Management's Discussion and Analysis of Financial Condition and Results of Operations

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Annual-Report-2020.Pdf

LAPORAN TAHUNAN LAPORAN TAHUNAN 2020 ANNUAL REPORT 2020 ANNUAL REPORT ANNUAL Kantor Pusat Headquarters Jl. Rungkut Industri Raya No.18 Surabaya 60293, Indonesia Telephone: +62-31-8431-699 Tbk. PT HM SAMPOERNA Facsimile: +62-31-8430-986 Kantor Perwakilan di Jakarta Corporate Representative Office in Jakarta One Pacific Place, 18th Floor Sudirman Central Business District (SCBD) Jl. Jend. Sudirman Kav.52-53 Jakarta 12190, Indonesia PT HM SAMPOERNA Tbk. Telephone: +62-21-5151-234 Facsimile: +62-21-5152-234 Website: www.sampoerna.com 2020 Email: [email protected] LAPORAN TAHUNAN | ANNUAL REPORT LAPORAN TAHUNAN LAPORAN TAHUNAN LAPORAN TAHUNAN 2020 ANNUAL REPORT 2020 ANNUAL REPORT ANNUAL Kantor Pusat Headquarters Jl. Rungkut Industri Raya No.18 Surabaya 60293, Indonesia Telephone: +62-31-8431-699 PT HM S Facsimile: +62-31-8430-986 Kantor Perwakilan di Jakarta Corporate Representative Office in Jakarta AMPOERNA One Pacific Place, 18th Floor Sudirman Central Business District (SCBD) Jl. Jend. Sudirman Kav.52-53 Jakarta 12190, Indonesia Telephone: +62-21-5151-234 Tbk. Facsimile: +62-21-5152-234 Website: www.sampoerna.com Email: [email protected] 2020 LAPORAN TAHUNAN | ANNUAL REPORT Daftar Isi Contents Ikhtisar Highlights Sekilas Sampoerna 4 Sampoerna at a Glance Fakta-fakta Penting 2020 6 2020 Key Facts Ikhtisar Utama 2020 8 Key Highlights 2020 Kinerja Utama dan Ikhtisar Keuangan 14 Key Performance and Financial Highlights Ikhtisar Saham 15 Stock Highlights Penghargaan dan Sertifikasi 16 Awards and Certifications -

Labour Migration from Indonesia

LABOUR MIGRATION FROM INDONESIA IOM is committed to the principle that humane and orderly migration benets migrants and society. As an intergovernmental body, IOM acts with its partners in the international community to assist in meeting the operational challenges of migration; advance understanding of migration issues; encourage social and economic development through migration; and uphold the human dignity and wellbeing of migrants. This publication is produced with the generous nancial support of the Bureau of Population, Refugees and Migration (United States Government). Opinions expressed in this report are those of the contributors and do not necessarily reect the views of IOM. All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise without the prior written permission of the publisher: International Organization for Migration Mission in Indonesia LABOUR MIGRATION FROM INDONESIA Sampoerna Strategic Square, North Tower Floor 12A Jl. Jend. Sudirman Kav. 45-46 An Overview of Indonesian Migration to Selected Destinations in Asia and the Middle East Jakarta 12930 Indonesia © 2010 International Organization for Migration (IOM) IOM International Organization for Migration IOM International Organization for Migration Labour Migration from Indonesia TABLE OF CONTENTS ACKNOWLEDGMENTS vii PREFACE ix EXECUTIVE SUMMARY xi ABBREVIATIONS AND ACRONYMS 1 INTRODUCTION 3 Purpose 3 Terminology 3 Methodology -

