Wine Market Profile

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

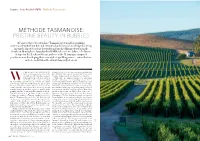

Méthode Tasmanoise

feature / Anne Krebiehl MW / Méthode Tasmanoise MÉTHODE TASMANOISE: PRISTINE BEAUTY IN BUBBLES It’s a mere three decades since Tasmania’s potential for sparkling wine was identified, but the cool, remote island is now acknowledged as being among the finest locations for traditional-method fizz production in the Southern Hemisphere. Anne Krebiehl MW takes a tour of this cool-climate hotspot in the Southern Ocean, and meets the Champagne-inspired producers now developing their own style of sparkling wines—wines that are as fresh and vivid as the island’s famously clean air indswept, remote, and totally brisk, the produced is in the niche premium wine sector retailing above island of Tasmania seems almost like $15 equivalent. This segment represents just 7 percent of an antithesis of the Australian mainland. Australia’s total wine production, but 28 percent of its value.” Surrounded by the cold, deep waters of While there are numerous instances of 19th-century the Southern Ocean, there is nothing viticulture in Tasmania, even of sparkling-wine production, Wbut sea between it and Antarctica. For decades, the weather none of the plantings survived.3 It was not until the late 1960s station at Cape Grim on its northwestern edge has measured and mid-1970s that Tasmania was rediscovered for viticulture, the cleanest air in the world. Yes, “Tassie” is as clean, as fresh, and another decade before the potential for sparkling wine as vivid as the wines that originate there. It is among not just was crystallized. While grapes for sparkling wines are sourced Australia’s but the world’s best regions for making quality from across the island, the northerly regions of Tamar Valley sparkling wine. -

San Francisco & New York City 2018 Event Wrap Up

San Francisco & New York City 2018 Event Wrap Up After a week of intensive conversations and visits with more than 160 sommeliers, wine buyers and media in San Francisco and New York, I am more optimistic than ever about the opportunities for Australian wine in one of the world’s most important markets. The US is currently at a crucial juncture at which the reputation and popularity of Australian wine is slowly but decisively on the rise, though a lot more work is required to realise its real potential. At a time when Australia’s export opportunities and growth in China are all the buzz, Wolf Blass commented to WBM’s Anthony Madigan recently that we should be getting more excited about the USA than China. That’s a big call, but this much is clear to me: Australia’s historical precedent and deep cultural ties with the US provide an opportunity far more promising than has ever been realised. In sparkling wine, for instance, the USA is the world’s biggest and fastest growing importer, responsible for landing more than 15 million cases of sparkling wine last year, and growing at almost 5% per annum. This market offers tremendous opportunity that Australia has failed to realise. Australia accounted for just 81,000 cases of last year’s volume. Australia produces 3% of the world’s sparkling wine yet supplies just 0.5% of US imports. Alarmingly, Australia’s sparkling white exports to the US have halved in the past five years. Australian wine in the US is no longer all about cheap and cheerful critter wines on the one hand and big, bold flagship shiraz on the other. -

HOUSE of ARRAS EJ Carr Late Disgorged 2003

HOUSE OF ARRAS EJ Carr Late Disgorged 2003 Arras EJ. Carr Late Disgorged Sparkling Chardonnay Pinot Noir pays tribute to the dedication and inspiration of its maker, EJ. Carr. As the pinnacle of the House of Arras, the EJ. Carr Late Disgorged is a wine of great intensity and character, with excellent structural elegance and flavour persistence. After at least 10 years on lees the wine has amazing complexity and yet retains the remarkable freshness of the character typical of a world class prestige cuvée. A true expression of Tasmanian terroir and impeccable winemaking - the 2003 vintage is the sixth release of this wine. VINTAGE The season remained warm and very dry from September to the end of February which, combined with moderate crop yields, promoted early ripening with the generosity of a temperate year. This was somewhat moderated by much cooler and wet weather from mid-March through which maturation slowed and natural acidity was retained. The fruit for this wine was harvested in excellent condition from sites less affected by the inclement weather and the wine retains the characteristics generated by the warmth of the early season. WINEMAKING Crafted with all the best winemaking and viticultural methods, including whole bunch pressing, primary fermentation on light grape solids & 100% malolactic fermentation of base wines to add sophistication and structure. Meticulous blending of only the best parcels of Tasmanian fruit and at least 10 years on lees has ensured this wine shows amazing complexity and yet continues to retain the remarkable freshness expected of a typical world-class prestige cuvée. -

