Nordea Cuts Payment Costs, Boosts Customer Satisfaction

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

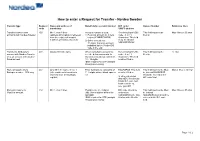

How to Enter a Request for Transfer - Nordea Sweden

How to enter a Request for Transfer - Nordea Sweden Transfer type Request Name and address of Beneficiary’s account number BIC code / Name of banker Reference lines code beneficiary SWIFT address Transfer between own 400 Min 1, max 4 lines Account number is used: Receiving bank’s BIC This field must not be Max 4 lines x 35 char accounts with Nordea Sweden (address information is retrieved 1) Personal account no = pers code - 8 or 11 filled in from the register of account reg no (YYMMDDXXXX) characters. This field numbers of Nordea, Sweden) 2) Other account nos = must be filled in 11 digits. Currency account NDEASESSXXX indicated by the 3-letter ISO code in the end Transfer to third party’s 401 Always fill in the name When using bank account no., Receiving bank’s BIC This field must not be 12 char account with Nordea Sweden see the below comments. In code - 8 or 11 filled in or to an account with another Sweden account nos consist of characters. This field Swedish bank 10 - 15 digits. must be filled in IBAN required for STP (straight through processing) Domestic payments to 402 Only fill in the name in line 1 Enter bankgiro no consisting of BGABSESS. This field This field must not be filled Max 4 lines x 35 char Bankgiro number - SEK only (other address information is 7 - 8 digits without blank spaces must be filled in. in. Instead BGABSESS retrieved from the Bankgiro etc should be entered in the register) In other currencies BIC code field than SEK: Receivning banks BIC code and bank account no. -

Fusion Netcapture Reporting and Deposit Management User Guide

Fusion NetCapture Reporting and Deposit Management User Guide Version 8.5 February 2019 Copyright © 2008 - 2019 Finastra International Limited, or a member of the Finastra group of companies (“Finastra”). All Rights Reserved. Confidential - Limited Distribution to Authorized Persons Only, pursuant to the terms of the license agreement by which you were granted a license from Finastra for the applicable software or services and this documentation. Republication or redistribution, in whole or in part, of the content of this documentation or any other materials made available by Finastra is prohibited without the prior written consent of Finastra. The software and documentation are protected as unpublished work and constitute a trade secret of Finastra International Limited, or a member of the Finastra group of companies, Head Office: One Kingdom Street, Paddington, London W2 6BD, United Kingdom. Trademarks Finastra, Fusion NetCapture, and their respective sub-brands, and the logos used with some of these marks, are trademarks or registered trademarks of Finastra International Limited, or a member of the Finastra group of companies (“Finastra”) in various countries around the world. All other brand and product names are trademarks, registered trademarks, or service marks of their respective owners, companies, or organizations, may be registered, and should be treated appropriately. Disclaimer Finastra does not guarantee that any information contained herein is and will remain accurate or that use of the information will ensure correct and faultless operation of the relevant software, services or equipment. This document contains information proprietary to Finastra. Finastra does not undertake mathematical research but only applies mathematical models recognized within the financial industry. -

UK Gender Pay Report 2018

UK Gender Pay Report 2018 Finastra International Limited © Finastra International Limited All rights reserved Registered in England & Wales No. 01360027 Registered Office © Finastra | 04 April 2019 | Title XXXXXXXXXXX Four Kingdom Street Paddington0 London W2 6BD United Kingdom LIFE AT FINASTRA “Our goal of becoming the most admired, inclusive and diverse employer in Fintech is taking shape. I am proud of the headway we are making, and the commitment of our teams to drive and push for balance as we continue on our mission” Simon Paris, Chief Executive Officer At Finastra, we believe with more than 10,000 of us across 48 different countries globally, it is us who create success, collaborate and contribute to making Finastra the place to work. We recognise the best talent and provide a work environment where people can drive results, develop and grow their careers. Our people are leaders in their roles and are always looking for new ways to help our customers grow, compete and optimise their businesses. After bringing together two global fintech leaders in June 2017, Finastra has recognised the opportunity and power that comes from combining our expertise, skills and innovation. Today we are one team creating a network of talent and creativity in a stimulating environment, dedicated to making a difference for each other and our customers. At Finastra, we are committed to creating an open and equal working environment whilst rewarding all of our colleagues fairly, based on their role, skills and experience. Our Global Career Framework provides a systematic approach to how we manage reward, performance and talent. -

