Central Jersey College Prep Charter School Comprehensive Annual

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

New Jersey & New York Groups Updated March 4, 2019

New Jersey & New York Groups Attached are some resources about groups that are active in opposing the Northeast Supply Enhancement (NESE) Project and other fossil fuel infrastructure projects as well as others, like ReThink Energy NJ and The Watershed Institute, that provide solid resources for good, high quality information on energy and the environment. Information includes way to reach contacts and gather information from websites, Facebook pages and Twitter. Updated March 4, 2019 Grassroots Advocacy Groups Central Jersey Safe Energy Coalition Central Jersey Safe Energy Coalition is a citizen Email Contact [email protected] organization protesting unsafe pipeline infrastructure in and around central Jersey with a Website http://www.safer-nj.org mission to protect the people and the environment of Central New Jersey, and to Facebook https://www.facebook.com/safernj/ preserve that environment for future generations. Twitter @safernj Central Jersey Environmental Defenders Defending the environment against corporate Email Contact [email protected] greed: A Grassroots Environmental Group working with the Franklin Township Task Force Website www.scrap-NESE.org (on CS206 & NESE) providing education, research, advocacy and outreach to support efforts to stop Facebook the NESE Project and move NJ toward actions to https://www.facebook.com/groups/1161375143904005/ protect our safety, health, air, water and the Twitter environment. @scrapNESE NGOs Food & Water Watch Food & Water Watch is a Washington, D.C.- based non-governmental organization group Email Contact NJ: Junior Romero at [email protected] which focuses on corporate and government accountability relating to food, water, and Email Contact NJ: Matt Smith at [email protected] corporate overreach. -

Zip Code City State Market 20701 ANNAPOLIS JUNCTION MD

Zip Code City State Market 20701 ANNAPOLIS JUNCTION MD BALTIMORE 20701 ANNAPOLIS JUNCTION MD BALTIMORE 20707 LAUREL MD BALTIMORE 20708 LAUREL MD BALTIMORE 20709 LAUREL MD BALTIMORE 20723 LAUREL MD BALTIMORE 20724 LAUREL MD BALTIMORE 20725 LAUREL MD BALTIMORE 20726 LAUREL MD BALTIMORE 20755 FORT GEORGE G MEADE MD BALTIMORE 20759 FULTON MD BALTIMORE 20763 SAVAGE MD BALTIMORE 20777 HIGHLAND MD BALTIMORE 20794 JESSUP MD BALTIMORE 20794 JESSUP MD BALTIMORE 21012 ARNOLD MD Baltimore 21013 BALDWIN MD Baltimore 21013 BALDWIN MD Baltimore 21014 BEL AIR MD Baltimore 21015 BEL AIR MD Baltimore 21020 BORING MD Baltimore 21022 BROOKLANDVILLE MD Baltimore 21023 BUTLER MD Baltimore 21028 CHURCHVILLE MD Baltimore 21029 CLARKSVILLE MD Baltimore 21030 COCKEYSVILLE MD Baltimore 21031 HUNT VALLEY MD Baltimore 21032 CROWNSVILLE MD Baltimore 21034 DARLINGTON MD Baltimore 21035 DAVIDSONVILLE MD Baltimore 21036 DAYTON MD Baltimore 21037 EDGEWATER MD Baltimore 21040 EDGEWOOD MD Baltimore 21041 ELLICOTT CITY MD Baltimore 21042 ELLICOTT CITY MD Baltimore 21043 ELLICOTT CITY MD Baltimore 21044 COLUMBIA MD Baltimore 21045 COLUMBIA MD Baltimore 21046 COLUMBIA MD Baltimore 21047 FALLSTON MD Baltimore 21050 FOREST HILL MD Baltimore 21051 FORK MD Baltimore 21053 FREELAND MD Baltimore 21054 GAMBRILLS MD Baltimore 21057 GLEN ARM MD Baltimore 21060 GLEN BURNIE MD Baltimore 21061 GLEN BURNIE MD Baltimore 21062 GLEN BURNIE MD Baltimore 21065 HUNT VALLEY MD Baltimore 21071 GLYNDON MD Baltimore 21074 HAMPSTEAD MD Baltimore 21075 ELKRIDGE MD Baltimore 21076 HANOVER MD Baltimore -

