Privately Speaking Issue #2: Tackling Innovation on a Tight

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Social Media: a Work in Progress for CPG

SocialSocial Media:Media: AA WorkWork inin ProgressProgress forfor CPGCPG AA NationalNational SurveySurvey ofof ManufacturersManufacturers Third Annual Conference “Shopper Strategies: From Insights to Activation” September 21, 2011 325 W. Huron – Suite 714 Tel: (312) 932-0285 [email protected] Chicago, IL 60654 Fax: (312) 932-0286 Agenda Introduction & Background Social Media: 2011 Situation Analysis Who uses social media? How is social media used? How are consumers responding to social media? How are social media evaluated? How successful are social media? Questions 2 About Partners In Loyalty Marketing What We Do 1. Strategic planning 2. Program optimization & oversight 3. Program evaluation Our strength as an organization comes from: Our high level of experience and expertise The fact that we’re a true unbiased 3rd party We have no vested interest in specific technologies, vehicles, or media We take evaluation very seriously. It’s a key driver of program success! Michael Schiff, Managing Partners 15 years of experience in loyalty marketing, customer segmentation and targeting Extensive experience in relationship program development, databases, targeting, and program evaluation 3 Background The Shopper Technology Institute, in collaboration with Partners in Loyalty Marketing (PILM) surveyed manufacturers on the role of Social Media in marketing strategy A brief 20-question online survey was fielded in June-July 2011 Who uses Social Media, and how Social Media’s role in overall marketing strategy Consumer engagement with this new way of connecting to companies and brands Whether Social Media are measureable, and by which metrics How successful Social Media are in achieving business objectives Results are based on responses from 126 manufacturers across CPG industries Including food/beverage, HBC, and general merchandise 4 Average U.S. -

Watching Elon Musk At

2 | TEN YEARS OF 5000 One of the things you do at a 10th anniversary is THIS YEAR MARKS look back. And so we at Inc. did, with your help. We TH THE 10 ANNIVERSARY asked Inc. 5000 multiyear winners to pick the Inc. articles that resonated most with them when they OF THE INC. 5000. were a young company. The chosen stories range from one entrepreneur’s timeless essay about the stress of being the boss—“Entrepreneurial Terror,” by Wilson Harrell in 1987—to the inspiring yarn of an accidental WELCOME entrepreneur who turned her down-and-out city around. That was “Along Came Lolly,” by Tom Foster from 2014. If you missed the full versions of these TO OUR stories when they fi rst ran in Inc., well, your fellow Inc. 5000 winners recommend you read the edited versions of them here. YEARBOOK We hope that you, too, will look back at all you’ve accomplished over the past 10 years—the company F COURSE, INC. HAS been recognizing you’ve grown, the jobs you’ve created, and the obsta- fast-growing companies like yours cles you’ve overcome along the way. The journey for more than 10 years. The whole you’re on as a business owner isn’t measured in yearly thing started in 1979 with a list of or even decade-long chunks, but the 10-year mark is a 100. That leapt three years later to chance to look back, with justifi ed pride, at how far 500. By 2007, with the economy you’ve come. -

Eptica Multichannel Customer Experience Study

RETAIL Eptica Multichannel Customer Experience Study 500 U.S. Retailers Surveyed © Copyright Eptica 2015 / CONTENTS 1/ FOREWORD BY SHEP HYKEN .................................................................................................. 3 2/ EXECUTIVE SUMMARY ............................................................................................................ 4 3/ INTRODUCTION ........................................................................................................................ 5 4/ KEY FINDINGS ......................................................................................................................... 7 5/ CUSTOMER SERVICE VIA THE WEB ......................................................................................11 6/ EMAIL AND CUSTOMER SERVICE .........................................................................................12 7/ SOCIAL CUSTOMER SERVICE ................................................................................................13 8/ CHAT AND CUSTOMER SERVICE ...........................................................................................15 9/ CONSISTENCY ........................................................................................................................16 10/ CONCLUSION AND TAKEAWAYS ............................................................................................ 17 11/ SECTOR COMPARISONS ........................................................................................................21 12/ ABOUT EPTICA .......................................................................................................................27 -

