Annual Report 2014 03 Code of Conduct

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Fall 2015 2014

VolumeVolume 18 17/ Number / Number 1 >>>> FALL FALL 2015 2014 In this issue: NESA Professional Development Events 2015-2016 Kathmandu Earthquake Relief School news from around the NESA region The New NESA Middle School Network The History of AERO and much more. 2 WELCOME From the NESA Board President: TO THE On behalf of the NESA Board of Trustees, I welcome you to a new school year of collaborative learning opportunities 2015-2016 with NESA. We look forward to meeting you at one of our conferences or institutes scheduled this year in Abu Dhabi, Dubai, Muscat, and Bangkok. Under the exceptional leader- ship of Executive Director David Chojnacki and his staff at SCHOOL YEAR. the NESA Center, we are providing unique opportunities for Dear Friends and Colleagues Across the NESA Region, professional development in support of sustainable and sys- temic school improvement. We encourage board members, “From Cairo to Kathmandu”: that’s a phrase we use when administrators, teachers, and support staff to join us. writing to speakers about NESA. And although our bounda- ries are actually Libya and Greece in the west to Bangla- This year, the NESA Board is focusing its efforts on an impor- desh, Sri Lanka and India in the east, the phrase does il- tant leadership transition. After 18 years of serving NESA, lustrate the richness and the challenges of our region. It’s a David Chojnacki will be resigning as Executive Director ef- wonderful part of the world. .and we welcome you to it (or fective July 2017. We in NESA realize how fortunate we back to it!) for another year of teaching and learning. -

Full Name Jobtitle Institution Country Kamal Abdel-‐Nour President Ibn

Full Name JobTitle Institution Country Kamal Abdel-Nour President Ibn Khuldoon National School Bahrain Abdul Nasser Business/Finance Universal American School UAE Browning Curriculum/P.D. Al Bayan Bilingual School Kuwait Saleh Abdullah Salem Al MekhleF Board Member/Trustee Kuwait Bilingual School Kuwait Mohammed Abdulmajeed Board Member/Trustee The American International School oF Muscat Oman Sana Abiad Other International Schools Group Saudi Arabia Roula Raidan AbiFaker Teacher Leader/Dept.Head American School oF Dubai UAE Carlos Aboumrad Other Bahrain Bayan School Bahrain Jeries Abu Al Etham Other Friends School Palestine Karim Abu Haydar Principal American Community School Lebanon Mohamed Hafez Mousa Abu-Lebdeh Teacher Leader/Dept.Head Dhahran Ahliyya Schools Saudi Arabia Baria Abu Zein Principal Al Najah Private School UAE Walid Abushakra Head oF School/Institution Educational Services Overseas Limited (ESOL) Egypt Tammam Abushakra Other Educational Services Overseas Limited (ESOL) Egypt Bassam Abushakra Head oF School/Institution Educational Services Overseas Limited (ESOL) Egypt Mr. JohnEric Advento Principal American School oF Dubai UAE Dana K. Adwan Business/Finance King's Academy Jordan Maisae AFFour ES Principal Ibn Khuldoon National School Bahrain Fazna Ahmed Board Member/Trustee The Overseas School oF Colombo Sri Lanka Sajeda Akbarally Board Member/Trustee The Overseas School oF Colombo Sri Lanka Ala-din Al-afghani Principal Kuwait bilingual school kuwait Lana Al-Aghbar Principal American School oF Doha Qatar Maryam Ahmed Naser Al Ali Other Abu Dhabi Education Council UAE Rashed Al Doulab Other International Schools Group Saudi Arabia Dahi Laili Al Fadhli ChieF Executive OFFicer Sama Educational Co KSCC-Kuwait Kuwait Feda Al Khatib Board Member/Trustee Advanced Learning Schools Saudi Arabia Amal Mustafa Al-Minawai Principal American Baccalaureate School Kuwait Alaa Mohammed Al Mumtan Business/Finance Dhahran Ahliyya Schools Saudi Rabia Maha Al Romaihi Asst. -

