 Kao Corp Japan 0.31 Secom Co Ltd Japan 0.31 Agnico Eagle Mines Ltd Canada 0.31 -

Appendix D - Securities Held by Funds October 18, 2017 Annual Report of Activities Pursuant to Act 44 of 2010 October 18, 2017

Report of Activities Pursuant to Act 44 of 2010 Appendix D - Securities Held by Funds October 18, 2017 Annual Report of Activities Pursuant to Act 44 of 2010 October 18, 2017 Appendix D: Securities Held by Funds The Four Funds hold thousands of publicly and privately traded securities. Act 44 directs the Four Funds to publish “a list of all publicly traded securities held by the public fund.” For consistency in presenting the data, a list of all holdings of the Four Funds is obtained from Pennsylvania Treasury Department. The list includes privately held securities. Some privately held securities lacked certain data fields to facilitate removal from the list. To avoid incomplete removal of privately held securities or erroneous removal of publicly traded securities from the list, the Four Funds have chosen to report all publicly and privately traded securities. The list below presents the securities held by the Four Funds as of June 30, 2017. 1345 AVENUE OF THE A 1 A3 144A AAREAL BANK AG ABRY MEZZANINE PARTNERS LP 1721 N FRONT STREET HOLDINGS AARON'S INC ABRY PARTNERS V LP 1-800-FLOWERS.COM INC AASET 2017-1 TRUST 1A C 144A ABRY PARTNERS VI L P 198 INVERNESS DRIVE WEST ABACUS PROPERTY GROUP ABRY PARTNERS VII L P 1MDB GLOBAL INVESTMENTS L ABAXIS INC ABRY PARTNERS VIII LP REGS ABB CONCISE 6/16 TL ABRY SENIOR EQUITY II LP 1ST SOURCE CORP ABB LTD ABS CAPITAL PARTNERS II LP 200 INVERNESS DRIVE WEST ABBOTT LABORATORIES ABS CAPITAL PARTNERS IV LP 21ST CENTURY FOX AMERICA INC ABBOTT LABORATORIES ABS CAPITAL PARTNERS V LP 21ST CENTURY ONCOLOGY 4/15