Final Terms 06F48357-5Ae1-4569-A4d4

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

CHALLENGES to BUSINESS in the TWENTY-FIRST CENTURY Challenges to Business in the Twenty-First Century AM ERICAN ACADEMY of ARTS & SCIENCES

CHALLENGES TO BUSINESS IN THE TWENTY-FIRST CENTURY CHALLENGES TO BUSINESS IN THE TWENTY-FIRST Challenges to Business in the Twenty-First Century AM ERICAN ACADEMY OF ARTS & SCIENCES ERICAN ACADEMY OF ARTS Edited by Gerald Rosenfeld, Jay W. Lorsch, and Rakesh Khurana AMERICAN ACADEMY OF ARTS & SCIENCES AMERICAN ACADEMY OF ARTS & SCIENCES Challenges to Business in the Twenty-First Century Please direct inquiries to: American Academy of Arts and Sciences 136 Irving Street Cambridge, MA 02138-1996 Telephone: 617-576-5000 Fax: 617-576-5050 Email: [email protected] Web: www.amacad.org Challenges to Business in the Twenty-First Century Edited by Gerald Rosenfeld, Jay W. Lorsch, and Rakesh Khurana © 2011 by the American Academy of Arts and Sciences “Long-Term Financial Security” © 2011 by Roger W. Ferguson, Jr. “Challenges of Financial Innovation” © 2011 by Myron S. Scholes “Reversing the Null: Regulation, Deregulation, and the Power of Ideas” © 2011 by David A. Moss All rights reserved. Copies of this publication can be downloaded from: http://www.amacad.org/publications/Challenges.aspx. Suggested citation: Gerald Rosenfeld, Jay W. Lorsch, and Rakesh Khurana, eds., Challenges to Business in the Twenty-First Century (Cambridge, Mass.: American Academy of Arts and Sciences, 2011). Cover image © Adam Gault/Getty Images. ISBN#: 0-87724-089-2 The statements made and views expressed in this publication are solely the responsibility of the authors and are not necessarily those of the Officers and Fellows of the American Academy of Arts and Sciences. Contents 1 Introduction Gerald Rosenfeld and Leslie Cohen Berlowitz 3 Chapter 1 Long-Term Financial Security Roger W. -

A Primer on U.S. Stock Price Indices

A Primer on U.S. Stock Price Indices he measurement of the “average” price of common stocks is a matter of widespread interest. Investors want to know how “the Tmarket” is doing, and to be able to compare their returns with a meaningful benchmark. Money managers often have their compensation tied to performance, typically measured by comparing their results to a benchmark portfolio, so they and their clients are interested in the benchmark portfolio’s returns. And policymakers want to judge the potential for sudden adjustments in stock prices when differences from “fundamental value” emerge. The most widely quoted stock price index, the Dow Jones Industrial Average, has been supplemented by other popular indices that are constructed in a different way and pose fewer problems as a measure of stock prices. At present, a number of stock price indices are reported by the few companies that we will consider in this paper. Each of these indices is intended to be a benchmark portfolio for a different segment of the universe of common stocks. This paper discusses some of the issues in constructing and interpreting stock price indices. It focuses on the most widely used indices: the Dow Jones Industrial Average, the Stan- dard & Poor’s 500, the Russell 2000, the NASDAQ Composite, and the Wilshire 5000. The first section of this study addresses issues of construction and interpretation of stock price indices. The second section compares the movements of the five indices in the last two decades and investigates the Peter Fortune relationship between the returns on the reported indices and the return on “the market.” Our results suggest that the Dow Jones Industrial Average (Dow 30) The author is a Senior Economist and has inherent problems in its construction. -

