Publisher's Version

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Forthlane Fridays - Guest Bios

Forthlane Fridays - Guest Bios Maria S. Jelescu Dreyfus CHIEF EXECUTIVE OFFICER AND FOUNDER ARDINALL INVESTMENT MANAGEMENT Maria is the Chief Executive Officer and Founder of Ardinall Investment Management, an investment firm focused on energy infrastructure that she started in 2017. Prior to Ardinall Investment Management, Ms. Dreyfus spent 15 years at Goldman Sachs, where she most recently served as a Portfolio Manager and Managing Director in the Goldman Sachs Investment Partners (GSIP) Group. She currently serves as a director on the board of Macquarie Infrastructure Corporation (NYSE: MIC), on the board of CDPQ (one of Canada’s largest pension plans), and on the advisory board of Eni Next (Eni SpA’s corporate venture arm). She also sits on the advisory board of the Center on Global Energy Policy at Columbia University and serves as co-chair of their Women in Energy program. Additionally, Ms. Dreyfus is a member of the MIT Corporation’s Development Committee and sits on the MIT Economics Department’s Visiting Committee. Ms. Dreyfus also serves as a member of the New York State Secure Choice Savings Program Board. Her current and past non-profit board memberships include New America Alliance, Breakthrough New York, and Girls Inc. of NYC. She is a member of the Economic Club of New York and a member of the Milken Institute’s Young Leaders Circle. Ms. Dreyfus has held her CFA since 2004, and holds a dual degree in economics and management science from the Massachusetts Institute of Technology. Daniel Dreyfus CHIEF INVESTMENT OFFICER AND FOUNDER BORNITE CAPITAL Dan serves as the Founder and Chief Investment Officer at Bornite Capital. -

Executive Branch Personnel Public Financial Disclosure Report (OGE Form 278E)

Nominee Report | U.S. Office of Government Ethics; 5 C.F.R. part 2634 | Form Approved: OMB No. (3209-0001) (March 2014) Executive Branch Personnel Public Financial Disclosure Report (OGE Form 278e) Filer's Information Shanahan, Patrick Michael Deputy Secretary of Defense, Department of Defense Other Federal Government Positions Held During the Preceding 12 Months: None Names of Congressional Committees Considering Nomination: ● Committee on Armed Services Electronic Signature - I certify that the statements I have made in this form are true, complete and correct to the best of my knowledge. /s/ Shanahan, Patrick Michael [electronically signed on 04/08/2017 by Shanahan, Patrick Michael in Integrity.gov] Agency Ethics Official's Opinion - On the basis of information contained in this report, I conclude that the filer is in compliance with applicable laws and regulations (subject to any comments below). /s/ Vetter, Ruth, Certifying Official [electronically signed on 06/08/2017 by Vetter, Ruth in Integrity.gov] Other review conducted by /s/ Vetter, Ruth, Ethics Official [electronically signed on 06/08/2017 by Vetter, Ruth in Integrity.gov] U.S. Office of Government Ethics Certification /s/ Apol, David, Certifying Official [electronically signed on 06/08/2017 by Apol, David in Integrity.gov] 1. Filer's Positions Held Outside United States Government # ORGANIZATION NAME CITY, STATE ORGANIZATION POSITION HELD FROM TO TYPE 1 The Boeing Company Chicago, Illinois Corporation Senior Vice 3/1986 Present President 2 The University of Washington Seattle, -