31 RRC Newsletter

HOAD RUNNERS C L U KSW YORK ASSOCIATION NriWSTJ^ITER No.31, WINTER 1967 Presidenta^at Cirulnick,2-fl™10 132 Rdc .Rosedale 225N.Y. (Urxitsd AA). Vice-Pro s. ^ Bill Taylor,4-3 Cliurch ot „ ,Groenv/iciijCcnn. O683O 2nd V,P. Ron; Brewington^ uC Navy/unitod AA Sec-Treas, sV.Chiappei;ta,26 Madison Pk.Gardens^Port , 11050 (NCV7 York"AC) _(PleasG__kGe2 Secretary ' . B/IPORTANT RRC MEETING™-Annual Spring RRC meeting and ^ election of officers. "Saturday Jujie 17:-,1967, 11^0 AIVI Alley Pond Park5Queens5N.Yo Meet at park locker room on Winchester Blvdc near Union Turnpikejacross the street from Creedmoro State Hospital. A Run" Per Pun will preceed the RHC Meeting. • REBEI^SER ~ = = = = rz = = = = = V 0 T E JACK BARRY"—Many will remember Jack Barry of Merchantville ,No J. He made many su.cc3ssful invasions into BIG TQrM to run cross-country^ track and road races. On a memorable cold, rainj^- Sunday in Bee. 1956^ Jack won the Jr.National Marathon Championship in Queens• He also conducted a training clinic for the New York area distance runners' ten years ago. Since then he has.travelled extensively and has spent time training under Igloi.He v/rote'an article for the News- letter on Igloi's methods. Jack still runs 6 to 10 miles a day but chooses not to try to fit in hard workouts on injury riddled legs while taking care of his successful, art.business. Jack never reached all of his ideal goals in .rujming and found running very hard but he is g3.ad that he made the effort. -

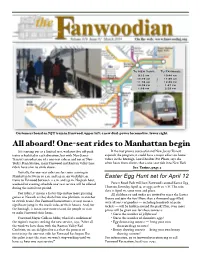

All Aboard! One-Seat Rides to Manhattan Begin

To New York: To Fanwood: 9:12 am 10:44 am 10:16 am 11:49 am 11:18 am 12:49 pm 12:18 pm 1:47 pm 1:16 pm 2:39 pm Customers board an NJT train in Fanwood, upper left; a new dual-power locomotive, lower right. All aboard! One-seat rides to Manhattan begin It’s starting out as a limited test, with just five off-peak If the test proves successful and New Jersey Transit trains scheduled in each direction, but with New Jersey expands the program, it could have a major e&ect on home Transit’s introduction of a one-seat ride in and out of New values in the borough. Local Realtor Pat Plante says she York’s Penn Station, many Fanwood and Raritan Valley Line often hears from clients that a one-seat ride into New York riders have a lot to smile about. See Trains, page 2 Initially, the one-seat rides are for trains arriving in Manhattan between 10 a.m. and 2 p.m. on weekdays, or Easter Egg Hunt set for April 12 trains to Fanwood between 11 a.m. and 3 p.m. No peak-hour, weekend or evening schedule one-seat service will be o&ered Forest Road Park will host Fanwood’s annual Easter Egg during the initial test period. Hunt on Saturday, April 12, at eggs-actly 10 A.M. The rain date is April 19, same time and place. For riders, it means a faster trip and no more guessing All children 10 and under are invited to meet the Easter games at Newark as they dash from one platform to another Bunny and join the fun! More than a thousand eggs filled to switch trains. -

