Management's Discussion and Analysis

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

2013 GGP Fact Sheets.Indb

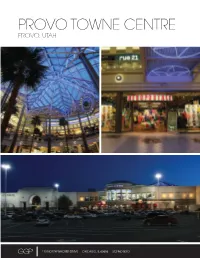

PROVO TOWNE CENTRE PROVO, UTAH 110 NORTH WACKER DRIVE CHICAGO, IL 60606 312 960 5000 PROPERTY HIGHLIGHTS MALL INFORMATION • Provo Towne Centre serves as the gateway into Northern LOCATION: I-15 and University Avenue cross streets Utah, conveniently located off the I-15 interstate and MARKET: Salt Lake City-Orem/Provo, Utah University Avenue. This artery receives an impressive average of 124,000 car counts daily. DESCRIPTION: Two-level, enclosed, regional center • Top performing categories include home furnishings and ANCHORS: Dillard’s, jcpenney, Sears, Cinemark Theatres accessories, health and beauty, jewelry and casual dining. OTHER FEATURES: 16-screen stadium-style theater, children’s soft • jcpenney underwent a key renovation in 2010, adding play area, 8-unit food court with children’s seating, and 1,900 square feet, including a Sephora department. fl oor-to-ceiling panoramic windows • Prompted by the changes in the Utah County retail TOTAL RETAIL SQUARE FOOTAGE: 801,601 landscape, Dillard’s now carries 30+ high-end brands new PARKING SPACES: 3,959 to the trade area. OPENED: 1998 • No state can match the consistent performance of Utah. It is the only state that ranks among Forbes’ top 15 states in each of six main categories: business costs, labor supply, TRADE AREA PROFILE regulatory environment, economic climate, growth prospect 2013 POPULATION 530,431 and quality of Life. (Forbes, November 2011) 2018 PROJECTED POPULATION 577,685 ALL ABOUT FAMILY 2013 HOUSEHOLDS 145,014 2018 PROJECTED HOUSEHOLDS 158,155 • Provo Towne Centre boasts over 70 family-inspired community events annually, including Provo City’s 15,000+ 2013 MEDIAN AGE 25.1 attendance New Year’s Eve event. -

Popular Annual Financial Report

2019 POPULAR ANNUAL FINANCIAL REPORT City of Provo, Utah FISCAL YEAR ENDED June 30, 2019 PROVO CITY, UTAH TABLE OF CONTENTS INTRODUCTION To the Citizens of Provo City ......................................................................................................................... 1 Provo at a Glance .......................................................................................................................................... 2 Elected Officials ............................................................................................................................................. 4 Key City Services .......................................................................................................................................... 5 Significant Events …. .................................................................................................................................... 6 Top Rankings ................................................................................................................................................ 7 FINANCIAL INFORMATION Statement of Net Position .............................................................................................................................. 8 Statement of Activities ................................................................................................................................... 9 General Fund Revenues ............................................................................................................................ -

FY 2013 School Vendor Totals

Provo City School District School Vendor Totals FY2012-2013 Vendor Name Sum of Amount 5 BUCK PIZZA $ 303.50 7 PEAKS $ 404.25 801 PROMOS $ 140.52 A+ BOOK FAIR $ 4,789.46 AATF $ 217.95 AATG $ 378.00 ABBOTT, DENISE $ 679.31 ABC-TEES INC $ 227.40 ABOUTFACE PROPERTIES $ 100.00 ABRAHAM TRISTAN $ 24.90 ABRAMS, JOHN $ 40.00 ACADEMIC INNOVATIONS, LLC $ 96.25 ACADEMY SPORTS $ 4,812.79 ACE RENTAL-OREM $ 48.95 ACHECAR, GEIDY $ 30.00 ACKROYD, DERRICK $ 4.00 ACOSTA, AIMEE $ 35.23 ACOSTA, SANDY $ 9.75 ACT $ 4,155.00 ADA BADMINTON & TENNIS $ 777.62 ADAIR, EMILY $ 16.00 ADAIR, JENNY $ 770.00 ADAMS, CECILIA $ 20.00 ADAMS, GABRIEL $ 16.00 ADAMS, LORRAINE $ 642.56 ADAMS, PATTY $ 80.00 ADAMS, TALIA $ 10.00 ADAMSON, KAYLA $ 13.25 ADSIT, JULIUS $ 6.00 ADVANCE EDUCATION, INC $ 1,494.43 AED PROFESSIONALS $ 297.50 AGGIE BASKETBALL CAMPS $ 2,000.00 AGILE SPORTS TECHNOLOGIES $ 2,800.00 AGUAYO, ALEX $ 16.00 AGUAYO, DANIELA $ 60.00 AGUAYO, EMILIA $ 15.00 AGUILAR, ABNER $ 6.50 AGUILERA, MAURICIO $ 54.00 AHN, SEONG JIN $ 20.00 AIRE-MASTER OF SO UTAH $ 525.00 ALAN ANDERSON $ 818.75 ALBACH, KURT $ 30.00 ALBERTSON, TANNER $ 4.00 ALDER, HAYLEY $ 92.00 ALEMAN MALDONADO, DANIEL $ 6.00 ALEXANDER'S PRINT ADVANTAGE $ 117.10 ALFARO, NICOLE $ 55.00 ALFRED PUBLISHING $ 20.00 ALGER, DEANNA $ 42.07 ALICIA HICKMAN $ 91.38 ALL EVENTS $ 450.00 ALL FOR KIDZ $ 2,605.96 ALL RESORT GROUP/LEWIS STAGES $ 5,030.00 ALL SPORTS UNIFORMS. NET $ 1,089.49 ALLAN, ASHLYN $ 249.67 ALLEN, GRACE $ 160.00 ALLEN, MIKE $ 113.20 ALLEN, NATHAN $ 38.64 ALLEN, SAMUEL $ 38.00 ALLENS $ 756.88 ALLEN'S CAMERA $ -

