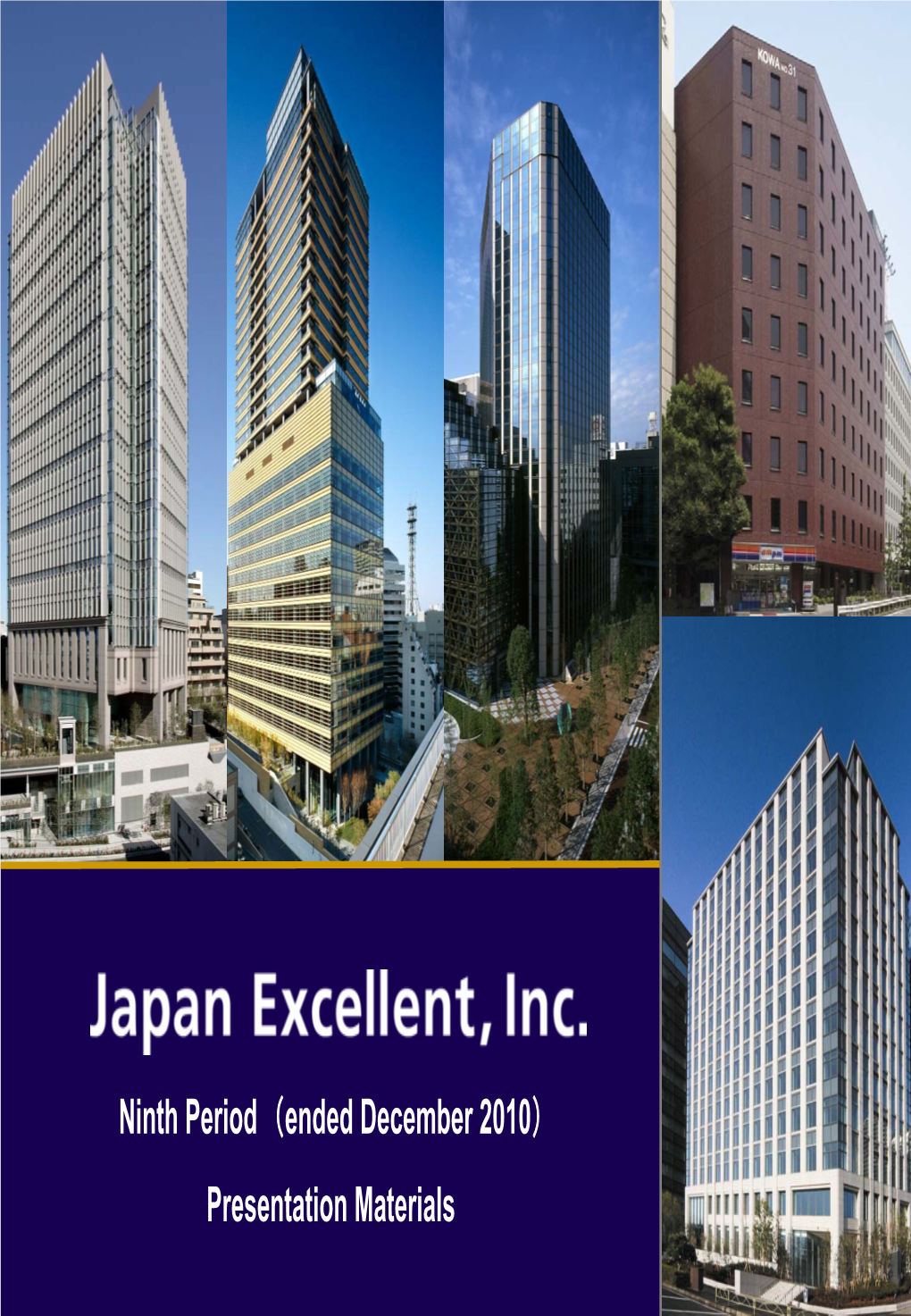

Ninth Period (Ended December 2010) Presentation Materials

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

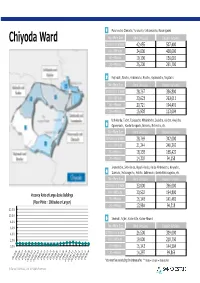

Chiyoda Ward 200Tsubo Or Greater 42,455 507,400 100〜199Tsubo 34,000 408,000 50〜99Tsubo 19,106 136,001 20〜49Tsubo 25,200 251,700

