ANNA Annual Report.Indd

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Chapter 1 Introduction

Chapter 1 Introduction 1 Capital Markets In India An Introduction: Capital is often defined as “wealth used in the production of further wealth.” In simple words, it comprises the money value invested in a business unit. Market is that place where buyer and sellers are contact to each other and when these two words are merging together make capital market A business enterprise can raise capital from various sources long-term funds can be raised either through issue of securities or by borrowing from certain institutions. Short- term funds can also be borrowed from various agencies. Thus business units can raise capital from issue of securities or by borrowings (long-term and short-term).The borrowers and lenders are brought together through the financial markets. The term „financial market‟ collectively refers to all those organizations and institutions which lend funds to business enterprises and public authorities. It is composed of two constituents. (i) The money market, (ii) The capital market. While the money market deals with the provision of short-term credit, the capital market deals in the lending and borrowing of medium-term and long-term and long-term credit. Structure of the capital market------------ two constituents. Broadly describe, the capital market can be divided into two constituents. (1) The financial institution:- e.g., IFCI, IDBI, SFCs, LIC, UTI etc. provide long-term and medium-term loan facilities. (2) The Securities Market:- The securities market is divided into (A) the gilt edged market and (B) the corporate securities market. 2 A) Gilt-Edged Market The gilt edged market is the market in government securities or the securities guaranteed (as to both principle and interest) by the government. -

Final Report Amending ITS on Main Indices and Recognised Exchanges

Final Report Amendment to Commission Implementing Regulation (EU) 2016/1646 11 December 2019 | ESMA70-156-1535 Table of Contents 1 Executive Summary ....................................................................................................... 4 2 Introduction .................................................................................................................... 5 3 Main indices ................................................................................................................... 6 3.1 General approach ................................................................................................... 6 3.2 Analysis ................................................................................................................... 7 3.3 Conclusions............................................................................................................. 8 4 Recognised exchanges .................................................................................................. 9 4.1 General approach ................................................................................................... 9 4.2 Conclusions............................................................................................................. 9 4.2.1 Treatment of third-country exchanges .............................................................. 9 4.2.2 Impact of Brexit ...............................................................................................10 5 Annexes ........................................................................................................................12 -

1048 Report of Special Study of Securities !V~Arkets

1048 REPORT OF SPECIAL STUDY OF SECURITIES !V~ARKETS TABLE VIII-29.--Size of large block, purchases and sales of stock,s by selected institutions (by size of block and type of institution, 1961) [Median value per block in thousands of dollars] Open-end investment College All insti- Pension Life Nonlife companies Closed-end endow- Founda- CoIilxnon Size of block tutions funds insurance ihsura~ce investment ment tions trust companies companies! companies funds funds Load No load purchases ......................................... 410 183 1, 000 621 1,324 614 473 378 504 $1,000,000 and over ........................... 1, 658 1, 172 1, 500 1, 500 2, 590 (~) 1,333 1,666 1,153......... Less than $1,000,000 .......................... 270 165 556 594 587 548 406 331 370 Listed stocks purchased primarily on exchanges.. 5O3 236 817 621 2, 429 771 658 437 478 $1,000,000 and over ........................... 1,807 1,221 1,400 2, 996 1,333 1, 048 1,160 ........... Less than $1,000,000 .......................... 347 175 698 616 776 630 379 366 242 Listed stocks purchased primarily over the counter ......................................... 311 198 794 ~93 1, 128 (~) 577 397 501 $1,000,000 and over ........................... 1, 605 1, 079 1, 537 3, 215 0) O) Less than $1,000,000 .......................... 257 180 282 772 (9 411 237 478 Unlisted stocks purchased over the counter ....... 384 161 1, 000 627 1, 127 257 421 262 685 $1,000,000 and over ........................... 1, 600 1,500 l, 260 1, 600 (9 O) Less than $1,000,000 .......................... 246 152 567 568 257 401 246 £11 sales ............................................. -