Provo City, Utah

Popular Annual Financial Report for the year ended June 30, 2018 2018 PAFR PROVO CITY, UTAH Table of Contents To the Citizens of Provo City ............................................................................................................ 1 Provo at a Glance ............................................................................................................................. 2 Meet the Elected Officials ................................................................................................................. 3 Key Services of Provo City................................................................................................................ 4 Significant Events of Provo City ........................................................................................................ 5 Statement of Net Position ................................................................................................................. 6 Statement of Activities ....................................................................................................................... 7 Where General Fund Money Comes From ....................................................................................... 8 Where General Fund Money Goes ................................................................................................... 9 General Fund, Fund Balance .......................................................................................................... 10 Library Fund ................................................................................................................................... -

Novell Management Tools

04 0789729849_ch03.qxd 11/10/03 12:43 PM Page 91 CHAPTER 3 Novell Management Tools Using ConsoleOne ConsoleOne is a Java-based tool for managing your network and its resources. It can be launched by running CONSOLEONE.EXE from where it was installed (default: SYS:PUBLIC\MGMT\CONSOLEONE\1.2\BIN). By default, it lets you manage Novell eDirectory objects, schema, parti- tions, and replicas and NetWare server resources. If you install other Novell products, the appropriate management capabil- ities are automatically snapped into the version of ConsoleOne installed on that server. ConsoleOne is installed during the NetWare 6.5 installation, but can also be re-installed or installed locally from the Novell client’s CD. ConsoleOne also supports remote server console access through a Java applet called RConsoleJ. To access the NetWare 6.5 server console remotely, launch ConsoleOne and browse to the desired server. Select Tools, and then Remote Console. Accessing Web Manager Web Manager is a Web-based “home page” for accessing most of the NetWare 6.5 Web-based tools and services. To access Web Manager, open your Web browser and enter your Web server’s domain name or IP address, followed by a colon and the Web Manager port, which by default is 2200. For example: 04 0789729849_ch03.qxd 11/10/03 12:43 PM Page 92 92 PART I Getting Started https://www.quills.com:2200 or https://137.65.192.1:2200 Accessing iManager iManager provides role-based management of your NetWare network, together with a nearly comprehensive set of administrative tools. -

Novell® Platespin® Recon 3.7.4 User Guide 5.6.4 Printing and Exporting Reports

www.novell.com/documentation User Guide Novell® PlateSpin® Recon 3.7.4 September 2012 Legal Notices Novell, Inc., makes no representations or warranties with respect to the contents or use of this documentation, and specifically disclaims any express or implied warranties of merchantability or fitness for any particular purpose. Further, Novell, Inc., reserves the right to revise this publication and to make changes to its content, at any time, without obligation to notify any person or entity of such revisions or changes. Further, Novell, Inc., makes no representations or warranties with respect to any software, and specifically disclaims any express or implied warranties of merchantability or fitness for any particular purpose. Further, Novell, Inc., reserves the right to make changes to any and all parts of Novell software, at any time, without any obligation to notify any person or entity of such changes. Any products or technical information provided under this Agreement may be subject to U.S. export controls and the trade laws of other countries. You agree to comply with all export control regulations and to obtain any required licenses or classification to export, re-export or import deliverables. You agree not to export or re-export to entities on the current U.S. export exclusion lists or to any embargoed or terrorist countries as specified in the U.S. export laws. You agree to not use deliverables for prohibited nuclear, missile, or chemical biological weaponry end uses. See the Novell International Trade Services Web page (http://www.novell.com/info/exports/) for more information on exporting Novell software. -