S17-Macmillan-SMP.Pdf

ST. MARTIN'S PRESS APRIL 2017 Get the Sugar Out! Shred It Forever Ian K. Smith From the New York Times #1 bestselling author of the SHRED diets, a book that fills an urgent need and supports all dieters who know cutting sugar is key. Get The Sugar Out! is the ultimate guide to eating well—and frequently —while dieting or making a lifestyle change after a diagnosis of diabetes or pre-diabetes. This book includes more than two dozen food swaps—vegetable and fruit flavored waters instead of soda, grains instead of rice, oven-baked sweet potatoes instead of fries—which are key to an achievable and permanent change in lifestyle. HEALTH & FITNESS St. Martin's Press | 4/25/2017 9781250130136 | $25.99 / $36.99 Can. Structured meal plans and more than 50 easy-to-follow recipes that are both Hardcover | 256 pages | Carton Qty: 24 nutritious and low or no sugar make Get the Sugar Out! both a great primer 9.3 in H | 6.1 in W for first-timers and a rich source of ideas for more knowledgeable readers. Subrights: UK: St. Martin's Press Translation: St. Martin's Press The book includes exercise routines and motivation to get bodies back on a healthy track and kick start weight loss. Other Available Formats: Ebook ISBN: 9781250130143 IAN K. SMITH, M.D., is the bestselling author of SHRED, The Fat Smash Diet, Extreme Fat Smash Diet, and The 4 Day Diet. He was the diet expert for six seasons on VH1’s Celebrity Fit Club, and has created two national health initiatives: the 50 Million Pound Challenge and the MARKETING National One Day Laydown Makeover Mile. -

Behind the Boom

RESEARCH the global leader in e-commerce data IRINTERNET RETAILER BEHIND THE ONLINE APPAREL BOOM There’s an explosion in online sales of apparel. Here are the financial, operating and marketing statistics and trends of the 250 leading apparel e-retailers that are taking all of the growth away from stores. Sponsored by: BEHIND THE ONLINE APPAREL BOOM BY JACK LOVE An exclusive look at who and what is steering U.S. apparel sales to the web from stores. he United States is the largest apparel market in Online Share of U.S. Apparel the world, consuming about 30% of the output of Tthousands of apparel manufacturers—and millions 2014 2015 of their workers—around the globe. And more of America’s retailers are dedicated to selling apparel than any other product line. So when there’s a sea change in the way apparel is 14.8% 17.0% sold, it’s a very big deal. According to a new research report published last month by Internet Retailer, that transformation has begun as billions of dollars of apparel sales are moving from physical stores to the internet. That report, entitled “Behind the Online Apparel Boom,” reveals 220 basis points increase that U.S. websites last year sold an estimated $80 billion in Source: Top500Guide.com apparel, an increase of 19.7% from the prior year, growth that’s fully five percentage points greater than the country’s Amazon’s apparel sales growth came largely at the total e-commerce market. By comparison, U.S. store sales expense of stores, not from other apparel e-retailers. -

