Weekly Trends

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Sustainability from the Ground up Eldorado Gold

Eldorado Gold 2020 Sustainability Report Sustainability from the Ground Up Eldorado Gold About 2020 Sustainability Report This 2020 Sustainability Report (the “Report”) has been produced Other In-Country Sustainability Reporting in accordance with the requirements of the core Global Reporting In addition to this report, our Greek subsidiary, Hellas Gold S.A., Initiatives (“GRI”) standards, and includes data on Eldorado Gold publishes a GRI-aligned Corporate Social Responsibility report, and Corporation’s (“Eldorado” or the “Company”) five producing mines our Turkish subsidiary, Tüprag Metal Madencilik Sanayive Ticaret A.S., in 2020 as well as construction, development and exploration publishes a biannual magazine called Altin Sayfa (Golden Pages) projects. However, the performance data focuses on our producing that includes articles, case studies and news relevant to our Turkish assets – Kışladağ, Lamaque, Efemçukuru, Olympias and Stratoni. Data mines’ social and environmental performance during the period. represents the full 2020 calendar year and, unless otherwise noted, Our Lamaque project, Eldorado Gold Québec, produces a biannual all costs are reported in US dollars. Although the Sustainability Report information bulletin that discusses the project’s health and safety, and is not externally verified, all data and content have been prepared and environmental and social performance and programs. The bulletin is reviewed internally by our management teams and the Sustainability distributed by mail to residents of the Abitibi-Témiscamingue region of Committee of the Board of Directors. Québec, Canada. Please note that, where applicable, restatements of prior year data have been highlighted throughout the Report. Restatements occur as a result of updated or more accurate data becoming available after the publication of our previous Sustainability Report on June 25, 2020. -

Financial Review

Financial Review Management’s Discussion and Analysis of Financial Condition 29 and Results of Operations Management’s Responsibility for Financial Reporting 55 Independent Auditors’ Report of Registered Public Accounting Firm 56 Report of Independent Registered Public Accounting Firm 57 Consolidated Balance Sheets 58 Consolidated Income Statements 59 Consolidated Statements of Comprehensive Income 60 Consolidated Statements of Cash Flows 61 Consolidated Statements of Changes in Equity 62 Notes to the Consolidated Financial Statements 63 Board of Directors, Officers and Senior Management Team 99 Mineral Reserves 100 Mineral Resources 101 Shareholder Information 102 Corporate Information 103 Cautionary Note About Forward-Looking Statements and Information 104 28 Eldorado gold Annual Report 2014 MANAGEMENT’S DISCUSSION and ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS (MD&A) for the year ended December 31, 2014 Throughout this MD&A, Eldorado, we, us, our and the Company mean Eldorado Gold Corporation. This year means 2014. All dollar amounts are in US dollars unless stated otherwise. The information in this MD&A is as of February 19, 2015. You should also read our audited consolidated financial statements for the year ended December 31, 2014. We prepare our consolidated financial statements in accordance with International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board (“IASB”). We file them with appropriate regulatory authorities in Canada and the United States. You can find more information about Eldorado, including our Annual Information Form, on SEDAR at www.sedar.com. About Eldorado Based in Vancouver, Canada, Eldorado owns and operates mines around the world. Its activities involve all facets of the mining industry including exploration, development, production and reclamation. -

Corporate Donations Program

Corporate Donations Program Issuers supporting the advancement of the investor relations profession in Canada Canadian Investor Relations Institute 601, 67 Yonge St. Toronto, ON M5E 1J8 CIRI.org To learn more, contact Yvette Lokker at 416-364-8200. The Canadian Investor Relations Institute’s (CIRI) mandate is to contribute to the transparency and integrity of the Canadian capital market by advancing the practice of investor relations, the professional competency of its members and the stature of the profession. OUR FOCUS Financial support through the CDP Since CIRI began in the early 1990s, we have provided ensures that CIRI can continue its professional development; resources; and issues advocacy and efforts to enhance the integrity of education to our 500 members across Canada. CIRI has been the Canadian capital markets instrumental in evolving the IR role in Canada from a tactical through research, advocacy and communications function to a strategic multi-disciplinary education of investor relations profession. professionals throughout Canada. WHY ISSUERS CONTRIBUTE At ARC we believe this is an important service to Canadian As a Corporate Donations Program (CDP) participant, your companies and institutional and company will be contributing to the advancement of the retail shareholders. investor relations profession in Canada. Your donation will be used to support the three key pillars for the advancement of IR David Carey in Canada: professional development; resources; and issues Past SVP, Capital Markets, ARC Resources advocacy and education, areas where CIRI invests more than CDP Participant Since 2009 $500,000 annually. CDP PARTICIPANTS The following issuers are committed to HOW YOU CAN MAKE A DIFFERENCE advancing the investor relations profession in Canada: Whether through a multi-year commitment or a one-time donation, your company will be recognized as a CDP Visionary participant and will be assisting CIRI in fulfilling its mandate. -