ED318701.Pdf

DOCUMENT RESUME ED 318 70]. SP 032 197 AUTHOR Bernardi, Ray D. TITLE Teaching in Other Countries. An Overview of the Opportunities for Teachers from the U.S.A. PUB DATE 2 Dec 89 NOTE 50p.; Paper presented at the Annual Meeting of the American Vocational Association (Orlando, FL, December 1-5, 1989). Printed on colored stock, therefore some lists may not reproduce clearly. PUB TYPE Speeches/Conference Papers (150)-- Reports - Descriptive (141) EDRS PRICE MF01/PCO2 Plus Postage. DESCRIPTORS *Cultural Differences; *Culture Conflict; Foreign Countries; *Overseas Employment; *Teacher Exchange Programs; *Teaching (Occupation); Teaching Conditions; Vocational Adjustment ABSTRACT Suggestions are made for teachers considering teaching abroad. The following topics are covered:(1) problems encountered In working in a foreign environment, e.g., culture shock; (2) general considerations in making the decision to teach overseas; (3) steps to follow when seeking an overseas position;(4) overseas employment opportunities with the Department of Defense Dependents Schools;(5) overseas placement services for educators; (6) The University of Maryland Overseas Program;(7) international jobs--teaching; (8) an alphabetical list of 225 Overseas American Community Schools; (9) answers to questions regarding recruitment for international schools; and (10) the Fulbright Teacher Exchange Program. (JD) *********************************************************************** Reproductions supplied by EDRS are the best that can be made from the original document. *********************************************************************** '"""e""""""'"'"'""""'"""'"W""'"'""eloW.I::M.Inxwn"."..%NI1rlswmlndW"""W"...""''"'"":'""w".'"'"""WasIWsll'"'""'"".Ow1000 MINIFIffilowympomn. .0. IN ....romemommag .111 TEACHING WY M/6 =wsn.O OTHER 0.0.11.1~0 Irenworreffir e.merwrame 610111.0. 11........ 1.101116 ....... .11......... ........INIMOIMPole ....... 40... wirdesearer 11 7'.":"=....... COUNTRIES 01.....0...10.4. -

This Is the New Order of 2011

This is the New order of 2011. 1 Education Bay [EBAY], this school was constructed around 15 years back and now has finally reached the top positions.It follows the O/A level system , and is known for its higher education studies and pleasing , appropriate environment. If you need more info regardint this go here http://www.facebook.com/group.php?gid=144773925564460&ref=ts 2.British overseas 3. Karachi Grammar School (KGS) 4. bayview academy(bva) 5Centre for Advanced Studies (CAS) School 6. Lyceum School 7. Frobel 8. Beaconhouse School System 9 bayview high school 10. The International School Read more: http://wiki.answers.com/Q/What_are_the_top_ten_schools_in_karachi#ixzz1HovjslRj According to my survey in the field of montessori education the one's providing quality education are MCDC CLIFTON MONTESSORI Aa Ba Ca Da Montessori MTLS AND FEW MORE When you say MCDC is it Mariam's Montessori Development Centre or Montessori Child Development Centre? http://navika.wordpress.com/2010/05/17/my-shocking-visits-to-schools/ Note: There are comments associated with this question. See the discussion page to add to the conversation. Read more: http://wiki.answers.com/Q/Top_ten_montessori_schools_in_karachi#ixzz1Hox3fRiO Read more: http://wiki.answers.com/Q/Top_ten_montessori_schools_in_karachi#ixzz1HowqHOPR Lahore 1)Atchison College 2)Divisional Public School 3)LGS 4)LACAS 5)SICAS5 6)BeachonHouse 7)Cresent Model School 8)ICAS 9)International School of Choiefat 10)Cathedral School Anthony's Read more: http://wiki.answers.com/Q/Which_are_top_ten_schools_in_lahore#ixzz1HoxMa6yt O Levels 1.b.v.s 2.st patrick 3.st paul 4.habib public ------------------------------------------------ 1.Beaconhouse School system 2.Karachi Grammar School 3.Foundation Public School 4.The City school Read more: http://wiki.answers.com/Q/Best_olevels_school_in_karachi#ixzz1Hp2EDwuM TOP SIX ARE: 1. -