Appendix 1. Categorization of Cigarette Brands As Either Premium Or Discount

Appendix 1. Categorization of Cigarette Brands as either Premium or Discount Category Name of Cigarette Brand Premium Accord, American Spirit, Barclay, Belair, Benson & Hedges, Camel, Capri, Carlton, Chesterfield, Davidoff, Du Maurier, Dunhill, Dunhill International, Eve, Kent, Kool, L&M, Lark, Lucky Strike, Marlboro, Max, Merit, Mild Seven, More, Nat Sherman, Newport, Now, Parliament, Players, Quest, Rothman’s, Salem, Sampoerna, Saratoga, Tareyton, True, Vantage, Virginia Slims, Winston, Raleigh, Business Club Full Flavor, Ronhill, Dreams Discount 24/7, 305, 1839, A1, Ace, Allstar, Allway Save, Alpine, American, American Diamond, American Hero, American Liberty, Arrow, Austin, Axis, Baileys, Bargain Buy, Baron, Basic, Beacon, Berkeley, Best Value, Black Hawk, Bonus Value, Boston, Bracar, Brand X, Brave, Brentwood, Bridgeport, Bronco, Bronson, Bucks, Buffalo, BV, Calon, Cambridge, Campton, Cannon, Cardinal, Carnival, Cavalier, Champion, Charter, Checkers, Cherokee, Cheyenne, Cimarron, Circle Z, Class A, Classic, Cobra, Complete, Corona, Courier, CT, Decade, Desert Gold, Desert Sun, Discount, Doral, Double Diamond, DTC, Durant, Eagle, Echo, Edgefield, Epic, Esquire, Euro, Exact, Exeter, First Choice, First Class, Focus, Fortuna, Galaxy Pro, Gauloises, Generals, Generic/Private Label, Geronimo, Gold Coast, Gold Crest, Golden Bay, Golden, Golden Beach, Golden Palace, GP, GPC, Grand, Grand Prix, G Smoke, GT Ones, Hava Club, HB, Heron, Highway, Hi-Val, Jacks, Jade, Kentucky Best, King Mountain, Kingsley, Kingston, Kingsport, Knife, Knights, -

Altria.Com/Proxy

6601 West Broad Street Richmond, Virginia 23230 Dear Fellow Shareholder: It is my pleasure to invite you to join us at the 2016 Annual Meeting of Shareholders of Altria Group, Inc. to be held on Thursday, May 19, 2016 at 9:00 a.m., Eastern Time, at the Greater Richmond Convention Center, 403 North 3rd Street, Richmond, Virginia 23219. At this year’s meeting, we will vote on the election of 11 directors, the ratification of the selection of PricewaterhouseCoopers LLP as the Company’s independent registered public accounting firm and, if properly presented, two shareholder proposals. We will also conduct a non-binding advisory vote to approve the compensation of the Company’s named executive officers. There also will be a report on the Company’s business, and shareholders will have an opportunity to ask questions. To attend the meeting, an admission ticket and government-issued photo identification are required. To request an admission ticket, please follow the instructions on page 9 in response to Question 16. One immediate family member who is 21 years of age or older may accompany a shareholder as a guest. We use the U.S. Securities and Exchange Commission rule that allows companies to furnish proxy materials to their shareholders over the Internet. We believe this expedites shareholders receiving proxy materials, lowers costs and conserves natural resources. We thus are mailing to many shareholders a Notice of Internet Availability of Proxy Materials, rather than a paper copy of the Proxy Statement and our Annual Report on Form 10-K for the fiscal year ended December 31, 2015. -

Altria Group, Inc. Annual Report

Altria Group, Inc. 2019 Annual Report an Altria Company an Altria Company an Altria Company an Altria Company an Altria Company an Altria Company an Altria Company an Altria Company an Altria Company an Altria Company an Altria Company an Altria Company an Altria Company an Altria Company an Altria Company an Altria Company an Altria Company an Altria Company an Altria Company an Altria Company an Altria Company an Altria Company an Altria Company an Altria Company an Altria Company Howard A. Willard III Dear Fellow Shareholders Chairman of the Board and CEO Altria delivered solid performance in a dynamic year for the tobacco industry. Our core tobacco businesses delivered outstanding financial performance, and we made significant progress advancing our non-combustible product platform. We believe Altria’s enhanced business platform positions us well for future success. 2019 Highlights n Grew adjusted diluted earnings per share (EPS) by 5.8%, primarily driven by our core tobacco businesses; and types of legal cases pending against it, especially during the fourth n Achieved $600 million in annualized cost savings, exceeding our $575 quarter of the year. Altria recorded two impairment charges of our JUUL million target announced in December 2018; asset in 2019, reducing our investment to $4.2 billion at year-end, down from n Increased our regular quarterly dividend for the 54th time in 50 years $12.8 billion, our 2019 initial investment. JUUL remains the U.S. leader in the and paid shareholders approximately $6.1 billion in dividends; and e-vapor category, and in January 2020 we revised certain terms governing n Repurchased 16.5 million Altria shares for a total cost of $845 million. -