Wine Industry Tasmania Ltd 147 Davey Street, Hobart TAS 7000 Phone: 03 6223 3770 Email: [email protected]

WINE TASMANIA SUBMISSION TO THE AUSTRALIAN GOVERNMENT’S TAX DISCUSSION PAPER May 2015 Submitted By: Sheralee Davies Chief Executive Officer Wine Industry Tasmania Ltd 147 Davey Street, Hobart TAS 7000 Phone: 03 6223 3770 Email: [email protected] Introduction The Tasmanian wine sector is an important and growing contributor to trade and the economy, regional employment, tourism and the overall Tasmanian brand. The quality of Tasmanian wine is increasingly being recognised around the world, including through independent endorsements, wine show results and sales, and the Tasmanian wine region is regarded as one of the strongest in the country. The Tasmanian wine sector has developed a strong, clear and collaborative position in the wine world, built on quality and value. Tasmania has emerged as one of the strongest wine regions with an opportunity to lead and drive the new wave of interest in Australian wine. Contrary to many other Australian wine regions, demand for Tasmanian wine continues to outstrip supply, and strong growth is occurring in the Tasmanian wine sector, including through the attraction of external investment. This response to the Australian Government’s Tax Discussion Paper focuses on the taxation treatment of wine on behalf of the island’s wine producers. Wine Tasmania confirms its support for retaining the value-based system of taxation on wine, together with the rebate, and only in conjunction with the rebate. Within Tasmania, the Wine Equalisation Tax (WET) rebate is being utilised as was originally intended - to support small wine producers / cellar doors making a significant contribution to Australia’s regional communities. Increasing net taxes paid by Tasmanian wine producers would severely impact on this developing high quality and value sector, which is increasing being recognised around the world. -

Tasmanian Wines

Tasmanian Wines Tasmania’s temperate climate nurtures plump chardonnay, pinot noir, gewürtztraminer and riesling grapes. These cool-climate varieties are the island’s specialty as the conditions are similar to Burgundy in France. Tassie’s impressive wine CV is strengthened by a touch of sparkle: Tasmanian grapes also give the zeitgeist to some of Australia’s best bubbly (sparkling wines). Some of Australia’s finest pinot noirs have their provenance on the island. Without a hint of braggadocio Tassie’s friendly, plain speaking vineyard owners, wine makers and cellar door folk will tell you themselves. But if you need more evidence of Tasmania’s wine kudos you could soak this up: Tamar Ridge’s sauvignon blanc was named the best of its type in the world by the UK’s Decanter magazine. Jansz Methode Tasmanoise® Jansz Tasmania is one of few Tasmanian specialist vineyards. It is solely devoted to sparkling winemaking and has described the technique used in creating their wines as Méthode Tasmanoise®. The winery was established in 1985 as a joint venture between Heemskerk Vineyards and famous Champagne house Louis Roederer. The Hill Smith family acquired Jansz in 1997 and the brand was re-born Jansz Tasmania. Jansz Tasmania’s Wine Room and Vineyard lies in a small north-eastern corner of Tasmania known as ‘Sparkling Tasmania’. Nestled in the heart of Pipers River region, Jansz Tasmania can be found by following the Northern Tasmanian Wine Route, circling the Tamar Valley and river. www.jansztas.com Tamar Ridge Tasmania Tamar Ridge has forged a reputation as one of the state’s finest wine producers and has gained international recognition for its sauvignon blanc, riesling, chardonnay and pinot noir. -