St. Martin's Press April 2017

ST. MARTIN'S PRESS APRIL 2017 Blast the Sugar Out! Lower Blood Sugar, Lose Weight, Live Better Ian K. Smith From the New York Times #1 bestselling author of the SHRED diets, a book that fills an urgent need and supports all dieters who know cutting sugar is key. Blast The Sugar Out! is the ultimate guide to eating well—and frequently —while dieting or making a lifestyle change after a diagnosis of diabetes or pre-diabetes. This book includes more than two dozen food swaps—vegetable and fruit flavored waters instead of soda, grains instead of rice, oven-baked sweet potatoes instead of fries—which are key to an achievable and permanent change in lifestyle. HEALTH & FITNESS / DIET & NUTRITION / WEIGHT LOSS St. Martin's Press | 4/25/2017 Structured meal plans and more than 50 easy-to-follow recipes that are both 9781250130136 | $25.99 / $36.99 Can. nutritious and low or no sugar make Blast the Sugar Out! both a great primer Hardcover | 240 pages | Carton Qty: 24 for first-timers and a rich source of ideas for more knowledgeable readers. 9.3 in H | 6.1 in W Subrights: UK: St. Martin's Press The book includes exercise routines and motivation to get bodies back on a Translation: St. Martin's Press healthy track and kick start weight loss. Other Available Formats: Ebook ISBN: 9781250130143 IAN K. SMITH, M.D., is the bestselling author of SHRED, The Fat Smash Diet, Extreme Fat Smash Diet, and The 4 Day Diet. He was the diet expert for six seasons on VH1’s Celebrity Fit Club, and has created two national health initiatives: the 50 Million Pound Challenge and the MARKETING Makeover Mile. -

Decker Announces Broadband Survey

Invite a Friend [email protected] Oct. 15, 2013 Decker Announces Broadband Survey N.C. Commerce Secretary Sharon Decker invites all North (Left-right) GE's Industrial Solutions General Carolina households and businesses to participate in a new Manager of Power Components Norm Sowards, broadband survey. NC Broadband is launching a statewide Governor McCrory's Senior Advisor on Jobs and survey and scorecard project during the month of October to the Economy Tony Almeida, GE's Industrial help households and businesses throughout the state increase Solutions General Manager of Power Equipment their economic vitality by better utilizing broadband Stuart Thompson, and state Senator Josh Stein technologies. "The vision of NC Broadband is to improve the GE Opens New Product competitiveness of North Carolina's businesses and workforce Development Facility in Cary by promoting the use of information technology in education, health care, economic development and all levels of Governor Pat McCrory congratulated GE government," said Decker. "By utilizing this opportunity, our Energy Management for opening its new residents and business leaders can provide valuable feedback office in Cary. The new Cary office co-locates and, as a state, North Carolina can leverage its strength as a GE's engineering and product management leader in the digital economy." with other critical functions under one roof. In addition, it creates a global headquarters for During October, households and organizations will be asked GE's Power Components and Power to conduct an online assessment of their use of broadband Equipment businesses. technologies. The survey results will provide valuable information on broadband usage by North Carolina residents, "GE recognizes North Carolina's educated and commercial and nonprofit organizations, and will allow for workforce and great quality of life," said a comparison of broadband usage and economic impacts with McCrory. -

Buying Unicorns: the Impact of Consumer-To-Consumer Branded Buy/Sell/Trade Communities on Traditional Retail Buying Behavior

University of Richmond UR Scholarship Repository Marketing Faculty Publications Marketing 2018 Buying Unicorns: The Impact of Consumer-to-Consumer Branded Buy/Sell/Trade Communities on Traditional Retail Buying Behavior Catherine Armstrong Soule Sara Hanson University of Richmond, [email protected] Follow this and additional works at: https://scholarship.richmond.edu/marketing-faculty-publications Part of the Business Administration, Management, and Operations Commons, and the Marketing Commons Recommended Citation Soule, Catherine Armstrong and Sara Hanson. "Buying Unicorns: The Impact of Consumer-to-Consumer Branded Buy/Sell/Trade Communities on Traditional Retail Buying Behavior." Journal of the Association for Consumer Research 3, no. 3 (July 2018): 260-276. https://dx.doi.org/10.1086/698416 This Article is brought to you for free and open access by the Marketing at UR Scholarship Repository. It has been accepted for inclusion in Marketing Faculty Publications by an authorized administrator of UR Scholarship Repository. For more information, please contact [email protected]. CONSUMER RESPONSE TO THE EVOLVING RETAILING LANDSCAPE Buying Unicorns: The Impact of Consumer-to- Consumer Branded Buy/Sell/Trade Communities on Traditional Retail Buying Behavior CATHERINE ARMSTRONG SOULE AND SARA HANSON ABSTRACT Branded buy/sell/trade (BBST) is a consumer-to-consumer (C2C) selling phenomenon that is both mas- sive in scale and meaningful in its impact on consumer behavior and the traditional retailing landscape. Consumers buy, sell, and trade one focal brand’s products in these social media-hosted, consumer-initiated communities. This ar- ticle introduces the phenomenon, differentiates it from other forms of C2C exchange, and explores relationships be- tween members and the brand. -