1 Marunouchi, Otemachi, Yurakucho, Uchisaiwaicho, Kasumigaseki Floor Plate Size Rent (\/tsubo) Deposit (\/tsubo) Chiyoda Ward 200tsubo or greater 42,455 507,400 100〜199tsubo 34,000 408,000 50〜99tsubo 19,106 136,001 20〜49tsubo 25,200 251,700 2 Kojimachi, Bancho, Hirakawacho, Kioicho, Hayabusacho, Nagatacho Floor Plate Size Rent (\/tsubo) Deposit (\/tsubo) 200tsubo or greater 28,267 336,800 100〜199tsubo 23,623 263,011 50〜99tsubo 20,721 194,491 20〜49tsubo 15,938 113,004 Uchi-Kanda, Tacho, Tsukasacho, Mitoshirocho, Sudacho, Kajicho, Awajicho, 3 Ogawamachi, Kanda-Surugadai, Jinbocho, Nishikicho, etc. Floor Plate Size Rent (\/tsubo) Deposit (\/tsubo) 200tsubo or greater 28,769 342,000 100〜199tsubo 21,244 240,292 50〜99tsubo 18,138 165,422 20〜49tsubo 14,307 94,158 Iwamotocho, Soto-Kanda, Higashi-Kanda, Kanda-Hirakawacho, Konyacho, 4 Izumicho, Matsunagacho, Aioicho, Sakumacho, Kanda-Matsunagacho, etc. Floor Plate Size Rent (\/tsubo) Deposit (\/tsubo) 200tsubo or greater 33,000 396,000 100〜199tsubo 20,532 194,800 Vacancy Rate of Large-Scale Buildings 50〜99tsubo 16,148 141,481 (Floor Plate︓ 200tsubo or Larger) 20〜49tsubo 13,984 94,318 12.0% 10.0% 5 Iidabashi, Fujimi, Kudan-Kita, Kudan-Minami 8.0% 6.0% Floor Plate Size Rent (\/tsubo) Deposit (\/tsubo) 4.0% 200tsubo or greater 26,500 309,000 2.0% 100〜199tsubo 19,000 210,750 0.0% 50〜99tsubo 16,143 144,504 20〜49tsubo 14,297 99,866 *Above rent fee are including of maintenance fee. **1 tsubo ≑ 3.3 sq.m ≑ 35.58 sq. feet © Sanko Estate Co., Ltd. -

