Uses and Abuses of Value Capture for Transit

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Applicant Spreadsheet.Pdf

Contracting Company Company Representative Representative Phone # Representative Email Site Address Block Lot Borough Work Description Keywords Contract Amount Start Date Zip Code CB Electrical, plumbing, Commercial, retail, new windows, doors, elevatr, 31 Avenue Realty LLC Law Office of Thomas E. Berinato 718 575-3400 [email protected] 56-02 31 Avenue 1134 1 Queens 12,000,000 7/1/2017 11377 26 building foundation, superstructure steel, concrete, electrical, CBP 441 Ninth Avenue 433-447 Ninth Commercial, addition Marcus & Pollack LLP 212 490-2900 [email protected] 732 36 Manhattan plumbing, façade, roof, 185,000,000 6/1/2017 10001 3 Owner LLC Avenue to new space windows, HVAC, elevator foundation, concrete, work, superstructure, masonsry, roofing, Tuchman, Korngold, 251-277 South Fifth 19, 35, 13, Commercial, retail, new Havemeyer Owner LLC 212 687-3747 [email protected] 2447 Brooklyn facadew, curtain wall, 120,000,000 4/15/2017 11211 34 Weiss,Liebman & Gelles, LLP Street 135, 41, 36 building storefron, plumbing, HVAC, electrical, fire protection demolition, SOE, excavation, foundation, Commercial, retail, exterior wall, 545 Broadway BK LLC Seiden & Schein PC 212 857-0110 545 Broadway 3076 6 Brooklyn alteration, addition to superstructure, misc 17,070,465 4/1/2017 11206 34 existing building metals, roofing, waterproofing, drywall, [email protected] stone, tile, wood flooring concrete, steel, electrical, 2109 Borden Avenue Owner 21-09 Borden Marcus & Pollack, Esq. 212 490-2900 [email protected] 69 4 Queens Commercial, alteration carpentry, HVAC, 14,600,000 4/1/2017 11101 26 LLC Avenue plumbing electrical, plumbing, 331 Park Avenue 331 PAS Property Anthony Como Associates 718 273-3080 [email protected] 880 4 Manhattan Commercial, alteration concrete, carpentry, 11,000,000 3/15/2017 10010 2 South metals, etc. -

Land Use Planning Qualifications and Experience

FIGURE 24 69-02 QUEENS BOULEVARD VIEW 5 - 69TH ST AND 48TH AVE LAND USE PLANNING QUALIFICATIONS AND EXPERIENCE No-Action Condition (looking north at the intersection of 69th Street and 48th Avenue) Source: Street photograph taken on June 21, 2017 H U D S O N PM R I V E R AM W as G ra h in ss la gt n o ds n Hig h L in e Sun dec P 1 0 t h A V E N U E u k blic Park 1 4 t h S T R E E T With-Action Condition (looking north at the intersection of 69th Street and 48th Avenue) A Friendly Neighbor... Proposed Project 9-Story Residential Building (No-Build Project) Compared to a tower mass extruded vertically from the property line, the solar- carved tower yields a significant increase WOODSIDE,in yearly sunlight hours QUEENS, to two key NY areas on the High Line park: The Washington Grasslands to the east of the site, and the High Line Sundeck to the north. light blue dark green blue = = LIGHT! No Light VS. annual Solar Carve design As-of-right design sun hours (F.A.R. = 7.5) (F.A.R. = 5) ...and double the daylight! A daylight model demonstrates that compared to an as-of-right scheme, the proposed tower’s shape and position significantly increase the natural light and air to the High Line. In particular, the area directly to the east of the site will see DRAFT about twice the amount of possible sun hours! HIGHLINETechnical Excellence 14 Practical Experience Client Responsiveness Map Map Reference: ESRI Basemap; NYC DCP; and http; //windhistory.com/station.html?KNYC ATTACHMENT $: WIND DIRECTION MAP AVERAGE YEARLY SUSTAINABLE DESIGN Langan professionals design solutions that maintain the inherent connections between structures and their natural surroundings. -

