2013 Audited Financial Statements

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Board Meeting Agenda

FLEETWOOD AREA SCHOOL DISTRICT Fleetwood, Pennsylvania BOARD MEETING AGENDA February 21, 2017 • Tuesday, 7 p.m. The Fleetwood Area School District, in partnership with families and community, is committed to excellence in providing the educational resources and opportunities which empower all students to become life-long learners and responsible citizens in a dynamic global environment. “Few things can help an individual more than to place responsibility on him, and to let him know that you trust him.” - Booker T. Washington I. ROLL CALL AND PLEDGE OF ALLEGIANCE SAFE SCHOOLS UPDATE Jeff Doelp, Director of Safe Schools II. VISITOR RECOGNITION During “Visitor Recognition,” persons wishing to address the board are asked to stand, stating name and municipality, prior to speaking on a subject. Speakers will be allotted three minutes and will be asked to be seated after the time provided. III. APPROVAL OF MINUTES (P. 1-5 January 17 regular meeting) IV. TREASURER'S REPORT (P. 6-10) V. APPROVAL OF BILLS (P. 11-45) VI. REPORT OF THE SUPERINTENDENT OF SCHOOLS A. UNFINISHED BUSINESS February 21, 2017 FASD...committed to excellence B. INSTRUCTIONAL PROGRAM 1. Recommend approval of the following planned instruction documents: - Algebra I – Grades 8 and 9 - Biology – Grade 10 - Film History – Grades 9 – 12 - Conspiracy Theory – Grades 9 – 12 C. PERSONNEL 1. Recommend approval of the following personnel actions: Assignments Co-Curricular - Kevin Smith, High School Assistant Football Coach, effective 1/13/17 @ a salary to be determined Instructional Staff - Scott Sandt, Annual Daily Substitute, effective 1/30/17 @ $100/day. 2016-17 building assignment will be at all three elementary buildings and the Middle School. -

Antietam School District ______(“___”)

PRELIMINARY OFFICIAL STATEMENT DATED DECEMBER 28, 2016 BOOK-ENTRY ONLY Rating S&P: Underlying: “A+” (Stable Outlook) Insured: See “Ratings” herein ___ Insured In the opinion of Bond Counsel, (if the Bonds are offered as Tax-Exempt Bonds (as hereinafter defined), assuming compliance with certain covenants of the School District, interest on the Bonds is excluded from gross income of the owners of the Bonds for federal income tax purposes under existing law, as currently enacted and construed. Interest on the Bonds is not an item of tax preference for purposes of either individual or corporate alternative e final Official Statement. minimum tax, although in the case of corporations (as defined for federal income tax purposes), such interest is taken into account in determining adjusted current earnings for purposes of such alternative minimum tax. Interest on the Bonds may be indirectly subject to certain other taxes imposed on certain corporations as more fully described under the caption “TAX EXEMPTION – FEDERAL: - Tax Exempt Bonds” herein. Under the laws of the Commonwealth of Pennsylvania, as currently enacted and construed, the Bonds are exempt from personal property taxes in Pennsylvania and the interest on the Bonds is exempt from Pennsylvania personal income tax and Pennsylvania corporate net income tax. The School District will designate the Bonds as “qualified tax-exempt obligations” for the purposes of Section 265(b)(3) of the Code (relating to the deductibility of interest expense by certain financial institutions). $7,700,000* -