School Programme Our Story

PBS for AKUH's 2019 School Programme Our Story In collaboration with the Aga Khan University Hospital (AKUH) Children's Hospital Service Line, the Patients' Behbud Society for AKUH designed a specific programme to involve children in alleviating the suffering of other children. The 'Kids for Kids' Concept came under the broad remit of the School Programme which was specifically designed to give students from across the country, an opportunity to be part of a worthy social cause, and collect funds for those children whose treatment at AKUH's Paediatric ward was critical yet outside their parents' financial capabilities. Through these students, the School Programme managed to reach their households with information about PBS for AKUH and its impact on patients from low-income backgrounds. This experience helps inculcate the concept of philanthropy in children from a very young age, allowing them to witness the impact of their generosity on those who are not as privileged. Our Reach 25 39 3 schools branches cities 35,000 students 30,000 households 100% participation from St. Joseph's Convent (Cambridge Section) - more than any other school Our Partners Our transformative impact and growing outreach is all thanks to our generous and collaborative educational partners, who allowed us not only to raise funds for an extremely important social cause, but also allowed us to spread awareness about our work through their networks. We are extremely grateful to all of them for their initiative and support. Avicenna Indus Academy SICAS Adler College Institute of Business Management St. Joseph's Convent School Aitchison College Karachi American School SZABIST Bahria University Lady Bird Grammar School The CAS School Dawood Public School L'ecole School The City School Habib Girls School Meritorious School The Educators Happy Home School Reads College The Smart School Ilmesters Academy Sacred Heart School White House Grammar School In Focus All our partners are equally important to us. -

The American Sponsored Overseas School Headship: Two Decades of Change and the Road Ahead Theron J

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by Lehigh University: Lehigh Preserve Lehigh University Lehigh Preserve Theses and Dissertations 2012 The American sponsored overseas school headship: Two decades of change and the road ahead Theron J. Mott Lehigh University Follow this and additional works at: http://preserve.lehigh.edu/etd Recommended Citation Mott, Theron J., "The American sponsored overseas school headship: Two decades of change and the road ahead" (2012). Theses and Dissertations. Paper 1341. This Dissertation is brought to you for free and open access by Lehigh Preserve. It has been accepted for inclusion in Theses and Dissertations by an authorized administrator of Lehigh Preserve. For more information, please contact [email protected]. The American Sponsored Overseas School Headship: Two Decades of Change and the Road Ahead By Theron J. Mott Presented to the Graduate and Research Committee of Lehigh University in Candidacy for the Degree of Doctor of Education in Educational Leadership Lehigh University December 2011 Copyright by Theron J. Mott December 2011 ii DISSERTATION SIGNATURE SHEET Approved and recommended for acceptance as a dissertation in partial fulfillment of the requirements for the degree of Doctor of Education. _______________________ Date _______________________ Accepted Date Dr. Roland K. Yoshida Professor of Educational Leadership Lehigh University Chair Committee Members: Dr. Daphne Hobson Executive Director, Office of Int’l Programs Lehigh University Dr. George White Professor of Educational Leadership Lehigh University Dr. Harlan Lyso Commission Chairperson Western Association of Schools and Colleges iii Acknowledgements A dissertation is much less about intelligence than it is about perseverance, and my perseverance was made possible by a host of supporters. -