TCS/Xtreme Fall Showcase October 8-9, 2016

TCS/Xtreme Fall Showcase October 8-9, 2016 TCS/Xtreme Fall Showcase ‐ Pool List REVISED 10/6/16 October 8‐9, 2016 CRS 14U Pool MW Pool #1 Hills Pool #1 Ewing #1 Pool B1 PA Xtreme 14U Black M1 Premier Sting H1 Jersey Girls Gold D1 Illinois Bash Gold B2 Neshaminy Shock 14U Elite M2 Burlington Sting 18U Gold H2 NJ Chill Gold H3 NJ Breakers Gold Lapicki B3 Top Gun 14U Blue M3 Long Island Pride Gold D3 Heartbreakers Gold B4 Lady Orioles Elite M4 Elite Fastpitch of Virginia 18U H4 NJ Fight Gold 18U Black B5 PA Xtreme Futures M5 USA Lady Hawks Brown H5 Magnolia Silver Bullets D5 ROCK 18 Gold ‐ Waye B6 NJ Fight 14U M6 Thunderbirds 18U Gold H6 CT Eliminators Showcase ‐ Smith D6 Team Long Island‐Castle/Carnaghi H7 NJ Mystics Gold CRS 16U Pool MW Pool #2 Ewing #2 Pool A1 Diamond Dolls Elite N1 Rage Gold Hills Pool #2 E1 NJ Mystics Gold ‐ Jackson A2 Hampton Roads Warriors N2 PA Vypers Gold I1 L.I. Sudden Impact Elite E2 CT Eliminators Gold A3 Jersey Shore Barracudas N3 PA Xtreme Black I2 Top Gun 18U Elite E3 Lady Lightning Select 18U Buchanan (VA) A4 NJ Fight 16U N4 Long Island Crush 18U Gold I3 NJ Fight 18U Blue E4 New Jersey Breakers Gold‐Salvatore A5 NJ Heist N5 The Wicked I4 East Coast Tsunami 18U Elite E5 NJ Heist Gold A6 Wagner's ‐ Galbreath N6 Angels Fastpitch 18U Gold I5 NJ Heist Elite E6 Boyertown Storm I6 South Jersey Gators Gold E7 ROCK 18 Gold ‐ Waye/Aspinwall MW Pool #3 I7 In The Zone Menace Showcase Council Rock South O1 Long Island Hurricanes 18u Elite Ewing #3 Pool 2002 Rock Way O2 Vienna Velocity Select Hills Pool #3 Southampton, -

North Versus South, Jersey Style

_______________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________ Contact: All references must attribute: PATRICK MURRAY “Monmouth University/Gannett New Jersey Poll” 732-263-5858 (office) 732-979-6769 (cell) For more information: Monmouth University Polling Institute [email protected] 400 Cedar Avenue West Long Branch, NJ 07764 EMBARGOED to: www.monmouth.edu/polling Monday, March 31, 2008, 5:00 am NORTH VERSUS SOUTH, JERSEY STYLE A shared sense of place hard to find in the Garden State New Jersey has had a split identity ever since Lord Berkeley and Sir George Carteret divided the new colony into east and west in the late 1600s. More than 300 years later, the state is still a tale of two Jerseys, with the more populous northern portion geared toward New York City and the southern half tuned into Philadelphia – Ben Franklin’s “barrel tapped at both ends.” Do these regional identities mean anything? Well, according to the latest Monmouth University/Gannett New Jersey Poll , if you’re from North Jersey, it means very little. However, if you’re from South Jersey, it means a great deal. When asked whether government spending and programs are distributed fairly across the Garden State or if a certain region is favored, state residents give the edge to the north. About 1-in-3 (33%) say that North Jersey gets more than its fair share of resources. Only 10% feel South Jersey benefits more than it should from public programs. Another 21% feel that aid is divided equitably across both regions and 35% have no opinion. The poll also found that how you see this issue depends on where you live. -