Ms Amy Spina Supervior of Special Education Antietam

MS AMY SPINA MR MATTHEW LINK SUPERVIOR OF SPECIAL EDUCATION DIRECTOR OF SPECIAL ED ANTIETAM SCHOOL DISTRICT KUTZTOWN SCHOOL DISTRICT 201 N. 25TH STREET 50 TREXLER AVENUE READING, PA 19606 KUTZTOWN, PA 19530 610-370-2898 610-683-3261 MS KALYN BARTMAN MS BEVERLY GALLAGHER DIRECTOR SPECIAL EDUCATION SUPERVISOR OF SPECIAL ED BOYERTOWN SCHOOL DISTRICT MUHLENBERG SCHOOL DISTRICT 120 N. MONROE STREET 827 BELLEVUE AVENUE BOYERTOWN, PA 19512 LAURELDALE, PA 19605 610-473-3613 610-921-8000 MS MARY DARRACH MS DAWN CAMBRIA DIRECTOR OF SPECIAL ED DIRECTOR OF STUDENT SVCS BRANDYWINE HEIGHTS AREA S.D. OLEY VALLEY SCHOOL DIST 200 WEST WEIS STREET ADMINISTRATION BUILDING TOPTON, PA 19562 17 JEFFERSON STREET 610-682-5182 OLEY, PA 19547 610-987-4100 MR EDWARD J SKOCZEN, JR MS JACKIE DUDASH DIRECTOR SPECIAL EDUCATION DIRECTOR SPECIAL EDUCATION CONRAD WEISER AREA SCHOOL DISTRICT READING SCHOOL DISTRICT 200 LINCOLN DRIVE 800 WASHINGTON STREET WERNERSVILLE, PA 19565 READING, PA 19601 610-678-9236 484-258-7171 MS SHELLY MIECZKOWSKI MS LACIE CUFFIUFFO DIRECTOR OF SPECIAL EDUCATION ELEMENTARY SCHOOL PRINCIPAL DANIEL BOONE AREA SCHOOL DIST SCHUYLKILL VALLEY SCHOOL DIST MATTHEW BROOKE BUILDING SUITE 200 62 ASHLEY WAY 321 N FURNACE ST PO BOX 490 LEESPORT, PA 19533 BIRDSBORO, PA 19508 610-926-4165 610-582-6167 DR. SUZANNE MILLER MS LISA KISS SUPERVISOR OF SPECIAL EDUCATION DIRECTOR/INSTR SUP SVCS EXETER AREA SCHOOL DISTRICT TULPEHOCKEN SCHOOL DIST 4355 DUNHAM DRIVE 27 REHRERSBURG ROAD READING, PA 19606 BETHEL, PA 19507 610-779-7102 717-933-4611 MS GWYNN BOLLINGER DR MARK SAKOIAN DIRECTOR OF STUDENT SVCS DIRECTOR OF PUPIL SERVICES FLEETWOOD MIDDLE SCHOOL TWIN VALLEY SCHOOL DISTRICT 801 N. -

Antietam SD District Level Plan 07/01/2015 - 06/30/2018

Antietam SD District Level Plan 07/01/2015 - 06/30/2018 2 District Profile Demographics 100 Antietam Rd Stony Ck Mills Reading, PA 19606 (610) 779-0554 Superintendent: Lawrence Mayes Director of Special Education: Amy Spina Planning Process Utilizing information gained from planning sessions and input/ feedback from our Intermediate Unit advisors, the Antietam School District utilized a collaborative process that sought input from all stakeholders. Data, utilized for the Needs Assessment component, was collected from a variety of sources and was reviewed at both the building and central office level. The final District-level Document was presented to their respective stakeholder groups and the Board. All documents were available for public review prior to their final adoption. Mission Statement Antietam School District: A community partnership pledged to lifetime achievement. Vision Statement In keeping with our stated mission, the Antietam School District in conjunction with our community will provide a sound educational experience in a caring and supportive environment that fosters lifetime learning which: • Challenges and empowers all students in a rigorous standards-based curriculum • Utilizes technology and data-driven decision making to foster sound educational practices • Develops the foundation for a social responsible, lifelong learner • Emphasizes problem solving, analytical and creative thinking • Promotes a culture of respect 3 Shared Values Shared Values 1. We believe that all children can learn and the limits of individual learning are unknown. 2. The role of the school community is to work cooperatively to support the needs of the students. 3. All students are entitled and the District has the responsibility to create a safe and caring learning environment. -