TOKYO TRAIN & SUBWAY MAP JR Yamanote

JR Yamanote Hibiya line TOKYO TRAIN & SUBWAY MAP Ginza line Chiyoda line © Tokyo Pocket Guide Tozai line JR Takasaka Kana JR Saikyo Line Koma line Marunouchi line mecho Otsuka Sugamo gome Hanzomon line Tabata Namboku line Ikebukuro Yurakucho line Shin- Hon- Mita Line line A Otsuka Koma Nishi-Nippori Oedo line Meijiro Sengoku gome Higashi Shinjuku line Takada Zoshigaya Ikebukuro Fukutoshin line nobaba Todai Hakusan Mae JR Joban Asakusa Nippori Line Waseda Sendagi Gokokuji Nishi Myogadani Iriya Tawara Shin Waseda Nezu machi Okubo Uguisu Seibu Kagurazaka dani Inaricho JR Shinjuku Edo- Hongo Chuo gawa San- Ueno bashi Kasuga chome Naka- Line Higashi Wakamatsu Okachimachi Shinjuku Kawada Ushigome Yushima Yanagicho Korakuen Shin-Okachi Ushigome machi Kagurazaka B Shinjuku Shinjuku Ueno Hirokoji Okachimachi San-chome Akebono- Keio bashi Line Iidabashi Suehirocho Suido- Shin Gyoen- Ocha Odakyu mae Bashi Ocha nomizu JR Line Yotsuya Ichigaya no AkihabaraSobu Sanchome mizu Line Sendagaya Kodemmacho Yoyogi Yotsuya Kojimachi Kudanshita Shinano- Ogawa machi Ogawa Kanda Hanzomon Jinbucho machi Kokuritsu Ningyo Kita Awajicho -cho Sando Kyogijo Naga Takebashi tacho Mitsu koshi Harajuku Mae Aoyama Imperial Otemachi C Meiji- Itchome Kokkai Jingumae Akasaka Gijido Palace Nihonbashi mae Inoka- Mitsuke Sakura Kaya Niju- bacho shira Gaien damon bashi bacho Tameike mae Tokyo Line mae Sanno Akasaka Kasumi Shibuya Hibiya gaseki Kyobashi Roppongi Yurakucho Omotesando Nogizaka Ichome Daikan Toranomon Takaracho yama Uchi- saiwai- Hachi Ebisu Hiroo Roppongi Kamiyacho -

Tokyo City Clinic Mita Ikefuji Bldg 2F 4-5-8 Shiba 5439-5566 Shintamati

List of Medical Institutions which provide Health Check-ups for 18-Month-old Infants Please inquire to the medical institution in advance as there may be changes in the medical institution or you may have to make an appointment . And also be sure to take your Maternity and Child Health Handbook and health insurance card with you when you go to a hospital or clinic. English Clinic/hospital Address Tel available Explanatory notes Tokyo City Clinic Mita Ikefuji Bldg 2F 4-5-8 Shiba 5439-5566 ○ Shintamati bldg Clinic Shin Tamachi Bldg 2F 5-34-6 Shiba 3451-2619 Tokyo Medical And Surgical Clinic 32 Shibakoen Bldg 2F 3-4-30 Shibakoen 3436-3028 ○ Shimbashi Allergy Rheumatism New Shimbashi Bldg318 2-16-1 Shimbashi 3591-5464 ○ Clinic Hospitals in affiliation with The Jikeikai University 3-19-18 Nishi-shimbashi 3433-1111 ○ A reservation is Toranomon Hospital 2-2-2 Toranomon 3588-1111 ○ required. International University of Health 1-4-3 Mita 3451-8121 ○ and Welfare, Mita Hospital Tokyo Saiseikai Central Hospital 1-4-17 Mita 3451-8211 Belle Foret Azabu3F Azabu Womens Clinic 6809-3103 2-3-12 Azabujuban Baba Clinic Kumai Bldg 2F 2-13-2 Azabujuban 3454-7788 Sunny Garden Clinic Pediatrics Plusone Bldg 3F 2-16-4 Azabujuban 6722-6623 ○ Odawara Clinic 3-11-12 Azabujuban 3451-4595 Azabukouki Clinic 3-3-2 Nishi-azabu 6240-2912 ○ Nishiazabu international Clinic LY Nishiazabu 2F 3-17-20 Nishi-azabu 6447-5966 ○ Furukawa Clinic MD Azabu 2F 3-7-13 Higashi-azabu 3583-2837 ○ Aiiku Clinic 5-6-8 Minami-azabu 3473-8305 Hiroo Kanamori Clinic Daini Sano Bldg 4F 5-10-24 -