Background- Madoff Page 1 of 1

Background- Madoff Page 1 of 1 Background - Madoff 3/28/20054:14:32 PM ~rom: Ostrow, Will To: Lamore, Peter Personal Privacy Attachments: image001.jpg Taken ~om httD://www.hofstra.edu/alumdev/alumni/alu aaa.cfm Bernard L. Madoff'60 The same year as his graduation from Hofstra, Bernard L. Madoff, Class of 1960, founded a successful investment firm that bears his name. Madoff Securities currently ranks among the top 1 percent of U.S. securities firms and is the third largest firm matching buyers and sellers of New York Stock Exchange and Nasdaq securities. While building his firm into a significant force in the securities industry, Bernard and his family have been deeply involved in leading the dramatic transformation that is currently underway in U.Si securities trading. Bernard has been a major figure in the National Association of Securities Dealers (NASD), the major self-regulato~y organization for U.S. broker/dealer fums. He is credited with being one of the five broker/dealers most closely involved in developing the Nasdaq Stock Market. He has served as chairman of the board of directors of the Nasdaq Stock Market as well as a member of the board of governors of the NASD and a member of numerous NASD committees. Bernard has also served as a member of the board of directors of the Securities Industry Association. In 1983 Madoff Securities opened a London office, which quickly became one of the first U.S. members of the London Stock Exchange. Bernard was also a founding member of the board of directors of the International Securities Clearing Corporation in London. -

FEDERAL REGISTER VOLUME 34 • NUMBER 224 Friday, November 21, 1969 • Washington, D.C

FEDERAL REGISTER VOLUME 34 • NUMBER 224 Friday, November 21, 1969 • Washington, D.C. Pages 18515-18580 Agencies in this issue— Business and Defense Services Administration Civil Aeronautics Board Consumer and Marketing Service Federal Aviation Administration Federal Communications Commission Federal Power Commission Federal Railroad Administration Food and Drug Administration Hazardous Materials Regulations Board Health, Education, and Welfare Department Internal Revenue Service Interstate Commerce Commission Land Management Bureau Monetary Offices Pipeline Safety Office Post Office Department Securities and Exchange Commission Small Business Administration MICROFILM EDITION FEDERAL REGISTER 35mm MICROFILM Complete Set 19 3 6 -6 8 ,174 Rolls $1,224 Vol. Year Price Vol. Year Price Vol. Year Price 1 1936 $8 12 1947 $26 23 1958 $36 2 1937 10 13 1948 27 24 1959 40 3 1938 9 14 1949 22 25 1960 49 4 1939 14 15 1950 26 26 1961 46 5 1940 15 16 1951 43 27 1962 50 6 1941 20 17 1952 35 28 1963 49 7 1942 35 18 1953 32 29 1964 57 8 1943 52 19 1954 39 .30 1965 58 9 1944 42 20 1955 36 31 1966 61 10 1945 43 21 1956 38 32 1967 64 11 1946 42 22 1957 38 33 v 1968 62 Order Microfilm Edition from Publications Sales Branch National Archives and Records Service Washington, D.C. 20408 tr TSi Published daily, Tuesday through Saturday (no publication on Sundays, Mondays, or FEDERAL^pEGISTER on the day after an official Federal holiday), by the Office of the Federal Register, National Archives and Records Service, General Services Administration, Washington, D.O. -

Doing Data Differently

General Company Overview Doing data differently V.14.9. Company Overview Helping the global financial community make informed decisions through the provision of fast, accurate, timely and affordable reference data services With more than 20 years of experience, we offer comprehensive and complete securities reference and pricing data for equities, fixed income and derivative instruments around the globe. Our customers can rely on our successful track record to efficiently deliver high quality data sets including: § Worldwide Corporate Actions § Worldwide Fixed Income § Security Reference File § Worldwide End-of-Day Prices Exchange Data International has recently expanded its data coverage to include economic data. Currently it has three products: § African Economic Data www.africadata.com § Economic Indicator Service (EIS) § Global Economic Data Our professional sales, support and data/research teams deliver the lowest cost of ownership whilst at the same time being the most responsive to client requests. As a result of our on-going commitment to providing cost effective and innovative data solutions, whilst at the same time ensuring the highest standards, we have been awarded the internationally recognized symbol of quality ISO 9001. Headquartered in United Kingdom, we have staff in Canada, India, Morocco, South Africa and United States. www.exchange-data.com 2 Company Overview Contents Reference Data ............................................................................................................................................ -