List of Bronze Medal Winners

LIST OF BRONZE MEDAL WINNERS FIRST POSITION IN INSTITUTION S. NO. ROLL NO. STUDENT NAME FATHER NAME CLASS INSTITUTION CITY/DISTRICT AAIMAH AHMED 1 18-47-20594-1-002-E IRFAN AHMED SUALEH 1 THE CITY NURSERY JHANG SUALEH 2 18-42-00739-1-014-E AAMINA HABIB HABIB QASIM 1 THE CITY SCHOOL JUNIOR LAHORE AL A'LA SCHOOL OF 3 18-42-20387-1-003-E AAMNA FAISAL FAISAL RIAZ 1 CONTEMPORARY AND LAHORE ISLAMIC STUDIES AANIYA AAMER 4 18-992-20490-1-003-E AAMER BHATTI 1 THE CITY NURSERY ABBOTTABAD BHATTI 5 18-051-00241-1-004-E AAYAN MASROOR TIPU MASROOR 1 ROOTS MILLENNIUM SCHOOL ISLAMABAD 6 18-544-20506-1-001-E ABBIHA MUNTAHA NISAR AHMAD 1 WINNINGTON SCHOOL JHELUM BLOOMFIELD HALL PREPS 7 18-61-00831-1-001-E ABDUL AHAD GARDEZI AHMAD NAWAZ GARDEZI 1 MULTAN AND JUNIOR SCHOOL ARMY PUBLIC SCHOOL 8 18-52-00546-1-069-E ABDUL AZIZ MUHAMMAD QASIM 1 SIALKOT JUNIOR CAMPUS 9 18-55-00222-1-011-E ABDUL AZIZ HAROON MUHAMMAD HAROON 1 THE NOOR SCHOOL GUJRANWALA THE CITY SCHOOL LIAQUAT 10 18-022-00518-1-001-E ABDUL HADI NASIR KHAN 1 HYDERABAD CAMPUS ALLIED SCHOOL 11 18-62-00468-1-009-E ABDUL HADI MUHAMMAD SHAKIR 1 BAHAWALPUR PRIMARY BAHAWALPUR CAMPUS ARMY PUBLIC SCHOOL 12 18-62-20346-1-008-E ABDUL KABEER HADI KHURRAM SHAHZAD 1 BAHAWALPUR MIDDLE BAHAWALPUR CANTT ABDUL MOIZ BIN MALIK RASHID THE CITY SCHOOL ATTOCK 13 18-57-00554-1-003-E 1 ATTOCK RASHID MEHMOOD CAMPUS AIR FOUNDATION SCHOOL 14 18-51-00538-1-004-E ABDUL RAFAY ABDUL HANAN ABBASSI 1 RAWALPINDI SYSTEM HARLEY CAMPUS AGA KHAN SCHOOL 15 18-021-00714-1-002-E ABDUL REHMAN MUHAMMAD IQBAL 1 KARACHI KHARADHAR ALLIED SCHOOL -

Academic Profile 2018–2019

Community The 2018-2019 enrollment is 250 (PS: 13; K-grade 5: 92; grades 6-8: 62; and grades 9-12: 83). Of the total, 75 are U.S. citizens, 80 are host-country nationals, and 95 are third-country nationals, representing 26 countries. Of the U.S. enrollment, 55 are dependents of U.S. government direct-hire or contract employees. For 2018-2019 there are 36 fully certified faculty members, including 26 U.S. citizens, 5 Canadian citizens, 2 French citizens, 2 Australian citizens, and 1 UK citizen. School Calendar and Schedule The school year consists of 180 days which are divided into two semesters. The first semester spans mid-August to mid-December and the second semester runs from January to mid-June. We offer Academic Profile eight periods on a rotation hybrid block schedule. Curriculum 2018–2019 Lincoln School offers an American curriculum with an international perspective. The the program is college preparatory with a wide Established in 1954, Lincoln School is an independent, selection of electives and extracurricular activities leading to an co-educational day school, providing an enriched North American high school diploma. Lincoln School provides student American college-preparatory curriculum for students services to English for Speakers of Other Languages (ESOL) and pre-school & pre-kindergarten to grade 12. Lincoln those students who need learning support. Students have the School has a long-established tradition of student- opportunity to take courses in the areas of health and physical centered education founded in current best practices education, music, art, and modern languages in Spanish and French. -