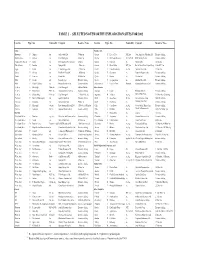

Selected Noteworthy Exploration Sites for 2002

TABLE 2 - SELECTED NOTEWORTHY EXPLORATION SITES FOR 2002 Location Type1 Site Commodity Company Resource2 Notes Location Type1 Site Commodity Company Resource2 Notes Africa Canada, cont. Botswana F Mupane Au Gallery Gold Ltd. 795koz Au Ontario P Lac des Iles PGE, Au North American Palladium Ltd. Extensive drilling Burkina Faso F Kalkasa Au Cluff Mining plc 470koz Au Ontario E McCreedy West area Ni, Cu, PGE FNX Mining Co. Inc. Extensive drilling Congo, Dem. Rep. of P Lonshi Cu First Quantum Minerals Ltd. 356kt Cu Ontario P Red Lake Au Goldcorp Inc. 5.2Moz Au Côte d’Ivoire E Bonikro Au Equigold NL 1.3Moz Au Ontario E River Valley PGE, Au Pacific North West Capital Corp. 1Moz PGE+Au Egypt F Sukari Au Centamin Egypt Ltd. 1.74Moz Au Quebec F Casa Berardi West Au, Cu Aurizon Mines Ltd. 1.4Moz Au Ghana F Chirano Au Red Back Mining NL 1.06Moz Au Quebec E Clearwater Au Eastmain Resources Inc. Extensive drilling Guinea P Lero area Au Kenor ASA 2.94Moz Au Quebec P Doyon Au Cambior Inc. Extensive drilling Mali P Sadiola Au Iamgold Corp. Extensive drilling Quebec P Sleeping Giant Au Aurizon Mines Ltd. Extensive drilling Mali F Segala/Takakoto Au Nevsun Resources Ltd. Extensive drilling Saskatchewan F Fort à la Corne Diamond Kensington Resources Ltd. Extensive drilling S. Africa F Blue Ridge PGE, Au Cluff Mining plc 4.6Moz PGE+Au Latin America S. Africa P Platreef area PGE, Au Anooraq Resources Corp. Extensive drilling Argentina F Esquel Au Meridian Gold Inc. Extensive drilling S. Africa E Sheba's Ridge PGE, Au Cluff Mining plc 17.4Moz PGE+Au Argentina D Veladero Au, Ag Barrick Gold Corp. -

AI Powered International Equity ETF Schedule of Investments August 31, 2020 (Unaudited)

AI Powered International Equity ETF Schedule of Investments August 31, 2020 (Unaudited) Shares Security Description Value COMMON STOCKS - 99.4% Argentina - 1.1% 360 Globant SA (a) $ 63,929 Australia - 3.3% 512 Atlassian Corporation plc - Class A (a) 98,182 700 Australia & New Zealand Banking Group, Ltd. - ADR 9,463 3,684 Mesoblast, Ltd. - ADR (a) 71,323 1,568 National Australia Bank, Ltd. - ADR 10,396 189,364 Belgium - 1.5% 233 Galapagos NV - ADR (a) 31,026 1,375 Materialise NV - ADR (a) 55,908 86,934 Canada - 38.0% 7,200 Alexco Resource Corporation (a) 22,248 1,089 Algonquin Power & Utilities Corporation 15,061 914 Aurinia Pharmaceuticals, Inc. (a) 13,555 12,605 Auryn Resources, Inc. (a) 24,580 1,140 B2Gold Corporation 7,684 2,052 Ballard Power Systems, Inc. (a) 34,063 1,650 Barrick Gold Corporation 48,923 132 BCE, Inc. 5,677 4,774 BlackBerry, Ltd. (a) 24,920 748 Brookfield Asset Management, Inc. - Class A 25,238 1,049 CAE, Inc. (a) 16,585 376 Canada Goose Holdings, Inc. (a) 9,208 462 Canadian National Railway Company 48,316 1,963 Canadian Natural Resources, Ltd. 38,612 146 Canadian Pacific Railway, Ltd. 43,169 1,491 Canadian Solar, Inc. (a) 48,443 1,635 Canopy Growth Corporation (a) 26,963 840 Canopy Growth Corporation (a) 13,877 2,220 Cascades, Inc. 23,607 2,744 Celestica, Inc. (a) 21,815 11 Constellation Software, Inc. 12,734 1,064 Descartes Systems Group, Inc. (a) 64,851 2,039 Dollarama, Inc. 79,600 1,597 Eldorado Gold Corporation (a) 18,238 13,136 EMX Royalty Corporation (a) 38,357 17,174 Enerplus Corporation 45,511 1,337 Fortis, Inc. -

