JOHCM UK Equity Income Fund Monthly Update

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

COVID-19 Proxy Governance Update

COVID-19 Proxy Governance Update 2020 AGM mid-season review FROM EQUINITI 01 Looking back and planning ahead It is incredible to note that it has been over 12 weeks since the official announcement on 23 March of the UK Government’s Stay at Home Measures, and nearly seven months since the severity of the pandemic became apparent in China. Over the said period, PLC boards, company secretaries and investor relations officers have kept their corporate calendars going thanks to rapid adoption of modified regulatory guidelines and inventive modes of engagement with investors. With annual general meetings being an obvious highlight in the corporate calendar, we take stock of the progress made so far over the 2020 AGM season, as well as using what we learned to plan ahead. Now that we are over the first ‘hump’ with the busy period of May AGMs out of the way, we are readying for the second ‘peak’ of June and July AGMs, and then an ‘easing’ until the second ‘mini’ season in the early autumn. As such, in this update, we look at: • 2020 AGM season statistics…so far • Proxy adviser engagement and ISS recommendations review • High-level assumptions for Q3 and Q4 • Relevant updates from the regulators, industry bodies and proxy advisers • Communications in the COVID-19 world – special commentary by leading financial PR firm,Camarco • How has COVID-19 impacted activism – special commentary by international law firm,White & Case 02 2020 AGM Season Statistics…so far Scope of data To assess progress and forecast what is to come, we look at the key statistics for the UK AGM season 2020 thus far. -

Aberdeen Standard Select Portfolio

Aberdeen Standard Select Portfolio This Fund Summary is for the following ILP sub-fund and should be read in conjunction with the Product Summary Aberdeen Standard India Opportunities Fund Aberdeen Standard Pacific Equity Fund Aberdeen Standard Singapore Equity Fund Aberdeen Standard Thailand Equity Fund Structure of ILP Sub-Fund The ILP Sub-Fund is an open-ended feeder fund and invests all or substantially all of its assets into the underlying Aberdeen Standard Select Portfolio which offers a group of separate and distinct portfolios of securities or obligations, each of which being a sub-fund investing in different securities or portfolios of securities. The units in the ILP Sub-Fund are not classified as Excluded Investment Products. Information on the Manager (the “Underlying Manager”) The Underlying Manager of Aberdeen Standard Select Portfolio (the “Underlying Fund”) Aberdeen Standard Investments (Asia) Limited, a wholly-owned subsidiary of the Aberdeen Asset Management PLC (the “Aberdeen Group”), was established in Singapore in May 1992, as the regional headquarters of the Aberdeen Group to oversee all of its Asia-Pacific assets, including collective investment schemes. In August 2017, Aberdeen Asset Management PLC merged with Standard Life plc to form Standard Life Aberdeen plc and Aberdeen Asset Management PLC became a wholly owned subsidiary of Standard Life Aberdeen plc (collectively the “Group”). Aberdeen Standard Investments is the asset management division of the Group. As at end December 2020, Aberdeen Standard Investments had over US$635.2 billion worth of assets under its management. The Aberdeen Group Standard Life Aberdeen plc was created in August 2017 from the merger of Aberdeen Asset Management plc and Standard Life plc. -

M&G (Lux) Investment Funds 1 M&G (Lux) Global Dividend Fund EUR A

31 May, 2021 M&G (Lux) Investment Funds 1 M&G (Lux) Global Dividend Fund EUR A This fund is managed by M&G Luxembourg S.A. EFC Classification Equity Global Price +/- Date 52wk range 12.65 EUR 0.10 28/05/2021 9.19 12.71 Issuer Profile Administrator M&G Luxembourg S.A. The fund has two aims: • To provide a combination of capital growth and income to deliver Address 16, boulevard Royal 2449 a return that is higher than that of the global stockmarket over any five-year period; • To increase the income stream every year in US dollar terms. Core investment: At least 80% City Luxemburg of the fund is invested in the shares of companies across any sector and of any size that Tel/Fax +33 (0)1 71 70 30 20 are domiciled in any country, including emerging markets*. The fund usually holds shares Website www.mandg.com in fewer than 50 companies. Other investment: The fund also holds cash or assets that can be turned quickly into cash. * Emerging market countries are defined as those included within the MSCI Emerging Markets Index and/or those included in the World General Information Bank’s definition of developing economies, as updated from time to time. Strategy in brief: ISIN LU1670710075 The investment manager focuses on companies with the potential to grow their dividends Fund Type Capitalization over the long term. The investment manager selects stocks with different sources of Quote Frequency daily dividend growth to build a... Quote Currency EUR Currency USD Chart 5 year Foundation Date 18/07/2008 Fund Manager Stuart Rhodes Legal Type Investment -

