The Economic Impact of Telecommunications in Senegal (*)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

APSCC Monthly E-Newsletter AUGUST 2017

APSCC Monthly e-Newsletter AUGUST 2017 The Asia-Pacific Satellite Communications Council (APSCC) e-Newsletter is produced on a monthly basis as part of APSCC’s information services for members and professionals in the satellite industry. Subscribe to the APSCC monthly newsletter and be updated with the latest satellite industry news as well as APSCC activities! To renew your subscription, please visit www.apscc.or.kr/sub4_5.asp. To unsubscribe, send an email to [email protected] with a title “Unsubscribe.” News in this issue has been collected from July 1 to July 31. INSIDE APSCC APSCC 2017 Satellite Conference & Exhibition, 10-12 October, Tokyo, Japan EARLY BIRD REGISTRATION IS NOW OPEN! The APSCC Satellite Conference and Exhibition is Asia’s must-attend executive conference for the satellite and space industry, where business leaders come together to gain market insight, strike partnerships and conclude major deals. Celebrating its 20th annual event APSCC 2017 #SATECHexplorer will incorporate industry veterans and new players through the 3-day of in-depth conference program to reach out to a broader audience. Join APSCC 2017 and expand your business network while hearing from a broad range of thought-provoking panels and speakers representing visionary ideas and years of business experience in the industry. For more information, please visit www.apscc2017.com SATELLITE BUSINESS Geoscience Australia Renews Life-Saving Connectivity Contracts with Speedcast July 5, 2017 - Speedcast International Limited announced Geoscience Australia, Australia’s pre-eminent public sector geoscience organization, has renewed its contract with Speedcast for life-saving connectivity applications. Speedcast provides VSAT connectivity for Geoscience Australia’s seismic reading and GPS land movement applications. -

Case 20-32299-KLP Doc 208 Filed 06/01/20 Entered 06/01/20 16

Case 20-32299-KLP Doc 208 Filed 06/01/20 Entered 06/01/20 16:57:32 Desc Main Document Page 1 of 137 Case 20-32299-KLP Doc 208 Filed 06/01/20 Entered 06/01/20 16:57:32 Desc Main Document Page 2 of 137 Exhibit A Case 20-32299-KLP Doc 208 Filed 06/01/20 Entered 06/01/20 16:57:32 Desc Main Document Page 3 of 137 Exhibit A1 Served via Overnight Mail Name Attention Address 1 Address 2 City State Zip Country Aastha Broadcasting Network Limited Attn: Legal Unit213 MezzanineFl Morya LandMark1 Off Link Road, Andheri (West) Mumbai 400053 IN Abs Global LTD Attn: Legal O'Hara House 3 Bermudiana Road Hamilton HM08 BM Abs-Cbn Global Limited Attn: Legal Mother Ignacia Quezon City Manila PH Aditya Jain S/O Sudhir Kumar Jain Attn: Legal 12, Printing Press Area behind Punjab Kesari Wazirpur Delhi 110035 IN AdminNacinl TelecomunicacionUruguay Complejo Torre De Telecomuniciones Guatemala 1075. Nivel 22 HojaDeEntrada 1000007292 5000009660 Montevideo CP 11800 UY Advert Bereau Company Limited Attn: Legal East Legon Ars Obojo Road Asafoatse Accra GH Africa Digital Network Limited c/o Nation Media Group Nation Centre 7th Floor Kimathi St PO Box 28753-00100 Nairobi KE Africa Media Group Limited Attn: Legal Jamhuri/Zaramo Streets Dar Es Salaam TZ Africa Mobile Network Communication Attn: Legal 2 Jide Close, Idimu Council Alimosho Lagos NG Africa Mobile Networks Cameroon Attn: Legal 131Rue1221 Entree Des Hydrocarbures Derriere Star Land Hotel Bonapriso-Douala Douala CM Africa Mobile Networks Cameroon Attn: Legal BP12153 Bonapriso Douala CM Africa Mobile Networks Gb, -