2020 Provo Campus

2020 Brigham Young University Annual Security and Fire Safety Reports ANNUAL SECURITY REPORT Contents ANNUAL SECURITY REPORT ........................................................................................................................... 1 Resource Phone Numbers ............................................................................................................................. 4 Message from Chris Autry ............................................................................................................................. 6 What Is the Clery Act? ................................................................................................................................... 7 Clery Act Annual Security Report Preparation .................................................................................................7 Collecting Crime Data and Reporting Procedures ........................................................................................... 8 Crime Log and Campus Warnings .....................................................................................................................8 2017-2019 Reported Crime Statistics ............................................................................................................. 9 BYU Campus Law Enforcement: BYU Police ................................................................................................. 11 BYU Police Mission Statement ...................................................................................................................... -

Housing Profile of Provo City: 2000 - 2010 3% Change

Provo City Parks and Recreation Master Plan December 2013 1 Acknowledgements The Provo City Parks and Recreation Master Plan was developed by Provo City’s Parks and Recreation Department with the technical expertise and design skills of PROS Consulting, LLC, and ETC/Leisure Vision Institute. Special thanks go to many residents, park users, and community leaders for their insight and support throughout this study. PROVO MAYOR AND MUNICIPAL COUNCIL PROVO PARKS AND RECREATION BOARD Mayor John Curtis Bill Bridges, Chair Gary Winterton, Chair Ross Salmon, Vice Chair Kay Van Buren, Vice Chair Michael Bateman Sterling Beck William Fillmore Laura Cabanilla Odell Miner Gary Garrett Marian Monnahan Rick Healey Dave Olpin Hal Miller Robin Roberts Tammy Runia Brian Smith PROVO CITY STAFF Wayne Parker, Chief Administrative Officer Shelliane White, Recreation Supervisor Roger Thomas, Director of Parks and Recreation Tucker Lougee, Recreation Supervisor Doug Robins, Parks Division Director Brian Smith, Community Programs/Events Supervisor Scott Henderson, Recreation Division Director Dean Hutchison, Parks Projects Coordinator Paul Duerden, Covey Center for the Arts Manager James Cornaby, Cemetery Sexton Matthew Brimhall, Parks Area Maintenance Supervisor Ron Adams, Parks Area Maintenance Supervisor Cathy Smits, Aquatics Supervisor Bill Peperone, Assistant Director of Community Development Penn Almoney, Recreation Supervisor RESIDENTS AND STAKEHOLDERS Steve Densley, Utah Valley Chamber of Commerce Joe Gledhill, Provo City School District Melanie McCoard -

Orem Moderate-Income Housing Study As Appendix I of the General Plan

CITY OF OREM CITY COUNCIL MEETING 56 North State Street, Orem, Utah October 23, 2018 This meeting may be held electronically to allow a Councilmember to participate. 4:30 P.M. WORK SESSION - CITY COUNCIL CONFERENCE ROOM ANNUAL REPORT - Orem Police Department Victim Advocates (10 min) Presentation of annual report Presenter: Renee Flitton DISCUSSION - Rank Choice Voting (30 min) Introduction and Discussion Presenter: Stan Lockhart 5:00 P.M. STUDY SESSION - CITY COUNCIL CONFERENCE ROOM 1. PREVIEW UPCOMING AGENDA ITEMS Staff will present to the City Council a preview of upcoming agenda items. 2. AGENDA REVIEW The City Council will review the items on the agenda. 3. CITY COUNCIL - NEW BUSINESS This is an opportunity for members of the City Council to raise issues of information or concern. 6:00 P.M. REGULAR SESSION - COUNCIL CHAMBERS 4. CALL TO ORDER 5. INVOCATION/INSPIRATIONAL THOUGHT: BY INVITATION 6. PLEDGE OF ALLEGIANCE: BY INVITATION 7. APPROVAL OF MINUTES 7.1. MINUTES - October 9, 2018 City Council Meeting - October 11, 2018 Joint City Council Meeting with Provo For Review and Approval 1 2018-10-09.ccmin DRAFT.pdf 2018-10-11.ccmin w Provo DRAFT.pdf 8. MAYOR’S REPORT/ITEMS REFERRED BY COUNCIL 8.1. UPCOMING EVENTS For Review Upcoming Events.pdf 8.2. REPORT - Orem Arts Council It is recommended that the City Council receive the annual report from the Orem Arts Council, a city commission. Presenter: Orem Arts Council 9. PERSONAL APPEARANCES – 15 MINUTES Time has been set aside for the public to express their ideas, concerns, and comments on items not scheduled as public hearings on the Agenda. -