Residential Apartments White Plains, NY

MX international MX International New York NY Westport CT 203 470 8888 tel 203 454 9689 fax mxinternational.com BUILDING PROJECTCONSTRUCTION MANAGEMENT A Total Project Management Company MX profile international MX International, LLC is a full service “Total Project Management Company” dedicated to providing its clients with best-in-class project and construction management services for a wide variety of building projects, in both the private and public sectors. As “total project managers,” MX takes full responsibility for the programming and supervision of the entire building project, from start to finish. Our team of experienced professionals work in close collaboration with our clients to provide them with customized and personalized service. The firm’s principals, each with well over twenty five years of experience in the design and construction management industries, have a thorough understanding of all phases of the building processes, from acquisition and funding through development and planning, architecture and design, and construction administration. Our wealth of industry knowledge and experience, in addition to our comprehensive resources of professionals in the development, construction, architectural and engineering industries, makes us uniquely equipped to fully comprehend and to service the individual needs of each and every one of our clients. Our management team consistently delivers a quality program, from project concept through project completion. Our innovative solutions go beyond our clients’ expectations and our reputation for integrity, honesty and excellence is of paramount importance to us. MX’s services are structured to provide our clients with the leadership role required for the successful planning and managing of their projects, whether large or small. -

Historic Albany Foundation Oldest Building Inventory (By Address) 1 Funded in Part by the Hudson River Valley Greenway, National

Historic Albany Foundation Oldest Building Inventory (by address) 1 ARCHITECT/BUILDER/1ST Locally Listed/ National Register/ STREET # STREET NAME BLD NAME DATE CIRCA NOTES OWNER National Historic Landmark Academy Park Albany Academy 1814 -17 Philip Hooker Joseph Henry Memorial name change in 1930 National Register Listed (individually) 17 Alexander Street 1850 -60 circa South End/Groesbeckville Historic District 28 Alexander Street 1855 circa Also listed as 1865-70 South End/Groesbeckville Historic District 29 Alexander Street 1850 -60 circa Christian Barum, First Owner Also listed as 1850-55 South End/Groesbeckville Historic District 30 Alexander Street 1855 George Burkhardt, First Owner South End/Groesbeckville Historic District 32 Alexander Street 1855 Conrad Hacker, First Owner South End/Groesbeckville Historic District 33 Alexander Street 1850 -55 circa Christian Winzel, First Owner South End/Groesbeckville Historic District 35 Alexander Street 1850 -60 circa Myler Fish, First Owner South End/Groesbeckville Historic District 35 Alexander Street 1860 circa or pre Mrs. Swartz Brick front South End/Groesbeckville Historic District 38 Alexander Street 1860 pre James Coyle, woodhshop; First Owner South End/Groesbeckville Historic District 55 Alexander Street 1850 pre Joseph Short, First Owner 57 Alexander Street 1846 -50 circa 47A Alexander Street 1846 -50 circa South End/Groesbeckville Historic District 47B Alexander Street 1846 -50 circa South End/Groesbeckville Historic District 7 Alfred Street 1850 circa greatly altered; very much -

Disposition Sheet & City Planning Commission Calendar

CITY PLANNING COMMISSION DISPOSITION SHEET PUBLIC MEETING: Yvette V. Gruel, Calendar Officer WEDNESDAY, MARCH 14, 2018 120 Broadway, 30th Floor 10:00 A.M. NYC CITY PLANNING COMMISSION HEARING ROOM New York, New York 10271 (212) 720-3370 LOWER CONCOURSE, 120 BROADWAY, NEW YORK, NY 10271 CAL CD NO. ULURP NO. NO. PROJECT NAME C.P.C. ACTION 1 C 180242 PPX 12 EDENWALD YMCA Scheduled to be Heard 3/28/18 2 N 180238 ZRM 4 HUDSON BOULEVARD AND PARK TEXT AMENDMENT " " 3 C 180130 HAX 1 PARK HAVEN RESIDENCE Favorable Report Adopted 4 C 180131 ZMX 1 " " " " 5 N 180132 ZRX 1 " " " " 6 N 180239 PXX 8 TLC OFFICE SPACE Previously Adopted (3/12/18) 7 N 180147 ZAX 8 BERCZELY RESIDENCE Authorization Approved 8 N 180136 ZAX 8 WIENER RESIDENCE " " 9 N 180137 ZAX 8 " " " " 10 N 180240 PXM 1 OLR OFFICE SPACE Previously Adopted (3/12/18) 11 C 180112 ZMM 7 WEST 108TH STREET WSFSSH DEVELOPMENT Favorable Report Adopted 12 N 180113 ZRM 7 " " " " 13 C 180114 HAM 7 " " " " 14 C 180062 ZSM 2 31 BOND STREET " " 15 C 180088 ZMX 1 WILLOW AVENUE REZONING Hearing Closed 16 N 180089 ZRX 1 " " " " 17 C 180063 ZSM 1 45 BROAD STREET " " COMMISSION ATTENDANCE: Present (P) COMMISSION VOTING RECORD: Absent (A) In Favor - Y Oppose - N Abstain - AB Recuse - R Calendar Numbers: 3 4 5 6 7 8 9 10 11 12 13 14 Marisa Lago, Chair P Y Y Y Y Y Y Y Y Y Y Y Y Kenneth J. Knuckles, Esq., Vice Chairman P Y Y Y Y Y Y Y Y Y Y Y Y Rayann Besser P Y Y Y Y Y Y Y Y Y Y Y Y Alfred C. -