Altria Group, Inc. Annual Report

ananan Altria Altria Altria Company Company Company an Altria Company ananan Altria Altria Altria Company Company Company | Inc. Altria Group, Report 2020 Annual an Altria Company From tobacco company To tobacco harm reduction company ananan Altria Altria Altria Company Company Company an Altria Company ananan Altria Altria Altria Company Company Company an Altria Company Altria Group, Inc. Altria Group, Inc. | 6601 W. Broad Street | Richmond, VA 23230-1723 | altria.com 2020 Annual Report Altria 2020 Annual Report | Andra Design Studio | Tuesday, February 2, 2021 9:00am Altria 2020 Annual Report | Andra Design Studio | Tuesday, February 2, 2021 9:00am Dear Fellow Shareholders March 11, 2021 Altria delivered outstanding results in 2020 and made steady progress toward our 10-Year Vision (Vision) despite the many challenges we faced. Our tobacco businesses were resilient and our employees rose to the challenge together to navigate the COVID-19 pandemic, political and social unrest, and an uncertain economic outlook. Altria’s full-year adjusted diluted earnings per share (EPS) grew 3.6% driven primarily by strong performance of our tobacco businesses, and we increased our dividend for the 55th time in 51 years. Moving Beyond Smoking: Progress Toward Our 10-Year Vision Building on our long history of industry leadership, our Vision is to responsibly lead the transition of adult smokers to a non-combustible future. Altria is Moving Beyond Smoking and leading the way by taking actions to transition millions to potentially less harmful choices — a substantial opportunity for adult tobacco consumers 21+, Altria’s businesses, and society. To achieve our Vision, we are building a deep understanding of evolving adult tobacco consumer preferences, expanding awareness and availability of our non-combustible portfolio, and, when authorized by FDA, educating adult smokers about the benefits of switching to alternative products. -

North Dakota Office of State Tax Commissioner Tobacco Directory List of Participating Manufacturers (Listing by Brand) As of May 24, 2019

North Dakota Office of State Tax Commissioner Tobacco Directory List of Participating Manufacturers (Listing by Brand) As of May 24, 2019 **RYO: Roll-Your-Own Brand Name Manufacturer 1839 U.S. Flue-Cured Tobacco Growers, Inc. 1839 RYO U.S. Flue-Cured Tobacco Growers, Inc. 1st Class U.S. Flue-Cured Tobacco Growers, Inc. American Bison RYO Wind River Tobacco Company, LLC Amsterdam Shag RYO Peter Stokkebye Tobaksfabrik A/S Ashford RYO Von Eicken Group Bali Shag RYO Commonwealth Brands, Inc. Baron American Blend Farmer’s Tobacco Co of Cynthiana, Inc. Basic Philip Morris USA, Inc. Benson & Hedges Philip Morris USA, Inc. Black & Gold Sherman’s 1400 Broadway NYC, LLC Bo Browning RYO Top Tobacco, LP Bugler RYO Scandinavian Tobacco Group Lane Limited Bull Brand RYO Von Eicken Group Cambridge Philip Morris USA, Inc. Camel R.J. Reynolds Tobacco Company Camel Wides R.J. Reynolds Tobacco Company Canoe RYO Wind River Tobacco Company, LLC Capri R.J. Reynolds Tobacco Company Carlton R.J. Reynolds Tobacco Company CF Straight Virginia RYO Von Eicken Group Charles Fairmon RYO Von Eicken Group Chesterfield Philip Morris USA, Inc. Chunghwa Konci G & D Management Group (USA) Inc. Cigarettellos Sherman’s 1400 Broadway NYC, LLC Classic Sherman’s 1400 Broadway NYC, LLC Classic Canadian RYO Top Tobacco, LP Commander Philip Morris USA, Inc. Crowns Commonwealth Brands Inc. Custom Blends RYO Wind River Tobacco Company, LLC Brand Name Manufacturer Danish Export RYO Peter Stokkebye Tobaksfabrik A/S Dark Fired Shag RYO Von Eicken Group Dave’s Philip Morris USA, Inc. Davidoff Commonwealth Brands, Inc. Djarum P.T. -