2016 Annual Report

bovishomesgroup.co.uk Bovis Homes Group PLC Annual report and accounts Bovis Homes Group PLC, The Manor House, North Ash Road, New Ash Green, Longfield, Kent DA3 8HQ. www.bovishomesgroup.co.uk 2016 Designed and produced by the Bovis Homes Graphic Design Department. Printed by Tewkesbury Printing Company Limited accredited with ISO 14001 Environmental Certification. Printed using bio inks formulated from sustainable raw materials. Printed on Cocoon 50:50 silk a recycled paper containing 50% recycled waste and 50% virgin fibre and manufactured at a mill certified with ISO 14001 environmental management standard. The pulp used in this product is bleached using an Elemental Chlorine Free process (ECF). When you have finished with this pack please recycle it. Annual report and accounts 2016 Bovis Homes Group PLC When you have finished with this pack please recycle it. Annual report and accounts Strategic report Business overview 4 2 2016 highlights Chairman’s statement A review of our business 4 Chairman’s statement model, strategy and Ian Tyler discusses how the 6 What we do summary financial and Group is well placed for 7 Reasons to invest operational performance the future 10 Housing market overview Our business and strategy 12 Interim Chief Executive’s report 18 Our business model 20 Strategic priorities 26 Principal risks and uncertainties 30 Risk management 12 Corporate social responsibility Interim Chief Executive’s report 32 Our CSR priorities Earl Sibley provides an overview of the year and Our financial performance discusses the -

Standard Life Aberdeen (SLA); FTSE 100; Financial Services

Selling: Standard Life Aberdeen (SLA); FTSE 100; Financial Services Managing a portfolio is a lot like managing a garden. In gardening there are regular recurring tasks such as trimming back fast-growing plants and replacing unattractive plants with more attractive alternatives. In a portfolio this means regularly trimming back oversized positions and replacing unattractive holdings with more attractive alternatives. Average purchase price Current price Holding period (including investment in Aberdeen AM) £3.76 £2.90 Feb 2016 to Apr 2021 (5yrs 2mo) Capital gain Dividend income Annualised return (including return of capital from de-mergers) -13.4% 31.2% 4.0% “Standard Life Aberdeen is one of the world’s largest investment companies, the largest active manager in the UK and one of the largest in Europe. It has a significant global presence and the scale and expertise to help clients meet their investment goals.” Overview Standard Life Aberdeen (SLA) originally joined the model portfolio in 2016 as Aberdeen Asset Management, which was then the second largest active fund manager in the UK (second only to Schroders). This investment worked out well, with the 2017 merger of Aberdeen and Standard Life leading to annualised return of 17% at the merger date. I decided to hold on to the SLA shares post merger because Standard Life was a leading asset manager and the combined group promised additional economies of scale and a more diverse and robust business. Four years later and as a more experienced investor, I now think both companies lacked durable competitive advantages and I think that’s true of the combined business too. -

WHAT ARE INVESTMENT ASSETS? • Assets Are What Your Fund Invests In

PORTFOLIO BOND (IPS) – FUNDS KEY FEATURES 5 WHAT ARE INVESTMENT ASSETS? • Assets are what your fund invests in. • The assets that a fund invests in will have a significant impact on the performance of your investment. It’s important that you understand the differences between the main types of assets. • There are four main types of asset and each has its own characteristics: − Equities − Fixed interest securities − Commercial property − Cash. • It’s generally a good idea to invest in a number of different assets so you don’t rely on the performance of one individual asset. This strategy, called ‘diversification’, is basically what funds offer as they spread your investment across lots of assets. • Many funds also invest in more than one type of asset to create even more diversification. • Investing in a mix of funds is another good way to spread your investment. WHAT ARE EQUITIES? NOTES • Equities (also known as 'shares') are a share in a company that allows the owner of those shares to participate in any financial success achieved by • Over the short term, the that company. value of funds investing in equities can go up and • Equities can achieve growth in two ways: down a lot. − Through increases in share prices. The share price reflects the • Company share prices can underlying value of the company. also change dramatically in − Through dividends, which are regular payments made to shareholders response to the activities generally based on the company’s annual profits. and financial performance of individual companies, • Investing in equities is considered by many investment experts to be one as well as being influenced of the best ways to achieve long-term growth. -

