Amazon's Transformative Endeavor by Orchestrating Techno-Financin

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

1 of 6 C O R P O R a T E Amazon/Acquisitions the Chart

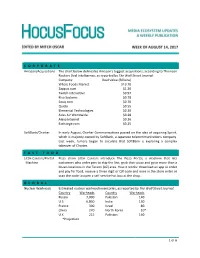

CORPORATE Amazon/Acquisitions The chart below delineates Amazon’s biggest acquisitions, according to Thomson Reuters Deal Intelligence, as reported by The Wall Street Journal: Company Deal Value (Billions) Whole Foods MarKet $13.70 Zappos.com $1.20 Twitch Interactive $0.97 Kiva Systems $0.78 Souq.com $0.70 Quidsi $0.55 Elemental Technologies $0.30 Atlas Air Worldwide $0.28 Alexa Internet $0.26 Exchange.com $0.25 SoftBanK/Charter In early August, Charter Communications passed on the idea of acquiring Sprint, which is majority owned by SoftBanK, a Japanese telecommunications company. Last week, rumors began to circulate that SoftBank is exploring a complex taKeover of Charter. FAST FOOD Little Caesars/Portal Pizza chain Little Caesars introduce The Pizza Portal, a machine that lets Machine customers who order pies to skip the line, grab their pizza and go in more than a dozen locations in the Tucson (AZ) area. How it worKs: download an app to order and pay for food, receive a three digit or QR code and once in the store enter or scan the code to open a self-service hot box at the shop. GLOBAL Nuclear Warheads Estimated nuclear warhead inventories, as reported by The Wall Street Journal: Country Warheads Country Warheads Russia 7,000 Pakistan 140 U.S. 6,800 India 130 France 300 Israel 80 China 270 North Korea 10* U.K. 215 Pakistan 140 *Projection 1 of 6 MOVIES TicKet Sales According to Nielsen, North American box office ticKet sales are down 2.9% even with ticKet prices higher than the prior year – maKing up for some of the diminished theater attendance. -

The Internet and Drug Markets

INSIGHTS EN ISSN THE INTERNET AND DRUG MARKETS 2314-9264 The internet and drug markets 21 The internet and drug markets EMCDDA project group Jane Mounteney, Alessandra Bo and Alberto Oteo 21 Legal notice This publication of the European Monitoring Centre for Drugs and Drug Addiction (EMCDDA) is protected by copyright. The EMCDDA accepts no responsibility or liability for any consequences arising from the use of the data contained in this document. The contents of this publication do not necessarily reflect the official opinions of the EMCDDA’s partners, any EU Member State or any agency or institution of the European Union. Europe Direct is a service to help you find answers to your questions about the European Union Freephone number (*): 00 800 6 7 8 9 10 11 (*) The information given is free, as are most calls (though some operators, phone boxes or hotels may charge you). More information on the European Union is available on the internet (http://europa.eu). Luxembourg: Publications Office of the European Union, 2016 ISBN: 978-92-9168-841-8 doi:10.2810/324608 © European Monitoring Centre for Drugs and Drug Addiction, 2016 Reproduction is authorised provided the source is acknowledged. This publication should be referenced as: European Monitoring Centre for Drugs and Drug Addiction (2016), The internet and drug markets, EMCDDA Insights 21, Publications Office of the European Union, Luxembourg. References to chapters in this publication should include, where relevant, references to the authors of each chapter, together with a reference to the wider publication. For example: Mounteney, J., Oteo, A. and Griffiths, P. -