New Plastic Package for PLANTERS Peanuts Is Worth the Weight April 3

New Plastic Package for PLANTERS Peanuts is Worth the Weight April 3, 2012 8:11 AM ET HARTSVILLE, S.C., April 3, 2012 /PRNewswire via COMTEX/ --For Planters, America's favorite snack nut brand, sustainability has been a core part of its business for some time. In order to reduce Planters' impact on the environment through packaging changes, the brand turned to Hartsville, S.C.-based packaging and sustainability leader Sonoco (NYSE: SON), one of the largest diversified global packaging companies. In conjunction with the launch of the "Naturally Remarkable" campaign in 2011, Planters introduced a completely new plastic package to further its heritage of sustainability. (Logo: http://photos.prnewswire.com/prnh/20120403/CL80773LOGO ) Given the weight of glass as a packaging material, Planters 16oz. and 20oz. glass peanut jars were candidates for an update. The challenge for Sonoco was developing a lighter package that would not compromise Planters' targets for quality, capacity, clarity and shelf life. Sonoco responded by delivering a durable, light-weight plastic option that weighted 84 percent less than the original packaging - while still meeting the Planters brand's stringent quality targets. The significant reduction in packaging materials led to several benefits, including a 25 percent reduction in the number of trucks required to transport Planters Dry Roasted Peanuts. Additionally, Planters new plastic packaging is 100 percent recyclable and BPA free. Planters and Sonoco share a commitment to sustainability and have a longstanding relationship that includes collaboration on many new products. For this "Naturally Remarkable" initiative, Sonoco had the capital and expertise needed to produce a sustainable container that met the company's product protection and shelf life requirements. -

GENERAL FOODS CORPORATE TIMELINE 1895 Charles William

GENERAL FOODS CORPORATE TIMELINE 1895 Charles William (C.W.) Post makes his first batch of Postum cereal beverage in a little white barn in Battle Creek, Michigan. With that step he enters the new retail cereal industry. 1896 Post’s company incorporates as The Postum Cereal Company, Ltd. 1897 C.W. Post introduces Post Grape-Nuts cereal, one of the first ready-to-eat cold cereals. 1914 C.W. Post dies and ownership of the business passes to his daughter, Marjorie. The Postum Cereal Company continues to follow the formula for success which C.W. established: selling high-quality, nutritious cereal products through marketing and advertising techniques that appealed to the common man and woman. The company invests over twelve million dollars in advertising between 1895 and 1914. 1922 The company reorganizes as the Postum Cereal Company, Incorporated. By 1923 The company’s executive offices are located at 342 Madison Avenue, New York with manufacturing facilities in Battle Creek, Michigan and Windsor, Ontario. 1923 The Postum Cereal Company, Inc. establishes an employee stock plan. 1924 An Educational Department is formed and one of its principal activities is providing consumer nutrition education. The department publishes nutrition stories for children and a nutrition handbook on school lunches for use by teachers, health workers and food service directors. In 1931, the department name is changed to Consumer Services. The Postum Cereal Company posts sales of over $24 million. The company’s executive offices are now located in the Postum Building at 250 Park Avenue, New York City. 1925 The Postum Cereal Company acquires the Jell-O Company for $67 million in cash and stock. -

Business Analytics

NICK, ’20 Business Analytics Business Analytics Experiential Learning SAMPLE COURSES: Throughout their undergraduate careers, students work in small teams to solve real-world problems from local companies. • BALT 3330: Database Structures and Queries Students get a briefing from company executives on the problem • BALT 4320: Data and Text Mining and work all semester on the project scope and deliverables. At • FINA 4330: Predictive Analytics the end of the semester, the student teams present the results to the company. • BALT 4350: Web Intelligence and Analytics Hackathon Benedictine hosts an annual Hackathon for current BenU students SIMILAR MAJORS: along with students from local community colleges. The event Finance, Marketing, Data Science offers students a chance to work collaboratively in small teams on an analytics and Big Data project. A more recent Hackathon was sponsored by IBM and teams explored Chicago crime data for their project. BUSINESS ANALYTICS ALUMNI Communication Skills Our alumni have built successful careers at Zurich All business analytics students have project-based classes which Insurance, Northwestern, Conversant, CDW, allow them to gain practical and valuable experience as well as Morningstar, UniFirst Corporation, Nicor Gas, learn how to communicate their findings effectively. Students Invesco, Ace Hardware, Dial America, Kraft Heinz learn how to present technical results through written and oral Company, FedEx, Crowe, First Midwest Bank, presentations. These skills are essential in a dynamic business and Chamberlain Group – just to name a few. world and are highly sought-after by employers. WHY STUDY BUSINESS ANALYTICS AT BENEDICTINE? The growing field of analytics is transforming the way companies do business. Analytics can help improve managerial and organizational decision making by transforming data into actions and business insights. -