Committee of the Whole Agenda

FLEETWOOD AREA SCHOOL DISTRICT Fleetwood, Pennsylvania COMMITTEE OF THE WHOLE AGENDA February 14, 2017 • 7 p.m. The Fleetwood Area School District, in partnership with families and community, is committed to excellence in providing the educational resources and opportunities which empower all students to become life-long learners and responsible citizens in a dynamic global environment. “Few things can help an individual more than to place responsibility on him, and to let him know that you trust him.” - Booker T. Washington CURRICULUM PRESENTATIONS Algebra I – Amy Schlott and Laura Treichler Biology – Stephanie Skelly Film History; Conspiracy Theory – Sean Gaston CALL TO ORDER Comments from community members will be entertained at the end of the meeting and will be limited to three minutes per speaker. A. UNFINISHED BUSINESS B. INSTRUCTIONAL PROGRAM 1. Recommend approval of the following planned instruction documents: - Algebra I – Grades 8 and 9 - Biology – Grade 10 - Film History – Grades 9 – 12 - Conspiracy Theory – Grades 9 – 12 C. PERSONNEL 1. Recommend approval of the following personnel actions: Assignments Co-Curricular - Kevin Smith, High School Assistant Football Coach, effective 1/13/17 @ a salary to be determined February 14, 2017 FASD...committed to excellence Instructional Staff - Scott Sandt, Annual Daily Substitute, effective 1/30/17 @ $100/day. 2016-17 building assignment will be at all three elementary buildings and the Middle School. Leave Requests - Michele Reitz, High School Food Service Worker, Leave without Pay, 2/13 through 2/16/17. - Jennie Schmoyer, Willow Creek Elementary Intervention Specialist, extension of FMLA/Qualifying Event leave, effective 2/28/17 through 3/14/17. -

Student Handbook 2016-2017

MT. PENN PRIMARY/ ELEMENTARY CENTER STUDENT HANDBOOK 2016-2017 ANTIETAM SCHOOL DISTRICT WELCOME The administration and staff would like to take this opportunity to WELCOME you to the Mt. Penn Elementary Center of the Antietam School District. The information contained in this handbook has been prepared to answer your questions concerning the operation and procedures regarding the school. If we have overlooked a question that you would like to have answered, please call the school so we may help you. The Mt. Penn Elementary Center has excellent teachers committed to providing our students with a quality education in a child-centered environment. The best education possible for your child may be attained through the cooperative efforts of the staff and supportive parents. Our community working together will provide a lifetime of success for our students. MISSION STATEMENT ANTIETAM’S COMMITMENT: A COMMUNITY PARTNERSHIP PLEDGED TO LIFETIME ACHIEVEMENT. POLICY OF NONDISCRIMINATION The Antietam School District is an equal opportunity education institution and will not discriminate on the basis of race, color, national origin, religion, age, sex, handicap, or Veteran status in its activities, programs, or employment practices as required by Title VI, Title IX, and Section 504. For information regarding civil rights, grievance procedures, services, activities, and facilities that are accessible to and usable by handicapped persons, contact Dr. Melissa Brewer, Compliance Coordinator, Antietam School District, 100 Antietam Road, Reading, PA 19606, (610) 779-0554. SCHOOL DISTRICT ADMINISTRATION Dr. Melissa Brewer Superintendent Mrs. Shirley Feyers Primary Center Principal Elementary Center Principal Mr. Aaron Kopetsky Assistant Principal Dr. Felice Stern Secondary Principal Mr. -

Local Right to Education Task Force

Member School Districts MEMBERSHIP Parents of special education students are the main- BERKS COUNTY of Berks County stay of the Local Task Force, which is required to Intermediate Unit 14 have a 51 percent parent-consumer membership. Also serving on the Local Right to Education Task Local Force are concerned citizens and representatives from: Antietam School District Right To Berks County Intermediate Unit #14 Boyertown Area School District Local school districts Education Brandywine Heights Area School District ARC Advocacy Services Conrad Weiser Area School District Local and regional special education service Task Force Daniel Boone Area School District Exeter Township School District CHILDREN ARE OUR INSPIRATION Fleetwood Area School District It is not enough to have a vision - We must embrace it Governor Mifflin School District The Right to Education Consent Agreement of and act upon it 1972 provided for the establishment of a Local Hamburg Area School District Together Task Force in each of the 29 Intermediate Units Kutztown Area School District to insure that the intent and spirit of the Berks County Muhlenberg School District Agreement is carried out throughout the Local Right to Education Commonwealth. Task Force Oley Valley School District Reading School District Schuylkill Valley School District Tulpehocken Area School District Twin Valley School District BERKS COUNTY Wilson School District Local Right To Education Task Force Wyomissing Area School District 1111 Commons Blvd PO Box 16050 Reading, PA 19612-6050 610-987-8511 Duties of the Resources Meetings Local Task Force 1. Assist families and professionals of school- Arc Advocacy Services Berks County Dates: Tues, Oct 5, 2010 age students with special education needs 610-603-0227 www.marcpa.org/ Tues, Dec 7, 2010 by providing educational and networking Tues, Feb 1, 2011 opportunities so that they are better able Autism Society of Berks County Tues, Apr 5, 2011 to make informed decisions to meet the 610-736-3739 www.autismsocietyofberks.org Agenda: 11:30 a.m.-noon Lunch needs of their student (s). -