Tsb Liste Des Codes De Points Sémaphores Internationaux

Annexe au Bulletin d'exploitation de l'UIT No 1199 – 1.VII.2020 UNION INTERNATIONALE DES TÉLÉCOMMUNICATIONS TSB BUREAU DE LA NORMALISATION DES TÉLÉCOMMUNICATIONS DE L'UIT _______________________________________________________________ LISTE DES CODES DE POINTS SÉMAPHORES INTERNATIONAUX (ISPC) (SELON LA RECOMMANDATION UIT-T Q.708 (03/99)) (SITUATION AU 1 JUILLET 2020) _______________________________________________________________ Genève, 2020 Liste des codes de points sémaphores internationaux (ISPC) Note du TSB 1. Cette Liste des codes de points sémaphores internationaux (ISPC) (international signalling point codes) remplace celle qui avait été publiée dans l’Annexe du Bulletin d'exploitation No 1109 du 1.X.2016. Depuis ce jour, différentes notifications ont été reçues au TSB et ont été publiées séparément dans différents numéros du Bulletin d'exploitation de l'UIT. La présente Liste récapitule tous les différents amendements qui ont été publiés jusqu'au Bulletin d'exploitation No 1199 du 1.VII.2020. 2. La Recommandation UIT-T Q.708 mentionne que l'attribution des codes de zone/réseau sémaphore (SANC) (signalling area network code) doit être régie par le TSB. L'attribution des codes de points sémaphores internationaux (ISPC) sera faite par chaque pays qui en avisera le TSB. 3. Le plan de numérotage de la Recommandation UIT-T Q.708 contient 2 048 codes SANC permettant de disposer de 16 384 points sémaphores internationaux. Parmi ces codes, 1 536 sont disponibles pour assignation, donnant 12 288 points sémaphores internationaux. A l'heure actuelle, 1 055 codes SANC sont attribués, et selon les indications reçues, 6 255 points sémaphores internationaux sont en service. 4. Pour que la Liste puisse être tenue à jour, les Administrations sont priées d'aviser le TSB, au moyen du formulaire de notification ci-joint, de toute attribution ou de retrait de code ISPC, www.itu.int/en/ITU-T/inr/forms/Pages/ispc.aspx . -

Financial Results 2018

Financial Results 2018 0 consolidation scope – general information The consolidated financial statements include the accounts of Sonatel and all its directly or indirectly controlled subsidiaries (see page 36). Subsidiaries are incorporated using the full consolidation method or the equity method of consolidation. Orange Sierra Leone owned at 50% is consolidated using the full consolidation method in accordance with the shareholders’ agreement. Orange Services Group “OSG” owned at 47% by Sonatel and its subsidiaries is accounted for in the consolidation scope using the equity method of consolidation as of June 2018. Transactions, balances and reciprocal incomes between integrated companies are eliminated. The consolidated financial statements are presented in XOF. Assets, liabilities and income statements of subsidiaries out of XOF zone are converted at the exchange rate prevailing at the closing period. The Group’s consolidated financial statements are prepared in accordance with the West African System of Accounting (SYSCOA), with a revised version effective since January 1, 2018 (SYSCOHADA). Sonatel 2018 Financial Results 1 warning This presentation contains information which may be deemed as forecasted information. Though the Company considers the statements and information rely on reasonable assumptions on the publication date of the present release, they are by nature subject to risks and uncertainties, which may give rise to a difference between the actual figures and those reported or induced in these statements or information. -

Orange Confirms Its Ambition to Achieve Digital Inclusion for All and Opens Its Second Orange Digital Center in Dakar

Press release Dakar, 24 October 2019 Orange confirms its ambition to achieve digital inclusion for all and opens its second Orange Digital Center in Dakar Today, in Dakar, Senegal, Orange is inaugurating its new concept of a place entirely dedicated to innovation, an “Orange Digital Center”. Several personalities attended the launch, including: Ms Ndèye Tické Ndiaye Diop, Minister for the Digital Economy and Telecommunications; Mr Dame Diop, Minister for Employment, Professional Training and Craftsmanship; Mr Alioune Ndiaye, CEO of Orange Africa and Middle-East; Ms Christine Albanel, Head of CSR, Diversity, Partnerships and Philanthropy for Orange, Deputy Chair of the Orange Foundation and former Minister; and Mr Sékou Dramé, CEO of Sonatel. Following on from Tunisia, Senegal will be home to the second Orange Digital Center in Africa and the Middle East. With a surface area of 2,000 m² on six floors, the Orange Digital Center in Dakar will be the first of its kind in West Africa. Working as a network, these places allow experiences and expertise to be shared between countries and offer a simple and inclusive approach to encourage innovation and entrepreneurship and to support the local digital ecosystem. The purpose of the Orange Digital Centers is to bring together several strategic programmes under the same roof: coding school, Solidarity FabLab, Orange Fab and Orange Digital Ventures Africa, the Group's investment fund. All of the programmes provided are free-of- charge and include digital training for young people, startup acceleration, and guidance for project owners and investment in these projects. Other centers are expected to open by the end of the year in Jordan,Cameroon and Côte d’Ivoire, with yet more in 2020 in Morocco and Egypt. -

