Focus on Russia Power Reform

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Energy Without Borders

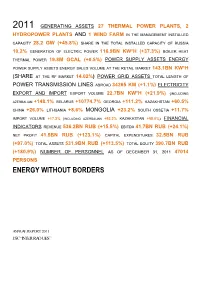

2011 GENERATING ASSETS 27 THERMAL POWER PLANTS, 2 HYDROPOWER PLANTS AND 1 WIND FARM IN THE MANAGEMENT INSTALLED CAPACITY 28.2 GW (+45.8%) SHARE IN THE TOTAL INSTALLED CAPACITY OF RUSSIA 10.2% GENERATION OF ELECTRIC POWER 116.9BN KW*H (+37.3%) BOILER HEAT THERMAL POWER 19.8M GCAL (+0.5%) POWER SUPPLY ASSETS ENERGY POWER SUPPLY ASSETS ENERGY SALES VOLUME AT THE RETAIL MARKET 143.1BN KW*H (SHARE AT THE RF MARKET 14.02%) POWER GRID ASSETS TOTAL LENGTH OF POWER TRANSMISSION LINES ABROAD 34265 KM (+1.1%) ELECTRICITY EXPORT AND IMPORT EXPORT VOLUME 22.7BN KW*H (+21.9%) (INCLUDING AZERBAIJAN +148.1% BELARUS +10774.7% GEORGIA +111.2% KAZAKHSTAN +60.5% CHINA +26.0% LITHUANIA +8.6% MONGOLIA +23.2% SOUTH OSSETIA +11.7% IMPORT VOLUME +17.2% (INCLUDING AZERBAIJAN +93.2% KAZAKHSTAN +58.0%) FINANCIAL INDICATORS REVENUE 536.2BN RUB (+15.5%) EBITDA 41.7BN RUB (+24.1%) NET PROFIT 41.5BN RUB (+123.1%) CAPITAL EXPENDITURES 32.5BN RUB (+97.0%) TOTAL ASSETS 531.9BN RUB (+113.5%) TOTAL EQUITY 390.7BN RUB (+180.9%) NUMBER OF PERSONNEL AS OF DECEMBER 31, 2011 47014 PERSONS ENERGY WITHOUT BORDERS ANNUAL REPORT 2011 JSC “INTER RAO UES” Contents ENERGY WITHOUT BORDERS.........................................................................................................................................................1 ADDRESS BY THE CHAIRMAN OF THE BOARD OF DIRECTORS AND THE CHAIRMAN OF THE MANAGEMENT BOARD OF JSC “INTER RAO UES”..............................................................................................................8 1. General Information about the Company and its Place in the Industry...........................................................10 1.1. Brief History of the Company......................................................................................................................... 10 1.2. Business Model of the Group..........................................................................................................................12 1.4. -

Annual Report ‘06 Contents

ANNUAL REPORT ‘06 CONTENTS MESSAGE TO SHAREHOLDERS ————————————————————————————— 4 MISSION AND STRATEGY ———————————————————————————————— 7 COMPANY OVERVIEW ————————————————————————————————— 13 ² GENERAL INFORMATION 13 ² GEOGRAPHIC LOCATION 14 ² CALENDAR OF KEY 2006 EVENTS 15 ² REORGANIZATION 16 CORPORATE GOVERNANCE —————————————————————————————— 21 ² PRINCIPLES AND DOCUMENTS 21 ² MANAGEMENT BODIES OF THE COMPANY 22 ² CONTROL BODIES 39 ² AUDITOR 40 ² ASSOCIATED AND AFFILIATED COMPANIES 40 ² INTERESTED PARTY TRANSACTIONS 41 SECURITIES AND EQUITY ——————————————————————————————— 43 ² CHARTER CAPITAL STRUCTURE 43 ² STOCK MARKET 44 ² DIVIDEND HISTORY 48 ² REGISTRAR 49 OPERATING ACTIVITIES. KEY PERFORMANCE INDICATORS ——————————————— 51 ² GENERATING FACILITIES 51 ² FUEL SUPPLY 52 ² ELECTRICITY PRODUCTION 56 ² HEAT PRODUCTION 59 ² BASIC PRODUCTION ASSETS REPAIR 59 ² INCIDENT AND INJURY RATES. OCCUPATIONAL SAFETY 60 ² ENVIRONMENTAL SAFETY 61 ELECTRICITY AND HEAT MARKETS ——————————————————————————— 65 ² COMPETITIVE ENVIRONMENT. OVERVIEW OF KEY MARKETS 65 ² ELECTRICITY AND HEAT SALES 67 FINANCIAL OVERVIEW ————————————————————————————————— 73 ² FINANCIAL STATEMENTS 73 ² REVENUES AND EXPENSES BREAKDOWN 81 INVESTMENT ACTIVITIES ———————————————————————————————— 83 ² INVESTMENT STRATEGY 83 ² INVESTMENT PROGRAM 84 ² INVESTMENT PROGRAM FINANCING SOURCES 86 ² DEVELOPMENT PROSPECTS 87 INFORMATION TECHNOLOGY DEVELOPMENT —————————————————————— 89 PERSONNEL AND SOCIAL POLICY. SOCIAL PARTNERSHIP ———————————————— 91 INFORMATION FOR INVESTORS AND SHAREHOLDERS —————————————————— -