Fools Gold Eldorado Gold

SO M O Fool’s Gold How Canadian firm Eldorado Gold destroys the Greek environment and dodges tax through Dutch mailbox companies SOMO March 2015 Fool’s gold | noun [U] UK 1. a yellow metal that looks like gold 2. something that you are very attracted to that you later find is not worth very much Colophon Fool’s Gold How Canadian firm Eldorado Gold destroys the Greek environment and dodges tax through Dutch mailbox companies March 2015 Authors: Ilona Hartlief, Katrin McGauran, Roos van Os, Indra Römgens Copy editor: Vicky Anning Layout: Frans Schupp Photo: Giannis Papanikos (www.demotix.com) ISBN: 978-94-6207-056-1 This publication was made possible through the financial support of the Halifax Initiative (Canada), InterPares (Canada), Mining Watch Canada and the Sigrid Rausing Trust (UK). SOMO would particularly like to thank individual supporters of this research who responded to a crowdfunding campaign. Besides a number of SOMO staff members, these are Jasper Blom, Tineke Egyedi, Rob Geurtsen, Mariska de Gooijer, Hugo Hoes, Marianne van Kalmthout, Gijsbert Koren, Lieke Ruijmschoot, Bahar Sakizlioglu, Georgios Smaragdos, David Sogge and Gemma Toppen. The content of this publication is the sole responsibility of SOMO. The authors would like to thank the following people for their substantial contributions to this report: Marica Frangakis (freelancer), Kees Hudig (freelancer), Maria Kadoglou (Hellenic Mining Watch), Karyn Keenan (Halifax Initiative), Jamie Kneen (MiningWatch Canada), Matti Kohonen (freelancer) and Theodora Oikonomides (freelancer). The following people reviewed specific sections of the report; their comments and additions were also invaluable: David Bruer (InterPares), George Chasiotis (WWF Greece), Roberta Cowen (SOMO), Rodrigo Fernandez (SOMO/University of Leuven), Christina Laskaridis (Corporate Watch), Patrick Kryticous Nshindano (ActionAid Zambia), Sol Picciotto (Lancaster University), Gerhard Schuil (SOMO) and Francis Weyzig (Oxfam Novib). -

Technical Report Lamaque Project Québec, Canada

Technical Report Lamaque Project Québec, Canada Project Location: Bourlamaque Township, Province of Québec, Canada (NTS: 32C/04) (UTM: 293960E, 5329260N) (NAD 83, Zone 18) Effective Date: March 21st, 2018 Signature Date: March 29th, 2018 Qualified Person Company Mr. Colm Keogh, P.Eng. Eldorado Gold Corporation Mr. Jacques Simoneau, P.Geo. Eldorado Gold Corporation Dr. Stephen Juras, Ph.D., P.Geo. Eldorado Gold Corporation Ms. Marianne Utiger, P.Eng. WSP Canada inc. Mr. François Chabot, P.Eng. Eldorado Gold Corporation. L AMAQUE P ROJECT, Q UÉBEC, C ANADA T ECHNICAL R EPORT TABLE OF CONTENTS SECTION • 1 EXECUTIVE SUMMARY ......................................................................................... 1-13 Introduction ................................................................................................. 1-13 Contributors and Qualified Persons ........................................................... 1-13 Property Description and Ownership .......................................................... 1-14 Accessibility, Climate, Local Resources, Infrastructure and Physiography .............................................................................................. 1-15 Geology and Mineralization ........................................................................ 1-15 Drilling, Sampling Method, Approach and Analyses .................................. 1-16 Metallurgical Testing ................................................................................... 1-17 Mineral Resource Estimates...................................................................... -

Eldorado Gold Year in Review 2017 About “Tomorrow, Together”