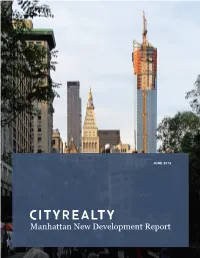

Manhattan New Development Report

JUNE 2016 Manhattan New Development Report MANHATTAN NEW DEVELOPMENT REPORT June 2016 New Buildings by Neighborhood Condominium development has largely centered on Midtown over the past several years, but there will be a wave of new construction and conversions in the Financial District in the near future, with large buildings such as 50 West Street, One Seaport and 125 Greenwich Street contributing to the roughly 1,250 new apartments slated for the neighborhood. NEW DEVELOPMENT KEY: UNITS: 10+ 50+ 100+ 150+ 200+ Unit Count NEIGHBORHOOD # OF UNITS NEIGHBORHOOD # OF UNITS Financial District 1,251 Broadway Corridor 264 Midtown West 1,229 Murray Hill 249 Lower East Side 912 East Village 207 Riverside Dr./West End Ave. 881 Chelsea 201 Flatiron/Union Square 499 SOHO 165 Gramercy Park 494 Central Park West 160 Tribeca 493 West Village 125 Midtown East 345 Beekman/Sutton Place 113 Yorkville 282 Carnegie Hill 105 2 June 2016 MANHATTAN NEW DEVELOPMENT REPORT Summary Condominium development is a multi-billion dollar business in Manhattan, and new apartment sales are poised to reach a level not seen since last decade’s boom cycle by 2018. While fewer developers in 2016 are signing on to build sky-grazing towers with penthouses that cost $100 million or more, condominium prices are still on an upward trajectory, with anticipated sales totaling roughly $30 billion through 2019. In total, 92 condominium projects with roughly 8,000 new apartments are under construction or proposed. Total New Development Sales (in Billions) $14B $12B $10.3B New development sales $10B totaled $5.4 billion last year, $8.4B up significantly from the $4.1 $8B billion in sales recorded in 2014. -

Review Session Disposition- June 11, 2018

Page 1 CITY PLANNING COMMISSION/REVIEW SESSION June 11, 2018 @ 1:00 P.M. ULURP Number(s) Description of Request(s) D I S P O S I T I O N Presentation Presentation by the New York City Department of Homeless Services on their process for siting facilities. DISCUSSED Manhattan Non-ULURP Referral 1 N180373 ZRM Garment Center Text Amendment; zoning text amendment. (M4,5) REFER TO COMMUNITY BOARD AND BOROUGH PRESIDENT FOR 60 DAYS Manhattan Certification 2 180290 ZSM 9 Orchard Street; special permit. (M3) CERTIFIED Brooklyn Certification 3 180347 ZMK Franklin Avenue Rezoning; zoning map and zoning text amendments. (K9) N180348 ZRK CERTIFIED Queens Certification 4 180174 ZMQ St. Michael’s Park Elimination; zoning map and city map amendments. (Q1) 180175 MMQ CERTIFIED Bronx Certification 5 180391 PQX 599 Courtlandt Avenue; acquisition, UDAAP designation, project approval and 180390 HAX disposition of c-o-p. (X1) CERTIFIED Bronx Pre-Hearing 6 C150314 PQX LSSNY Early Life Bronxworks Innovative Senior Center; acquisition. (X5) (7/30) TO PUBLIC HEARING ON 6 / 13 / 18 Queens Non-ULURP Post Referral 7 N180279 CMQ 90-10 Ditmars Boulevard Restrictive Declaration; modification to a previously approved restrictive declaration. (Q3) APPROVED; SEND LETTER TO BUILDINGS DEPARTMENT Manhattan Pre-Hearing 8 C180249 HAM Balton Commons; UDAAP designation, project approval and disposition of c-o-p. (M10) (7/23) TO PUBLIC HEARING ON 6 / 13 / 18 Brooklyn Pre-Hearings 9 C180148 ZMK 1601 Dekalb Avenue Rezoning; zoning map and zoning text amendments. N180149 ZRK (K4) (7/23) TO PUBLIC HEARING ON 6 / 13 / 18 {COMMISSIONER DOUEK; RECUSED} 10 C180216 ZMK 80 Flatbush Avenue; zoning map, zoning text amendments and special permit. -