Tasmania Wine

THE ULTIMATE GUIDE TO TASMANIA WINE Learn all about the island state’s wine community and the cool-climate elegance of its most famous varieties. CONTENTS – The history of Tasmania – Geography, climate and soil – Viticulture and winemaking – Prominent varieties Cover: Jennifer Doyle, Jansz, Tasmania NORTHERN TERRITORY AUSTRALIA QUEENSLAND WESTERN AUSTRALIA SOUTH AUSTRALIA NEW SOUTH WALES VICTORIA 0 500 TASMANIA Kilometres PIPERS BROOK DEVONPORT PipER s RivER North Wes t LAUNCESTON TaMA r V a LL ey BICHENO TASMANIA E as t C oas t Coal RivER V a LL ey DER wen t RICHMOND V a LL ey HOBART H u ON / ch ann el CYGNET The ultimate guide to Tasmania wine TASMANIA: TINY ISLAND, BIG PRESENCE Celebrated as one of Australia’s finest cool-climate wine-growing areas, Tasmania is turning heads as one of the world’s premier wine regions. - Small, isolated island at the south-eastern tip of Australia - Cool climate and diverse, unique terroirs - Ideal conditions for Chardonnay, Pinot Noir and sparkling wines - Booming food and wine tourism industry TASMANIA: Tasmania has found its way to centre stage TINY ISLAND, BIG PRESENCE thanks to its wonderful collection of cool- Tasmania is a small island state off the climate wines that are proving themselves south-eastern tip of Australia. The climate worthy among the world’s finest. and soils of the region combine to create With its pristine and picturesque ideal growing conditions for developing environment, cool climate and fine-food naturally elegant, intensely flavoured and scene, Tasmania is also one of Australia’s aromatic wines, with Chardonnay and leading tourist destinations, and the Pinot Noir the region’s most renowned brilliant Tasmanian wine and grape varieties. -

Wine Tasmania Strategic Plan 2021-23

STRATEGy 2021–2023 RELEASED: APRIL 2021 OUR VISION: To build Tasmania’s reputation as a cool wine region like no other on the planet, with demand for its wines continuing to exceed production. Contents Introduction.................... 3 Our strategies................ 7–9 Measures of success............. 4 About Wine Tasmania............ 10 About the Tasmanian Key stakeholders............... 13 wine sector..................... 5 Managing Wine Tasmania Why is Tasmania so awesome?..... 6 successfully................... 14 INTRODUCTION The Tasmanian wine sector is a significant and growing contributor to the state’s economy, regional employment, agriculture, manufacturing, tourism, hospitality and the overall Tasmanian brand. Wine Tasmania’s Strategy 2021-23 is focused on maximising the opportunities for Tasmanian wine producers, driving the demand, value and increasing price points of Tasmanian wine, and supporting the profitability of individual wine businesses. While always maintaining a long-term focus, Covid-19 has negatively impacted the Tasmanian wine sector. Wine Tasmania’s Strategic Plan therefore reflects changing priorities to best support wine producers to recover and contribute to future success. OUR Strategies 1 >> Proactively pursue opportunities to communicate, position and promote the unique Tasmanian wine story and drive market-led growth. 2 >> Progress Tasmania’s reputation as a differentiated wine producing and visitor destination. 3 >> Inspire, support, educate and assist Tasmanian wine producers to grow their business -

For Fish to Taste Good It Needs to Swim Three Times in the Sea, in Butter and Finally in Wine