2019 SEC Form 10-K (PDF File)

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-K ☑ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2019 OR ☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from to Commission file number 001-14905 BERKSHIRE HATHAWAY INC. (Exact name of Registrant as specified in its charter) Delaware 47-0813844 State or other jurisdiction of (I.R.S. Employer incorporation or organization Identification No.) 3555 Farnam Street, Omaha, Nebraska 68131 (Address of principal executive office) (Zip Code) Registrant’s telephone number, including area code (402) 346-1400 Securities registered pursuant to Section 12(b) of the Act: Title of each class Trading Symbols Name of each exchange on which registered Class A Common Stock BRK.A New York Stock Exchange Class B Common Stock BRK.B New York Stock Exchange 0.750% Senior Notes due 2023 BRK23 New York Stock Exchange 1.125% Senior Notes due 2027 BRK27 New York Stock Exchange 1.625% Senior Notes due 2035 BRK35 New York Stock Exchange 0.500% Senior Notes due 2020 BRK20 New York Stock Exchange 1.300% Senior Notes due 2024 BRK24 New York Stock Exchange 2.150% Senior Notes due 2028 BRK28 New York Stock Exchange 0.250% Senior Notes due 2021 BRK21 New York Stock Exchange 0.625% Senior Notes due 2023 BRK23A New York Stock Exchange 2.375% Senior Notes due 2039 BRK39 New York Stock Exchange 2.625% Senior Notes due 2059 BRK59 New York Stock Exchange Securities registered pursuant to Section 12(g) of the Act: NONE Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. -

The H1B Records Below List the Companies That Have Submitted the Greatest Number of H1B Visa Petitions for This Location

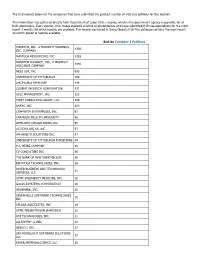

The H1B records below list the companies that have submitted the greatest number of H1B visa petitions for this location. This information was gathered directly from Department of Labor (DOL) records, which is the government agency responsible for all H1B submissions. Every quarter, DOL makes available a listing of all companies who have submitted H1B visa applications for the most recent 3 months for which records are available. The records contained in Going Global's H1B Plus database contains the most recent 12-month period of records available. Sort by Company | Petitions MASTECH, INC., A MASTECH HOLDINGS, 4339 INC. COMPANY MASTECH RESOURCING, INC. 1393 MASTECH ALLIANCE, INC., A MASTECH 1040 HOLDINGS COMPANY NESS USA, INC. 693 UNIVERSITY OF PITTSBURGH 169 UHCP D/B/A UPMC MEP 144 COGENT INFOTECH CORPORATION 131 SDLC MANAGEMENT, INC. 123 FIRST CONSULTING GROUP, LLC 104 ANSYS, INC. 100 COMPUTER ENTERPRISES, INC. 97 CARNEGIE MELLON UNIVERSITY 96 INTELLECT DESIGN ARENA INC. 95 ACCION LABS US, INC. 63 HM HEALTH SOLUTIONS INC. 57 UNIVERSITY OF PITTSBURGH PHYSICIANS 44 H.J. HEINZ COMPANY 40 CV CONSULTING INC 36 THE BANK OF NEW YORK MELLON 36 INFOYUGA TECHNOLOGIES, INC. 36 BAYER BUSINESS AND TECHNOLOGY 31 SERVICES, LLC UPMC EMERGENCY MEDICINE, INC. 28 GALAX-ESYSTEMS CORPORATION 26 HIGHMARK, INC. 25 SEVEN HILLS SOFTWARE TECHNOLOGIES 25 INC VELAGA ASSOCIATES, INC 24 UPMC PRESBYTERIAN SHADYSIDE 22 DVI TECHNOLOGES, INC. 21 ALLEGHENY CLINIC 20 GENCO I. INC. 17 SRI MOONLIGHT SOFTWARE SOLUTIONS 17 LLC BAYER MATERIALSCIENCE, LLC 16 BAYER HEALTHCARE PHARMACEUTICALS, 16 INC. VISVERO, INC. 16 CYBYTE, INC. 15 BOMBARDIER TRANSPORTATION 15 (HOLDINGS) USA, INC. -