27322-ASI Investment Flyer BRO 0817.Indd

An asset manager for today’s global opportunities The coming together of Standard Life Investments and Aberdeen Asset Management under the Aberdeen Standard Investments brand will create the largest active investment manager in the UK* and one of the largest investment houses globally. Assets Investment managed Clients in More than managers in Client support in $718bn** 80 1,000 24 50 countries*** investment offices*** locations*** staff*** ** as of December 31, 2016, £/US$ rate: 1.2356 *** as of May 31, 2017 Source: Standard Life plc, Aberdeen Asset Management PLC “ The industry is changing; we have ensured we are well placed to meet our clients’ evolving needs and remain their trusted partner.” Martin Gilbert, Chief Executive, Standard Life Aberdeen plc * As of May 31, 2017, Source: Standard Life plc, Aberdeen Asset Management PLC An asset manager for today’s global opportunities Standard Life Investments was the investment On-the-ground expertise arm of Standard Life plc, a major UK listed Employing over 1,000 investment professionals, we can draw fi nancial services company which started life upon a breadth of investment talent. Our portfolio managers in 1825. Aberdeen Asset Management plc was are located across 24 offi ces, allowing us to be deeply rooted formed in 1983 via a management buyout and in every market in which we invest. Our uncompromising emphasis on conducting our own fi rst-hand research into has grown from a pioneer investor in Asian and companies and markets helps us fi nd opportunities at an emerging markets into a full-service, UK-listed early stage and screen out market noise. -

Fidelity Special Values Plc 31 August 2021

ret.en.xx.20210831.GB00BWXC7Y93.pdf FIDELITY INVESTMENT TRUSTS MONTHLY FACTSHEET FIDELITY SPECIAL VALUES PLC 31 AUGUST 2021 Investment Objective Portfolio Manager Commentary To achieve long term capital growth primarily through investment in UK equities recorded a seventh straight monthly gain in August. equities (and their related securities) of UK companies which the Sentiment remained buoyant, propelled by M&A activity, alongside Investment Manager believes to be undervalued or where the expectations for continued earnings strength. potential has not been recognised by the market It is encouraging to see the underlying stock picking coming through despite the recent underperformance of value stocks. This is partly down to the Trust benefiting from a number of M&A bids, Investment Trust Facts the latest being Meggitt, but is also a reflection of improving corporate fundamentals. Launch date: 17.11.94 Portfolio manager: Alex Wright, Jonathan Winton UK equities remain significantly undervalued compared to global 01.09.12, 03.02.20 markets, and reasonably valued in absolute terms on 13x 2022 Appointed to trust: estimates. While the UK market has looked cheap over the past Years at Fidelity: 20, 16 five years, the key differentiator in 2021 is that fundamentals on the Total Net Assets (TNA): £ 954m ground look very good. UK stocks are well positioned not only to Ordinary shares in Issue: 313,028,920 benefit from a recovery from the COVID pandemic, but also from Share price: 308.50p the lifting of the Brexit uncertainty. 304.79p NAV: We remain comfortable with how the portfolio looks from a Premium 1.22% valuations, returns on capital and risk perspective, and continue to Gross Market Gearing: 14.6% see meaningful upside potential for our holdings. -

FTSE Factsheet

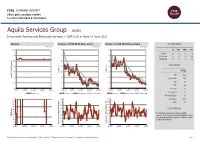

FTSE COMPANY REPORT Share price analysis relative to sector and index performance Aquila Services Group AQSG Investment Banking and Brokerage Services — GBP 0.26 at close 18 June 2021 Absolute Relative to FTSE UK All-Share Sector Relative to FTSE UK All-Share Index PERFORMANCE 18-Jun-2021 18-Jun-2021 18-Jun-2021 0.35 115 115 1D WTD MTD YTD Absolute 0.0 0.0 0.0 0.0 0.3 110 110 Rel.Sector 1.9 2.8 1.0 -2.0 Rel.Market 1.7 1.7 0.4 -8.2 0.25 105 105 VALUATION 0.2 100 100 Trailing 0.15 95 95 Relative Price Relative Price Relative PE 82.2 Absolute Price (local (local currency) AbsolutePrice 0.1 90 90 EV/EBITDA 38.4 0.05 85 85 PB 2.0 PCF +ve 0 80 80 Div Yield 1.1 Jun-2020 Sep-2020 Dec-2020 Mar-2021 Jun-2021 Jun-2020 Sep-2020 Dec-2020 Mar-2021 Jun-2021 Jun-2020 Sep-2020 Dec-2020 Mar-2021 Jun-2021 Price/Sales 1.3 Absolute Price Relative Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Net Debt/Equity 0.1 100 90 90 Div Payout 90.5 90 80 80 ROE 2.6 80 70 70 70 Index) Share Share Sector) Share - - 60 60 60 DESCRIPTION 50 50 50 40 The Company operates as a venture capital 40 40 RSI RSI (Absolute) 30 company. The Company provides financing for one or 30 30 more growing unquoted companies looking for capital 20 20 to expand the business. -