Disaster Prevention Map for Takanawa, Minato City Disaster

6 3 10 1 30 29 10 15 Ichinohashi Jct 1 Shimboribashi 13 Azabu-san Kindergarten 12 14 6 2 Minami-azabu 5-chome 8Moto-azabu 2-chome 21 Nakanohashi 29 4 Zenpuku-ji Temple Azabujuban 2-chome Hiroo Children's Park 7 11 16 Children's Park Azabu Sports Grounds 17 10 Hiroo Station 15 16 Tokyo Metropolitan Central Library 9 Moto-azabu Nakanohashi Ando Memorial Church 8 7 3 Azabu Hikawa-jinjya 1-chome 7 Kindergarten Azabu Fire Station Shrine 5 4 4 5 6 14 7 6 2 Iikura Branch 1 Azabujuban Station Mita Koyamacho DisasterDisaster PreventionPrevention MapMap forfor Arisugawa-no-miya Memorial Park 5 Shiba Park Nanbu-zaka Kindergarten 1 Azabujuban Children's Park Arisugawanomiya Memorial Park Sendai-zaka 9 Azabujuban 3-chome Hiroo-inari Jinja Shrine Mita 1-chome Tenshin-ji Temple 10 4-chome 2 11 Minato Health Care Center 13 6 Embassy of the Federal Embassy of the Republic of Korea 14 Children and Families Support Center Republic of Germany Azabu Kids-to-Teens Hall/ 5 Ninohashi 11 Takanawa, Minato City Arisu Iki-iki Plaza 2 3 4 Takanawa, Minato City 6 IUHW Mita Hospital 1 1 Nursing Home "Arisu-no-mori Kinoko Hommura Nursery School 12 Saiseikai Central Hospital Minami-azabu 3-chome e Hyuga-zaka Minami-azabu" Minami-azabu 1-chome u 5 Nursery School n 5 e (Scheduled to open in March 2020) 15 v Akabane Elementary School Nursing Home Minami-azabu Senior Garden Alice A Nursing Home "Rakuwa Villa Minami-azabu" 21 16 i 4 Hiroo 5-chome r Akabane Kindergarten Disabled Individual Support Home Minami-azabu(Scheduled to open in March 2020) Minami-azabu Iki-iki Plaza -

SHIBA Area AZABU Area

Index SHIBA Area 1 Seppuku site of nine of the righteous samurai (Site of Mizuno Kenmotsu Residence) …… 22 2 Site of the Seppuku of Asano Takumi-no-kami ……………………………………… 20 3 Site of the Seppuku of Ōishi Chikara and other 9 Rōnin …………………………… 22 4 Birthplace of Kōyō Ozaki ………………………………………………………………… 59 5 Site of the Residence of the Dutch and other Missions (Shimpukuji-Temple) … … 34 6 Site of the Encounter between Kaishū Katsu and Takamori Saigō ……………… 30 7 Kamezuka Mound ………………………………………………………………………… 7 8 Karasumori-jinja Shrine …………………………………………………………………… 4 9 Birthplace of Japanese Nursing Education (Jikei University School of Medicine) ……… 49 Kyū-Shiba-rikyū Gardens ………………………………………………………………… 12 Site of the Old Shimbashi Station ……………………………………………………… 51 Site of Keio Gijuku and Kōgyōkusha …………………………………………………… 50 Keio University …………………………………………………………………………… 60 Site of the First Shiba City Office (Anyoin Temple) ………………………………… 50 Site of the First French Legation (Saikaiji Temple) ………………………………… 39 Site of the Incident of Setting Fire to the Satsuma Domain's Residence in Edo … 30 Birthplace of Japanese Dental Education …………………………………………… 46 Autumn Leaves Waterfall and Mountain Stream in Shiba Park …………………… 12 Shiba-Maruyama-kofun Tumulus ………………………………………………………… 4 Site of the First Newspaper Publication ……………………………………………… 52 Site of the Residence of the Swiss Mission ………………………………………… 39 Site of the Residence of Sengoku Hōki-no-kami……………………………………… 20 Zōjōji Temple ……………………………………………………………………………… 5 Site of Tokyo Broadcasting Station -