The SAT-3/WASC Cable Senegal Case Study Ben Akoh1

The Case for “Open Access” Communications Infrastructure in Africa: The SAT-3/WASC cable Senegal case study Ben Akoh1 ASSOCIATION FOR PROGRESSIVE COMMUNICATIONS (APC) APC-200805-CIPP-R-EN-PDF-0047 ISBN 92-95049-49-7 COMMISSIONED BY THE ASSOCIATION FOR PROGRESSIVE COMMUNICATIONS (APC) CREATIVE COMMONS ATTRIBUTION-NONCOMMERCIAL-SHAREALIKE 3.0 LICENCE GRAPHICS: COURTESY OF AUTHOR 1Ben Akoh works extensively in the development and use of Free and Open Source Software in Africa and African content creation and knowledge management. He is also active in the development of policy and advocacy for favorable ICT environment in West Africa. APC Publications The Case for “Open Access” Communications Infrastructure in Africa: The SAT-3/WASC cable – Senegal Case Study i Table of Contents 1 Overview of report.............................................................................................. 4 2 Background .......................................................................................................... 5 2.1 Brief country profile..................................................................................... 5 2.2 Overview of Senegal’s telecommunications industry ............................ 7 2.3 History of the SAT-3/WASC cable in Senegal ...................................... 12 2.4 The impact of SAT-3/WASC in Senegal................................................. 14 3 Performance indicators – successes and failures.......................................... 17 3.1 Subscription, usage and capacity utilization......................................... -

Annual Report 2016

ANNUAL REPORT 2016 SONATEL A WORD FOR THE LEAST MYSTERIOUS Behind it lies more than an artistic or cultural movement. It alone crystallizes the emancipating will of an entire continent. Afro-futurists revisit history, biology, mythology and technology to reinvent Africa but above all, to give it the place it deserves in the world of tomorrow. Every day we work with you to prepare this world and prepare Africa to enter it. Tomorrow is getting prepared right now. 4 LETTER FROM THE CHAIRMAN 7 MESSAGE FROM THE MANAGING DIRECTOR 9 1 GOOD GOVERNANCE, PLEDGE FOR 12 TRANSPARENCY: GOOD GOVERNANCE RULES BOARD OF DIRECTORS – AUDIT COMMITTEE 2 HUMAN RESOURCES 26 3 SONATEL’S CITIZEN ENGAGEMENT 32 IN SENEGAL AND IN THE SUBSIDIARIES 3.1 Corporate Social Responsibility 34 3.2 Philanthropy 42 4 OUR ACTIVITIES 52 IN SENEGAL… 54 4.1 Mobile and Orange Money 54 4.2 Fixed-lines and Internet 57 4.3 Corporate Services 57 4.4 Contents: development and innovation 58 4.5 Commercial Service Transformation 60 4.6 Customer relation Transformation Project 64 … IN THE SUBSIDIARIES 66 4.7 Orange Mali 66 4.8 Orange Guinea 69 4.9 Orange Bissau 70 4.10 Starting of the activities in Sierra Leone 72 74 5 NETWORKS AND INFORMATION SYSTEMS 6 SONATEL IN THE WORLD 80 7 KEY NUMBERS AND SONATEL IN THE STOCK EXCHANGE 88 8 FINANCIAL REPORT 108 9 FINANCIAL STATEMENTS 140 10 APPENDIX 172 AUDITORS’ GENERAL AND SPECIAL REPORTS 174 AGENDA OF THE ORDINARY GENERAL MEETING 207 5 6 LETTER FROM THE CHAIRMAN onatel Group confirmed in 2016, its leadership and its good operational and financial results. -