Nordea Group Annual Report 2018

Annual Report 2018 CEO Letter Casper von Koskull, President and Group CEO, and Torsten Hagen Jrgensen, Group COO and Deputy CEO. Page 4 4 Best and most accessible advisory, with an 21 easy daily banking experience, delivered at scale. Page 13 Wholesale Banking No.1 relationship Asset & Wealth bank in the Nordics Management with operational Personal Banking 13 excellence. Page 21 Commercial & Business Banking Our vision is to become the lead- ing Asset & Wealth Manager in the 25 Nordic market by 2020. Page 25 Best-in-class advisory and digital experience, 17 ef ciency and scale with future capabilities in a disruptive market. Page 17 Annual Report 2018 Contents 4 CEO letter 6 Leading platform 10 Nordea investment case – strategic priorities 12 Business Areas 35 Our people Board of Directors’ report 37 The Nordea share and ratings 40 Financial Review 2018 46 Business area results 49 Risk, liquidity and capital management 67 Corporate Governance Statement 2018 76 Non-Financial Statement 78 Conflict of interest policy 79 Remuneration 83 Proposed distribution of earnings Financial statements 84 Financial Statements, Nordea Group 96 Notes to Group fi nancial statements 184 Financial statements Parent company 193 Notes to Parent company fi nancial statements 255 Signing of the Annual Report 256 Auditor’s report Capital adequacy 262 Capital adequacy for the Nordea Group 274 Capital adequacy for the Nordea Parent company Organisation 286 Board of Directors 288 Group Executive Management 290 Main legal structure & Group organisation 292 Annual General Meeting & Financial calendar This Annual Report contains forward-looking statements macro economic development, (ii) change in the competitive that reflect management’s current views with respect to climate, (iii) change in the regulatory environment and other certain future events and potential fi nancial performance. -

Finastra Universe 2017 Was a Resounding Success, Breaking All of Our Previous Records

7 - 8 NOVEMBER 2017 - DUBAI POST-EVENT SUMMARY SPONSORED BY: HOSTED BY: Platinum Sponsor Gold Sponsor Silver Sponsor THE FIRST AND THIRD A YEAR OF RE-BIRTH AN OPEN FUTURE Finastra Universe 2017 was a resounding success, breaking all of our previous records. The attendance at Finastra Universe this year highlights that the regional financial services market is increasingly subscribing to a policy of change, as digital transformation catches up with us. To counter the growing competition seen from new FinTechs, it is becoming critically important for the more traditional financial service instututions to embrace innovative technological solutions, becoming the disruptors rather Wissam Khoury Managing Director than the disrupted. Middle East, Africa & South Asia We are at an inflection point, with the next few years determining the new Finastra financial services landscape; one driven by the dynamic needs of our client-base instead of our competitive environment. Finastra Universe 2017 offered an unparralled exploration of that future, drawing together many of the region’s leading FinTech and banking experts to begin the process of building a roadmap to help us develop the solutions of tomorrow. An evolution of the Misys Connect Forum, Finastra Universe grew from the merger this year of Misys and D+H Insight. Our third annual event and the first of a new breed, our goal was to further the regional conversion on the challenges our market faces and, with over 330 attendees and more than 50 speakers covering the spectrum of financial service instutions, FinTechs and new market incumbents, we’ve laid the groundwork to continue that process as we move into 2018. -