Course Selection Guide 2020-2021

Table of Contents Page General Information 2-5 Grade Level Scheduling Patterns (Grades 9-12) 5-6 Drop/Add Policy 6 Career Pathways 7-9 Fine Arts (Grades 7-8) 10-12 English – Language Arts 12-16 Family & Consumer Science 16-17 Health & Physical Education 17-18 Mathematics 18-22 Music 23-24 Science 24-27 Social Studies 28-30 Technology 30-31 World L anguage 31-32 Internships (Grades 11-12) 32 On-line Learning 33 Service Learning (Community Service) 33 Dual Enrollment (RACC Grade 12) 33-34 BCTC (Grades 10-12) 34-36 1 The Antietam School District is an equal opportunity education institution and employer and will not discriminate on the basis of race, color, national origin, sex, disability, age, religion, Veteran status, or any other legally protected classification in accordance with State and Federal laws, including Title VI, Title IX, or the American with Disabilities Act, Section 504. Complaints or questions should be directed to: Dr. L. W. Mayes, Superintendent of Schools, Antietam School District, 100 Antietam Road, Reading, PA 19606-1018. GENERAL INFORMATION The Antietam High School Course Selection Handbook should be used in conjunction with Grade Level Scheduling Patterns found following this section. The patterns provide: ● Required grade level subjects ● Number of electives possible ● Scheduling guidelines for each grade You will note that courses in the handbook are arranged departmentally, including all required and elective subjects. In addition to a brief content description of each course, grade sequences, prerequisites, and periods meeting per cycle are indicated. Subjects are presented in grade level order whenever possible. -

Welcome and Introduction

Antietam Middle-Senior High School HANDBOOK Course Selection Handbook Grades 7 - 12 2013 - 2014 100 Antietam Road, Reading, PA 19606-1018 (610) 779-3545 FAX (610) 779-0378 Table of Contents Page General Information ....................................................................................................................................... 1-4 Grade Level Scheduling Patterns (Grades 9-12) .............................................................................................. 5 Drop/Add Policy ................................................................................................................................................ 6 Weighted Courses .............................................................................................................................................. 7 Electives (Grades 10-12) .................................................................................................................................... 8 Fine Arts (Grades 7-8) ....................................................................................................................................... 9 Art ................................................................................................................................................................ 10-12 Business Education ..................................................................................................................................... 13-15 Computer Science ...................................................................................................................................... -

Course Selection Guide 2019-2020.Pdf

Table of Contents Page General Information 2-5 Grade Level Scheduling Patterns (Grades 9-12) 5-6 Drop/Add Policy 6 Career Pathways 7-9 Fine Arts (Grades 7-8) 10-12 English – Language Arts 12-16 Family & Consumer Science 16-17 Health & Physical Education 17-18 Mathematics 18-22 Music 23-24 Science 24-27 Social Studies 28-30 Technology 30-31 World L anguage 31-32 Internships (Grades 11-12) 32 On-line Learning 33 Service Learning (Community Service) 33 Dual Enrollment (RACC Grade 12) 33-34 BCTC (Grades 10-12) 34-36 1 The Antietam School District is an equal opportunity education institution and employer and will not discriminate on the basis of race, color, national origin, sex, disability, age, religion, Veteran status, or any other legally protected classification in accordance with State and Federal laws, including Title VI, Title IX, or the American with Disabilities Act, Section 504. Complaints or questions should be directed to: Dr. L. W. Mayes, Superintendent of Schools, Antietam School District, 100 Antietam Road, Reading, PA 19606-1018. GENERAL INFORMATION The Antietam High School Course Selection Handbook should be used in conjunction with Grade Level Scheduling Patterns found following this section. The patterns provide: ● Required grade level subjects ● Number of electives possible ● Scheduling guidelines for each grade You will note that courses in the handbook are arranged departmentally, including all required and elective subjects. In addition to a brief content description of each course, grade sequences, prerequisites, and periods meeting per cycle are indicated. Subjects are presented in grade level order whenever possible. -