Vanguard Total Stock Market Index Fund

Fact sheet | June 30, 2021 Vanguard® Vanguard Total Stock Market Index Fund Domestic stock fund | Institutional Shares Fund facts Risk level Total net Expense ratio Ticker Turnover Inception Fund Low High assets as of 04/29/21 symbol rate date number 1 2 3 4 5 $227,984 MM 0.03% VITSX 8.0% 07/07/97 0855 Investment objective Benchmark Vanguard Total Stock Market Index Fund seeks Spliced Total Stock Market Index to track the performance of a benchmark index that measures the investment return of the Growth of a $10,000 investment : January 31, 2011—D ecember 31, 2020 overall stock market. $35,603 Investment strategy Fund as of 12/31/20 The fund employs an indexing investment $35,628 approach designed to track the performance of Benchmark the CRSP US Total Market Index, which as of 12/31/20 represents approximately 100% of the 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 investable U.S. stock market and includes large-, mid-, small-, and micro-cap stocks regularly traded on the New York Stock Exchange and Annual returns Nasdaq. The fund invests by sampling the index, meaning that it holds a broadly diversified collection of securities that, in the aggregate, approximates the full Index in terms of key characteristics. These key characteristics include industry weightings and market capitalization, as well as certain financial measures, such as Annual returns 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 price/earnings ratio and dividend yield. Fund 1.09 16.42 33.49 12.56 0.42 12.67 21.17 -5.16 30.81 21.00 For the most up-to-date fund data, Benchmark 1.08 16.44 33.51 12.58 0.40 12.68 21.19 -5.17 30.84 20.99 please scan the QR code below. -

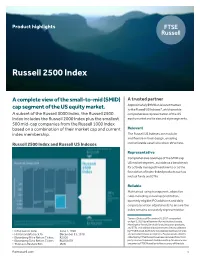

Russell 2500 Index

Product highlights Russell 2500 Index A complete view of the small-to-mid (SMID) A trusted partner Approximately $9 trillion is benchmarked cap segment of the US equity market. to the Russell US Indexes*, which provide A subset of the Russell 3000 Index, the Russell 2500 comprehensive representation of the US Index includes the Russell 2000 Index plus the smallest equity market and its size and style segments. 500 mid-cap companies from the Russell 1000 Index based on a combination of their market cap and current Relevant index membership. The Russell US Indexes are modular and flexible in their design, enabling Russell 2500 Index and Russell US Indexes customizable asset allocation structure. Representative Comprehensive coverage of the SMID cap US market segment, suitable as a benchmark for actively managed investments or as the foundation of index-linked products such as mutual funds and ETFs. Reliable Maintained using transparent, objective rules including annual reconstitution, quarterly eligible IPO additions and daily corporate action adjustments to ensure the index remains accurately representative. *Source: Data as of December 31, 2017 as reported on April 2, 2018 by eVestment for institutional assets, Morningstar for retail mutual funds, insurance products, and ETFs, and additional passive assets directly collected • Initial launch date: June 1, 1990 by FTSE Russell. AUM data includes blended benchmarks • Historical data back to: December 31, 1978 and excludes futures and options. Passive assets directly • Bloomberg Price Return Ticker: R2500 collected by FTSE Russell have been removed from third • Bloomberg Total Return Ticker: RU25INTR party sources to prevent double counting. No assurances • Thomson Reuters RIC: .R25I are given by FTSE Russell as to the accuracy of the data. -

No. 2 Newsmaker of 2016 Was City Manager Change Rodgers Christmas Basket Fund Are Still Being Accepted

FRIDAY 162nd YEAR • No. 208 DECEMBER 30, 2016 CLEVELAND, TN 22 PAGES • 50¢ Basket Fund Donations to the William Hall No. 2 Newsmaker of 2016 was city manager change Rodgers Christmas Basket Fund are still being accepted. Each By LARRY C. BOWERS Service informed Council members of year, the fund supplies boxes of Banner Staff Writer the search process they faced. food staples to needy families TOP 10 MTAS provided assistance free of during the holiday season. The The Cleveland City Council started charge, and Norris recommended the fund, which is a 501(c)(3) charity, the 2016 calendar year with a huge city hire a consultant. This was prior is a volunteer-suppported effort. challenge — an ordeal which devel- NEWSMAKERS to the Council’s decision to hire Any funds over what is needed to oped into the No. 2 news story of the Wallace, who had also assisted with pay for food bought this year will year as voted by Cleveland Daily the city’s hiring of Police Chief Mark be used next Christmas. Banner staff writers and editors — The huge field of applicants was Gibson. Donations may be mailed to First when the city celebrated the retire- vetted by city consultant and former Council explored the possibility of Tennessee Bank, P.O. Box 3566, ment of City Manager Janice Casteel Tennessee Bureau of Investigation using MTAS and a recruiting agency, Cleveland TN 37320-3566 or and announced the hiring of new City Director Larry Wallace, of Athens, as but Norris told them she had never dropped off at First Tennessee Manager Joe Fivas. -