Form 8-K the Kraft Heinz Company

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 Form 8-K CURRENT REPORT Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 Date of Report (Date of earliest event reported): August 10, 2015 The Kraft Heinz Company (Exact name of registrant as specified in its charter) Commission File Number: 001-37482 Delaware 46-2078182 (State or other jurisdiction of (IRS Employer incorporation) Identification No.) One PPG Place, Pittsburgh, Pennsylvania 15222 (Address of principal executive offices, including zip code) (412) 456-5700 (Registrant’s telephone number, including area code) Not Applicable (Former name or former address, if changed since last report) Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions: [ ] Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) [ ] Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a- 12) [ ] Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d- 2(b)) [ ] Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e- 4(c)) Item 8.01. Other Events. The Kraft Heinz Company (“Kraft Heinz”) is filing this Current Report on Form 8-K (this “Current Report”) to update the presentation of certain financial information and related disclosures included in the Annual Report of Kraft Foods Group, Inc. (“Kraft”) on Form 10-K for the year ended December 27, 2014, which was filed with the Securities and Exchange Commission on February 19, 2015 (the “Annual Report”). -

The History of Kraft Foods Inc

The History of Kraft Foods Inc. All About Kraft Learn everything there is to know about Kraft: like who we are, how you can reach us and what we’re doing in your community. Kraft Foods Inc. is a company with many different roots and founders, all sharing a commitment to quality, a willingness to take risks and a spirit of innovation. Among the products now sold by Kraft Foods Inc. are so many “firsts” and innovations that a history of the company is almost a history of the food industry. Kraft traces its history to three of the most successful food entrepreneurs of the late 19th and early 20th centuries — J.L. Kraft, who started his cheese business in 1903; C.W. Post, who founded Postum Cereal Company (later renamed General Foods Corporation) in 1895; and Oscar Mayer, who began his meat business in 1883. The Story of J.L. Kraft The history of KRAFT goes back to 1903, when, with $65 in capital, a rented wagon and a horse named Paddy, J.L. Kraft started purchasing cheese at Chicago’s Water Street wholesale market and reselling it to local merchants. Within a short time, four of J.L. Kraft’s brothers joined him in the business, and, in 1909, they incorporated as J.L. Kraft & Bros. Co. In 1914, J.L. Kraft and his brothers purchased their first cheese factory in Stockton, Illinois. In 1915, they began producing processed cheese in 3-1/2 and 7-3/4 ounce tins. J.L. Kraft’s method of producing processed cheese was so revolutionary, in 1916 he obtained a patent for it and in 1917 the company started supplying cheese in tins to the U.S. -

