Short Communication on the Tunisian Exchange Regime a Decade After the Revolution

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

What Future of the Tunisian Dinar Against the Euro? Prediction with the ARIMA Model

Munich Personal RePEc Archive What future of the Tunisian dinar against the euro? Prediction with the ARIMA model GRITLI, Mohamed Ilyes Université de Tunis El Manar, Faculté des Sciences Economiques et de Gestion de Tunis, Université de Pau et des Pays de l’Adour (UPPA), CATT, 64016 Pau, France 15 January 2018 Online at https://mpra.ub.uni-muenchen.de/83937/ MPRA Paper No. 83937, posted 15 Jan 2018 14:20 UTC Quel avenir du dinar tunisien face à l'euro ? Prévision avec le modèle ARIMA MOHAMED ILYES GRITLI Université de Tunis El Manar, Faculté des Sciences Economiques et de Gestion de Tunis, Laboratoire d’Intégration Économique Internationale, 2092 Tunis, Tunisie Université de Pau et des Pays de l’Adour (UPPA), CATT, 64016 Pau, France [email protected] Résumé: L'Union européenne absorbe près de 75% des exportations tunisiennes et représente environ 50% des importations tunisiennes, ce qui explique le poids important de l’euro dans le panier d’ancrage du dinar tunisien. Ainsi, l’objet de cet article consiste à prédire les fluctuations du taux de change EUR/DNT à court terme, en utilisant le modèle ARIMA (0,1,1). Les résultats montrent qu’une unité d’euro sera échangée contre 3.05126 dinars (modèle sans rupture) et contre 3.22409 dinars (modèle avec rupture), pour le mois d’octobre 2018. Cela suggère que le degré de dépréciation du dinar va dépendre de la politique menée par la Banque Centrale de Tunisie. Summary: The European Union absorbs nearly 75% of Tunisian exports and represents about 50% of Tunisian imports, which explains the important weight of the euro in the Tunisian dinar anchor basket. -

Countries Codes and Currencies 2020.Xlsx

World Bank Country Code Country Name WHO Region Currency Name Currency Code Income Group (2018) AFG Afghanistan EMR Low Afghanistan Afghani AFN ALB Albania EUR Upper‐middle Albanian Lek ALL DZA Algeria AFR Upper‐middle Algerian Dinar DZD AND Andorra EUR High Euro EUR AGO Angola AFR Lower‐middle Angolan Kwanza AON ATG Antigua and Barbuda AMR High Eastern Caribbean Dollar XCD ARG Argentina AMR Upper‐middle Argentine Peso ARS ARM Armenia EUR Upper‐middle Dram AMD AUS Australia WPR High Australian Dollar AUD AUT Austria EUR High Euro EUR AZE Azerbaijan EUR Upper‐middle Manat AZN BHS Bahamas AMR High Bahamian Dollar BSD BHR Bahrain EMR High Baharaini Dinar BHD BGD Bangladesh SEAR Lower‐middle Taka BDT BRB Barbados AMR High Barbados Dollar BBD BLR Belarus EUR Upper‐middle Belarusian Ruble BYN BEL Belgium EUR High Euro EUR BLZ Belize AMR Upper‐middle Belize Dollar BZD BEN Benin AFR Low CFA Franc XOF BTN Bhutan SEAR Lower‐middle Ngultrum BTN BOL Bolivia Plurinational States of AMR Lower‐middle Boliviano BOB BIH Bosnia and Herzegovina EUR Upper‐middle Convertible Mark BAM BWA Botswana AFR Upper‐middle Botswana Pula BWP BRA Brazil AMR Upper‐middle Brazilian Real BRL BRN Brunei Darussalam WPR High Brunei Dollar BND BGR Bulgaria EUR Upper‐middle Bulgarian Lev BGL BFA Burkina Faso AFR Low CFA Franc XOF BDI Burundi AFR Low Burundi Franc BIF CPV Cabo Verde Republic of AFR Lower‐middle Cape Verde Escudo CVE KHM Cambodia WPR Lower‐middle Riel KHR CMR Cameroon AFR Lower‐middle CFA Franc XAF CAN Canada AMR High Canadian Dollar CAD CAF Central African Republic -