A Strategic Plan for a Greater Lexington ACCOMPLISHMENTS

2020 RENAISSANCE – A Strategic Plan for a Greater Lexington ACCOMPLISHMENTS June 2013 – June 2018 Accomplishments June 2013 through June 2018 Updated 7/11/2018 OVERVIEW OF ACCOMPLISHMENTS Business / Job Development City Council endorsed Business Development Consortium Strategic Plan Contract through ElectriCities Retail Strategies (Lacy Beasley) for recruitment – Atlanta show, Charlotte show, Las Vegas show Promoting successes on City website - Uptown Lexington businesses that were recognized for façades; Lolly Wolly Doodle and Image Wizards publicity Completed Phase I feasibility and Phase II of a “Food Hub” or "Farm to Table" initiative - entrepreneurs invited to participate via website news “Lexington, NC Local First” trademark logo to promote support for existing businesses Increased CityWiFi access in Depot District Installed Uptown Lexington’s CityWiFi medallions – decorating streets and promoting CityWiFi Land purchase and amendment to United Furniture economic development expansion grant agreement - total of $3,250,000 investment and 400 jobs Lexington’s entrepreneurial initiative featured on Fox 8 News – January 12, 2014 with additional exposure via website news Ordinance amendment to permit and regulate Food Trucks Assisted with opening of approximately 10 new local businesses Issued Major Zoning Permits for Taco Bell, Walmart Neighborhood Market, Huntington Place Apartments, Family Dollar, Bojangles Issued 63 Certificates of Occupancy for new businesses Represented at International Council of Shopping Centers -

Spring/Summer 2013

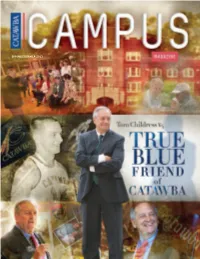

2013 UMMER /S NG I R SP SPRING/SUMMER 2013 CATAWBA CAMPUS MAGAZINE www.catawba.edu PAID PERMIT 29 U. S. Postage U. Salisbury, NC Salisbury, Non Profit Org. Non Profit A N BURY S SALI www.catawba.edu 1.800.CATAWBA www.catawba.edu NORTH CAROLI Office Relations Public of 2300 W Innes St NC 28144-2488 Salisbury, SPRING/SUMMER 2013 October 18-20 DATE THE SAVE FEATURES Register online by October 8 www.catawba.edu/homecoming CATAWBA KUDOS 8 Catawba makes Forbes’ Grateful Grads Index EdiTOR & CHIEF COMMUNicaTIONS OFFICER Tonia Black-Gold McCORKLE’S 12 DIRECTOR OF GRapHic DESIGN SERVicES McCorkle’s to serve & PHOTOGRAPHER Starbucks® Products Tracy MacKay-Ratliff 704.637.4394 www.catawba.edu/giving STAFF COORDINATOR Nancy Mott What is the Catawba fund? WEB DEsiGNER & DEVELOPER COMMENCEMENT 16 The Catawba Fund is a giving umbrella Just as others provided Maegen G. Worley under which the following categories The Class of 2013, dignitaries support while you were here, of support for Catawba are grouped: SPORTS INFORMATION DIRECTOR & guests gathered to celebrate now you hold the key to assist James D. Lewis ’89 at commencement exercises General Unrestricted Giving the next generation. affects the entire College and every individual in it — every program, every Your assistance allows Catawba ALUMNI UpdaTES TOM CHILDRESS 38 activity, every aspect of the institution. to offer the best facilities, [email protected] These funds are applied directly hire the best faculty & to current operating expenses. True Blue, Tom Childress ’64 ADDREss CHANGES attract the best students. retired May 31st Campus Magazine, Catawba College Unendowed Student Aid 2300 W Innes St, Salisbury, NC 28144-2488 comprises the majority of the large We can direct funds immediately financial assistance program Catawba uses to things that are important to you to assist students in attending the College. -