2017 Annual Report of PJSC Inter RAO / Report on Sustainable Development and Environmental Responsibility

INFORMATION TRANSLATION Draft 2017 Annual Report of PJSC Inter RAO / Report on Sustainable Development and Environmental Responsibility Chairman of the Management Board Boris Kovalchuk Chief Accountant Alla Vainilavichute Contents 1. Strategic Report ...................................................................................................................................................................................... 8 1.1. At a Glance .................................................................................................................................................................................. 8 1.2. About the Report ........................................................................................................................................................................ 11 Differences from the Development Process of the 2016 Report ............................................................................................................ 11 Scope of Information ............................................................................................................................................................................. 11 Responsibility for the Report Preparation .............................................................................................................................................. 11 Statement on Liability Limitations ......................................................................................................................................................... -

3. Inter RAO Group Today | 11

10 | PJSC Inter RAO | 2016 Annual Report 3. INTER RAO GROUP TODAY The Group operates in the following segments: A leading electricity export and import operator in Rus- — Electricity and heat generation sia. The Inter RAO Group’s supply geography comprises — Electricity supply and heat supply Finland, Belarus, Lithuania, Latvia, Estonia, Poland, Nor- — International electricity trading way, Ukraine, Georgia, Azerbaijan, South Ossetia, Ka- A diversified energy holding company — Engineering, power equipment export zakhstan, China and Mongolia. managing assets in Russia, as well as — Management of electricity distribution grids outside Russia Effectively manages power supply companies – guaran- in European and CIS countries. teed suppliers in 12 regions of Russia. Since 2010, PJSC Inter RAO has been rated in the List of Strategic Enterprises and Strategic Joint Stock Compa- Owns independent suppliers of electricity to large indus- nies of the Russian Federation1. trial consumers. GENERATING ASSETS SUPPLY ACTIVITIES ELECTRICITY EXPORT in 2016 THERMAL POWER PLANTS 41 17.0bn kWh ELECTRICITY IMPORT HYDROPOWER PLANTS 62 (including 5 low capacity HPPs) 10 in 2016 IN 62 REGIONS OF RUSSIA bn kWh WIND FARMS 3.1 1 According to the Decree of the President of Russia No. 1190 dated 30.09.2010 PJSC Inter RAO was included in the List of Strategic Enterprises and Strategic Joint-Stock Companies (Section 2 of the List of Open Joint Stock Companies with its assets held in federal ownership managed by the Russian Federation in order to ensure strategic 2 interests of State defence and security, moral values, healthcare, rights and legitimate interests protection of the citizens of the Russian Federation). -

INTER RAO Share Placement Price – 0.0535 RUB

Additional share issue Fundamentals Basic results of Private placement : INTER RAO share placement price – 0.0535 RUB Number of shares issued – 13,800,000,000,000 common shares Total number of shares placed with the participants of private placement – 6,822,972,629,771 shares. A total of 49.4% of newly issued shares were placed Number of shares placed with Inter RAO Capital – 2,917,890,939,501 (including shares for deal with Norilsk Nickel, stock option program and future deals) Final volume of Inter RAO’s authorized capital after private placement - 9,716,000,000,000 ordinary shares (increase by a factor of 3.36) Value of the share capital of the Company - 272.997 billion RUB* Total value of assets acquired by Inter RAO within the private placement: • Shares of utility companies - 283.2 bn RUB** • Cash – 81.8 bn RUB Share of government and state-owned companies in the authorized capital of Inter RAO amounts to 60%; Registration of additional share placement report by Federal Service for Financial Markets is planned for June 2011 Newly issued shares should start trading in June 2011 and merge into main symbol in October 2011 (MICEX) * Par value of 1 share - 0.02809767 RUB ** Value of assets based on independent appraisers. It does not include assets that might be received by INTER RAO’ s subsidiaries (closed subscription participants) after May, 17 2 Ownership structure Equity structure before Equity structure to May 17, 2011 Target equity structure after deals placement Minority finalization shareholders Federal Property Federal Property -