WM/Refinitiv Closing Spot Rates

The WM/Refinitiv Closing Spot Rates The WM/Refinitiv Closing Exchange Rates are available on Eikon via monitor pages or RICs. To access the index page, type WMRSPOT01 and <Return> For access to the RICs, please use the following generic codes :- USDxxxFIXz=WM Use M for mid rate or omit for bid / ask rates Use USD, EUR, GBP or CHF xxx can be any of the following currencies :- Albania Lek ALL Austrian Schilling ATS Belarus Ruble BYN Belgian Franc BEF Bosnia Herzegovina Mark BAM Bulgarian Lev BGN Croatian Kuna HRK Cyprus Pound CYP Czech Koruna CZK Danish Krone DKK Estonian Kroon EEK Ecu XEU Euro EUR Finnish Markka FIM French Franc FRF Deutsche Mark DEM Greek Drachma GRD Hungarian Forint HUF Iceland Krona ISK Irish Punt IEP Italian Lira ITL Latvian Lat LVL Lithuanian Litas LTL Luxembourg Franc LUF Macedonia Denar MKD Maltese Lira MTL Moldova Leu MDL Dutch Guilder NLG Norwegian Krone NOK Polish Zloty PLN Portugese Escudo PTE Romanian Leu RON Russian Rouble RUB Slovakian Koruna SKK Slovenian Tolar SIT Spanish Peseta ESP Sterling GBP Swedish Krona SEK Swiss Franc CHF New Turkish Lira TRY Ukraine Hryvnia UAH Serbian Dinar RSD Special Drawing Rights XDR Algerian Dinar DZD Angola Kwanza AOA Bahrain Dinar BHD Botswana Pula BWP Burundi Franc BIF Central African Franc XAF Comoros Franc KMF Congo Democratic Rep. Franc CDF Cote D’Ivorie Franc XOF Egyptian Pound EGP Ethiopia Birr ETB Gambian Dalasi GMD Ghana Cedi GHS Guinea Franc GNF Israeli Shekel ILS Jordanian Dinar JOD Kenyan Schilling KES Kuwaiti Dinar KWD Lebanese Pound LBP Lesotho Loti LSL Malagasy -

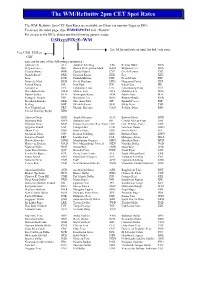

WM/Refinitiv 2Pm CET Spot Rates

The WM/Refinitiv 2pm CET Spot Rates The WM/ Refinitiv 2pm CET Spot Rates are available on Eikon via monitor Pages or RICs. To access the index page, type WMRESPOT01 and <Return> For access to the RICs, please use the following generic codes : USDxxxFIXzE=WM Use M for mid rate or omit for bid / ask rates Use USD, EUR or GBP xxx can be any of the following currencies : Albania Lek ALL Austrian Schilling ATS Belarus Ruble BYN Belgian Franc BEF Bosnia Herzegovina Mark BAM Bulgarian Lev BGN Croatian Kuna HRK Cyprus Pound CYP Czech Koruna CZK Danish Krone DKK Estonian Kroon EEK Ecu XEU Euro EUR Finnish Markka FIM French Franc FRF Deutsche Mark DEM Greek Drachma GRD Hungarian Forint HUF Iceland Krona ISK Irish Punt IEP Italian Lira ITL Latvian Lat LVL Lithuanian Litas LTL Luxembourg Franc LUF Macedonia Denar MKD Maltese Lira MTL Moldova Leu MDL Dutch Guilder NLG Norwegian Krone NOK Polish Zloty PLN Portugese Escudo PTE Romanian Leu RON Russian Rouble RUB Slovakian Koruna SKK Slovenian Tolar SIT Spanish Peseta ESP Sterling GBP Swedish Krona SEK Swiss Franc CHF New Turkish Lira TRY Ukraine Hryvnia UAH Serbian Dinar RSD Special Drawing Rights XDR Algerian Dinar DZD Angola Kwanza AOA Bahrain Dinar BHD Botswana Pula BWP Burundi Franc BIF Central African Franc XAF Comoros Franc KMF Congo Democratic Rep. Franc CDF Cote D’Ivorie Franc XOF Egyptian Pound EGP Ethiopia Birr ETB Gambian Dalasi GMD Ghana Cedi GHS Guinea Franc GNF Israeli Shekel ILS Jordanian Dinar JOD Kenyan Schilling KES Kuwaiti Dinar KWD Lebanese Pound LBP Lesotho Loti LSL Malagasy Ariary -