Summary of Transcript of Proceedings in the Matter of Commission Rate Structures of Registered National Securities Exchanges

SUMMARY OF TRANSCRIPT OF PROCEEDINGS IN THE MATTER OF COMMISSION RATE STRUCTURES OF REGISTERED NATIONAL SECURITIES EXCHANGES July 1, 1968 -- July 31, 1968 Office of Regulation Division of Trading and Markets Securities and Exchange Commission SCHEDULE OF WITNESSES MATTER OF COMMISSION RATE STRUCTURE OF REGISTERED NATIONAL SECURITIES EXCHANGES 1. Robert M. Bishop -- NYSE -- July 1, 1968 2. Pershing & Company -- July 2, 1968 3. Michael J. Heaney & Co. -- July 2, 1968 4. Jefferies & Co., Inc. -- July 3, 1968 5. Dominick & Dominick -- July 3, 1968 6. Reynolds & Company -- July 8, 1968 % Bache & Company -- July 8, 1968 8. Paine, Webber, Jackson & Curtis -- July 9, 1968 9. Salomon Brothers & Hutzler -- July 9, 1968 10. Donaldson Lufkin & Jenrette, Inc. -- July 10, 1968 11. Cantella & Company, Inc. -- July 10, 1968 12. A. I. Jablonski & Company -- July 11, 1968 13. Harry C. Dackerman & Company, Inc. -- July 11, 1968 14. A. G. Becker & Co., Inc. -- July 15, 1968 15. Ralph W. Davis & Company (Scott Davis) -- July 15, 1968 16. Mitchum, Jones & Templeton, Inc. -- July 16, 1968 1% Stifel, Nicolaus & Company, Inc. July 16, 1968 18. H. O. Peet & Company -- July 17, 1968 19. E. F. Hutton & Company, Inc. -- July 17, 1968 20. Dishy Easton & Company -- July 18, 1968 21. Weeden & Company -- July 18, 1968 22. Delafield & Delafield -- July 19, 1968 23. Maxwell Ohlman & Company -- July 19, 1968 24. Anchor Corporation -- July 22, 1968 25. Fidelity Management & Research 26. Keystone Custodian Funds, Inc. -- July 23, 1968 2% Tsai Management & Research Corporation -- July 23, 1968 28. Elkins Wetherill -- PBW -- July 24, 1968 29. INA Trading Corporation -- July 25, 1968 30. -

Market Mechanics: a Guide to U.S

BRCM CDWC CEFT CEPH CHIR CHKP CHTR CIEN CMCSK CMVT CNXT COST CPWR CSCO CTAS CTXS CYTC DELL Market Mechanics: A Guide to U.S. Stock Markets release 1.2 Although the inner workings of the stock market are fas- cinating, few introductory texts have the space to describe them in detail. Furthermore, the U.S. stock markets have been chang- ing so rapidly in recent years that many books have not yet caught up with the changes. This quick note provides an up-to- date view of how the U.S. stock markets work today. This note will teach you about: • The functions of a stock market; • Stock markets in the United States, including Nasdaq JAMES J. ANGEL, Ph.D. and the NYSE; Associate Professor of Finance • The difference between limit and market orders; McDonough School of Business • How stock trades take place; and Georgetown University • Lots of other interesting tidbits about the stock market that you wanted to know, but were afraid to ask. Market Mechanics: A Guide to U.S. Stock Markets DISH EBAY ERICY ERTS ESRX FISV FLEX GENZ GILD GMST HGSI ICOS IDPH IDTI IMCL IMNX INTC INTU ITWO What a Stock Market Does most productive opportunities are. These signals channel The stock market provides a mechanism where people capital to the areas that investors think are most produc- who want to own shares of stock can buy them from peo- tive. Finally, the financial markets provide important risk- ple who already own those shares. This mechanism not management tools by letting investors diversify their only matches buyer and seller, but it also provides a way investments and transfer risk from those less able to toler- for the buyer and seller to agree mutually on the price. -