Germany in Japan

Since 1970 FREE Vol.41 No.18 Oct 1st - Oct 15, 2010 www.weekenderjapan.com Including Japan’s largest online classifieds Germany in Japan A 150 year-old-relationship that began in Yokohama Plus: The Forests of Aśoka at the Hara Oktoberfest! and Bill Hersey’s Parties People & Places CONTENTS Volume 41 Number 18 Oct 1st - Oct 15th, 2010 4 Executive Profiles: Trevor Reynolds 5 The View From Here 6-7 Tokyo Happenings 9 Arts and Entertainment 10-11 Tokyo Tables 12-16 Feature: Yokohama 19-21 Weekender Interview: Terrence Parker 22-25 Parties, People & Places 26-27 London Calling Event 28-29 Products: Designed in Deutschland 30-31 Real Estate 32-33 Classifieds 34 Back in the Day: Sumo comes to Germany CONTRIBUTORS Christopher Jones, Thomas PUBLISHER Ray Pedersen Fukuyama, Ian de Stains OBE, EDITOR Ray Pedersen ASSISTANT EDITOR Stephen Parker Cover and inside photo courtesy of: Library of Congress MEDIA MANAGER Tomas Castro MEDIA CONSULTANTS Mary Rudow, Pia von Waldau EST. Corky Alexander and Susan Scully, 1970 RESEARCHER Rene Angelo Pascua OFFICE Weekender Magazine, 5th floor, Regency Shinsaka Building, CONTRIBUTING EDITORS Owen Schaefer (Arts), Bill Hersey 8-5-8 Akasaka, Minato-ku, Tokyo 107-0052 (Society), Elisabeth Lambert (Health & Eco), Darrell Nelson Tel. 03-6846-5615 Fax: 03-6846-5616 (Sustainable Business) Email: [email protected] Opinions expressed by Weekender contributors are not necessarily www.weekenderjapan.com those of the publisher. 3 WEEKENDER B u s i n e s s C-Level Profiles / Executives in Japan Photo courtesy of Australia Society of Australia courtesy Photo EdwardTrevor Reynolds Suzuki President of the Australia Society Tokyo A 20 year resident of Japan, Trevor Reynolds has many hats: father, money manager and president of the Australian Society of Japan. -

Railway and Subway Route Map: Metropolitan Area 1 2 3 4 5

How to Get to Sightseeing Spots: Tokyo and The Surrounding Areas L andmarks H istory M useums Map Index Map Index Map Index Railway 東京都庁 皇居二重橋 国立西洋美術館 Tokyo Metropolitan Government 2B Imperial Palace Nijubashi Bridge 3B The National Museum of Western Art 3A/4A Access: Access: Access: Shinjuku 10min. Imperial Palace Outer Gardens Ueno 1min. JY JC JB JA JS Tōkyō 10min. JK JY JU JJ 17 05 10 11 20 JT JO JK JY JC 30 05 02 01 and Subway 01 19 26 01 01 JR West Exit JU JE JR Park Exit E 01 01 G H Tochomae 0min. 28 8min. 16 17 Yūrakuchō 10min. JY JK Keisei-Ueno 7min. 30 25 Route Map C 10 Nijubashimae 2min. of the Metropolitan area H Hibiya 2min. 07 東京周辺 鉄道路線図 Y JR and Sakuradamon 8min. 17 [JR・地下鉄・私鉄] Other ©TCVB Major Lines Map Index Map Index Map Index Map Index Map Index Map Index Sunshine City 2A Tokyo Tower 3B/3C Meiji Jingu Shrine 2B Hama-rikyu 3C/4C Tokyo National 3A/4A Tokyo Metropolitan 4B サンシャインシティ 東京タワー 明治神宮 Gardens 浜離宮恩賜庭園 Museum Edo-Tokyo Museum 東京国立博物館 東京都江戸東京博物館 ©TCVB Access: Access: Access: ©TCVB Access: Harajuku 1min. Ueno 10min. JK JY JU JJ JY Shimbashi 12min. Hamamatsuchō 15min. 19 JR Omotesandō Exit 30 05 02 01 JR Park Exit JT JO JK JY Access: JK JY G H 23 28 JR North Exit 02 18 24 29 JR Shiodome Exit 15min. 8min. Yoyogi 5min. 16 17 Ikebukuro E G A JY JB E 08 10 ©TCVB JY JA JS M Y F Akabanebashi 5min. -