Financial Market Data for R/Rmetrics

Financial Market Data for R/Rmetrics Diethelm Würtz Andrew Ellis Yohan Chalabi Rmetrics Association & Finance Online R/Rmetrics eBook Series R/Rmetrics eBooks is a series of electronic books and user guides aimed at students and practitioner who use R/Rmetrics to analyze financial markets. A Discussion of Time Series Objects for R in Finance (2009) Diethelm Würtz, Yohan Chalabi, Andrew Ellis R/Rmetrics Meielisalp 2009 Proceedings of the Meielisalp Workshop 2011 Editor Diethelm Würtz Basic R for Finance (2010), Diethelm Würtz, Yohan Chalabi, Longhow Lam, Andrew Ellis Chronological Objects with Rmetrics (2010), Diethelm Würtz, Yohan Chalabi, Andrew Ellis Portfolio Optimization with R/Rmetrics (2010), Diethelm Würtz, William Chen, Yohan Chalabi, Andrew Ellis Financial Market Data for R/Rmetrics (2010) Diethelm W?rtz, Andrew Ellis, Yohan Chalabi Indian Financial Market Data for R/Rmetrics (2010) Diethelm Würtz, Mahendra Mehta, Andrew Ellis, Yohan Chalabi Asian Option Pricing with R/Rmetrics (2010) Diethelm Würtz R/Rmetrics Singapore 2010 Proceedings of the Singapore Workshop 2010 Editors Diethelm Würtz, Mahendra Mehta, David Scott, Juri Hinz R/Rmetrics Meielisalp 2011 Proceedings of the Meielisalp Summer School and Workshop 2011 Editor Diethelm Würtz III tinn-R Editor (2010) José Cláudio Faria, Philippe Grosjean, Enio Galinkin Jelihovschi and Ri- cardo Pietrobon R/Rmetrics Meielisalp 2011 Proceedings of the Meielisalp Summer Scholl and Workshop 2011 Editor Diethelm Würtz R/Rmetrics Meielisalp 2012 Proceedings of the Meielisalp Summer Scholl and Workshop 2012 Editor Diethelm Würtz Topics in Empirical Finance with R and Rmetrics (2013), Patrick Hénaff FINANCIAL MARKET DATA FOR R/RMETRICS DIETHELM WÜRTZ ANDREW ELLIS YOHAN CHALABI RMETRICS ASSOCIATION &FINANCE ONLINE Series Editors: Prof. -

Ready Coller Institute of Venture, • Sources of IP – We Will Awash with Cash

ISSUE 1a — 2014 WELCOME ISSUE $45 THE VENTURE ECOSYSTEM FRAMEWORK: MESSY, FAST, AND GLOBAL 企业生态系统框架: 凌 乱 、快 速 、全 球 化 Trends Shaping the Venture Ecosystem in 2014 / 06 IS THE VC MODEL ‘BROKEN’? 风险投资模式“破损”了吗? VC Success Definition and Understanding Who Wins and Who Loses / 20 MEASURING SCIENCE PARKS' PERFORMANCE 度量科技园区的业绩 TusPark, Imperial West, and 15 other Parks / 28 time to Impact THE PUBLIC VENTURE POLICY MENU A toolbox of PrOVEN 企业公共政策清单 Policies Public Authorities government policies /36 Can Take / 36 EDITORIAL BOARD Jeremy Coller Eli Talmor Contents Moshe Zviran Yesha Sivan (Editor-in-Chief) Robyn Klingler-Vidra (Associate Editor) COLLER INSTITUTE OF VENTURE 36 Yù (Zöe) Zhái Itai Asaf Odeya Pergament 04 Ann Iveson COPYRIGHT © Coller Institute of Venture at Tel Aviv University 2014 www.collerinstituteofventure.org 05 06 20 28 WHAT IS THE COLLER INSTITUTE MEASURING SCIENCE PARKS' OF VENTURE?—04 PERFORMANCE—28 TusPark, Imperial West, RESEARCH IS AT THE CORE and 15 other Parks OF THE CIV’S VISION—05 How they are designed and managed to T HE VENTURE ECOSYSTEM achieve optimal performance FRAMEWORK: MESSY, FAST, AND GLOBAL—06 Six Trends Shaping the THE PUBLIC VENTURE Venture Ecosystem in 2014 POLICY MENU—36 44 Policies Public Authorities This article presents a generative Can Take framework for the venture ecosystem and highlights the current trends Public policymakers’ tools for fostering affecting the ecosystem local venture ecosystems I S THE VC MODEL ‘BROKEN’?—20 NEWS IN BRIEF—44 VC Success Definition and The News section offers a selection -