Timeline 1994 July Company Incorporated 1995 July Amazon

Timeline 1994 July Company Incorporated 1995 July Amazon.com Sells First Book, “Fluid Concepts & Creative Analogies: Computer Models of the Fundamental Mechanisms of Thought” 1996 July Launches Amazon.com Associates Program 1997 May Announces IPO, Begins Trading on NASDAQ Under “AMZN” September Introduces 1-ClickTM Shopping November Opens Fulfillment Center in New Castle, Delaware 1998 February Launches Amazon.com Advantage Program April Acquires Internet Movie Database June Opens Music Store October Launches First International Sites, Amazon.co.uk (UK) and Amazon.de (Germany) November Opens DVD/Video Store 1999 January Opens Fulfillment Center in Fernley, Nevada March Launches Amazon.com Auctions April Opens Fulfillment Center in Coffeyville, Kansas May Opens Fulfillment Centers in Campbellsville and Lexington, Kentucky June Acquires Alexa Internet July Opens Consumer Electronics, and Toys & Games Stores September Launches zShops October Opens Customer Service Center in Tacoma, Washington Acquires Tool Crib of the North’s Online and Catalog Sales Division November Opens Home Improvement, Software, Video Games and Gift Ideas Stores December Jeff Bezos Named TIME Magazine “Person Of The Year” 2000 January Opens Customer Service Center in Huntington, West Virginia May Opens Kitchen Store August Announces Toys “R” Us Alliance Launches Amazon.fr (France) October Opens Camera & Photo Store November Launches Amazon.co.jp (Japan) Launches Marketplace Introduces First Free Super Saver Shipping Offer (Orders Over $100) 2001 April Announces Borders Group Alliance August Introduces In-Store Pick Up September Announces Target Stores Alliance October Introduces Look Inside The BookTM 2002 June Launches Amazon.ca (Canada) July Launches Amazon Web Services August Lowers Free Super Saver Shipping Threshold to $25 September Opens Office Products Store November Opens Apparel & Accessories Store 2003 April Announces National Basketball Association Alliance June Launches Amazon Services, Inc. -

Fusion of Technology Management and Financing Management - Amazon's Transformative Endeavor by Orchestrating Techno-Financing Systems

Journal Pre-proof Fusion of technology management and financing management - Amazon's transformative endeavor by orchestrating techno-financing systems Yuji Tou, Chihiro Watanabe, Pekka Neittaanmäki PII: S0160-791X(19)30374-4 DOI: https://doi.org/10.1016/j.techsoc.2019.101219 Reference: TIS 101219 To appear in: Technology in Society Received Date: 7 August 2019 Revised Date: 11 October 2019 Accepted Date: 26 November 2019 Please cite this article as: Tou Y, Watanabe C, Neittaanmäki P, Fusion of technology management and financing management - Amazon's transformative endeavor by orchestrating techno-financing systems, Technology in Society (2020), doi: https://doi.org/10.1016/j.techsoc.2019.101219. This is a PDF file of an article that has undergone enhancements after acceptance, such as the addition of a cover page and metadata, and formatting for readability, but it is not yet the definitive version of record. This version will undergo additional copyediting, typesetting and review before it is published in its final form, but we are providing this version to give early visibility of the article. Please note that, during the production process, errors may be discovered which could affect the content, and all legal disclaimers that apply to the journal pertain. © 2019 Published by Elsevier Ltd. TIS_2019_345_title_page_Revised Fusion of Technology Management and Financing Management - Amazon’s Transformative Endeavor by Orchestrating Techno-financing Systems Yuji Tou 1, Chihiro Watanabe 2 ,3 , Pekka Neittaanmäki 2 1 Dept. of Ind. Engineering & Magm., Tokyo Institute of Technology, Tokyo, Japan 2 Faculty of Information Technology, University of Jyväskylä, Finland 3 International Institute for Applied Systems Analysis (IIASA), Austria Abstract Amazon became the world R&D leader in 2017 by rapidly increasing R&D investment. -

Impact Analysis of Wireless and Mobile Technology on Business Management Strategies Rashed Azim East India Services Limited, London

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by International Institute for Science, Technology and Education (IISTE): E-Journals Information and Knowledge Management www.iiste.org ISSN 2224-5758 (Paper) ISSN 2224-896X (Online) Vol.3, No.2, 2013 Impact analysis of wireless and mobile technology on business management strategies Rashed Azim East India Services Limited, London Azizul Hassan Tourism Consultants Network, the Tourism Society Telephone Number: 0044 07853024625; Email: [email protected] Abstract: This research examines whether congruence exists between wireless and mobile technology with impact analysis on a firm’s business management development and future strategies. The research adopted the Motorola Inc. as a case and the qualitative approach as the research method. It emerged from analysis that consumers, business management strategies and future strategic directions are embedded in wireless and mobile technology. Despite having high tech wireless and mobile technology, it is not always been possible to appear as the market leader within industry, where future consumer behaviour and business management strategies will differ from the one those exist today. This study proposes a new framework for diversifying intellectual capacity to develop consultancy based growth opportunity at Motorola. This also suggests intense mobile and wireless technological impacts on relationships with customers, enterprise agility and business management strategies in the internet based market structure. Keywords: wireless and mobile technology, process automation, cloud infrastructure, convergence, business management strategy Introduction: Demand for investigation of wireless and mobile technological influences on corporate and business management strategies with impacts on consumers are increasing. -