Ijiu a Tb P (Him Es Treatment Plant Will Cost $3.12 Million

A Weekly Newspaper Is Close To The People ijiU atbp (Himes 15 ESTABLISHED 1924 OFFICIAL NEWSPAPER OF THE TOWNSHIP AND SCHOOL DISTRICT OF HILLSIDE VOL. XLVIII, NO. 45 HILLSIDE, NEW JERSEY, THURSDAY, SEPTEMBER 7,1972 Treatment Plant Will Cost $3.12 Million A $3.12 million bonding to share In the cost of con benefits. Employee coverage ^ In the township. Installation of New Jersey State League of ordinance for the construction of structing the - planned facility. der medical - surgical, major a traffic light' at, the,intersec Municipalities in Atlantic City a secondary sewage treatment Kulish said that Elizabeth Is medical and hospitalization in tion of Nr Broad St., Central' from November 14 to 17 with plant was introduced at the town not now a member of the Joint surance would be extended to all Ave. and Evans Terminal was reimbursement to each one at a fUlF’U'ytime employees, both ship committee meeting Tuesday Meeting, which has been In exis also proposed. maximum rate of $35 per day. evening to provide what Commis tence since June 1, 1926. Eliza temporary and permanent after All of the. ordinances Intro --Approved the action of the ’ 60 days employment, by one sioner Albert S. Parsonnet called beth, now buys the services of duced will come up for public police chief in assigning Ptlm. ordinance. "the most effective sewage the existing sewage treatment hearing and final adoption at Alois Stier to attend a twelve- treatment available." plant and would like to continue Two others deal with salary the township committee meeting day criminal investigation Increases for the police depart The 40-year bond Is Hillside’s this arrangement for the on September 19. -

May 14, 2021 Dear Governor Lamont, Senator Looney, Senator Duff, Speaker Ritter, Representative Rojas, Senator Kelly

May 14, 2021 Governor Ned Lamont Representative Jason Rojas Office of the Governor House Majority Leader 210 Capitol Avenue Legislative Office Building, Room 4100 Hartford, CT 06106 Hartford, CT 06106 Senator Martin Looney Senator Kevin Kelly President Pro Tempore Senate Minority Leader Legislative Office Building, Room 3300 Legislative Office Building, Room 3400 Hartford, CT 06106 Hartford, CT 06106 Senator Bob Duff Representative Vincent Candelora Senate Majority Leader House Minority Leader Legislative Office Building, Room 3300 Legislative Office Building, Room 4200 Hartford, CT 06106 Hartford, CT 06106 Representative Matt Ritter Speaker of the House Legislative Office Building, Room 4106 Hartford, CT 06106 Dear Governor Lamont, Senator Looney, Senator Duff, Speaker Ritter, Representative Rojas, Senator Kelly, and Representative Candelora, We, the 104 undersigned clergy, stand in support of the Education Justice Now campaign and FaithActs for Education, which represents 6,000 committed voters and 11,000 congregants across the state. We are writing to urge you to end our state’s racist education funding system and give our children the funding they deserve. Specifically, we ask you to use your power as leaders to: ● Secure $10 million additional dollars for education across Bridgeport, Hartford, New Haven, Waterbury, and New Britain in the current biennial budget; and ● In the next legislative session, pass antiracist legislation to close Connecticut’s racial funding gap by the time federal dollars run out. As leaders, you are called by God to “do right, seek justice, defend the oppressed” (Isaiah 1:17). But when you fund education based on property taxes, draw lines to keep Black and Brown people out of districts with the best resources, and spend $639 million more on majority white districts, we ask you: How far is Connecticut from whites-only drinking fountains and segregated lunch counters? This racial funding gap is immoral, unjust, and unacceptable. -