Final Report Amending ITS on Main Indices and Recognised Exchanges

Final Report Amendment to Commission Implementing Regulation (EU) 2016/1646 11 December 2019 | ESMA70-156-1535 Table of Contents 1 Executive Summary ....................................................................................................... 4 2 Introduction .................................................................................................................... 5 3 Main indices ................................................................................................................... 6 3.1 General approach ................................................................................................... 6 3.2 Analysis ................................................................................................................... 7 3.3 Conclusions............................................................................................................. 8 4 Recognised exchanges .................................................................................................. 9 4.1 General approach ................................................................................................... 9 4.2 Conclusions............................................................................................................. 9 4.2.1 Treatment of third-country exchanges .............................................................. 9 4.2.2 Impact of Brexit ...............................................................................................10 5 Annexes ........................................................................................................................12 -

Equity Indexes: Broadly Diversified Or Concentrated and Risky?

Equity Indexes: Broadly Diversified or Concentrated and Risky? OCTOBER 2020 David Hintz, CFA Portfolio Manager, U.S. Large Cap Equities Ethan Kiliany Research Analyst, U.S. Equities Snapshot Most investors, even those based outside the U.S., are quite familiar with › Many equity indexes, such as the popular the S&P 500 Index. The index represents 500 of the largest U.S. companies S&P 500 Index, are often considered and is often used as a model for popular passive mutual funds that seek to broadly diversified because they hold a mirror its performance. One of the reasons that it is often used as a model large number of securities. by passive investors is its perceived diversification. After all, how can an index with 500 stocks not be diversified? Of course, if that’s not diversified › Today 25% of that index is concentrated enough, investors can easily find indexes that include more U.S. companies. in just the five largest stocks by market The Russell 1000 Index represents about 1,000 U.S. large and mid-cap capitalization—and it is not the only stocks. Or there is the Russell 3000 Index which adds another 2,000 U.S. top-heavy equity index. small companies to that list and represents about 98% of the investible U.S. › The significant outperformance of the five equity market. Many investors, including SEI, believe it’s prudent to diversify largest stocks has led to investors falling equity holdings globally. Here, investors may look at the MSCI ACWI Index, into the recency bias trap—believing what which contains more than 3,000 constituents from 23 developed and 26 has happened recently is likely to continue emerging markets. -

Ishares Russell 1000 Large-Cap Index Fund Fact Sheet

iShares Russell 1000 Large-Cap BRGKX Index Fund As of 06/30/2021 | Class K: BRGKX | Institutional: BRGNX | Investor A: BRGAX INVESTMENT STRATEGY Invests in a portfolio of assets whose performance seeks to match the performance of the Russell 1000® Index. Rated against 1,257 Large Blend Funds, as of 06/30/2021 based on risk adjusted total return. Overall Ratings are determined monthly and subject to change. The Overall Morningstar Rating for a fund is derived from a weighted average of the performance figures associated with its 3-, 5- and 10-year (if applicable) Morningstar Rating metrics.†† ANNUALIZED PERFORMANCE KEY FACTS Without Sales Charge 1 Year 3 Year 5 Year 10 Year Size of Fund (Millions) $682.3M Class K 42.95 19.06 17.89 14.78 Fund Launch Date 03/31/2011 Benchmark 43.07 19.16 17.99 14.90 Share Class Launch Date 03/31/2011 Morningstar Average 40.47 16.77 16.15 13.21 Morningstar Category Large Blend Number Of Holdings 1,024 CALENDAR YEAR PERFORMANCE Benchmark Russell 1000 Index Without Sales Charge 2016 2017 2018 2019 2020 YTD 2Q2021 ANNUAL EXPENSES Class K 11.92 21.60 -4.85 31.28 20.84 14.92 8.50 Gross Expense Ratio 0.08% Benchmark 12.05 21.69 -4.78 31.43 20.96 14.95 8.54 Net Expense Ratio 0.08% Morningstar Average 10.37 20.44 -6.27 28.78 15.83 14.84 7.55 The Net Expense Ratio excluding Investment Performance data shown represents past performance which is no guarantee of future results. -