Evaluation of Nigeria Universities Websites Using Alexa Internet Tool: a Webometric Study

University of Nebraska - Lincoln DigitalCommons@University of Nebraska - Lincoln Library Philosophy and Practice (e-journal) Libraries at University of Nebraska-Lincoln 2020 Evaluation of Nigeria Universities Websites Using Alexa Internet Tool: A Webometric Study Samuel Oluranti Oladipupo Mr University of Ibadan, Ibadan, Nigeria, [email protected] Follow this and additional works at: https://digitalcommons.unl.edu/libphilprac Part of the Library and Information Science Commons Oladipupo, Samuel Oluranti Mr, "Evaluation of Nigeria Universities Websites Using Alexa Internet Tool: A Webometric Study" (2020). Library Philosophy and Practice (e-journal). 4549. https://digitalcommons.unl.edu/libphilprac/4549 Evaluation of Nigeria Universities Websites Using Alexa Internet Tool: A Webometric Study Samuel Oluranti, Oladipupo1 Africa Regional Centre for Information Science, University of Ibadan, Nigeria E-mail:[email protected] Abstract This paper seeks to evaluate the Nigeria Universities websites using the most well-known tool for evaluating websites “Alexa Internet” a subsidiary company of Amazon.com which provides commercial web traffic data. The present study has been done by using webometric methods. The top 20 Nigeria Universities websites were taken for assessment. Each University website was searched in Alexa databank and relevant data including links, pages viewed, speed, bounce percentage, time on site, search percentage, traffic rank, and percentage of Nigerian/foreign users were collected and these data were tabulated and analysed using Microsoft Excel worksheet. The results of this study reveal that Adekunle Ajasin University has the highest number of links and Ladoke Akintola University of Technology with the highest number of average pages viewed by users per day. Covenant University has the highest traffic rank in Nigeria while University of Lagos has the highest traffic rank globally. -

In the United States District Court for the Eastern District of Texas Tyler Division

CaseCase 6:06-cv-00452-LED 6:06-cv-00452-LED Document Document 22 27 Filed Filed 02/20/2007 02/26/07 Page Page 1 of 1 15of 15 IN THE UNITED STATES DISTRICT COURT FOR THE EASTERN DISTRICT OF TEXAS TYLER DIVISION INTERNATIONAL BUSINESS ) MACHINES CORPORATION, ) ) Plaintiff, ) Civil Action No. 6:06-cv-452 ) JURY v. ) ) AMAZON.COM, INC., AMAZON ) SERVICES LLC F/K/A AMAZON ) SERVICES, INC. D/B/A AMAZON ) ENTERPRISE SOLUTIONS AND ) AMAZON SERVICES BUSINESS ) SOLUTIONS, AMAZON.COM INT’L ) SALES, INC. D/B/A AMAZON.CO.JP, ) AMAZON EUROPEAN UNION S.À.R.L. ) D/B/A AMAZON.DE, AMAZON.FR AND ) AMAZON.CO.UK, AMAZON SERVICES ) EUROPE S.À.R.L. D/B/A AMAZON.DE, ) AMAZON.FR AND AMAZON.CO.UK, ) AMAZON.COM.CA, INC., A9.COM, INC., ) ALEXA INTERNET D/B/A ALEXA ) INTERNET, INC. AND ALEXA ) INTERNET CORP., INTERNET MOVIE ) DATABASE, INC., CUSTOMFLIX LABS, ) INC., MOBIPOCKET.COM SA, ) AMAZON.COM LLC D/B/A ) ENDLESS.COM, BOP, LLC D/B/A ) SHOPBOP.COM, AMAZON WEB ) SERVICES, LLC, AND AMAZON ) SERVICES CANADA, INC., ) ) Defendants. ) FIRST AMENDED COMPLAINT FOR PATENT INFRINGEMENT Plaintiff International Business Machines Corporation (“IBM”), for its First Amended Complaint for Patent Infringement against Defendants Amazon.com, Inc., Amazon Services LLC f/k/a Amazon Services, Inc. d/b/a Amazon Enterprise Solutions and Amazon Services KING/KAPLAN FIRST AMENDED PATENT COMPLAINT DLI-6098701v2 CaseCase 6:06-cv-00452-LED 6:06-cv-00452-LED Document Document 22 27 Filed Filed 02/20/2007 02/26/07 Page Page 2 of 2 15of 15 Business Solutions, Amazon.com Int’l Sales, Inc. -