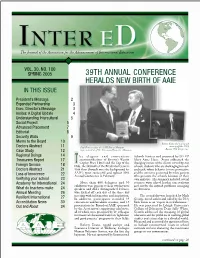

39TH ANNUAL CONFERENCE HERALDS NEW BIRTH of AAIE in THIS ISSUE President’S Message 2 Expanded Partnership 3 Exec

The Journal of the Association for the Advancement of International Education VOL. 30, NO. 100 SPRING 2005 39TH ANNUAL CONFERENCE HERALDS NEW BIRTH OF AAIE IN THIS ISSUE President’s Message 2 Expanded Partnership 3 Exec. Director’s Message 3 Insites: A Digital Update 4 Understanding Intercultural 5 Social Project 5 Advanced Placement 7 Editorial 8 Security Walls 9 Memo to the Board 10 Robert Evans did a great job Doctors Abstract 11 Paul Poore receives the AAIE Ernest Mannino starting off the 2005 Case Study 12 Superintendent of the Year award from Dr. Mannino. Boston 39th Conference. Regional Doings 14 he elegant and convenient Schools Services and presented by ISS VP Treasurers Report 17 accommodations of Boston’s Westin Mary Anne Haas. Evans addressed the T Copley Place Hotel and the Top of the changing nature of the clients served by our Foreign Service 18 Hub, the Skywalk of the Prudential Center’s schools, students who are challenging to reach Doctors Abstract 21 50th floor Skywalk were the background for and teach, whose behavior is more provocative AAIE’s most successful and upbeat 39th and the concerns presented by more parents Loss of Innocence 22 Annual Conference in February. who pressure the schools because of their Verifying your school 23 own anxieties. His summary included several Academy for International 24 More than 400 delegates and 50 concrete ways school leaders can confront exhibitors were present to hear two keynote and resolve the myriad problems emerging What do teachers make 24 speakers and AIE’s distinguished lecturer, in education. Annual Meeting 26 who kicked off each day of the three-day meeting with information and inspiration. -

First Name Lastname Fullname Institution 1 Liz Abbasi Elizabeth Abbasi Int'l School of Islamabad 2 Micheli

# First Name LastName FullName Institution 1 Liz Abbasi Elizabeth Abbasi Int'l School of Islamabad 2 Micheline Abboud Micheline Abboud International Schools Group 3 Lara Abdallah Lara Abdallah AMSI Schools 4 Mamoon Abdelqader Mamoon Mohammad Turki Abdelqader Dhahran Ahliyya Schools 5 Roula Abifaker Roula Raidan Abifaker American School of Dubai 6 Alissar Abou Jaoude Alissar Abou Jaoude International College 7 Sarah Aboul Hosn Sarah Moughrabi Aboul Hosn American school of Dubai 8 Suad Abu Harb Suad Abu Harb Dubai National School 9 Mohamad Abu Lebdeh Mohamad Hafez Mousa Abu-Lebdeh Dhahran Ahliyya Schools 10 Sakina Ahmad Sakina Ahmad Collegiate American School 11 Roula Akkaoui Roula Akkaoui American School of Dubai 12 Reem Albakary Reem Albakary American School of Dubai 13 Manal AlFarkh Manal Al Farkh American School of Dubai 14 Aysha Alghool Aysha Alghool Riffa Views International School 15 Fatima Sarah Allibahai Fatima Sarah Allibahai Qatar Academy Al Khor 16 Abdul Razzak Almatan Abdul Razzak M. Nassar Almatan Dhahran Ahliyya Schools 17 Saarah Alsunaid Saarah Abdulmuhsen A Alsunaid Dhahran Ahliyya Schools 18 Faten Alzohaily Faten Alzohaily Al-Mizhar American Academy 19 Suzanne Ames Suzanne Ames Riffa Views International School 20 Robert Andre Robert Andre International Schools Group 21 Rima Aoun Rima Aoun International College 22 Hilda Ashkar Hilda Ashkar The American International School of Muscat 23 Nermeen Ata Nermeen Saleh Ata Al Maarifa International School 24 Abeera Atique Abeera Atique International Schools Group 25 Salwa Bachir -