Analysis of Cadbury

JOURNAL OF CRITICAL REVIEWS ISSN- 2394-5125 VOL 7, ISSUE 14, 2020 Brand Management: Analysis of Cadbury Rinoy Babu ManakkalethuResearch Scholar Department of Commerce Sree Narayana Guru College, K.K. Chavadi, P.O., Coimbatore Dr.D.MahilaVasanthiThangam Associate Professor of Commerce Karunya Institute of Technology and Sciences Coimbatore-114 Abstract This study is conceptual in nature, covers a detailed description and analysis of the Brand Elements, Brand Loyalty, Brand Architecture, Positioning, repositioning, Brand Image, Brand Awareness etc. The objective of this research was to breakdown and analyses the strategic brand management process of Cadbury, a subsidiary of Mondelez International. As we all know, Cadbury is a brand that enjoys much Brand Equity owing to its high Brand Awareness, Brand Loyalty, and perceived quality. The Brand Elements of Cadbury has played a major role in its branding over the years. It is because of the high popularity of the brand elements of Cadbury that even after its acquisition by Mondelez International, they have not altered the name or any other aspect of the Brand Elements. In this project, we analyse various dimensions of the strategic brand management process of Cadbury. Also tried to analyse the Brand Image and Awareness for Cadbury. Various Frameworks and examples have been applied for this study. Introduction Cadbury, formerly known as Cadbury’s and Cadbury Schweppes, is a British multinational confectionery company wholly owned by Mondelez International (originally Kraft Foods) since 2010. It is the second largest confectionery brand in the world after Mars. Cadbury is internationally headquartered in Uxbridge, West London, and operates in more than 50 countries worldwide. -

Will Exelon Cut the Cord with Comed?

REAL ESTATE: The “Crayola House” on Wisconsin’s shoreline is for sale. PAGE 27 BOOZE: Spirit Hub aims to get craft spirits to the masses. PAGE 3 CHICAGOBUSINESS.COM | OCTOBER 5, 2020 | $3.50 Will Exelon cut the cord with ComEd? estimated earnings, Exelon’s It’s a move Wall Street has applauded elsewhere in the power industry stock price is at a multiple that But ComEd’s admissions in for nancial success. badly trails its utility peers, which BY STEVE DANIELS July that it engaged in a bribery Now Wall Street is wondering average about 16 times. Exelon’s More and more, Exelon looks scheme over nearly a decade to why Exelon, unlike virtually ev- stock has fallen 21 percent this like the last man standing in its win lucrative legislation in the ery major electricity company in year, while the Standard & Poor’s industry—and not in a good way. Illinois Capitol—coupled with the U.S., isn’t uncoupling its - Utilities Index is down 7 percent. e Chicago-based nuclear repeated requests for ratepayer nancially struggling power plants e valuation implies that inves- power giant and parent of Com- bailouts from Exelon’s unregu- from its healthy utilities, which tors ascribe essentially no value monwealth Edison long has lated arm that once pledged fe- along with ComEd include mo- to Exelon’s merchant arm even maintained that owning regulat- alty to market forces—make this nopoly power-delivery compa- Exelon CEO Chris Crane though the company projects it ed utilities like ComEd alongside marriage look rocky at best. -

The Preqin Quarterly Update: Private Equity

Q1 2013 The Preqin Quarterly Update: Private Equity Content Includes: Fundraising We review the latest fundraising figures, including regional breakdown, time spent on the road, and the largest funds to close in the quarter. Investors We take a look at investor appetite for private equity in the year ahead, including geographies and strategies to be targeted. Buyout Deals We examine private equity buyout deals and exits in Q1 2013 by type, value and region. Venture Capital Deals We provide a breakdown of the latest venture capital deal activity by value, region and stage. Performance We analyze the latest performance data for private equity funds, featuring dry powder figures, IRRs by fund type and vintage and the PrEQIn Private Equity Quarterly Index. alternative assets. intelligent data. The Preqin Quarterly Update: Private Equity, Q1 2013 Download Data Foreword Private equity fundraising in the fi rst quarter of 2013 was relatively robust, with 130 funds closed having raised an aggregate $67.2bn. However, in an increasingly competitive fundraising market – 1,906 funds are in market as of the start of Q2 2013 – many LPs are choosing to invest in funds raised by more established managers. First-time funds that closed in Q1 2013 secured just $4.2bn in aggregate capital, compared to the peak of $31.6bn in Q2 2008. However, Preqin’s interviews with private equity investors in December 2012 reveal that investor attitudes towards fi rst-time fund managers are more positive moving forwards; half of LPs interviewed will consider committing to fi rst-time funds or those managed by spin-off teams in the following 12 months.