Fourth Quarter 2019 Performance Report

Q4 Fourth Quarter 2019 Performance Report Pueblo County Employees’ Retirement Plan February 24, 2020 Dale A. Connors, CFA Senior Consultant This presentation is accompanied by additional disclosures which can be found on the last pages. All information herein is confidential and proprietary. CONTENTS 1 Capital Markets Exhibits 15 Pension Plan Analysis 39 Benchmark History 40 Manager Roster 41 Fee Schedule 42 Endnotes 4th Quarter 2019 Capital Markets Exhibits This presentation is accompanied by additional disclosures which can be found on the last pages. All information herein is confidential and proprietary. 1 All Asset Classes Rally in 2019 Major Capital Market Returns vs. Long-Term Average Returns Yields Compress Yield (%) Return (%) 10.00 8.00 S&P 500 Index 11.8 31.5 276bps 6.00 4.00 Russell 2000 Index 10.7 25.5 77bps 2.00 0.00 MSCI EAFE Index 8.8 22.0 10 Yr Treasury High Yield YE 2018 YE 2019 Source: Bloomberg Finance, LP MSCI Emerging Markets Index 9.0 18.4 Synchronized Capital Market Gains All major asset classes generated returns above their long- Bloomberg Barclays Aggregate 7.5 8.7 term average returns. Index 2019 marks the first time in the last 50 years the S&P 500, bonds, and gold posted positive returns of at least 30%, Bloomberg Barclays High Yield 8.8 14.3 5%, and 10%, respectively. Index The S&P 500 had the best return since 2013. Non-US equities had strong positive performance but lagged domestic equities. Bloomberg Commodity Index 1.9 7.7 Both interest rates and credit spreads compressed within the fixed income market. -

Fitch Ratings ING Groep N.V. Ratings Report 2020-10-15

Banks Universal Commercial Banks Netherlands ING Groep N.V. Ratings Foreign Currency Long-Term IDR A+ Short-Term IDR F1 Derivative Counterparty Rating A+(dcr) Viability Rating a+ Key Rating Drivers Support Rating 5 Support Rating Floor NF Robust Company Profile, Solid Capitalisation: ING Groep N.V.’s ratings are supported by its leading franchise in retail and commercial banking in the Benelux region and adequate Sovereign Risk diversification in selected countries. The bank's resilient and diversified business model Long-Term Local- and Foreign- AAA emphasises lending operations with moderate exposure to volatile businesses, and it has a Currency IDRs sound record of earnings generation. The ratings also reflect the group's sound capital ratios Country Ceiling AAA and balanced funding profile. Outlooks Pandemic Stress: ING has enough rating headroom to absorb the deterioration in financial Long-Term Foreign-Currency Negative performance due to the economic fallout from the coronavirus crisis. The Negative Outlook IDR reflects the downside risks to Fitch’s baseline scenario, as pressure on the ratings would Sovereign Long-Term Local- and Negative increase substantially if the downturn is deeper or more prolonged than we currently expect. Foreign-Currency IDRs Asset Quality: The Stage 3 loan ratio remained sound at 2% at end-June 2020 despite the economic disruption generated by the lockdowns in the countries where ING operates. Fitch Applicable Criteria expects higher inflows of impaired loans from 4Q20 as the various support measures mature, driven by SMEs and mid-corporate borrowers and more vulnerable sectors such as oil and gas, Bank Rating Criteria (February 2020) shipping and transportation. -