INTER RAO UES Generating Assets: Target Shareholding Structure

INTER RAO UES Generating Assets: Target Shareholding Structure March,16 2012 1. Strategy recap and update INTER RAO at a Glance A Leading Russian Power Company Diversified Group Structure . Diversified power holding involved in electricity/heat generation and supply, export/import of electricity and engineering . Operates and manages 27 thermal, 2 hydro power plants and 1 wind power farm Domestic Engineering . Total installed electricity capacity of 29GW and electricity output of Generation Trading Supply International 117 TWh⁽¹⁾ in 2011 . INTER RAO – . RAO Nordic Oy . 9 supply companies . Generation: . Quartz Group . 2 Hydro PP - 0.2 GW Electrogeneration (Finland) . Customer base: . 4 Thermal PP - 5.2 GW . JV with Worley Leading Russian export-import operator accounting for 97% of Russian (100%) . Kazenergoresurs . 1 wind power farm - Parsons electricity export in 2011 . 314 thousand 0.03 GW . OGK-1 (75%) (Kazakhstan) legal entities and . Distribution . JV with Rosatom . OGK-3 (82%) . TGR Enerji (Turkey) . c. 34 ths. km of power . Operations in over 14 countries, including Russia, Belarus, Lithuania, 9.8 million . JV with GE lines (Georgia, residential . TGK-11 (68%) . INTER RAO Lietuva Armenia) Georgia, Armenia, Kazakhstan, Tajikistan, Moldova, and Finland . EMAlliance (the Baltics) customers Engineering (2) . Listed on RTS and MICEX (List A1), MCAP of $10.2bn. Shares are (2) included into MSCI Large Caps Index (0,54%) . GDRs admitted to LSE trading Ownership Structure Broad Geographical Coverage INTER RAO UES Finland Generation Assets -

ENERGY BEYOND BORDERS Company Profi Le

ENERGY BEYOND BORDERS Company profi le INTER RAO UES is a fast-growing energy company In 2003, Rosenergoatom purchased a 40% stake in the with a number of generation and distribution assets Company. This rendered CJSC INTER RAO UES the sta- in Russia and abroad. The total installed capacity of tus of an integrated exporter and importer of electric pow- the electric power stations controlled by the Company er generated by two major Russian energy producers, and is about 8,000 MW. The company is a major investor it started exporting power to 12 foreign countries. At the same time, the company actively built up its own genera- and a leading exporter and importer of electricity in tion and distribution capacities. Russia. Between 2003 and 2005, the INTER RAO UES Group The company was set up in spring 2008 as a successor bought Georgia-based assets such as JSC Telasi and Mt- to CJSC INTER RAO UES merged with a number of kvari Energy LLC, as well as the Sevano-Razdanskiy cas- Russian-based generation companies transferred un- cade of hydroelectric power plants (JSC MEK) in Arme- der its control as part of the reform of Russia’s power nia. industry. In 2004, its trading arm, RAO Nordic Oy, became a major player on the business scene in Finland. In 2005, CJSC INTER RAO UES was given the ownership of 50% of the shares in JSC Stantsia Ekibastuzskaya GRES-2 and JSC RAO UES International, a subsidiary of RAO UES of became a shareholder in the Russian-Tajik venture JSC Russia, was founded in 1997. -