Silicon Harbor

See the Future on SILICON HARBOR 2015 LOOKBOOK #EXPLORE Photo: Ron Cogswell The South Rises Again (but not like that) Is Elon Musk the Marco Polo of our age? Jeff Bezos the The new explorers who capitalize on this opportunity are Magellan? Are Google developers akin to Edison’s Menlo exactly who you will find at DIG SOUTH. In their honor, Park inventors? we declare the Festival theme for 2015 to be a simple call to action: #Explore. From Google Glass to SpaceX, we’ve entered a new age of exploration. The winners in this wild frontier will be Yes, the South is rising … but not in the way some the innovators, disruptors and startup hustlers now sailing old-timers might proclaim. It’s a new day, time to write into unchartered waters, upending old worlds as they hit the next chapter. So join us in Charleston to get inspired shore and planting their flags deep into the firmament. and tell us why your brilliant idea is next in line, poised for the big time and ripe for funding. Closer to home, the South is experiencing a moment of its own. And people like AOL founder Steve Case sense The revolution continues… the potential, declaring that through his Revolution fund he intends to seek and support high-impact, homegrown startups outside of traditional tech centers like Silicon Valley, Seattle and Boston. Case calls the movement “The Rise of the Rest.” And he is looking southward. Stanfield Gray 2 | DIG SOUTH 2015 FESTIVAL SCHEDULE MON, APRIL 27 TUES, APRIL 28 WED, APRIL 29 PRE-CONFERENCE DIG CONFERENCE & DIG SHOW REGISTRATION & BADGE PICK UP REGISTRATION & BADGE PICK UP REGISTRATION & BADGE PICK UP DIG MASHUP 11 AM – 7 PM | CINEBARRE 11 AM – 7 PM | CINEBARRE 7 AM – 7 PM | CINEBARRE Presented by OPEN SOURCE CHS 963 Houston Northcutt Blvd, Mt. -

Banking on the Future New Financing Models Are Emerging to Accom- Modate Metrics That Don’T Fit the Old Mold

BANKING ON THE FUTURE NEW FINANCING MODELS ARE EMERGING TO ACCOM- MODATE METRICS THAT DON’T FIT THE OLD MOLD. LISA JOHNSTON irect-to-consumer selling certainly isn’t for the faint of heart, and no one knows that better than those who are financing the brands going this route. D While retail has taken its share of lumps over the years—and will undoubtedly continue to do so—DTC sellers operate on a formula that combines the uncertainty of consumer behavior with a lack of sales history to predict future performance. What’s more, many DTC financing being cobbled together—convertible hyper growth that especially sets them apart. apparel and footwear brands rely heavily upon notes/friends-and-family money, etc.—in the Wholesalers typically experience a significant social media for their marketing strategies, [small and medium enterprise] space.” expansion by receiving an open order from a which can cause customer acquisition rates Roli Saxena, chief customer officer of B2B new retailer, which carries a longer lead time to fluctuate wildly. As such, many traditional solutions provider Brex, agreed that the and is easier for a bank to digest, said Eric Fisch, financing options fail to translate into secure banking industry has failed to keep up. head of retail and apparel, commercial banking lending experiences. “It’s not just legacy banking, but legacy at HSBC. Brick-and-mortar retailers, meanwhile, “Most lenders are still struggling to financing broadly,” she said. “Banks have similar grow through expanded store presence, which is provide good financing solutions to DTC/ underwriting policies for all businesses, and a more gradual capital constraint.