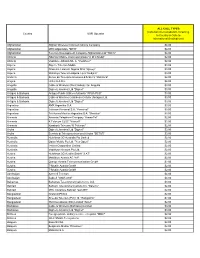

New Simplification Rates

ALL CALL TYPES (Calls back to Canada/US, Incoming, Country GSM Operator In Country & Calls to International Destinations) Afghanistan Afghan Wireless Communications Company $4.00 Afghanistan MTN Afganistan, "MTN" $4.00 Afghanistan Telecom Development Company Afghanistan Ltd "TDCA" $4.00 Albania Albanian Mobile Communications "A M C Mobil" $2.00 Albania Vodafone Albania Sh. A. "Vodafone" $2.00 Algeria Algerie Telecom Mobile $3.00 Algeria Orascom Telecom Algeria SPA "Djezzy" $3.00 Algeria Wataniya Telecom Algerie s.p.a."Nedjma" $3.00 Andorra Servei de Telecomunicacions d'Andorra "Mobiland" $2.00 Angola Unitel S.A.R.L. $4.00 Anguilla Cable & Wireless (West Indies) Ltd. Anguilla $3.00 Anguilla Digicel (Jamaica) Ltd "Digicel" $3.00 Antigua & Barbuda Antigua Public Utilities Authority "APUA PCS" $3.00 Antigua & Barbuda Cable & Wireless Caribbean Cellular (Antigua) Ltd. $3.00 Antigua & Barbuda Digicel (Jamaica) Ltd "Digicel" $3.00 Argentina AMX Argentina S.A. $3.00 Argentina Telecom Personal S.A. "Personal" $3.00 Argentina Telefonica Moviles Argentina S.A. "Movistar" $3.00 Armenia Armenia Telephone Company "ArmenTel" $2.00 Armenia K Telecom CJSC "Vivacell" $2.00 Armenia Karaback Telecom "K Telecom" $2.00 Aruba Digicel (Jamaica) Ltd "Digicel" $3.00 Aruba Servicio di Telecomunicacion di Aruba "SETAR" $3.00 Australia Hutchison 3G Australia Pty Limited $2.00 Australia Optus Mobile Pty Ltd. "Yes Optus" $2.00 Australia Telstra Corporation Limited $2.00 Australia Vodafone Network Pty Ltd. $2.00 Austria Hutchison 3G Austria GmbH "3 AT" $2.00 Austria Mobilkom Austria AG "A1" $2.00 Austria Orange Austria Telecommunication GmbH $2.00 Austria T-Mobile Austria GmbH $2.00 Austria T-Mobile Austria GmbH $2.00 Azerbaijan Azercell Telecom $4.00 Azerbaijan Bakcell "GSM 2000" $4.00 Bahamas Bahamas Telecommunications Co. -

Telecoms 150 2020

Telecoms 150 2020The annual report on the most valuable and strongest telecom brands April 2020 Contents. About Brand Finance 4 Get in Touch 4 Brandirectory.com 6 Brand Finance Group 6 Foreword 8 Brand Value Analysis 10 Regional Analysis 16 Brand Strength Analysis 18 Brand Finance Telecoms Infrastructure 10 20 Sector Reputation Analysis 22 Brand Finance Telecoms 150 (USD m) 24 Definitions 28 Brand Valuation Methodology 30 Market Research Methodology 31 Stakeholder Equity Measures 31 Consulting Services 32 Brand Evaluation Services 33 Communications Services 34 Brand Finance Network 36 brandirectory.com/telecoms Brand Finance Telecoms 150 April 2020 3 About Brand Finance. Brand Finance is the world's leading independent brand valuation consultancy. Request your own We bridge the gap between marketing and finance Brand Value Report Brand Finance was set up in 1996 with the aim of 'bridging the gap between marketing and finance'. For more than A Brand Value Report provides a 20 years, we have helped companies and organisations of all types to connect their brands to the bottom line. complete breakdown of the assumptions, data sources, and calculations used We quantify the financial value of brands We put 5,000 of the world’s biggest brands to the test to arrive at your brand’s value. every year. Ranking brands across all sectors and countries, we publish nearly 100 reports annually. Each report includes expert recommendations for growing brand We offer a unique combination of expertise Insight Our teams have experience across a wide range of value to drive business performance disciplines from marketing and market research, to and offers a cost-effective way to brand strategy and visual identity, to tax and accounting. -

ITU Operational Bulletin 1098

ITU Operational Bulletin www.itu.int/itu-t/bulletin No. 1098 15.IV.2016 (Information received by 31 March 2016) ISSN 1564-5223 (Online) Place des Nations CH-1211 Standardization Bureau (TSB) Radiocommunication Bureau (BR) Genève 20 (Switzerland) Tel: +41 22 730 5211 Tel: +41 22 730 5560 Tel: +41 22 730 5111 Fax: +41 22 730 5853 Fax: +41 22 730 5785 E-mail: [email protected] E-mail: [email protected] / [email protected] E-mail: [email protected] Table of Contents Page General information Lists annexed to the ITU Operational Bulletin: Note from TSB ...................................................................... 3 Approval of ITU-T Recommendations ............................................................................................................ 4 Data Transmission Service (Recommendation ITU-T X.121 (10/2000)): Senegal (Autorité de Régulation des Télécommunications et des Postes (ARTP), Dakar) ........................ 5 Telephone Service Armenia (Ministry of Transport and Communication, Yerevan) ............................................................... 6 Croatia (Croatian Regulatory Authority for Network Industries (HAKOM), Zagreb) ................................ 18 Denmark (Danish Energy Agency, Copenhagen) ...................................................................................... 22 Senegal (Autorité de Régulation des Télécommunications et des Postes (ARTP), Dakar) ........................ 23 Legal time change Azerbaijan (Ministry of Communications and High Technologies, Baku) ................................................ -