Mr. Alp Eroglu International Organization of Securities Commissions (IOSCO) Calle Oquendo 12 28006 Madrid Spain

1301 Second Avenue tel 206-505-7877 www.russell.com Seattle, WA 98101 fax 206-505-3495 toll-free 800-426-7969 Mr. Alp Eroglu International Organization of Securities Commissions (IOSCO) Calle Oquendo 12 28006 Madrid Spain RE: IOSCO FINANCIAL BENCHMARKS CONSULTATION REPORT Dear Mr. Eroglu: Frank Russell Company (d/b/a “Russell Investments” or “Russell”) fully supports IOSCO’s principles and goals outlined in the Financial Benchmarks Consultation Report (the “Report”), although Russell respectfully suggests several alternative approaches in its response below that Russell believes will better achieve those goals, strengthen markets and protect investors without unduly burdening index providers. Russell is continuously raising the industry standard for index construction and methodology. The Report’s goals accord with Russell’s bedrock principles: • Index providers’ design standards must be objective and sound; • Indices must provide a faithful and unbiased barometer of the market they represent; • Index methodologies should be transparent and readily available free of charge; • Index providers’ operations should be governed by an appropriate governance structure; and • Index providers’ internal controls should promote efficient and sound index operations. These are all principles deeply ingrained in Russell’s heritage, practiced daily and they guide Russell as the premier provider of indices and multi-asset solutions. Russell is a leader in constructing and maintaining securities indices and is the publisher of the Russell Indexes. Russell operates through subsidiaries worldwide and is a subsidiary of The Northwestern Mutual Life Insurance Company. The Russell Indexes are constructed to provide a comprehensive and unbiased barometer of the market segment they represent. All of the Russell Indexes are reconstituted periodically, but not less frequently than annually or more frequently than monthly, to ensure new and growing equities and fixed income securities are reflected in its indices. -

Brexit Shadow Across EU

Stocks DOW NASDAQ S&P 500 10-YR T-NOTE 30-YR T-BOND CRUDE OIL GOLD EURO p 25,063.89 +64.22 q 7,263.87 -17.87 p 2,706.53 +2.43 p 2.69% +.06 p 3.03% +.03 p $55.26 +1.47 q $1,316.90 -2.80 p $1.1461 +.0017 Spotlight on Mickey Downshifting in Detroit Buy now, pay later DIS $111.30 Consumer credit $120 Walt Disney serves up its latest General Motors struggled The Federal Reserve seasonally adjusted change quarterly report card Tuesday. $108.67 through much of 2018, largely issues its monthly tally of 25.0 $25 billion Wall Street expects the 105 due to declining sales in the U.S. consumer borrowing 22.2 entertainment giant will report U.S. and China. Thursday. 21.0 20 est. that its fiscal first-quarter earn- ’18 In November, the automak- The tally, which excludes 90 15.1 16.0 ings and revenue declined er launched a restructuring mortgages and other loans 15 from a year earlier. Beyond its plan that called for the elimina- secured by real estate, is Operating $1.89 est. October-December results, $1.55 tion of five North American expected to show consumer 10 9.6 eek Ahead EPS investors will be keen for an Q1 ’18 Q1 ’19 factories and 14,000 jobs. In- borrowing increased by update on the company’s plans vestors will be listening for an $16 billion in December, 5 Price-earnings ratio: 13 to roll out video streaming ser- update on how the strategy is below November’s $22.2 0 The W based on past 12-month results vices and its acquisition of 21st working on Wednesday, when billion gain.