Capital Markets Day

Capital Markets Day Wootton Park and Chicheley Hall • 24 May 2018 bovishomesgroup.co.uk Capital Markets Day Welcome to Wootton Park Wootton Park is an attractive new Agenda for the day development in the pretty Bedfordshire 9:45am village of Wootton, less than 6 miles from Arrival on site, PPE and refreshments. the county town of Bedford and within Welcome and introductions, safety easy reach of busy Milton Keynes. briefing, divide into groups The vibrant village has a wide range of Site visit activities, sports and clubs for all ages, and 1. Site set up and management 2. Health and safety boasts a 14th century church, post office, 3. Phoenix Collection re-plan pharmacy, two convenience stores, pubs, a 4. Sales and marketing health centre, a library and local schools. 5. Sales specification Wootton Park offers a wide choice of 6. Show home brand new homes, each carefully designed 7. Build best practice to meet the needs of today’s lifestyles. 8. Build specification 12:30pm Depart site for Chicheley Hall, refreshments on arrival Presentation - Affordable Housing 1:20pm Buffet lunch 2:00pm Northampton A45 Presentations - A6 Business update A428 A4280 The Phoenix Collection A509 A422 Newport A1 Q&A Paynell Road Bedford M1 A603 3:30pm Wootton Bedford Road 15 Day ends - coach departs Chicheley Hall A421 14 for Bedford station Milton Keynes 13 A6 A421 4:11pm N A5 Train departs Bedford for London St Pancras 4:55pm Train arrives London St Pancras Fields Road 4 5 10 11 12 1 2 3 13 6 14 9 7 21 9 44 15 42 8 20 16 41 8 17 47 24 19 46 7 18 86 45 23 -

Challenging Road Ahead but Outlook Stable on Asset Manager Sector

Elizabeth Campbell Sean C. Tillman, CFA Asset Managers Have Stable Outlook Brian Estiz, CFA Jenny Panger, CFA With Risks Balanced For 2021 Nigel Greenwood Asset Manager Outlook 2021 January 15, 2021 Key Takeaways – Our outlook on both the traditional and alternative asset managers is stable. – We return to a stable outlook (from negative) on the traditional asset managers after two years that saw 19 negative rating actions, meaning negative outlook, or downgrade, out of 32 negative rating actions and 48 total rating actions. Alternative asset managers saw 10 negative rating actions while investment holding companies rounded out the difference. – We continue to believe that alternative asset managers are better positioned vis-à-vis their traditional peers. That said, we expect the traditional asset managers credit risk to be more balanced over 2021 as accommodative monetary and fiscal policy offsets some of the industry headwinds. Our current ratings incorporate these more balanced conditions and should result in a more equal distribution of upgrades and downgrades over the year. – Mergers and acquisitions (M&A) remain a focal point. 2020 saw a series of large acquisition announcements, both within the sector and involving banks and insurance companies. While the size of the deals may taper, we expect M&A to be a key strategy in the sector as firms reach for greater scale, capital, and capabilities. – In the U.S., which represents the largest pool of assets under management (AUM) and where the majority of ratings are based, S&P Global Economists expect a 4.2% U.S. real GDP rebound in 2021, after a 3.9% contraction in 2020. -

Booking Form Intercontinental London – the O2 Wednesday 24 November

BOOKING FORM INTERCONTINENTAL LONDON – THE O2 WEDNESDAY 24 NOVEMBER Housebuilder invites you to book your place at the ‘must attend event’ of the housebuilding year, the Housebuilder Awards. The Housebuilder Awards returns to the InterContinental London - The O2. The hotel stands out in the buzzing Greenwich Peninsula, enjoying spectacular Canary Wharf views and with the O2 arena just steps away. 18.45 – Drinks reception, Arora Foyer 19.30 – Dinner and Awards ceremony, East London Suite, Arora Ballroom 22.45 – Awards ceremony close followed by the after party 01.00 – Carriages The Housebuilder Awards is a black tie event. In partnership with Sponsored by: AWARDS 2021 FINALISTS BEST CUSTOMER BEST MARKETING BEST DESIGN FOR FOUR SATISFACTION INITIATIVE INITIATIVE STOREYS OR MORE Carriden Homes – Ribbonfield Catalyst & Focus – Time for a Barratt London – Nestlé Steadings place of your own apartments at Hayes Village, Hayfield – The Hayfield difference London Clixifix® – Customer care campaign Dandara – 1887 The Pantiles, simplified software Kingswood Homes – Shape your Tunbridge Wells Hill – Integration with Hill, home Places for People – 55 Degrees Yourkeys and pdCRM is the McCarthy Stone – Rebranding a North, Granton Waterfront, solution to lockdown sales well lived life Edinburgh Redrow – My Redrow, homeowner Taylor Wimpey – Not all rg+p – Magenta Court, Apsley support housebuilders are equal Telford Homes – Stone Studios, Taylor Wimpey – Customer service William Davis Homes – The time Hackney Wick hub is right Vistry Group – Vistry Partnerships’