Negativliste. Tobaksselskaber. Oktober 2016

Negativliste. Tobaksselskaber. Oktober 2016 Læsevejledning: Indrykket til venstre med fed tekst fremgår koncernen. Nedenunder, med almindelig tekst, fremgår de underliggende selskaber, som der ikke må investeres i. Alimentation Couche Tard Inc Alimentation Couche-Tard Inc Couche-Tard Inc Alliance One International Inc Alliance One International Inc Altria Group Inc Altria Client Services Inc Altria Consumer Engagement Services Inc Altria Corporate Services Inc Altria Corporate Services International Inc Altria Enterprises II LLC Altria Enterprises LLC Altria Finance Cayman Islands Ltd Altria Finance Europe AG Altria Group Distribution Co Altria Group Inc Altria Import Export Services LLC Altria Insurance Ireland Ltd Altria International Sales Inc Altria Reinsurance Ireland Ltd Altria Sales & Distribution Inc Altria Ventures Inc Altria Ventures International Holdings BV Batavia Trading Corp CA Tabacalera Nacional Fabrica de Cigarrillos El Progreso SA Industria de Tabaco Leon Jimenes SA Industrias Del Tabaco Alimentos Y Bebidas SA International Smokeless Tobacco Co Inc National Smokeless Tobacco Co Ltd Philip Morris AB Philip Morris Albania Sh pk Philip Morris ApS Philip Morris Asia Ltd Philip Morris Baltic UAB Philip Morris Belgium BVBA Philip Morris Belgium Holdings BVBA Philip Morris Belgrade doo Philip Morris BH doo Philip Morris Brasil SA Philip Morris Bulgaria EEOD Philip Morris Capital Corp Philip Morris Capital Corp /Rye Brook Philip Morris Chile Comercializadora Ltda Philip Morris China Holdings SARL Philip Morris China Management -

Complete Annual Report

Philip Morris International 2016 Annual Report THIS CHANGES EVERYTHING 2016 Philip Morris Annual Report_LCC/ANC Review Copy February 22 - Layout 2 We’ve built the world’s most successful cigarette company with the world’s most popular and iconic brands. Now we’ve made a dramatic decision. We’ve started building PMI’s future on breakthrough smoke-free products that are a much better choice than cigarette smoking. We’re investing to make these products the Philip Morris icons of the future. In these changing times, we’ve set a new course for the company. We’re going to lead a full-scale effort to ensure that smoke- free products replace cigarettes to the benefit of adult smokers, society, our company and our shareholders. Reduced-Risk Products - Our Product Platforms Heated Tobacco Products Products Without Tobacco Platform Platform 1 3 IQOS, using the consumables Platform 3 is based on HeatSticks or HEETS, acquired technology that features an electronic holder uses a chemical process to that heats tobacco rather Platform create a nicotine-containing than burning it, thereby 2 vapor. We are exploring two Platform creating a nicotine-containing routes for this platform: one 4 vapor with significantly fewer TEEPS uses a pressed with electronics and one harmful toxicants compared to carbon heat source that, once without. A city launch of the Products under this platform cigarette smoke. ignited, heats the tobacco product is planned in 2017. are e-vapor products – without burning it, to generate battery-powered devices a nicotine-containing vapor that produce an aerosol by with a reduction in harmful vaporizing a nicotine solution. -

2009 Annual Report About PMI

2009 Annual Report About PMI Philip Morris International Inc. (PMI) is the leading inter- Contents 2 Highlights national tobacco company, with seven of the world’s top 3 Letter to Shareholders 15 brands, including Marlboro, the number one cigarette 6 2009 Business Highlights 8 Profitable Growth Through brand worldwide. PMI has more than 77,000 employees Innovation 16 Responsibility and its products are sold in approximately 160 coun- 17 Board of Directors/ tries. In 2009, the company held an estimated 15.4% Company Management 18 Financial Review share of the total international cigarette market outside 85 Comparison of Cumulative of the U.S., or 26.0% excluding the People’s Republic of Total Return 86 Reconciliation of China and the U.S. Non-GAAP Measures 88 Shareholder Information Highlights n Full-Year Reported Diluted Earnings per Share of $3.24 versus $3.31 in 2008 n Full-Year Reported Diluted Earnings per Share excluding currency of $3.77, up 13.9% n Full-Year Adjusted Diluted Earnings per Share of $3.29 versus $3.31 in 2008 n Full-Year Adjusted Diluted Earnings per Share excluding currency of $3.82, up 15.4% n During 2009, PMI repurchased 129.7 million shares of its common stock for $5.5 billion n PMI increased its regular quarterly dividend during 2009 by 7.4%, to an annualized rate of $2.32 per share n In July 2009, PMI announced an agreement to purchase the Colombian cigarette manufacturer, Productora Tabacalera de Colombia, Protabaco Ltda., for $452 million n In September 2009, PMI acquired Swedish Match South Africa (Proprietary) Limited, for approximately $256 million n In February 2010, PMI announced a new share repurchase program of $12 billion over 3 years n In February 2010, PMI announced the creation of a new company in the Philippines resulting from the unification of the business operations of Fortune Tobacco Corporation and Philip Morris Philippines Manufacturing Inc. -