Federal Grid Company of Unified Energy System

FEDERAL GRID COMPANY OF UNIFIED ENERGY SYSTEM ANNUAL REPORT WorldReginfo - b29cb2af-cbc8-402d-b3a6-fffe86634d00 ANNUAL REPORT 2008 WorldReginfo - b29cb2af-cbc8-402d-b3a6-fffe86634d00 Address to Shareholders Operating Corporate Operating Development of the Human Resources Environmental policy. Attachments of Chairmen of Board Results (13) Governance (23) Activity (51) Corporate Information management and Corporate Social (127) of Directors and Management System Social policy. Responsibility (117) Management Board (5) (CIMS) and Telecom- Social Partnership (103) munication Network (91) History of Establishing Scientific and Technical Contact information Most Important and Core Types Economics and work and Innovative for Shareholders Events in 2008 (9) of Activity (17) Securities (43) Finance (71) Investments (81) Procurement (99) Technologies (111) and Investors (123) WorldReginfo - b29cb2af-cbc8-402d-b3a6-fffe86634d00 CHAPTER 1. ADDRESS TO SHAREHOLDERS OF CHAIRMEN OF BOARD OF DIRECTORS AND MANAGEMENT BOARD 4 5 WorldReginfo - b29cb2af-cbc8-402d-b3a6-fffe86634d00 FGC UES Annual Report 2008 Chapter 1 Address to Shareholders of Chairmen of Board of Directors and Management Board Address to shareholders of Chairmen of Board of Directors and Management Board During 2008 the Company continued realization of its large-scale investment program. JSC FGC UES invested RUR 136.221 billion into modernization of assets within the Unified national energy grid (UNEG) enabling to put into service 1,047 km of electric energy transmis- sion facilities; 10,314 MVA of transformer capacity; 1,285 MVA of reactor capacity, back up commissioning of future periods. Key UNEG facilities were commissioned during 2008. In particular, modernization of substations 500 kV Beskudnikovo and 500 kV Otchakovo was completed and substation 500 kV Zapadnaya was built within the Moscow energy system that increased reliability, transmission capacity of the backbone grid and provided for con- necting new customers in Moscow and Moscow region. -

Moscow, Russian Federation September 21, 2007 Dear Holders of Depositary Receipts: the Board of Directors of Open Joint-Stock Co

Moscow, Russian Federation September 21, 2007 Dear Holders of Depositary Receipts: The Board of Directors of Open Joint-Stock Company Unified Energy System of Russia (‘‘RAO UES’’) decided on July 27, 2007 to call an extraordinary general meeting of RAO UES shareholders (the ‘‘EGM’’) for approval of shareholders, including holders of depositary receipts, of a reorganization involving: • the spin-offs by RAO UES to newly-formed Russian open joint-stock companies established by RAO UES (each, a ‘‘Holdco’’ and collectively, the ‘‘Holdcos’’) of the entire equity interests of RAO UES in certain of its subsidiaries (the ‘‘Spin-Offs’’), including (i) six wholesale generating companies (the ‘‘OGKs’’), comprised of five wholesale thermal generating companies and Open Joint-Stock Company ‘‘The Federal Hydro-Generation Company’’ (‘‘HydroOGK’’), (ii) thirteen territorial generating companies (the ‘‘TGKs’’ and together with the OGKs, the ‘‘Gencos’’), (iii) power companies in the Far East and other isolated areas (the ‘‘Far East Energos’’), (iv) inter-regional distribution grid companies (‘‘MRSKs’’) and distribution grid companies (‘‘RSKs’’), (v) Open Joint-Stock Company the Federal Grid Company of Unified Energy System (the ‘‘FSK’’) and the trunk grid companies, (vi) Closed Joint-Stock Company ‘‘Inter RAO UES’’ (‘‘InterRAO’’), (vii) Open Joint-Stock Company Sochinskaya TES (‘‘Sochinskaya TES’’) and (viii) Open Joint-Stock Company System Operator-Central Dispatching Office of the Unified Energy System (the ‘‘System Operator’’ and together with the Gencos, -