Kenshu-In Guidebook

KENSHU-IN GUIDEBOOK 2019 1 S M T W T F S 7 S M T W T F S 1 2 3 4 5 1 2 3 4 5 6 6 7 8 9 10 11 12 7 8 9 10 11 12 13 13 14 15 16 17 18 19 14 15 16 17 18 19 20 20 21 22 23 24 25 26 21 22 23 24 25 26 27 27 28 29 30 31 28 29 30 31 2 S M T W T F S 8 S M T W T F S 1 2 1 2 3 3 4 5 6 7 8 9 4 5 6 7 8 9 10 10 11 12 13 14 15 16 11 12 13 14 15 16 17 17 18 19 20 21 22 23 18 19 20 21 22 23 24 24 25 26 27 28 25 26 27 28 29 30 31 3 S M T W T F S 9 S M T W T F S 1 2 1 2 3 4 5 6 7 3 4 5 6 7 8 9 8 9 10 11 12 13 14 10 11 12 13 14 15 16 15 16 17 18 19 20 21 17 18 19 20 21 22 23 22 23 24 25 26 27 28 24 31 25 26 27 28 29 30 29 30 4 S M T W T F S 10 S M T W T F S 1 2 3 4 5 6 1 2 3 4 5 7 8 9 10 11 12 13 6 7 8 9 10 11 12 14 15 16 17 18 19 20 13 14 15 16 17 18 19 21 22 23 24 25 26 27 20 21 22 23 24 25 26 28 29 30 27 28 29 30 31 5 S M T W T F S 11 S M T W T F S 1 2 3 4 1 2 5 6 7 8 9 10 11 3 4 5 6 7 8 9 12 13 14 15 16 17 18 10 11 12 13 14 15 16 19 20 21 22 23 24 25 17 18 19 20 21 22 23 26 27 28 29 30 31 24 25 26 27 28 29 30 6 S M T W T F S 12 S M T W T F S 1 1 2 3 4 5 6 7 2 3 4 5 6 7 8 8 9 10 11 12 13 14 9 10 11 12 13 14 15 15 16 17 18 19 20 21 16 17 18 19 20 21 22 22 23 24 25 26 27 28 23 30 24 25 26 27 28 29 29 30 31 : National Holidays : Substitute Holidays For a further explanation, please refer to Appendix 7. -

Financial Services Agency Kanto Local Finance Bureau(FIBO) No.16 AXA INVESTMENT MANAGERS JAPAN LTD