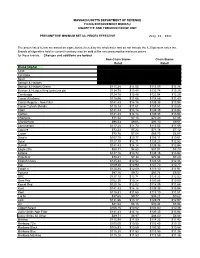

Cigarette Minimum Retail Price List

MASSACHUSETTS DEPARTMENT OF REVENUE FILING ENFORCEMENT BUREAU CIGARETTE AND TOBACCO EXCISE UNIT PRESUMPTIVE MINIMUM RETAIL PRICES EFFECTIVE July 26, 2021 The prices listed below are based on cigarettes delivered by the wholesaler and do not include the 6.25 percent sales tax. Brands of cigarettes held in current inventory may be sold at the new presumptive minimum prices for those brands. Changes and additions are bolded. Non-Chain Stores Chain Stores Retail Retail Brand (Alpha) Carton Pack Carton Pack 1839 $86.64 $8.66 $85.38 $8.54 1st Class $71.49 $7.15 $70.44 $7.04 Basic $122.21 $12.22 $120.41 $12.04 Benson & Hedges $136.55 $13.66 $134.54 $13.45 Benson & Hedges Green $115.28 $11.53 $113.59 $11.36 Benson & Hedges King (princess pk) $134.75 $13.48 $132.78 $13.28 Cambridge $124.78 $12.48 $122.94 $12.29 Camel All others $116.56 $11.66 $114.85 $11.49 Camel Regular - Non Filter $141.43 $14.14 $139.35 $13.94 Camel Turkish Blends $110.14 $11.01 $108.51 $10.85 Capri $141.43 $14.14 $139.35 $13.94 Carlton $141.43 $14.14 $139.35 $13.94 Checkers $71.54 $7.15 $70.49 $7.05 Chesterfield $96.53 $9.65 $95.10 $9.51 Commander $117.28 $11.73 $115.55 $11.56 Couture $72.23 $7.22 $71.16 $7.12 Crown $70.76 $7.08 $69.73 $6.97 Dave's $107.70 $10.77 $106.11 $10.61 Doral $127.10 $12.71 $125.23 $12.52 Dunhill $141.43 $14.14 $139.35 $13.94 Eagle 20's $88.31 $8.83 $87.01 $8.70 Eclipse $137.16 $13.72 $135.15 $13.52 Edgefield $73.41 $7.34 $72.34 $7.23 English Ovals $125.44 $12.54 $123.59 $12.36 Eve $109.30 $10.93 $107.70 $10.77 Export A $120.88 $12.09 $119.10 $11.91 -

Countervailing Effects of a Potential Ban on Menthol Cigarettes

Countervailing Effects of a Potential Ban on Menthol Cigarettes Joe Murillo – Vice President and Associate General Counsel Altria Client Services on behalf of PM USA February 10, 2011 Altria Client Services on behalf of PM USA | 2.10.2011 | 1 Brand Integrity’s Role & Strategies Role: To protect the integrity of Altria’s tobacco operating companies’ brands and the legitimate trade channels through which they are distributed and sold. Strategies: . Market Monitoring . Investigative Intelligence . Law Enforcement Engagement & Support . Litigation . Trade Compliance . Product Intelligence & Security . Legislation Altria Client Services on behalf of PM USA | 2.10.2011 | 2 Key Points of Dec. 30, 2010 Submission to FDA PM USA believes that banning menthol cigarettes could trigger a series of unintended consequences that would be detrimental to FDA’s public health objectives and to society more generally. These unintended consequences would likely include: . Significant expansion of the unregulated, illicit cigarette market . Increased organized crime . Increased burdens for law enforcement . An erosion in underage access prevention . Declining tax revenues and tobacco settlement payments to the states . Significant job losses within the legitimate distribution chain – from farmers to retail clerks; and . Self-mentholation of cigarettes Altria Client Services on behalf of PM USA | 2.10.2011 | 3 Unlicensed Manufacturing (Loosies) ATF New York - United States CBSA - Canada Source: Images provided to ALCS upon request by ATF & CBSA January 2011