FAO Country Name ISO Currency Code* Currency Name*

FAO Country Name ISO Currency Code* Currency Name* Afghanistan AFA Afghani Albania ALL Lek Algeria DZD Algerian Dinar Amer Samoa USD US Dollar Andorra ADP Andorran Peseta Angola AON New Kwanza Anguilla XCD East Caribbean Dollar Antigua Barb XCD East Caribbean Dollar Argentina ARS Argentine Peso Armenia AMD Armeniam Dram Aruba AWG Aruban Guilder Australia AUD Australian Dollar Austria ATS Schilling Azerbaijan AZM Azerbaijanian Manat Bahamas BSD Bahamian Dollar Bahrain BHD Bahraini Dinar Bangladesh BDT Taka Barbados BBD Barbados Dollar Belarus BYB Belarussian Ruble Belgium BEF Belgian Franc Belize BZD Belize Dollar Benin XOF CFA Franc Bermuda BMD Bermudian Dollar Bhutan BTN Ngultrum Bolivia BOB Boliviano Botswana BWP Pula Br Ind Oc Tr USD US Dollar Br Virgin Is USD US Dollar Brazil BRL Brazilian Real Brunei Darsm BND Brunei Dollar Bulgaria BGN New Lev Burkina Faso XOF CFA Franc Burundi BIF Burundi Franc Côte dIvoire XOF CFA Franc Cambodia KHR Riel Cameroon XAF CFA Franc Canada CAD Canadian Dollar Cape Verde CVE Cape Verde Escudo Cayman Is KYD Cayman Islands Dollar Cent Afr Rep XAF CFA Franc Chad XAF CFA Franc Channel Is GBP Pound Sterling Chile CLP Chilean Peso China CNY Yuan Renminbi China, Macao MOP Pataca China,H.Kong HKD Hong Kong Dollar China,Taiwan TWD New Taiwan Dollar Christmas Is AUD Australian Dollar Cocos Is AUD Australian Dollar Colombia COP Colombian Peso Comoros KMF Comoro Franc FAO Country Name ISO Currency Code* Currency Name* Congo Dem R CDF Franc Congolais Congo Rep XAF CFA Franc Cook Is NZD New Zealand Dollar Costa Rica -

List of Currencies of All Countries

The CSS Point List Of Currencies Of All Countries Country Currency ISO-4217 A Afghanistan Afghan afghani AFN Albania Albanian lek ALL Algeria Algerian dinar DZD Andorra European euro EUR Angola Angolan kwanza AOA Anguilla East Caribbean dollar XCD Antigua and Barbuda East Caribbean dollar XCD Argentina Argentine peso ARS Armenia Armenian dram AMD Aruba Aruban florin AWG Australia Australian dollar AUD Austria European euro EUR Azerbaijan Azerbaijani manat AZN B Bahamas Bahamian dollar BSD Bahrain Bahraini dinar BHD Bangladesh Bangladeshi taka BDT Barbados Barbadian dollar BBD Belarus Belarusian ruble BYR Belgium European euro EUR Belize Belize dollar BZD Benin West African CFA franc XOF Bhutan Bhutanese ngultrum BTN Bolivia Bolivian boliviano BOB Bosnia-Herzegovina Bosnia and Herzegovina konvertibilna marka BAM Botswana Botswana pula BWP 1 www.thecsspoint.com www.facebook.com/thecsspointOfficial The CSS Point Brazil Brazilian real BRL Brunei Brunei dollar BND Bulgaria Bulgarian lev BGN Burkina Faso West African CFA franc XOF Burundi Burundi franc BIF C Cambodia Cambodian riel KHR Cameroon Central African CFA franc XAF Canada Canadian dollar CAD Cape Verde Cape Verdean escudo CVE Cayman Islands Cayman Islands dollar KYD Central African Republic Central African CFA franc XAF Chad Central African CFA franc XAF Chile Chilean peso CLP China Chinese renminbi CNY Colombia Colombian peso COP Comoros Comorian franc KMF Congo Central African CFA franc XAF Congo, Democratic Republic Congolese franc CDF Costa Rica Costa Rican colon CRC Côte d'Ivoire West African CFA franc XOF Croatia Croatian kuna HRK Cuba Cuban peso CUC Cyprus European euro EUR Czech Republic Czech koruna CZK D Denmark Danish krone DKK Djibouti Djiboutian franc DJF Dominica East Caribbean dollar XCD 2 www.thecsspoint.com www.facebook.com/thecsspointOfficial The CSS Point Dominican Republic Dominican peso DOP E East Timor uses the U.S. -