Financial Instruments Business Operators As of August 31, 2021 Type I Type II Investment Investment Securities- Financial Financial Advisory and Jurisdiction Registration numbers Name JCN Address Telephone Management Related Instruments Instruments Agency Business Business Business Business Business Financial Services Agency Kanto Local Finance Bureau(FIBO) No.16 AXA INVESTMENT MANAGERS JAPAN LTD. 4010401061149 1-17-3, Shirokane, Minato-ku, Tokyo 03-5447-3100 ○ ○ ○ ○ ○ Kanto Local Finance Bureau(FIBO) No.18 Ichigo Estate Co., Ltd. 1010001125620 1-1-1,Uchisaiwai-cho,Chiyoda-ku,Tokyo 03-3502-5625 ○ ○ ○ Kanto Local Finance Bureau(FIBO) No.44 SBI Securities CO., LTD. 3010401049814 1-6-1, Roppongi, Minato-ku, Tokyo 03-5562-7210 ○ ○ ○ ○ Kanto Local Finance Bureau(FIBO) No.45 Japannext Co.,Ltd. 2010001139289 3-1-1, Roppongi, Minato-ku, Tokyo 03-4577-4040 ○ ○ Kanto Local Finance Bureau(FIBO) No.51 Yensai.com Co., Ltd. 8010001082954 1-16-1, Kanda-Nishikicho, Chiyoda-ku, Tokyo 03-3518-8011 ○ ○ Kanto Local Finance Bureau(FIBO) No.52 Okasan Online Securities Co.,Ltd 2010001097479 3-9-7, Ginza, Chuo-ku, Tokyo 03-3547-0100 ○ ○ ○ ○ Kanto Local Finance Bureau(FIBO) No.53 OKASAN SECURITIES CO.,LTD. 5010001082560 1-17-6,Nihonbashi,Chuo-ku,Tokyo 03-3272-2211 ○ ○ ○ ○ Kanto Local Finance Bureau(FIBO) No.57 Janus Henderson Investors (Japan) Limited 3010001012362 1-6-5,Marunouchi, Chiyoda-ku, Tokyo 03-5219-8000 ○ ○ ○ Kanto Local Finance Bureau(FIBO) No.61 au Kabucom Securities Co., Ltd. 5010001066670 1-3-2, Otemachi, Chiyoda-ku, Tokyo 03-4221-3551 ○ ○ ○ ○ Kanto Local Finance Bureau(FIBO) No.66 Credit Suisse Securities (Japan) Limited 2010401059260 1-6-1,Roppongi Minato-ku,Tokyo 03-4550-9000 ○ ○ ○ ○ ○ Kanto Local Finance Bureau(FIBO) No.69 Goldman Sachs Japan Co.,Ltd. -

Minato City Guide

Tourist spot ※More tourist spots are listed on the back of this map. Shiba Daijingu 1 MAP F-5 www.shibadaijingu.com/ An old shrine that was constructed in the middle of the Heian Period. Shiba Park 2 MAP E-5 One of Japan's oldest public parks. It is a place in Tokyo for relaxation and refreshment. Mori Art Museum 3 MAP C-4 https://www.mori.art.museum/en/ This international art museum, which focuses primarily on modern art, is located on the 53rd oor of the Roppongi Hills Mori Tower. In addition to running its own exhibitions designed from unique perspectives, Mori Art Museum also stages diverse array of programs that includes collection exhibits and the showcasing of video works.The museum is open until 10 P.M. (5 P.M. on Tuesdays). 4 Monuments presented by the embassies of 12 countries MAP D-4 Here, there are monuments presented by the neighboring embassies. A sight unique to a neighborhood with many embassies. Statue of Kimi-chan 5 MAP D-5 A statue commemorating Kimi-chan, the model for the children's song "Red Shoes". Tourist spot ※More tourist spots are listed on the back of this map. 6 United Church of Christ in Japan 7 Nogi-jinja Shrine 8 Toyokawa Inari Tokyo Branch Temple 9 Nezu Museum 10 Happo-en 11 Shibaura-minami Futo Park 12 Odaiba Marine Park Ando Memorial Chapel MAP C-2 MAP D-2 MAP B-3 MAP B-7 MAP F-8 MAP H-9 http://www.toyokawainari-tokyo.jp/ http://www.nezu-muse.or.jp/ http://www.happo-en.com/ MAP C-5 The shrine honoring General Nogi A marine park below the Rainbow A seaside beach park on Tokyo Bay An irreplaceable church that was erected in and his wife. -