For fish to taste good it needs to swim three times in the sea, in butter and finally in wine. Polish proverb – one of George Mure’s favourites! Since the opening of Mures Fish House in Battery Point in 1973, the Mure Family have been proud supporters of local produce. Today, some 40 years later, our beverage selection has an emphasis on some of the best of Tasmania’s wine, beer and most recently spirit industries. We round our beverage list off with a selection from Mainland Australia and imported offerings from both the old and new world of winemakers. Table of Contents Cocktail List 3 Beers & Ciders 4 George Mure Range 5 Wine by the Glass 6 Cellar Bin Ends & Small Format Bottles 7 Reserve Selection – Champagne & Sparkling 8 Reserve Selection – White Wine 9 Reserve Selection – Red Wine 10 Reserve Selection – Imports & Super Premium 11 Sparkling – Non Vintage 12 Sparkling – Vintage 13 Riesling 14 Pinot Gris/Grigio 15 Sauvignon Blanc 16 Chardonnay 17 White Varietals 18 Pinot Noir 19 Merlot 20 Cabernet Sauvignon & Blends 21 Shiraz/Syrah 22 Red Varietals 23 Rosé 24 Dessert Wine 25 Spirits, Digestives & Liqueurs 26 Non Alcoholics & Organic Tea Selection 29 2 Cocktail List Ginger ‘Hammer’ Yule $24 Starring Belgrove Ginger Hammer teamed with spiced rum, triple sec, fresh lime & a dash of lemonade, it is the perfect way to unwind from the day & slip into the evening. Spritz Con Aperol $18 A classic Italian aperitivo, with Prosecco & Aperol it will refresh you at a glance, a great way to get your taste buds working, it is bitter, sweet & addictive. -

Meiningers Tasmania

REGIONAL ANALYSIS THE SPARKLING ISLE 6/14 MEININGER’S WBI 6/14 MEININGER’S Tasmania produces a mere half of one per cent of all Australian wine, yet the island state is increasingly being seen as a world-class location for sparkling wine. Stephen Quinn reports. he island of Tasmania, Australia’s south- ernmost state, was discovered by Dutch Pipers Brook winery Texplorer Abel Janszoon Tasman in Novem- ber 1642. Tasman, who is also credited as hav- ing discovered New Zealand and Fiji, is said to have been driven onto the west coast by a storm. His ship, the Heemskerk, gave its name to Tas- mania’s first modern winery, founded 124 years later, while his middle name lives on in the suc- cessful Jansz sparkling wine produced there. Tasmania was one of the first Australian regions to be planted with vines, and a bottle his Chardonnay, Pinot Noirs and Rieslings first surplus to table wine requirements”. of Tasmanian wine was presented at a Paris caught the attention of Australian, and then The shift to sparkling wine helps to explain exhibition in 1848, a few years before wines overseas, critics. how, while Tasmania produces only half of 1% from the Hunter Valley were to win acclaim at The fact that these modern pioneers only of all the wine made in Australia, it sells 6% the a similar Parisian event. Despite the auspicious began to produce wine in the 1970s helps to ultra-premium end of the market. As Carr says, beginning, Tasmanian winemaking languished explain why most of Tasmania’s vines are under “Tasmania has become very noticed globally; for more than a century, until Graham Wiltshire two decades old and the total area under vines Tasmanian sparkling is in the Australian media established the Heemskirk vineyard in 1966. -

2009 AWRI Annual Report 2009 45 Financial Report – Director’S Report

www.awri.com.au BOARD MEMBERS THE COMPANY The AWRI’s laboratories and offices are housed in the Wine Innovation Central Building of the Dr J.W. Stocker AO BMedSc, MBBS, PhD, FRACP, FTSE The Australian Wine Research Institute Ltd was incor- Wine Innovation Cluster (WIC). The WIC is located Chairman–Elected a member under Clause 25.2(d) porated on 27 April 1955. It is a company limited by within an internationally renowned research of the Constitution (from 1 January 2009) guarantee that does not have a share capital. cluster on the Waite Precinct at Urrbrae in the Adelaide foothills, on land leased from The Mr J.F. Brayne, BAppSc(Wine Science) The Constitution of The Australian Wine Research University of Adelaide. Collocated in the Wine Elected a member under Clause 25.2(d) Institute Ltd (AWRI) sets out in broad terms the Innovation Central Building with the AWRI is of the Constitution (from 1 January 2009) aims of the AWRI. In 2006, the AWRI implemented grape and wine scientists from The University of its ten-year business plan Towards 2015, and stated Adelaide and the South Australian Research and Mr P.D. Conroy, LLB(Hons), BCom its purpose, vision, mission and values: Development Institute. The parties in the Wine Elected a member under Clause 25.2(c) Innovation Cluster, who are accommodated over of the Constitution Purpose three buildings, include also CSIRO Plant Industry To contribute substantially in a measurable way to and Provisor Pty Ltd. Mr P.J. Dawson, BSc, BAppSc(Wine Science) the ongoing success of the Australian grape and Elected a member under Clause 25.2(d) wine sector Along with the WIC parties mentioned, the of the Constitution AWRI is clustered with the following research Vision and teaching organisations: Australian Centre Mr G.R. -