Scholarship Luncheon

Scholarship Luncheon June 3, 2019 12 p.m. DoubleTree by Hilton, Reading Welcome to Berks County Community Foundation’s 2019 Scholarship Luncheon Welcome Kevin K. Murphy, President Berks County Community Foundation Lunch Remarks Berks' Best presentation: Garry Lenton, Editor, Reading Eagle Keynote Speaker: Dr. Thomas F. Flynn, President, Alvernia University Recognition of scholarship recipients, donors and volunteers: Kevin K. Murphy, President Berks County Community Foundation Use #BerksBest on Twitter and Instagram for today's event. Keynote Speaker: Dr. Thomas F. Flynn Thomas F. Flynn, Ph.D., is Alvernia’s sixth president, having served since 2005. During this time, he has overseen the development of new strategic and campus master plans and the campus-wide process culminating in the achievement of university status. Under his leadership, Alvernia has launched “Values and Vision:” The Fiftieth Anniversary Campaign. In addition to major capital projects already completed, endowed professorships and centers of excellence have been established, notably the O’Pake Institute for Ethics, Leadership and Public Service and the Holleran Center for Community Engagement. Prior to his arrival at Alvernia, Dr. Flynn served as Senior Advisor for the Council of Independent Colleges (CIC), where he led a national symposium on the relation between liberal arts education and professional leadership, involving corporate leaders and university presidents. Previously, he served nine years at Millikin University (IL), initially as Provost and subsequently as President. He also spent fourteen years on the faculty of Mount Saint Mary's College (MD), where he was Professor of English and served as Dean of the College. A native of Boston, he earned his B.A. -

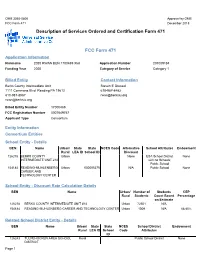

Description of Services Ordered and Certification Form 471 FCC Form

OMB 3060-0806 Approval by OMB FCC Form 471 December 2018 Description of Services Ordered and Certification Form 471 FCC Form 471 Application Information Nickname 2020 RWAN BEN 1700469 Xtel Application Number 201009184 Funding Year 2020 Category of Service Category 1 Billed Entity Contact Information Berks County Intermediate Unit Steven E Dressel 1111 Commons Blvd Reading PA 19612 610-987-8482 610-987-8567 [email protected] [email protected] Billed Entity Number 17000469 FCC Registration Number 0007649767 Applicant Type Consortium Entity Information Consortium Entities School Entity - Details BEN Name Urban/ State State NCES Code Alternative School Attributes Endowment Rural LEA ID School ID Discount 126278 BERKS COUNTY Urban None ESA School District None INTERMEDIATE UNIT #14 with no Schools; Public School 154184 READING-MUHLENBERG Urban 000005275 N/A Public School None CAREER AND TECHNOLOGY CENTER School Entity - Discount Rate Calculation Details BEN Name Urban/ Number of Students CEP Rural Students Count Based Percentage on Estimate 126278 BERKS COUNTY INTERMEDIATE UNIT #14 Urban 72501 N/A 154184 READING-MUHLENBERG CAREER AND TECHNOLOGY CENTER Urban 1009 N/A 68.80% Related School District Entity - Details BEN Name Urban/ State State NCES School District Endowment Rural LEA ID School Code Attributes ID 126243 TULPEHOCKEN AREA SCHOOL Rural Public School District None DISTRICT Page 1 BEN Name Urban/ State State NCES School District Endowment Rural LEA ID School Code Attributes ID 126246 BOYERTOWN AREA SCHOOL Urban Public School District