PERFECT TIMING the Precision Engineering Behind the Iconic Swiss Brand

FEBRUARY 2014 Japan’s number one English language magazine BREAKING THE SILENCE Former Miss International speaks out against the yakuza BARUTO We speak with the Baltic sumo superstar on the eve of his retirement THE MAYOR OF MINATO Managing Tokyo’s most international ward TAG HEUER PERFECT TIMING The precision engineering behind the iconic Swiss brand ALSO: Interview with former Prime Minister Yoshiro Mori, Agenda, People, Parties, and Places, and much more FEBRUARY 2014 CONTENTS 10 TAG HEUER The inner workings of a Swiss watchmaking legend 6 16 42 BARUTO IKUMI YOSHIMATSU MOGWAI An Estonian sumo phenom looks back at a Standing up to a system of intimidation in Scottish post-rockers on Rave Tapes and their storied career in the ring Japan’s talent agencies upcoming show at Hostess Weekender 8 The Lexus 6 22 Valentine’s Day 34 People, Parties, Places In the fast lane with Issac Nelson, a star Cupid got you stumped? Here are our The 16th Annual Orphans’ Holiday Party, of the Tokyo rock and soul scene suggestions for gifts and things to do saying sayonara to old friends, and more 18 Yoshir Mori 25 Education 40 Movies Former Prime Minister speaks about New trends in learning, and a look at A Formula One throwback, a return to foreign policy and Vladimir Putin some of Tokyo’s top schools Middle-earth, and the Mighty Thor 20 Patina 30 The Mayor of Minato 44 Agenda California fine dining comes to the Masaaki Takei tells us what it takes to run The Stones, Eric Clapton, Nine Inch Nails, heart of Tokyo the most international ward in Tokyo and cultural celebrations FEBRUARY 2014 www.tokyoweekender.com www.tokyoweekender.com FEBRUARY 2014 A WORD FROM THE EDITOR with France’s Ambassador to Japan, FEBRUARY 2014 Christian Masset, as he looked back at a landmark year in Franco-Japanese relations FEBRUARY 2014 and ahead to a year of even greater cultural Japan’s number one English language magazine connections. -

TOKYO TOURIST and SUBWAY MAP TOKYO POCKET GUIDE

TOKYO TOURIST and SUBWAY MAP TOKYO POCKET GUIDE Chiyoda A B C D Line Marunouchi JR JR Takasaka E F Line Saikyo Mita Namboku line Toneri Fukutoshin Line Line Line JR Joban Keisei Line Ginza Line Kana Liner Line to Narita Line mecho JR Nishi Otsuka Sugamo Komagome Yamanote Tabata North Ikebukuro Line Nippori Nippori Hibiya 1 JR Line 1 Yamanote Yurakucho Line Line Shin- Hon- Sky Tree Sengoku Komagome Higashi Otsuka Uguisudani Meijiro Ikebukuro Sendagi Sensoji Temple Zoshigaya JR Asakusa Yamanote Iriya Tozai Hakusan Line Waseda Line Takadanobaba Gokokuji Todai-Mae Tawara Nezu Natl Museum machi Nishi Myogadani Waseda Mita Namboku Chiyoda Oedo Seibu Line Ueno Zoo Inaricho Shin Shinjuku Kagurazaka Yurakucho Line Line Line Marunouchi Line Marunouchi Okubo Ginza Line Oedo Higashi Line Yushima Ueno Line Shinjuku Wakamatsu Tozai Kasuga Line Hongo Naka- JR Kawada Line Edogawa Okachimachi 2 Chuo & Sobu Kabukicho Ushigome bashi Korakuen San-chome 2 Line Yanagicho Ueno JR Oedo Shin- Chuo & Sobu Shinjuku Shinjuku Shinjuku Line Hirokoji Okachimachi Line Met.Gov.Bldg San-chome Line Ushigome Kagurazaka Marunouchi Shin-Ocha Okachimachi Gyoenmae Tokyo Dome Line nomizu Keio Fukutoshin Akebonobashi Oedo Suehirocho Sumo Edo Museum Line Line Iidabashi Line JR Suido-Bashi Ocha Electric Town Yamanote Shinjuku Park Ryogoku Line no JR Yotsuya Chuo & Sobu mizu Line Akihabara Odakyu Sanchome Shinjuku Line Ichigaya Shinjuku Sendagaya Line Kudanshita Mita Line Yoyogi JR Line Kodemmacho Chuo & Sobu Shinano- Line Hibiya machi Ogawa Kanda Line Kojimachi Jimbocho machi Hanzomon