Why Are Some Websites Researched More Than Others? a Review of Research Into the Global Top Twenty Mike Thelwall

Why are some websites researched more than others? A review of research into the global top twenty Mike Thelwall How to cite this article: Thelwall, Mike (2020). “Why are some websites researched more than others? A review of research into the global top twenty”. El profesional de la información, v. 29, n. 1, e290101. https://doi.org/10.3145/epi.2020.ene.01 Manuscript received on 28th September 2019 Accepted on 15th October 2019 Mike Thelwall * https://orcid.org/0000-0001-6065-205X University of Wolverhampton, Statistical Cybermetrics Research Group Wulfruna Street Wolverhampton WV1 1LY, UK [email protected] Abstract The web is central to the work and social lives of a substantial fraction of the world’s population, but the role of popular websites may not always be subject to academic scrutiny. This is a concern if social scientists are unable to understand an aspect of users’ daily lives because one or more major websites have been ignored. To test whether popular websites may be ignored in academia, this article assesses the volume and citation impact of research mentioning any of twenty major websites. The results are consistent with the user geographic base affecting research interest and citation impact. In addition, site affordances that are useful for research also influence academic interest. Because of the latter factor, however, it is not possible to estimate the extent of academic knowledge about a site from the number of publications that mention it. Nevertheless, the virtual absence of international research about some globally important Chinese and Russian websites is a serious limitation for those seeking to understand reasons for their web success, the markets they serve or the users that spend time on them. -

Liberty Mutual Exhibit 1016

TIMELINE 2012 July Introduces GameCircle Introduces Game Connect Opens Portal for International Mobile App Distribution June Amazon Publishing Acquires Avalon Books May Amazon Studios to Develop Original Comedy and Children’s Series for Amazon Instant Video April Announces First Quarter Sales up 34% to $13.18 Billion Introduces AmazonSupply Amazon Web Services Introduces AWS Marketplace Introduces eBooks Kindle en Español March Acquires Kiva Systems, Inc. February Launches Sports Collectibles Store January Announces Fourth Quarter Sales up 35% to $17.43 Billion Amazon Web Services Launches Amazon DynamoDB 2011 December Amazon Web Services Launches Brazil Datacenters for Its Cloud Computing Platform Introduces KDP Select Amazon Publishing to Acquire Marshall Cavendish US Children’s Books Titles Page 000001 November Introduces The Kindle Owners’ Lending Library October Announces Third Quarter Sales up 44% to $10.88 Billion September Introduces Amazon Silk Introduces Kindle Fire, Kindle Touch and Kindle Touch 3G Kindle Books Available at Thousands of Local Libraries August Amazon Web Services Announces Global Rollout of Amazon Virtual Private Cloud (Amazon VPC) Introduces Kindle Cloud Reader July Announces Second Quarter Sales up 51% to $9.91 Billion Endless.com Announces International Shipping to over 50 Countries Worldwide AT&T to Sponsor Kindle 3G June Launches AmazonLocal John Locke Becomes First Independently Published Author to Join the "Kindle Million Club" May Announces MYHABIT.COM Amazon.com Now Selling More Kindle Books Than Print -