Supported Currencies

AMERICAN EXPRESS GLOBAL MERCHANT SERVICES Supported Currencies Start Navigating Through the Global Marketplace with Multi-Currency Albanian Lek Danish Krone* Lesotho Loti Saudi Arabia Rial Algerian Dinar Djibouti Franc Liberian Dollar Serbian Dinar Armenian Dram Dominican Peso Libyan Dinar Seychelles Rupee Aruba Guilder Sierra Leone Leone Australian Dollar* East Caribbean Dollar Macau Pataca Singapore Dollar* Azerbaijanian Manat Egyptian Pound Macedonia Denar Solomon Islands Dollar Ethiopian Birr Malagasy Ariary Somali Shilling Bahamian Dollar Euro* Malawi Kwacha South African Rand* Bahraini Dinar Malaysian Ringgit Sri Lanka Rupee Fiji Dollar Bangladesh Taka Maldives Rufiyaa Swedish Krona* Barbados Dollar Mauritania Ouguiya Gambia Dalasi Swiss Franc* Belarussian Ruble Mauritius Rupee Georgian Lari Swaziland Lilangeni Belize Dollar Mexican Peso* Ghana Cedi Bermudian Dollar Moldovan Leu Taiwanese Dollar Gibraltar Pound Bhutan Ngultrum Mongolian Tugrik Tajik Somoni Guinea Franc Bosnia and Herzegovina Moroccan Dirham Tanzanian Shilling Guyana Dollar Convertible Marks Mozambique New Metical Thai Baht Guatemala Quetzal Botswana Pula Tonga Pa’anga Brunei Dollar Namibia Dollar Trinidad and Tobago Dollar Haiti Gourde Bulgarian Lev Nepalese Rupee Tunisian Dinar Hong Kong Dollar* Burundi Franc Netherlands Antillean Guilder Turkish Lira Hungarian Forint* New Zealand Dollar* Turkmenistan New Manat Honduras Lempira Cambodia Riel Nigerian Naira Uae Dirham Canadian Dollar* Iceland Krona Norwegian Krone* Uganda Shilling Cape Verde Escudo Indian Rupee -