Annual Report Annual Report 2015

www.fsk-ees.ru 20 15 Annual Report Annual Report 2015 Federal Grid Company is a Russian energy company that provides electricity transmission services through the Unified National Electric Grid. In this type of business, the Company is a natural monopoly. The bulk of our revenue is generated through tariffs for electricity transmission that are approved by the Federal Anti-Monopoly Service. Our major consumers are regional distribution companies, sales companies and large industrial enterprises. The Annual Report has been preliminary approved by the Board of Directors of Federal Grid Company, Minutes No. 322 dated 27 May 2016 CHANGE OF COMPANY NAME On June 26 2015, the Annual General Meeting of Federal Grid Company resolved to approve a revised version of the Articles of Association, according to which Open Joint-Stock Company ‘Federal Grid Company of Unified Energy System’ has been renamed into Public Joint-Stock Company ‘Federal Grid Company of Unified Energy System’. In the text of this Annual Report, Public Joint-Stock Company ‘Federal Grid Company of Unified Energy Chairman of the Management Board A. Murov System’ is also referred to as: PJSC FGC UES, JSC FGC UES (former name until 07 July 2015), Federal Grid Company, Federal Grid, the Company. OUR MISSION About the concept of the Annual Report To ensure reliable operation and development of UNEG that will be While implementing its strategic priority – providing reliable, adequate to economic growth, and demonstrate high economic quality and secure energy supply for customers, Federal Grid efficiency and cost minimisation Company is taking proactive efforts to improve openness and transparency of its business, implementing the most effective management tools, maintaining a constant dialogue with all stakeholders. -

Russian Electricity Reform

INTERNATIONAL ENERGY AGENCY RUSSIAN ELECTRICITY REFORM Emerging challenges and opportunities INTERNATIONAL ENERGY AGENCY RUSSIAN ELECTRICITY REFORM Emerging challenges and opportunities page2-20x27b 14/03/05 9:40 Page 1 INTERNATIONAL ENERGY AGENCY The International Energy Agency (IEA) is an autonomous body which was established in November 1974 within the framework of the Organisation for Economic Co-operation and Development (OECD) to implement an international energy programme. It carries out a comprehensive programme of energy co-operation among twenty-six of the OECD’s thirty member countries. The basic aims of the IEA are: • to maintain and improve systems for coping with oil supply disruptions; • to promote rational energy policies in a global context through co-operative relations with non-member countries, industry and international organisations; • to operate a permanent information system on the international oil market; • to improve the world’s energy supply and demand structure by developing alternative energy sources and increasing the efficiency of energy use; • to assist in the integration of environmental and energy policies. The IEA member countries are: Australia, Austria, Belgium, Canada, the Czech Republic, Denmark, Finland, France, Germany, Greece, Hungary, Ireland, Italy, Japan, the Republic of Korea, Luxembourg, the Netherlands, New Zealand, Norway, Portugal, Spain, Sweden, Switzerland, Turkey, the United Kingdom, the United States. The European Commission takes part in the work of the IEA. ORGANISATION FOR ECONOMIC CO-OPERATION AND DEVELOPMENT The OECD is a unique forum where the governments of thirty democracies work together to address the economic, social and environmental challenges of globalisation. The OECD is also at the forefront of efforts to understand and to help governments respond to new developments and concerns, such as corporate governance, the information economy and the challenges of an ageing population. -

Annual Report 2007 MOSENERGO’S Mission

Mosenergo annual report 2007 MOSENERGO’s mission Mosenergo’s mission is to provide consumers with electric and thermal energy, generated by using resource- saving advanced technologies with equipment, meeting the highest ecological standards and provide the Com- pany’s shareholders with reasonable income MOSENERGO’s strategic objective The strategic objective is to maintain the leading position on the Moscow Area energy market, to take the lead on the Russian wholesale market of electric energy and power and to multiply company’s equity capital (to achieve maximum economic and social effect) MOSENERGO Structure General meeting of shareholders Board of Directors Audit commission Chairman of the Board of Directors Chairman of the Commission Mosenergo Executive Board annual report 2007 General Director General directorate Power plants Service branches (17 branches) (16 branches) •P.G. Smidovich TEP-1 •APK Shatursky •R.E. Classon LAPS-3 •Avtokhozyaistvo •TEP-6 •Central Mechanical Repair Works •TEP-8 •Energosvyaz •TEP-9 •Energotorg •M.Ya. Ufaev TEP-11 • Experimental Plant for Automation Means •TEP-12 and Devices •TEP-16 •Heating networks •TEP-17 •Industrial-Technological Completing Enterprise •TEP-20 •Information-Computing Center •TEP-21 •Medsanchast •TEP-22 •Moselektroremenergo •TEP-23 •Mosenergonaladka •TEP-25 •Mosenergoproyekt •TEP-26 •Mosenergospetsremont •TEP-27 • Special Construction-Technological Bureau •TEP-28 for High-Voltage and Cryogenic Technology •Teplosbyt MOSENERGO Generating Facilities in Moscow and in the Moscow Region TEP-27TEEP-227