Bofa List of Execution Venues

This List of Execution Venues and the associated Bank of America EMEA Order Execution Policy Summary form part of the General Terms & Conditions of Business available on the Bank of America MifID II Website www.bofaml.com/mifid2 The tables below set out the execution venues accessed by entities in the Bank of America Entities List and Associated Companies. These tables are not exhaustive and we may amend them from time to time in accordance with our policies. MLI and BofASE may also use other execution venues from time to time where they deem appropriate but in accordance with their policies (including the Bank of America Order Execution Policy). Asset class Region Regulated Markets of which MLI / BofASE is a direct member and MTFs accessed by MLI / BofASE Equities EMEA Aquis UK Equities EMEA Athex Group Equities EMEA Bloomberg BV Equities EMEA Bloomberg UK Equities EMEA Borsa Italiana Equities EMEA Cboe BV Equities EMEA Cboe UK Equities EMEA Deutsche Borse Xetra Equities EMEA Equiduct Equities EMEA Euronext Amsterdam Equities EMEA Euronext Brussels Equities EMEA Euronext Dublin Equities EMEA Euronext Lisbon Equities EMEA Euronext Oslo Equities EMEA Euronext Paris Equities EMEA ITG Posit Equities EMEA Liquidnet Equities EMEA Liquidnet Europe Equities EMEA London Stock Exchange 1 – ©2020 Bank of America Corporation Asset class Region Regulated Markets of which MLI / BofASE is a direct member and MTFs accessed by MLI / BofASE Equities EMEA NASDAQ OMX Nordic – Helsinki Equities EMEA NASDAQ OMX Nordic – Stockholm Equities EMEA NASDAQ OMX -

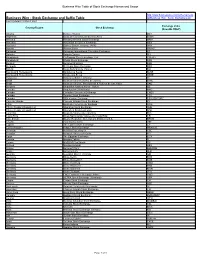

Stock Exchange and Suffix Table Ml/Business Wire Stock Exchanges.Pdf Last Updated 12 March 2021

Business Wire Table of Stock Exchange Names and Usage http://www.businesswire.com/schema/news Business Wire - Stock Exchange and Suffix Table ml/Business_Wire_Stock_Exchanges.pdf Last Updated 12 March 2021 Exchange Value Country/Region Stock Exchange (NewsML ONLY) Albania Bursa e Tiranës BET Argentina Bolsa de Comercio de Buenos Aires BCBA Armenia Nasdaq Armenia Stock Exchange ARM Australia Australian Securities Exchange ASX Australia Sydney Stock Exchange (APX) APX Austria Wiener Börse WBAG Bahamas Bahamas International Securities Exchange BS Bahrain Bahrain Bourse BH Bangladesh Chittagong Stock Exchange, Ltd. CSEBD Bangladesh Dhaka Stock Exchange DSE Belgium Euronext Brussels BSE Bermuda Bermuda Stock Exchange BSX Bolivia Bolsa Boliviana de Valores BO Bosnia and Herzegovina Banjalucka Berza BLSE Bosnia and Herzegovina Sarajevska Berza SASE Botswana Botswana Stock Exchange BT Brazil Bolsa de Valores do Rio de Janeiro BVRJ Brazil Bolsa de Valores, Mercadorias & Futuros de Sao Paulo SAO Bulgaria Balgarska fondova borsa - Sofiya BB Canada Aequitas NEO Exchange NEO Canada Canadian Securities Exchange CNSX Canada Toronto Stock Exchange TSX Canada TSX Venture Exchange TSX VENTURE Cayman Islands Cayman Islands Stock Exchange KY Chile Bolsa de Comercio de Santiago SGO China, People's Republic of Shanghai Stock Exchange SHH China, People's Republic of Shenzhen Stock Exchange SHZ Colombia Bolsa de Valores de Colombia BVC Costa Rica Bolsa Nacional de Valores de Costa Rica CR Cote d'Ivoire Bourse Regionale Des Valeurs Mobilieres S.A. BRVM Croatia -