Academic Profile 2020–2021

Community The enrollment is 250 (PS: 16; K-grade 5: 93; grades 6-8: 60; and grades 9-12: 81). Of the total, 83 are U.S. citizens, 77 are host- country nationals, and 90 are third-country nationals, representing 25 countries. Of the U.S. enrollment, 59 are dependents of U.S. government direct-hire or contract employees. For 2019-2020 there are 40 fully certified faculty members, including 29 U.S. citizens, 6 Canadian citizens, 2 French citizens, 2 Australian citizens, and 1 UK citizen. School Calendar and Schedule The school year consists of 180 days which are divided into two semesters. The first semester spans mid-August to mid-December and the second semester runs from January to mid-June. We offer Academic Profile eight periods on a rotation hybrid block schedule. Curriculum 2020–2021 Lincoln School offers an American curriculum with an international perspective. The program is college preparatory with a wide Established in 1954, Lincoln School is an independent, selection of electives and extracurricular activities leading to an co-educational day school, providing an enriched North American high school diploma. Lincoln School provides student American college-preparatory curriculum for students services to English for Speakers of Other Languages (ESOL) and pre-school & pre-kindergarten to grade 12. Lincoln those students who need learning support. Students have the School has a long-established tradition of student- opportunity to take courses in the areas of health and physical education, music, art, and modern languages in Spanish and French. centered education founded in current best practices and offers small class sizes, outstanding international Lincoln provides a dynamic, engaging project-based learning faculty, support staff and a community-oriented program called Innovation Lab based on the inquiry that is learning environment that fosters the well-being of the responsive to the passions of our students. -

2017 SAISA Track & Field Meet

Overseas School of Colombo Hy-Tek's MEET MANAGER 9:12 AM 4/21/2017 Page 1 2017 SAISA Track & Field Meet - 4/20/2017 to 4/22/2017 Colombo, Sri Lanka Results Girls 10-12 100 Meter Dash ====================================================================================== Name Age Team Seed Prelims H# Alternate ====================================================================================== Preliminaries 1 Sydney Henry 12 Geckos 15.80 15.00q 4 2 Shandaneh Penker 11 American School 15.10q 1 3 Shanaya Panjwani 12 Eagles 13.30 15.40q 4 4 Melanie Frankenberger 11 Tigers 15.90 J15.40q 4 5 Pari Pandey 12 Eagles 14.40 J15.40q 3 6 Niamh Powell 12 Lincoln School 15.32 15.50q 1 7 Savanna Woods 12 Eagles 14.50 15.90 2 8 Stephie Turner 10 Geckos 16.40 16.00 1 9 Hayaa Tabba 12 Knights 15.68 16.10 2 9 Aya Al Mazrouai 12 Eagles 15.72 16.10 3 11 Arfa Edhi 11 Knights 15.30 16.20 1 12 Sarah Levitt 11 Scorpions 16.35 16.30 2 12 Ammaarah Rassool 11 Tigers 17.27 16.30 1 14 Chelsea Karunaratne 10 Geckos 16.00 16.60 3 15 Mariam Jatoi 12 Knights 16.90 2 16 Anya Reddy 10 American School 17.29 17.60 2 17 Kshamya Khadka 11 Tigers 18.07 18.10 4 18 Lujain Attiga 11 Scorpions 17.89 18.20 3 19 Dhivya Sasha 11 American School 19.25 19.20 4 20 Eman Naufil 11 Buffalos 19.55 19.70 3 Girls 10-12 100 Meter Dash ========================================================================================== Name Age Team Prelims Finals Points Alternate ========================================================================================== Finals 1 Shandaneh Penker 11 American