Conrail Elizabeth Site

02-8803-69-51 REV. NO. 0 FINAL DRAFT SITE INSPECTION REPORT CENTRAL RAILROAD OF NEW JERSEY ELIZABETH, NEW JERSEY PREPARED UNDER TECHNICAL DIRECTIVE DOCUMENT NO. 02-8803-69 CONTRACT NO. 68-01-7346 FOR THE ENVIRONMENTAL SERVICES DIVISION U.S. ENVIRONMENTAL PROTECtiON AGENCY MAY 24,1989 NUS CORPORA nON SUPERFUND DIVISION SUBMITTED BY; !ku .!wk~1 _ DIANETRUBE REVIEWED/APPROVED BY; PROJECT MANAGER ; ~~&;. DA~DH8M 7 SITE MANAGER -i~~,---FIT OFFICE MANAGER TIERRA-B-01 ~457 B .~BOO 0 a 0 1 I 02-8803-69-51 Rev. No. 0 SITENAME: Central Railroad of New Jersey EPAID NO.: NJD981557895 Trumbull Street LATITUDE: 40039' 28"N ADDRESS: Elizabeth, New Jersey LONGITUDE: 074010' 56"W LOT: 1380 BLOCK: 1 1.0 SITE SUMMARY The Central Railroad of New Jersey Site is located in an industrial section of Elizabeth, Union County, New Jersey. The population residing within 1 mile of the site is 20,380, and 155,534 people live within 3 miles. The 85-acre site is an inactive train yard which serviced passenger and freight train engines and cars from 1901 until 1988. Central Railroad of New Jersey, CONRAIL, and New Jersey Transit have operated at the site, which is owned by CONRAIL The site is the most recently actne remaining portion of the larger CONRAIL Elizabethport Yard, which consisted of several hundred acres. The other portions of the site have been leased to various tenants, including the Armin Poly- Film Co. and Kawasaki Kisen, Kaisha, Ltd. (K-Line), a trucking firm. The site is not secured, and there is evidence of uncontrolled dumping on site, such as drums, tires, and other debris. -

Letterhead BRP Lette

Participating Organizations Alliance for a Living Ocean American Littoral Society Arthur Kill Coalition Clean Ocean Action www.CleanOceanAction.org Asbury Park Fishing Club Bayberry Garden Club Bayshore Saltwater Flyrodders Belford Seafood Co-op Belmar Fishing Club Main Office Institute of Coastal Education Beneath The Sea Bergen Save the Watershed Action Network 18 Hartshorne Drive 3419 Pacific Avenue Berkeley Shores Homeowners Civic Association P.O. Box 505, Sandy Hook P.O. Box 1098 Cape May Environmental Commission Wildwood, NJ 08260-7098 Central Jersey Anglers Highlands, NJ 07732-0505 Citizens Conservation Council of Ocean County Voice: 732-872-0111 Voice: 609-729-9262 Clean Air Campaign Fax: 732-872-8041 Fax: 609-729-1091 Coalition Against Toxics Ocean Advocacy [email protected] Coalition for Peace & Justice [email protected] Coastal Jersey Parrot Head Club Since 1984 Coast Alliance Communication Workers of America, Local 1034 Concerned Businesses of COA Concerned Citizens of Bensonhurst Concerned Citizens of COA Concerned Citizens of Montauk Statement of Clean Ocean Action Dosil’s Sea Roamers Eastern Monmouth Chamber of Commerce Environmental Response Network Blue Ribbon Panel on Development of Explorers Dive Club Fisheries Defense Fund Wind Turbine Facilities in Coastal Waters Fishermen’s Dock Cooperative Fisher’s Island Conservancy Monmouth County Library Friends of Island Beach State Park Friends of Liberty State Park Friends of Long Island Sound Manalapan, NJ Friends of the Boardwalk Garden Club of Englewood May 23, 2005 Garden Club of Fair Haven Garden Club of Long Beach Island Garden Club of Morristown Garden Club of Navesink Garden Club of New Jersey Thank you for the opportunity to submit comments at tonight’s meeting. -