H Plan Ordin Hearing Nning C Staff R Nance a Date

Planning Commission Staff Report Ordinance Amendment Hearing Date: January 9, 2013 ITEM 3* The Engineering Department requests an ammendment to Provo City Code, Sections 15.13.010 Names of Streets, 15.13.030 System to be Followed, and 15.13.040 Costs Related to Street Name Changes, in order to modify and update the sections relaated to Street Naming. City Wide Impact 12-0019OAO Appplicant: Provo City Engineering Current Legal Use: Not applicable Staff Coordinator: Carrie Walls Relevant History: Provo City Code Sections 15.13.010, Number of Properties: City-wide Impact 15.13.030, and 15.13.040 were repealed and reenacted in 1999. There have been no amendments to these sections since that time. *Council Action Required: Yes Neighborhood Issues: Staff is unaware of any Related Application(s): None neighborhood issues in regard to the proposed amendments. ALTERNATIVE ACTIONS 2. Continue to a future date to obtain Summary of Key Issues: additional information or to further consider information presented. The • The Code Sections were repealed and reenacted in next available meeting date is 1999. February13, 2013, at 5:00 p.m. • There have been no amendments sincee that time. 3. Recommend Denial of the Staff Recommendation: proposed ordinance amendment. This 1. Recommend Approval of the proposed ordinance would be a change from the Staff amendment. This action would be consistent with the recommendation; the Planning recommendation of the Staff Report. Any additional Commission should state new findings. changes should be stated with the motion OVERVIEW The current ordinances for the naming of streets, the system of address numbering and how the costs are recouped were repealed and reenacted in 1999. -

Winter 2015 FWA Newsletter

BRIGHAM YOUNG UNIVERSITY Faculty Women’s Association NEWSLETTER Fall 2014/Winter 2015 INSIDE 2 3 4 5 10 THIS A word from Upcoming By Study, By Recent FWA FWA our President Events Faith Publications Membership ISSUE About FWA Recap: Spring Application 2014-2015 2014 Annual Board Retreat 2 Dear Women, Our association welcomes you—all of you. As we continue this academic A WORD year on campus, it is our hope that many more of you will participate in the activities and camaraderie of the Faculty Women’s Association. Our theme—”Expressions of Faith: Women Fulfilling the Mission of BYU”— FROM OUR provides opportunity for spiritual uplift, professional support, and friend- ship. PRESIDENT We recognize that all women have busy schedules, but we ask that you give FWA a chance to bless your life. You will see wonderful examples of faithful women who are fulfilling the mission of BYU in diverse and “GIVE FWA A exemplary ways, while personally progressing and assisting the students they teach. Did I mention that we need your contribution? Experienced CHANCE TO faculty and administrators, new women faculty, part-time faculty, faculty from every college, clinical faculty, and even those who don’t fit a category, BLESS YOUR please come. LIFE.” We began the year by celebrating the anniversary of the HFAC with Janielle Christensen and enjoyed a historical review of women with vision who helped develop the musical performance groups at BYU, which have achieved high acclaim in the performing arts. Those in attendance heard some amazing music. We continued the year with a fun evening of watch- ing and cheering on the BYU Women’s Soccer Team. -

Student Exchange Program

student exchange program whitmore global management center marriott school brigham young university 1 contents 5 : about the university 6 : marriott school of management 10 : marriott school student resources 12 : byu campus 17 : useful information 19 : byu culture 21 : recreation and entertainment 2 Dear student, It has never been more important to be connected to the global economy than it is today. In spite of the global economic crisis and slowdown in world trade, the future of international business is still bright. Now more than ever, you will likely work in the global economy. You might be working abroad or working in your home country for either a local multinational corporation or for a foreign-based company that is enter- ing your market. Whatever your future brings, it will be important for you to understand how to negotiate foreign languages and culture. It is one thing to study a language in school, but you also need to get used to different countries and cultures as well. Cultural is broad, and language is just one aspect. BYU is a great place to study, because over 70 percent of our students speak a second language and many have lived abroad for a year or more. In your classes, you will be able to interact with students from other countries but also with U.S. students with broad international experience. In any given class, you will have classmates with international experience in multiple countries in all regions of the world. These students have gained a knowledge of and love for the people, language, and culture of places where they have lived.