Final List of Participants

Plenipotentiary Conference (PP-06) Antalya, 6-24 November 2006 Final list of participants 1) Member States 2) Observers - Resolution 99 (PP-98) 3) Observers - United Nations and its Specialized Agencies 4) Observers - Regional Telecommunication Organizations 5) Observers - Recognized Operating Agencies (CV229) invited pursuant to Number 269E of the Convention 6) Observers - Scientific or Industrial Organizations (CV229) invited pursuant to Number 269E of the Convention 7) Observers - Regional and other International Organizations (CV231) invited pursuant to Number 269E of the Convention vendredi, 24. novembre 2006 Page 1 of 48 1) MEMBER STATES Afghanistan C H.E. Mr Mr. Amirzai SANGIN, Minister of Communications, Ministry of Communications, [email protected], Box: 621 CA H.E. Mr Mr. Baryalai HASSAM, Deputy Minister " Technical ", Ministry of Communications, [email protected], Box: 282 D Mr Mr. Ajmal AYAN, Director of Research & Development, Ministry of Communications, [email protected], Box: 283 D Mr Oliver ODZIGGEL, Advisor to Atra, Ministry of Communications, [email protected], Box: 3397 Albania C Mr Etion KAPEDANI, Director of Information Technology, Delegation of Albania, [email protected], Box: 3345 D Mr Hydajet KOPANI, Executive Director, Delegation of Albania, [email protected], Box: 3346 D Mr Arian SINOIMERI, Tre Board Memeber, Telecommunication Regulatory Entity, [email protected] Algeria C H.E. Mr Boudjemaa HAICHOUR, Ministre de la Poste et des Technologies de l'information et de la Communication, Ministère -

Data Roaming Rates for Customers Using Old Sim

DATA ROAMING RATES FOR CUSTOMERS USING OLD SIM Country Operator USD Price per MB per 100 kb Afghanistan Telecom Development Company Afghanistan Ltd (TDCA) 16.3650 1.60 Albania Albanian Mobile Communications (A M C MOBIL) 0.2219 0.02 Algeria Orascom Telecom Algerie Spa (Djezzy) 0.3810 0.04 Andorra S.T.A (Mobiland) 17.6222 1.72 Angola Movicel 24.5264 2.40 Anguilla Cable & Wireless (West Indies) Ltd. Anguilla 20.2449 1.98 Antigua & Barbuda Cable & Wireless Caribbean Cellular (Antigua) Limited 18.9231 1.85 Argentina Telecom Personal SA (Personal) 1.7736 0.17 Armenia K-Telecom Vivacel 14.4581 1.41 Australia Singtel Optus Limited (YES OPTUS) 0.1584 0.02 Austria ONE GMBH 0.1400 0.01 Austria Mobilkom Austria AG & Co KG (A1) 0.1400 0.01 Austria T-Mobile + ex Telering 0.1400 0.01 Azerbaijan, Republic of J.V.Bakcell (BAKCELL GSM 2000) 0.2213 0.02 Bahamas The Bahamas Telecommunications Company Ltd 21.0269 2.05 Bahrain Batelco (BHR MOBILE PLUS) 0.4844 0.05 Bangladesh TM Int'l (Bangladesh) Ltd (AKTEL) 15.2073 1.49 Barbados Cable and wireless 18.9183 1.85 Belarus, Republic of Mobile Digital Communications (VELCOM) 22.4973 2.20 Belgium Belgacom Mobile (PROXIMUS) 0.1400 0.01 Belgium BASE NV/SA (KPN group belgium) 0.1400 0.01 Belgium Mobistar S.A. 0.1400 0.01 Belize Belize Telecommunications Ltd 22.5000 2.20 Benin GLOMobile 22.5000 2.20 Bermuda DIGITAL 0.5475 0.05 Bhutan Tashi InfoComm Ltd 37.5000 3.66 Bolivia Nuevatel 2.1692 0.21 Bosnia Herzegovina HT Mobile communication (ex Eronet Mobile) 7.9847 0.78 Botswana Orange Botswana 22.5000 2.20 Brazil Oi (TNL