Maximum Monthly Stipend Rates for Fellows and Scholars

MAXIMUM MONTHLY STIPEND RATES FOR FELLOWS AND SCHOLARS Dec 2018 COUNTRY Local Currency Local DSA MAX RES RATE MAX TRV RATE Effective % date Afghanistan Afghani 12,300 129,150 193,725 01-Aug-07 * Albania Albania Lek(e) 16,200 255,150 382,725 01-Jan-05 Algeria Algerian Dinar 30,400 319,200 478,800 01-Aug-07 * Angola Kwanza 71,300 748,650 1,122,975 01-Aug-07 #N/A Antigua and Barbuda (1 Apr. - 30 Nov.) E.C. Dollar #N/A #N/A #N/A 01-Aug-07 #N/A Antigua and Barbuda (1 Dec. - 31 Mar.) E.C. Dollar #N/A #N/A #N/A 01-Aug-07 * Argentina Argentine Peso 8,660 71,445 107,168 01-Jan-05 Australia AUL Dollar 453 4,757 7,135 01-Aug-07 Australia - Academic AUL Dollar 453 1,200 7,135 01-Aug-07 Austria Euro 249 2,615 3,922 01-Aug-07 * Azerbaijan (new)Azerbaijan Manat 219 1,478 2,217 01-Jan-05 Bahrain Bahraini Dinar 106 2,226 3,180 01-Jan-05 Bahrain - Academic Bahraini Dinar 106 1,113 1,670 01-Aug-07 * Bangladesh Bangladesh Taka 11,200 117,600 176,400 01-Aug-07 Barbados Barbados Dollar 850 8,925 13,388 01-Aug-07 Barbados Barbados Dollar 850 8,925 13,388 01-Aug-07 Belarus New Belarusian Ruble 530 5,168 7,751 01-Jan-06 * Belgium Euro 338 3,549 5,324 01-Aug-07 * Benin CFA Franc(XOF) 115,000 1,207,500 1,811,250 01-Aug-07 Bhutan Bhutan Ngultrum 8,200 86,100 129,150 01-Aug-07 Bolivia Boliviano 1,140 10,260 15,390 01-Jan-07 Bosnia and Herzegovina Convertible Mark 268 3,417 5,126 01-Jan-05 Botswana Botswana Pula 2,220 23,310 34,965 01-Aug-07 Brazil Brazilian Real 560 4,620 6,930 01-Jan-05 * British Virgin Islands (16 Apr. -

Republic of Tunisia Impact of the Libya Crisis on the Tunisian Economy

Report No: ACS16340 . Republic of Tunisia Public Disclosure Authorized Impact of the Libya Crisis on the Tunisian Economy . February 2017 Public Disclosure Authorized . GMF05 MIDDLE EAST AND NORTH AFRICA Public Disclosure Authorized Public Disclosure Authorized Macroeconomics & Fiscal Management Global Practice Middle East and North Africa Region Contents Acknowledgements .................................................................................................................................... v Executive Summary .................................................................................................................................. 1 Introduction ................................................................................................................................................ 4 Chapter 1 Libyan Households in Tunisia: How Many and Who are They? ............................ 10 ....................................................................................................................................... 10 ......................................... 11 ......................................................... 12 ...................... 18 ................................................................................................................................................... 22 ................................................................. 26 Chapter 2 The Impact on Financial Flows and the Banking System ......................................... 30 ...................................................................................................................................... -

PDF External Sector Statistics ISO Country Codes

External Sector Statistics (ESS) System - Submission of International Transactions Page 285 of 300 and External Position Information APPENDIX 8 STANDARD CODES Appendix 8(a) List of Country and Currency Codes ISO Country and Currency Codes* Country Code Currency Code AFGHANISTAN AF Afghani AFN ÅLAND ISLANDS AX Euro EUR ALBANIA AL Lek ALL ALGERIA DZ Algerian Dinar DZD AMERICAN SAMOA AS US Dollar USD ANDORRA AD Euro EUR ANGOLA AO Kwanza AOA ANGUILLA AI East Caribbean Dollar XCD ANTARCTICA AQ No universal currency ANTIGUA AND BARBUDA AG East Caribbean Dollar XCD ARGENTINA AR Argentine Peso ARS ARMENIA AM Armenian Dram AMD ARUBA AW Aruban Florin AWG AUSTRALIA AU Australian Dollar AUD AUSTRIA AT Euro EUR AZERBAIJAN AZ Azerbaijanian Manat AZN BAHAMAS BS Bahamian Dollar BSD BAHRAIN BH Bahraini Dinar BHD BANGLADESH BD Taka BDT BARBADOS BB Barbados Dollar BBD BELARUS BY Belarussian Ruble BYR BELGIUM BE Euro EUR BELIZE BZ Belize Dollar BZD BENIN BJ CFA Franc BCEAO XOF BERMUDA BM Bermudian Dollar BMD BHUTAN BT Ngultrum BTN BHUTAN BT Indian Rupee INR BOLIVIA, PLURINATIONAL STATE OF BO Boliviano BOB BOLIVIA, PLURINATIONAL STATE OF BO Mvdol BOV BONAIRE, SINT EUSTATIUS AND SABA BQ US Dollar USD BOSNIA AND HERZEGOVINA BA Convertible Mark BAM BOTSWANA BW Pula BWP BOUVET ISLAND BV Norwegian Krone NOK BRAZIL BR Brazilian Real BRL BRITISH INDIAN OCEAN TERRITORY IO US Dollar USD BRUNEI DARUSSALAM BN Brunei Dollar BND BULGARIA BG Bulgarian Lev BGN BURKINA FASO BF CFA Franc BCEAO XOF BURUNDI BI Burundi Franc BIF CAMBODIA KH Riel KHR CAMEROON CM CFA Franc BEAC -