A Resource Guide for New Jersey's Military, Veterans, and Families

Veterans, life doesn't have to be a battlefield... Vet 2 Vet Counseling Helpline You answered the call of duty... We answer the call for you. 1-866-VETS-NJ4 (1-866-838-7654) NJ Vet to Vet, is operated by Rutgers University and funded by the New Jersey Department of Military and Veterans Affairs, and is a peer-counseling program for assessing a Veteran’s mental health needs. The toll-free help line is available 24-hours a day, 7 days a week for Veterans and their families. Services include: Veteran peer support, family support, clinical assessment, case management, referrals to a network of mental health providers, web-based peer support, and live chat. Call (866) 838-7654 or visit http://ubhc.rutgers.edu/vet2vet/ III Table of Contents Support Assistance for Military and Veterans Families 1 New Jersey Prevention Network: Military Family Nights Program 2 New Jersey Prevention Network: Achieving Personal Balance Program 2 NJ National Guard State Family Readiness Council Fund 2 TurboTAP (Transition Assistance Program) 3 G.I.GO –Fund: The Transition Center, New Brunswick, NJ 3 Military OneSource 4 Army Information Line 5 Army Family Team Building (AFTB) 5 Army Family Action Plan (AFAP) 6 Army Reserve Family Program (Online) 7 Army Reserve Family Network 7 The Army Reserve Child & Youth School Services (CYSS) 7 Soldiers and Sailors Civil Relief Act of 1940 9 Army Reserve Financial Readiness Program 9 MyMoney.gov 10 Displaced Homemaker Centers 10 7 Habits of Highly Successful Military Families 11 US Department of Veteran Affairs: East Orange and Lyons Campuses 12 Delaware & Pennsylvania US Department of Veteran Affairs: Serving New Jersey Veterans 13 New Jersey National Guard Family Assistance Centers 14 U.S. -

Program of Studies

PROGRAM OF STUDIES Central Jersey College Prep Charter School 101 Mettlers Rd. Somerset Somerset, NJ www.cjcollegeprep.org 2020-2021 1 | Page Central Jersey College Prep- Somerset 101 Mettlers Rd. Somerset, NJ 08873 P: 732-649-3954 ex:1321 F: 732-302-9992 Central Jersey College Prep- New Brunswick 222 Livingston Ave, New Brunswick, NJ 08901 P: 732-532-6848 Administration Namik Sercan, Principal and CEO Fatih Cekic, Assistant Principal of School Operations Tasha Mosconi, Assistant Principal of Curriculum and Instruction JOHN E. TOZAN School Operations Director-New Brunswick Counselors Zafer Suslu, School Counselor- Director Laura Alvarez, School Counselor Natalie Perez-Sudah, School Counselor Barbara Grossmann- School Counselor-New Brunswick Amanda McIntyre- School Counselor Board of Trustees Dr. Ferhan Tunagur, President Mrs. Jackie Lewis, Vice President Dr. Ozcan Uzun, Member Mrs. Sevil Eke, Member Mr. Eric Van Bladel, Member Ex-Officio Members Dr. Namik Sercan - Chief Education Officer Mr. Fatih Kayalar - Board Secretary Mr. Christopher Lessard - Treasurer 2 | Page Mission Statement: The mission of the Central Jersey College Prep Charter School is to provide academic and social challenges and opportunities to students, instilling the skills and knowledge that they will need to succeed in their lives. The CJCPCS aims to forge a powerful partnership out of the student-teacher- parent triad. This partnership will provide and empower our youth with the support necessary to reach their highest potential - intellectually, socially, emotionally and physically— building on their inherent promise to aid in their preparation for college and career. The CJCPCS seeks to graduate men and women who think critically and creatively; have acquired strong skills in mathematics, science, language, technology, history, and the arts; and are committed to a lifetime of learning and civic involvement. -