A NEW AGE of FINANCIAL SOFTWARE IS HERE the Banking Dilemma

A NEW AGE OF FINANCIAL SOFTWARE IS HERE The Banking Dilemma We live in an era of increasing choice and next-generation technologies — yet many banks and financial institutions are still grappling with disparate legacy systems, siloed business models, and locked IT budgets. So how can financial institutions keep up with their customers’ demands for greater value and digital-first technologies? By leveraging open platform technology, they can enjoy faster time to market, increased efficiencies, and above all deliver a better customer experience. 2 FINASTRA A new age of financial software is here The Future of Finance Is Open A once-in-a-generation transformation is currently underway in the financial services industry. Closed legacy systems are coming to an end as banks and financial institutions seek more open and agile software solutions to accelerate growth, optimize costs, and improve customer experience. Community collaboration and industry co-innovation are becoming the norm as financial institutions look to the outside to differentiate and stay competitive. The open banking journey has only just begun, and the financial institutions who embrace this paradigm shift will not only survive, but thrive in the world of tomorrow. Collaborate Collaboration is the new strategy for innovation. COLLABORATE TO INNOVATE to Innovate 3 FINASTRA A new age of financial software is here The Future with Finastra Finastra is a Fintech powerhouse delivering next-generation financial services solutions. As a pioneer in SaaS and cloud, we build and deploy componentized technology on our open FusionFabric software architecture – offering the broadest and deepest range of financial software solutions on the market. -

September 2018

The definitive source of news and analysis of the global fintech sector | September 2018 www.bankingtech.com ELEMENTS OF FINTECH Pure in substance FOOD FOR THOUGHT Ecosystem is not a safe word EXCLUSIVE INTERVIEW: YVES TYRODE, BPCE A whole new digital strategy FINTECH FUTURES BT_AFS Transformation Partner_Final_Layout 1 8/20/2018 9:42 AM Page 1 IN THIS ISSUE Your Core Lending Transformation Partner With hundreds of implementations on time and on budget. Contents AFS System Capabilities •End-to-End Credit Processing NEWS 04 The latest fintech news from around the globe: •Scaleable & Agile the good, the bad and the ugly. •Mobile Enabled 17 Interview: Serena Smith, FIS Being at the heart of the exciting, changing •Real-Time world of payments. •Digital 18 PayTech Awards 2018 Celebrations, winners, photos – all the best bits! •RPA, ML & AI 22 Lendtech vendor spotlight: AFS Innovating and transforming the credit •Data Integrity process globally. •Cyber Security & Risk 23 White paper The state of IT incident response in financial services. •Web Services/APIs for Bank Ecosystem 30 Food for thought •And Much More Fellow bankers: “ecosystem” is not a “safe word”. 33 Spotlight: Sunrise Banks A US bank that is “social enterprise first”. AFS is where technological innovation meets financial services expertise, 34 Case study: Afghanistan International Bank offering the latest in core lending with advanced credit process Facing challenges far more extreme than most banks around the globe. management that is operational in multiple, large banks. We provide 38 Interview: Yves Tyrode, BPCE unique, industry-leading solutions with proven successes to help you On a mission to deploy a whole new digital strategy. -

Nordea Fund of Funds, SICAV Société D’Investissement À Capital Variable R.C.S

Nordea Fund of Funds, SICAV Société d’Investissement à Capital Variable R.C.S. Luxembourg B 66 248 562, rue de Neudorf, L-2220 Luxembourg NOTICE TO SHAREHOLDERS On 25th January 2018 NORDEA and UBS announced an agreement on the acquisition of part of Nordea’s Luxembourg-based private banking business by UBS (hereinafter the “Transaction”). The Transaction foresees the acquisition of part of Nordea Bank S.A.’s business and its integration onto UBS’s advisory platform. Subject to the completion of the Transaction, the shareholders (the “Shareholders“) of Nordea Fund of Funds (the “Company”) are hereby informed of the following changes: 1. Change of the Investment Managers and appointment of an Investment Sub Manager: 1.1. Nordea Investment Management AB : New Investment Manager : Current Investment Manager Investment Manager with effect as of the 15th of October 2018 Nordea Bank S.A. Nordea Investment Management AB, including 562, rue de Neudorf its branches L-2220 Luxembourg Mäster Samuelsgatan 21 Stockholm, M540 10571 Sweden 1.2. UBS Europe SE, Luxembourg Branch : Investment Sub Manager : Nordea Investment Management AB has further appointed UBS Europe SE, Luxembourg Branch, 33 A Avenue J.F. Kennedy L-1855 Luxembourg as investment sub-manager with effect as of the 15th of October 2018. 2. Redemption of shares free of charges Shareholders who do not agree to the changes as described above may redeem their Shares free of any charges, with the exception of any local transaction fees that might be charged by local intermediaries on their own behalf and which are independent from the Company and the Management Company. -