1 ELDORADO GOLD Tomorrow, Together Eldorado Gold Year in Review 2017 About “Tomorrow, Together” “Tomorrow, Together” is a reflection of our belief that in mining the hard work of taking a project from exploration to reclamation can only be done with support from, and in partnership with, our employees, local communities and host governments. Our goal is to work with our stakeholders to build a stronger future. This 2017 Year in Review report (the “Report”) has been produced Table of Contents in accordance with the requirements of the “Core” Global Reporting Initiative (GRI) fourth generation (G4) Sustainability Reporting Guidelines, Eldorado Gold at a Glance ..................................................................1 and includes data on Eldorado Gold Corporation’s (“Eldorado” or “the Letter from the President & CEO ........................................................ 2 Company”) four producing mines in 2017, as well as its construction and development projects. However, the performance data focuses on our Our Business ................................................................................ 4 producing assets – Kışladağ, Efemçukuru, Olympias and Stratoni. As our 2017 Key Outcomes ....................................................................... 5 Lamaque site was acquired part way through 2017, its operations are not Creating Value Throughout the Mining Life Cycle ........................... 6 included in this Report unless otherwise noted. Data represents the full Our Products ............................................................................... -

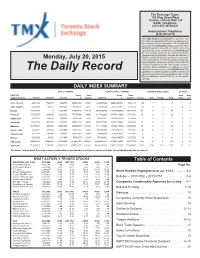

The Daily Record Is Published by TSX Inc

The Exchange Tower, 130 King Street West Toronto, Ontario M5X 1J2 Editor Telephone: (416) 947-4655/4231 Subscriptions Telephone: (416) 947-4778 The Daily Record is published by TSX Inc. TSX Inc. does not guarantee either the completeness or the accuracy of this information. The information contained in the Daily Record is provided for infor- mational purposes only and you agree not to rely upon the information contained in the Daily Record for any trading, business or financial purpose. These sheets are printed in Canada and issued by Monday, July 20, 2015 TSX Inc. under the express condition, to which ev- eryone purchasing or making use thereof assents, that no liability shall be incurred by TMX Group or its affiliated companies or any other vendor or donor, including, without limitation, for reliance on or for The Daily Record any errors or inaccuracies in the Daily Record. This publication is under copyright. © 2015 TSX Inc. All rights reserved. Do not copy, distribute, sell or mod- ify this publication without TSX Inc.’s prior written consent. DAILY INDEX SUMMARY ––——————————————————————— DAILYTRADING ———————————————— YEAR-TO-DATETRADING ————————— ADVANCES/DECLINES————— 52 WEEK— S&P/TSX Value Trans- Value Trans- New New Capped Sectors Volume Adv/Vol Dec/Vol $ actions Volumes $ actions Traded Adv Unchg Decl High Low Cons. Discret. 5321120 1729763 3359767 206887384 31803 1089910698 44352856586 5501117 25 7 1 17 1 0 Cons. Staples 2225030 141827 2083203 92102107 14217 459836644 20546195819 2554564 10 1 0 9 4 1 Energy 43181487 0 43181487 577883443 149718 8674886468 118926066609 26215473 52 0 0 52 0 17 Financial 14732655 1429923 13302732 777708805 75842 3127292236 157500113892 13761326 25 3 0 22 0 1 Health Care 1818123 358834 458616 96341694 5839 270461971 22041906638 1078098 6 2 1 3 2 0 Industrials 11342263 2627206 8715057 298017225 40881 2407827763 50700138667 6360509 22 5 0 17 0 2 Materials 64640947 839480 63801467 630295075 194622 7444464968 87262115792 20210500 48 2 0 46 1 17 Inform. -

Présentation Powerpoint

A Capital Opportunity A Global Market for Mining Companies Disclaimer This document is for information purposes only. While the information herein is collected and compiled with care, neither TMX Group Limited nor any of its affiliated companies represents, warrants or guarantees the accuracy or the completeness of the information. You agree not to rely on the information contained herein for any trading, legal, accounting, tax, investment, business, financial or other purpose. This information is provided with the express condition, to which by making use thereof you expressly consent, that no liability shall be incurred by TMX Group Limited and/or any of its affiliates as a result of any errors or omissions herein or any use or reliance upon this information. 2 © 2014 TSX Inc. All rights reserved. Do not sell or modify without the prior written consent of TSX Inc. Canada and TSX: Strong Fundamentals Economically stable • Canada is the fifth largest equity market by float capitalization in the MSCI World Index • World’s soundest banking system • Lowest debt-to-GDP among G7 • Strong equity culture • ~$2.4 Trillion in market cap • $270 billion in equity capital raised in last 5 years Resource rich • World’s largest producer of zinc and uranium and major producer of gold, nickel, aluminum and lead • #1 in resource listings 3 The World Lists on TSX and TSXV TSX and TSXV International Listings by Country/Region Total International Listings as at December 31 2013= 314 TSX = 164 Listings | QMV=$151 B TSXV = 150 Listings | QMV= $2.8 B 4 The World -