I Have Attached the Names and Projects for the 114 Local Members

In the Name of Allah, the Most Gracious, the ever Merciful November 4, 2017 Most Beloved Huzur, Asalamo Alaikum wa Rahmatullah! Based on Huzur’s guidance about tabligh from the Friday sermons in September 2017, the Tabligh Department USA has mobilized initiatives for engaging our local Amila members and general members of all 74 chapters in the USA by holding ten regional tabligh conferences with the goal to conveying Huzur-e- Anwar’s message. Alhumdolillah, the tabligh conference for North East 2 region was held today on Saturday November 4, 2017 with 114 local members (Men, Women and Children) in attendance. I have attached the names and projects for the 114 local members attended from Bronx, Brooklyn, Central Jersey, Long Island, Middletown NY, North Jersey, Queens NY, Willingboro. I beg for prayers for all these members and that Allah Blesses their efforts with results and that we can all fulfill Huzur-e-Anwar’s desires for USA Jama’at in the field of Tabligh. Ameen. Wa-salam, Huzur ka ik adna sa ghulam, Usman Nasir Choudhary Serving as Assistant, National Tabligh Department, USA Address: 7919 Harwood Pl. Springfield, Virginia 22152 – USA 1 In the Name of Allah, the Most Gracious, the ever Merciful North East 2 - Regional Tabligh Conference 11/4/2017, Queens, NY USA Tabligh Programs based on Shura 2016 & 2017 Tabligh proposals. 1. Coffee Cake and True Islam weekly events in Mosque or outside venue (CCTI) 2. Tabligh In Neighborhoods - Coffee Cake and True Islam in your Homes (Homes) 3. Tabligh to Ethnic Communities in the US (Ethnic) National Tabligh Team Members Usman Nasir Choudhary, Mirza Ghulam Rabbi, Sazzad Khandakar, that Attendance Ahmad Iqbal Khan Total of 114 - Men, Women and children Daeen Name (Volunteering for Tabligh Initiative No.) 1. -

The Spooky Shootout

The Spooky Shootout Powered by Bracket Team ® 2020 Date: Oct 31, 2020 Iron Peak Iron Peak Sports & Sports & Time Sportika - Court 1 Sportika - Court 3 Sportika - Court 5 Sportika - Court 6 Events - Court Events - Court 1 3 8:00 AM Boys 8th: Sat - Boys 8th: Sat - No Games Boys 6th: Sat - No Games No Games Sportika Sportika Sportika Game #1 Game #2 Game #2 STR Elite The Mavericks Westwood Team Reborn B Valley A's Warriors The Village 6B 9:00 AM Boys 8th: Sat - Boys 8th: Sat - Boys 9th: Sat - Boys 6th: Sat - No Games No Games Sportika Sportika Sportika Sportika Game #3 Game #4 Game #2 Game #4 STR Elite Team Reborn B NJ Future EEP Valley A's The Mavericks The Mavericks The Village 6A 10:00 AM Boys 9th: Sat - Boys 9th: Sat - Boys 6th: Sat - Boys 6th: Sat - No Games No Games Sportika Sportika Sportika Sportika Game #1 Game #5 Game #1 Game #3 Brooklyn USA Brooklyn USA EEP Brookyn USA Basketball B Basketball A Westwood Basketball STR Elite The Mavericks Warriors The Village 6A 11:00 AM Boys 9th: Sat - Boys 9th: Sat - Boys 8th: Sat - Boys 6th: Sat - No Games No Games Sportika Sportika Sportika Sportika Game #4 Game #3 Game #5 Game #5 Brooklyn USA Brooklyn USA Brooklyn USA Brookyn USA Basketball B Basketball A Basketball Basketball NJ Future STR Elite Hudson Valley The Village 6B Panthers 12:00 PM Boys 10th: Sat - Boys 10th: Sat - Boys 10th: Sat - Boys 6th: Sat - No Games No Games Sportika Sportika Sportika Sportika Game #1 Game #2 Game #3 Game #1 Brooklyn Royal Brooklyn Wolfpack Central Bucks Elite #1 from pool A Crusaders Point Pleasant MSU Cardinals