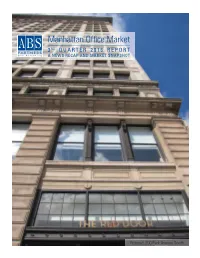

Manhattan Office Market

Manhattan Off ce Market 3 RD QUARTER 2016 REPORT A NEWS RECAP AND MARKET SNAPSHOT Pictured: 200 Park Avenue South Looking Ahead Tax Plan Proposal Could Potentially Help Leveraged RE Firms An emerging tax plan proposed by Republican candidate Donald Trump could reportedly benef t debt-laden real estate companies by coupling 2-policies — letting businesses deduct interest and allowing expensing, or immediate write-offs, for investments in equipment and buildings. The proposal would “provide negative tax rates for investments f nanced with debt, creating incentives for companies to pursue projects that wouldn’t make sense economically without the tax benef ts.” Currently tax law requires businesses to spread the deductions over multiple years, but under Trump’s proposed plan “a business would be able to generate signif cant losses in the f rst year of an investment and then generate ongoing interest deductions. Those losses could be carried forward and used to offset future income.” It is reportedly the intended goal of the tax plan, which is still a work-in-progress, to “tie expensing to job creation and new investment and not, for example, purchases of existing leveraged real estate portfolios,” according to reported comments by a Trump advisor. Interest Deductions: The pairing of an end to interest deductions and expensing is typically done to prevent giving an extra subsidy according to some sources, however it is anticipated that the taking away of interest deductibility would make it hard for businesses to capitalize; and with that in mind Trump had proposed an unspecif ed “reasonable cap” in an earlier proposed tax plan. -

“EB-5 Project Database: 2017 Supplement with Trends and Observations”

“EB-5 Project Database: 2017 Supplement with Trends and Observations” By: Scholar-in-Residence Gary Friedland and Professor Jeanne Calderon NYU Stern School of Business August 16, 2017 DRAFT Copyright 2017 Gary Friedland and Jeanne Calderon 1 Table of Contents I Introduction ................................................................................................................................................ 3 II Methodology .............................................................................................................................................. 4 1. Sources .............................................................................................................................................. 4 2. Format ............................................................................................................................................... 4 3. Projects selected for inclusion in this 2017 Database ...................................................................... 5 III Trends and Observations .......................................................................................................................... 6 1. The growing presence of Chinese developers in EB-5 projects ........................................................ 6 2. Megaprojects continue to dominate ................................................................................................ 9 3. Many of the largest developers continue to utilize EB-5 capital .................................................... 11 4. -

4.5 MILLION SF Surpassed 2016’S Total

OFFICE RETAIL TOURISM & HOSPITALITY RESIDENTIAL MAJOR PROJECTS UPDATE ALLIANCE FOR DOWNTOWN NEW YORK LOWER MANHATTAN REAL ESTATE MARKET REPORT Q3 2017 LOWER MANHATTAN ON TRACK FOR STRONG YEAR END FINISH LOWER MANHATTAN LEASING ACTIVITY SURPASSES 2016 TOTAL IN THIRD QUARTER Lower Manhattan logged another positive quarter in 2017, positioning the market for its best year since 2014. The Lower Manhattan’s commercial office market is experiencing its area’s vacancy rate dropped for the third consecutive strongest year since 2014 and continued to perform well in the quarter making Lower Manhattan the 15th tightest third quarter. Activity was up 20 percent over last quarter. Lower submarket nationwide, according to Cushman & Wakefield. Manhattan logged 1.43 million square feet of new activity in Lower Manhattan’s status as the third quarter, bringing the year-to-date volume to 4.5 million a media mecca reached new square feet. According to CBRE, heights with ESPN Studios’ year-to-date activity has already announced relocation to the 4.5 MILLION SF surpassed 2016’s total. Seaport District’s Pier 17, as well as Macmillan Publishers’ Highest YTD Leasing Activity While leasing activity is up year-over-year Manhattan-wide, commitment to relocate its since 2014 headquarters from the Flatiron Lower Manhattan’s 56 percent Building to 120 Broadway. year-over-year jump far outpaces Investment activity in the office market is higher than 2016 other market’s performance as compared to this time last year. activity, with several large deals demonstrating investors’ Midtown activity is up 20 percent, bolstered by strong activity at positive outlook on the market.