ACE CATAIR Appendix B

CBP and Trade Automated Interface Requirements Appendix B – Valid Codes July 28, 2021 DRAFT 1 Pub # 0875-0419 The reader should be advised that this technical document is considered final. However, the document retains the DRAFT designation in the footer until such time that an official OPA (Office of Public Affairs) publication number has been assigned to the new “ACE ABI CATAIR” publication. For your information, subsequent revisions to this document will be controlled through the official CBP document amendment process. DRAFT 2 Table of Contents General Appendix Information ....................................................................................................... 6 Country and Currency Codes ...................................................................................................... 7 EU Country Codes .................................................................................................................... 18 Location Identifiers ................................................................................................................... 19 Units of Measure ....................................................................................................................... 23 Entry Type Codes ...................................................................................................................... 27 Mode of Transportation Codes .................................................................................................. 28 Equipment Description Codes .................................................................................................. -

Retail Price Indices Relating to Living Expenditures of United Nations

Price indices Indices des prix Retail price indices relating to living expenditures of United Nations Officials New York City = 100, Index date = June 2017 Indices des prix de détail relatif aux dépenses de la vie courante des fonctionnaires de l'ONU New York = 100, Date d'indice = Juin 2017 National currency per US $ Index - Indice Monnaie nationale du $ E.U. Excluding Country or Area Duty Station housing 2 Pays ou Zone Villes-postes Per US$ 1 Currency Total Non compris 1 Monnaie 2 Cours du $E-U l'habitation Afghanistan Kabul 67.570 Afghani 88 94 Albania - Albanie Tirana 118.700 Lek 75 82 Algeria - Algérie Algiers 108.549 Algerian dinar 86 90 Angola Luanda 165.090 Kwanza 131 120 Argentina - Argentine Buenos Aires 16.040 Argentine peso 88 95 Armenia - Arménie Yerevan 482.000 Dram 78 80 Australia - Australie Sydney 1.341 Australian dollar 81 91 Austria - Autriche Vienna 0.893 Euro 86 95 Azerbaijan - Azerbaïdjan Baku 1.690 Azerbaijan manat 75 80 Bahamas Nassau 1.000 Bahamanian dollar 102 96 Bahrain - Bahreïn Manama 0.377 Bahraini dinar 85 92 Bangladesh Dhaka 80.770 Taka 84 90 Barbados - Barbade Bridgetown 2.000 Barbadian dollar 95 106 Belarus - Bélarus Minsk 1.865 New Belarusian ruble 83 87 Belgium - Belgique Brussels 0.893 Euro 87 95 Belize Belmopan 1.999 Belize dollar 80 85 Benin - Bénin Cotonou 586.095 CFA franc 76 88 Bhutan - Bhoutan Thimpu 64.670 Ngultrum 81 88 Bolivia (Plurinational State of) - Bolivie (État plurinational de) La Paz 6.910 Boliviano 81 88 Bosnia and Herzegovina - Bosnie-Herzégovine Sarajevo 1.748 Convertible mark 73 79 Botswana Gaborone 10.309 Pula 73 81 Brazil - Brésil Brasilia 3.269 Real 87 90 Bulgaria - Bulgarie Sofia 1.748 Lev 74 82 Burkina Faso Ouagadougou 586.095 CFA franc 82 90 Burundi Bujumbura 1,705.645 Burundi franc 90 99 Cabo Verde - Cap-Vert Praia 98.521 CV escudo 80 88 Cambodia - Cambodge Phnom Penh 4,040.000 Riel 79 86 Cameroon - Cameroun Yaounde 586.095 CFA franc 81 88 Canada Montreal 1.348 Canadian dollar 82 88 Central African Rep.