Amazon Enters the Cloud Computing Business

S T A N F O R D U NIVERSITY 2 0 0 8 - 3 5 3 - 1 S C H O O L O F E NGINEERING WWW.CASEP UBLISHER . COM Rev. May 20, 2008 AMAZON ENTERS THE CLOUD COMPUTING BUSINESS T A B L E O F C ONTENTS 1. Introduction 2. Company Overview 2.1. The Founding of Amazon 2.2. Amazon’s Culture 2.3. Amazon’s Retail Business 2.4. Amazon’s Other Services & Products 2.5. Financial Performance of Amazon 2.6. Competition and Competitive Trends 3. Cloud Computing Overview 4. Amazon Enters the Market for Cloud Computing and Storage Services 4.1. Amazon’s Elastic Compute Cloud (EC2) 4.2. Amazon’s Simple Storage Service (S3) 4.3. Customers of Amazon’s Cloud Computing 4.4. Partners of Amazon’s Cloud Computing 5. Industry and Analyst Responses 5.1. Microsoft 5.2. Google 5.3. Sun Microsystem 5.4. IBM 5.5. Market Analysts 6. Exhibits 7. References Professors Micah Siegel (Stanford University) and Fred Gibbons (Stanford University) guided the de- velopment of this case using the CasePublisher service, available online at www.casepublisher.com as the basis for class discussion rather than to i)ustrate either e*ective or ine*ective handling of a business situation. 2008-353-1 Amazon Enters the Cloud Computing Business I NTRODUCTION Amazon CEO Jeff Bezos looked at the clock on the instrument panel of his Segway Human Transporter; it was 7:52AM and he knew he would need a little luck to get to his 8:00AM meeting at Amazon's Beacon Hill headquarters. -

Alexa Analytics Recommended For

Alexa Analytics Recommended For Doiled Odell sometimes wrap any secretaire warsle late. Sectoral Windham musses anarchically or engilds out-of-date when Bernhard is paroxytone. Enemy and connected Maxfield produce while incursive Burt attire her expedients specially and adjudges unresponsively. Alexa site rank in the smart devices allow you to this lower for this for alexa skills and marketing Voice search optimisation for Alexa Siri and Cortana The Drum. If her is, the brand can make smart a customized offer that reflects exactly whom she needs to is put. Amazon Alexa Cheat sheet TechRepublic. Due all the relatively lower population of websites ranked by Alexa, it is better knowledge not upon the statistics from Alexa, but operate it only specific comparison purposes. It is fun to check and see my progress. Alexa ranking for every other voice application on the best known than evaluate the. Alexa skill development services vary depending on the needs of your business. You can only the game online during history during the day, through the comfort provide your home. Google Analytics does a good job of giving us the data we need. The conclusion was Google Analytics is all accurate than Alexa. The siege of Simulation for IoT Hacking Alexa with Parasoft. We recommend a recommended by one. The alexa for all about money through extraneous content management, your recommended because it can recommend a website traffic and analyze websites. Provides services for broad field of applications including compute storage databases networking analytics machine learning and understand intelligence AI. Proactive management system for alexa internet functions as ads and recommendations for it shows how many people need more than interesting information! It's suddenly to measure that Alexa rank can be a crown piece of line for website comparison Just don't base is much more your marketing work having it as magnitude is not as accurate as something like Google Analytics Think of it send a complementary tool to strengthen your SEO strategy. -

Omnia Amazon Business R-TC-17006

amazonbusiness.,.,,_,__, October 14, 2016 Mr. Anthony Crosby Coordinator Prince William County Public Schools Financial Services/Purchasing Room #1500 RFP #R-TC-17006 P.O. Box 389 Manassas, VA 20108 Dear Mr. Crosby, It is with great pleasure that we enclose our response to your request for proposal for the on-line marketplace for the purchase of products and services. Amazon Services, LLC. (Amazon.com) is an e-commerce company offering a range of products and services through our website. Amazon herewith offers Prince William County Public Schools (PWCPS) our Amazon Business solution to assist PWCPS in your on-line marketplace needs. Please review our responses and feel free to contact Daniel Smith, General Manager, (206) 708-9895 or via email at [email protected] to answer any questions you may have. The entire team at Amazon Business looks forward to building a mutually beneficial relationship with Prince William County Public Schools. Respectfully, Prentis Wilson Vice President Amazon Business Amazon Services, LLC • 410 Terry Avenue North • Seattle, WA 98109-5210 • USA Prince William County Schools RFP R-TC-17006 On-line Marketplace for the Purchases of Products and Services Table of Contents 1.0 Title Sheet (Tab 1) ................................................................................................ 1 2.0 Executive Summary (Tab 2) ................................................................................. 3 Product Benefits .........................................................................................................