Board Shareholder Confidence Index 2015

Board Shareholder Confidence Index 2015 Developed in spring 2003, the Board Shareholder Confidence Index comprises factors often used by active shareholders to assess Boards of Directors*. While there are other variables not in our model that contribute to the effectiveness of Boards -- including elements that can only be observed from inside the boardroom -- we capture factors affecting shareholders’ confidence in the Boards’ abilities to fulfill their duties. These factors are different from the TSX Guidelines for effective corporate governance in that they take into account the shareholders’ perception of risk. Based on factors available to those outside the walls of the boardroom, we evaluate and rank Boards of Directors by their potential to act in an effective way and by their performance, as indicated by past practices. The score is developed using four linked steps. The result is a transparent, objective, and adaptable rating system that assigns companies listed on the S&P/TSX Composite Index a score out of 150. *Please see the BSCI 2015 Methodology for further details. Sections in Report: 1 - Totals (10 pages) 2 - Individual Potential (10 pages) 3 - Group Potential (6 pages) 4 - Board Decision Output (6 pages) Joseph L. Rotman School of Management Tel: (416) 978-8998 105 St. George Street, Toronto, Ontario M5S 3E6 1/33 Email: [email protected] TOTALS Joseph L. Rotman School of Management Tel: (416) 978-8998 105 St. George Street, Toronto, Ontario M5S 3E6 2/33 Email: [email protected] 2015 Board Shareholder Confidence Index TOTALS Information on scoring can be found on our website at http://goo.gl/SCt3lU SCORE / INDIVIDUAL BOARD DECISION TICKER COMPANY 150 POTENTIAL GROUP POTENTIAL OUTPUT Maximum Deduction 0 -31 -54 -65 AAV Advantage Oil and Gas Ltd 99 -2 -11 -38 ARE Aecon Group Inc. -

Resources Participating Companies.Indd

BMO CAPITAL MARKETS 2007 GLOBAL RESOURCES CONFERENCE TAMPA, FLORIDA • FEBRUARY 25 - 28 • SADDLEBROOK RESORT INVITED COMPANIES Join BMO Capital Markets at the Saddlebrook Resort in Tampa for our 16th Annual Global Resources Conference. This three-day event brings together senior management from over 100 of the world’s leading mining and precious metals companies. One of the hallmarks of this conference is the opportunity for interaction with senior management – including one-on-one meetings as well as informal events such as evening activities and golf. For further registration details, please contact your BMO Capital Markets sales representative. Invited companies include* Aurizon Mines Ltd. Eldorado Gold Corporation Adamus Resources Ltd. Aurora Energy Resources Inc. Electrum USA Ltd. Aflease Gold Ltd. Australian Solomon Gold Ltd. Energy Fuels Inc. African Copper plc. Axmin Eurasian Natural Resources African Platinum Plc BHP Billiton plc Equinox Minerals Limited Agnico-Eagle Mines Ltd. Baffinland Iron Mines Corp. European Goldfields Limited Alamos Gold Inc. Banro Corp Farallon Resources Ltd. Alcan Inc. Bear Creek Mining Co. First Quantum Minerals Ltd. Alcoa Inc. Barrick Gold Corporation First Uranium Corp. Allegiance Bendigo Mining Limited FNX Mining Co. Inc . Alferon Management Birim Goldfields Inc. Freeport-McMoran Copper & Gold Inc. Altius Minerals Corp. Breakwater Resources Ltd. Gabriel Resources Ltd. Amerigo Resources Ltd. Buenaventura S.A. (Cia de Minas) Gammon Lake Resources Ltd. Anatolia Minerals Development Ltd. Cameco Corporation GBS Gold International Inc. Andagan Resource Corp. Canadian Royalties Inc. Geovic Mining Corp. Andean Resources Ltd. Centenario Copper Corp. Glencairn Gold Andina Minerals Inc. Centerra Gold Inc. Global Alumina Corporation Anglo American plc Century Aluminum Company Globestar Mining AngloGold Ashanti Limited Cleveland-Cliffs Inc.