The Trend Is Not Your Friend! Why Empirical Timing Success Is Determined by the Underlying's Price Characteristics and Market Efficiency Is Irrelevant

A Service of Leibniz-Informationszentrum econstor Wirtschaft Leibniz Information Centre Make Your Publications Visible. zbw for Economics Scholz, Peter; Walther, Ursula Working Paper The trend is not your friend! Why empirical timing success is determined by the underlying's price characteristics and market efficiency is irrelevant CPQF Working Paper Series, No. 29 Provided in Cooperation with: Frankfurt School of Finance and Management Suggested Citation: Scholz, Peter; Walther, Ursula (2011) : The trend is not your friend! Why empirical timing success is determined by the underlying's price characteristics and market efficiency is irrelevant, CPQF Working Paper Series, No. 29, Frankfurt School of Finance & Management, Centre for Practical Quantitative Finance (CPQF), Frankfurt a. M. This Version is available at: http://hdl.handle.net/10419/55525 Standard-Nutzungsbedingungen: Terms of use: Die Dokumente auf EconStor dürfen zu eigenen wissenschaftlichen Documents in EconStor may be saved and copied for your Zwecken und zum Privatgebrauch gespeichert und kopiert werden. personal and scholarly purposes. Sie dürfen die Dokumente nicht für öffentliche oder kommerzielle You are not to copy documents for public or commercial Zwecke vervielfältigen, öffentlich ausstellen, öffentlich zugänglich purposes, to exhibit the documents publicly, to make them machen, vertreiben oder anderweitig nutzen. publicly available on the internet, or to distribute or otherwise use the documents in public. Sofern die Verfasser die Dokumente unter Open-Content-Lizenzen (insbesondere CC-Lizenzen) zur Verfügung gestellt haben sollten, If the documents have been made available under an Open gelten abweichend von diesen Nutzungsbedingungen die in der dort Content Licence (especially Creative Commons Licences), you genannten Lizenz gewährten Nutzungsrechte. may exercise further usage rights as specified in the indicated licence. -

INITIAL INQUIRY INTO the RESPONSIBILITY to DISCLOSE MARKET INFORMATION* ARTHUR FLEISC-ER, JR.T ROBERT H

AN INITIAL INQUIRY INTO THE RESPONSIBILITY TO DISCLOSE MARKET INFORMATION* ARTHUR FLEISC-ER, JR.t ROBERT H. MUNDEimtt JoHN C. MURPHY, JR.ttt I. MARKET INFORMATION AND RULE lOb-5 A. Market Information A company discovers that land it owns contains substantial mineral deposits which can be commercially exploited. Officers and directors of the company who are aware of this discovery purchase the company's stock in the market before the information is made public. These facts describe a by now familiar inside information situation When the information is made public, the market will know that the value of the company's assets and its earning power have been substantially aug- mented and the price of the stock will adjust to reflect the increase in the value of the company. Purchase of the stock by directors and officers of the company under these circumstances violates the antifraud pro- visions of rule 10b-52 promulgated under Section 10(b) of the Securities Exchange Act of 1934.1 The following facts describe another situation in which material, non-public information is present. The president of ABC Company learns from Giant Brokerage Firm's analyst, who interviews him about * This Article bears a date of February 26, 1973. Some citations have been updated editorially. t BA. 1953, LL.B. 1958, Yale University. Member, New York Bar. ttFred Carr Professor of Law, University of Pennsylvania; Director, University of Pennsylvania Law School Center for Study of Financial Institutions. BA. 1954, LL.B. 1957, Harvard University. Member, New York Bar. itfA.B. 1967, Georgetown University; J.D.