Lloyds Banking Group PLC

Lloyds Banking Group PLC Primary Credit Analyst: Nigel Greenwood, London (44) 20-7176-1066; [email protected] Secondary Contact: Richard Barnes, London (44) 20-7176-7227; [email protected] Table Of Contents Major Rating Factors Outlook Rationale Related Criteria Related Research WWW.STANDARDANDPOORS.COM/RATINGSDIRECT JUNE 5, 2020 1 THIS WAS PREPARED EXCLUSIVELY FOR USER CIARAN TRELLIS. NOT FOR REDISTRIBUTION UNLESS OTHERWISE PERMITTED. Lloyds Banking Group PLC Major Rating Factors Issuer Credit Rating BBB+/Negative/A-2 Strengths: Weaknesses: • Market-leading franchise in U.K. retail banking, and • Geographically concentrated in the U.K., which is strong positions in U.K. corporate banking and now in recession owing to the impact of COVID-19. insurance. • Our risk-adjusted capital (RAC) ratio is lower than • Cost-efficient operating model that supports strong the average for U.K. peers, which partly reflects the pre-provision profitability, business stability, and deduction of Lloyds' material investment in its competitiveness. insurance business. • Supportive funding and liquidity profiles anchored by strong deposit franchise. WWW.STANDARDANDPOORS.COM/RATINGSDIRECT JUNE 5, 2020 2 THIS WAS PREPARED EXCLUSIVELY FOR USER CIARAN TRELLIS. NOT FOR REDISTRIBUTION UNLESS OTHERWISE PERMITTED. Lloyds Banking Group PLC Outlook The negative outlook on Lloyds Banking Group reflects potential earnings pressures arising from the economic and market impact of the COVID-19 pandemic. Downside scenario If we saw clear signs that the U.K. systemwide domestic loan loss rate was going to exceed 100 basis points in 2020, and not be offset by the prospect of a quick economic recovery, we would likely lower the anchor, our starting point for rating U.K. -

Terms and Conditions of Purchase of Goods and Services

TERMS AND CONDITIONS OF PURCHASE OF GOODS AND SERVICES 31 January 2018 © Finastra | 15 February 2018 | Title XXXXXXXXXXX 0 These terms and conditions govern the purchase of goods (“Goods”) and/or services (“Services”) identified on the Purchase Order (“PO”) by the Finastra entity identified on the front of such PO (“Finastra”) and which issues the PO to the person, firm, company or organisation whose name appears on the coversheet of the PO, or who accepts the PO (“Vendor”). 1. ENTRY INTO FORCE Save where there is a written agreement signed by the Parties relating to Goods and/or Services (including without limitation a Master Services Agreement) the terms and conditions herein, together with any attachments and exhibits, specifications, drawings, notes, instructions and other information, whether physically attached or incorporated by reference (together, “PO”) constitute the entire and exclusive agreement between Finastra and the Vendor. Vendor agrees that any terms different from or in addition to the terms herein, whether communicated orally or contained in any PO confirmation, invoice, acknowledgement, release, acceptance or other written correspondence, irrespective of the timing, shall not form a part of this PO, even if Vendor purports to condition its acceptance of the PO on Finastra agreement to such different or additional terms. Vendor’s electronic acceptance, acknowledgement of this PO, or commencement of performance constitutes Vendor’s acceptance of the terms and conditions set out herein. 2. DELIVERY AND DELAY Time is of the essence in all orders specifying a delivery date. The delivery period specified shall be deemed to begin from the date of the PO.