The Perfect Location for Producing Premium Cool-Climate Wines

Tasmania Delivers... The perfect location for producing premium cool-climate wines Tasmania is Australia’s finest cool-climate wine producing region, Tasmania's wine industry is enjoying solid and sustainable growth, already recognised for award-winning Pinot Noir, sparkling wine, with recent investments and awards confirming the state’s position Chardonnay and Riesling. as a premium cool-climate wine region. With a focus on market-led growth, Tasmania's wine sector Despite demonstrable geographic and style variations in viticultural has been steadily growing over the past ten years. It currently areas across the island, Tasmania remains the only Australian represents 1% of Australia's wine production by volume but statewide zone in its own right. This single Geographic Indication more than 4% of its total value. The Tasmanian wine industry is (GI) gives Tasmanian producers the advantage of a united small and dynamic with great potential for growth. The state has marketing approach, and the wide recognition of Tasmania as a a well-earned reputation, both nationally and internationally, for brand in national and international markets. producing premium cool-climate wines. The wine industry has excellent growth prospects. The Tasmanian With a cool climate and long, sunny and dry autumns, Tasmania Government is keen to work with potential investors to secure value- has ideal growing conditions for premium wines. Pinot Noir and adding investment for the wine industry within the state.Through Chardonnay in particular have done well, although other early the Office of the Coordinator-General, the government will tailor ripening varieties have proven suitable for planting. assistance to suit the specific requirements of potential investors. -

Tasmania Facilitator Guide Australian Wine Discovered Education Program

TASMANIA FACILITATOR GUIDE AUSTRALIAN WINE DISCOVERED EDUCATION PROGRAM The comprehensive, free education program providing information, tools and resources to discover Australian wine. To access course presentation, videos and tasting tools, as well as other programs, visit Wine Australia www.australianwinediscovered.com supports the responsible service of alcohol. For enquiries, email [email protected] TASMANIA Jansz, Tasmania Jansz, Jennifer Doyle, Jennifer Australia’s unique climate and landscape have fostered a fiercely independent wine scene, home to a vibrant community of growers, winemakers, viticulturists, and vignerons. With more than 100 grape varieties grown across 65 distinct wine regions, we have the freedom to make exceptional wine, and to do it our own way. We’re not beholden by tradition, but continue to push the boundaries in the pursuit of the most diverse, thrilling wines in the world. That’s just our way. Tasmania / Facilitator guide TASMANIA: TINY ISLAND, BIG PRESENCE Celebrated as one of Australia’s finest cool-climate wine-growing areas, Tasmania is turning heads as one of the world’s premier wine regions. - Small, isolated island at the south-eastern tip of Australia - Cool climate and diverse, unique terroirs - Ideal conditions for Chardonnay, Pinot Noir and sparkling wines - Booming food and wine tourism industry FIRST TASTE advantages of a naturally pristine, cool-climate environment. THIS MAY BE A GOOD Until relatively recently, this small, isolated OPPORTUNITY TO GIVE island was an overlooked piece in the EVERYONE A TASTE OF A Australian wine puzzle. An outlier both physically and in terms of perception, CLASSIC TASMANIAN WINE. Tasmania spent years quietly going about THE FULL TASTING COMES its business with only a few big-name LATER IN THE PROGRAM.