Julie Miloud Kaddar Vaccine 2

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Trends in Vaccine Development

ADVERTISEMENT FEATURE NATUREJOBS SPOTLIGHT ON VACCINES Trends in vaccine development How are public-private partnerships, low-cost manufacturers and new technology afecting the vaccine field? “The vaccine field BILL GATES is a handy person to grow over the next few years. the virus was identifed in 1984, to have in your corner, which In the United States, demand researchers were optimistic they is going to enlarge bodes well for those committed to will increase by around 7 percent could formulate a vaccine quickly. vaccine research. In January 2010 annually until 2015, according to a As HIV proved resilient, hopes for substantially beyond the philanthropist called for a 2011 report published by industry a fast response faded and by the SPOTLIGHT ON IMMUNOLOGY / VACCINES ON IMMUNOLOGY SPOTLIGHT “decade of vaccines” and pledged analysts Freedonia. “It’s probably early 1990s several research groups the traditional US$10 billion for vaccine research the best growth area right now in and companies had abandoned and development (R&D) and infectious disease,” says Steve Projan, the search for a vaccine. preventive vaccine.” distribution. Te Bill & Melinda senior vice president of R&D in It became clear that a new Gates Foundation funding will the innovative medicines unit at model of vaccine development was Rafi Ahmed, Emory Vaccine Center boost an already burgeoning feld. vaccine manufacturer MedImmune. needed, one that could bridge the Although vaccines comprise Te industry is being shaped by gap between the public and private a small portion of the global increased collaboration between the sectors and focus on the developing pharmaceutical market — 2 percent public and private sectors, the rise world. -

Welcome NOTE President

2015 welcome NOTE from the president EXECUTIVE COMMITEE MEMBERS Mr. Mahendra Suhardono President Bio Farma, Indonesia Mr. Rajender Kumar Suri Dr. Akira Homma Vice President Treasurer Panacea Biotech Limited, India Bio-Manguinhos (Fiocruz),Brazil Mr. Rayasam Prasad Ms. Meng Li Mr. Patrick Tippoo Biological E. Limited, India China National Biotec Group Co.Ltd., China The Biovac Institute, South Africa Mr. Juliman Dr. Steven Gao Mr. Adar Poonawalla GAVI Board Alternate Xiamen Innovax Biotech Co. Ltd., China GAVI Board Representative Bio Farma, Indonesia Serum Institute of India Ltd., India Member Organizations’ Geographical Presence Argentina Bangladesh Brazil Cuba Egypt India Indonesia IR of Iran Mexico P.R. China Republic of Korea Saudi Arabia South Africa Taiwan Thailand Vietnam Name of the company : Arab Company for Pharmaceutical Products (Arabio) Head of Institution : Dr. Majed Saeed Bahatheq (Arabio CEO) Established : Arabio is a limited liability company established in 2005 Location : Saudi Arabia Overview of the company Arabio is a biopharmaceutical company specialized in human vaccines, and other biopharmaceuticals. It is the first biopharmaceutical company in the Gulf Cooperation Council (GCC). The size and scope of activities intended to be made in Arabio would make Arabio the first biological company of its kind in the Middle East. Arabio aims to bring to the markets of the Middle East, North Africa, and high quality products that comply with the international quality standards. Arabio has production lines of pre-filled syringes, liquid vials and lyophilized vials from the best global machines suppliers to make high quality products and meet cGMP & international standards. Description of ARABIO capabilities – Biological sterile manufacturing – PFS and vial filling – PFS and vial blister packaging Arabio Partners: 1. -

PDF: 300 Pages, 5.2 MB

The Bay Area Council Economic Institute wishes to thank the sponsors of this report, whose support was critical to its production: The Economic Institute also wishes to acknowledge the valuable project support provided in India by: The Bay Area Council Economic Institute wishes to thank the sponsors of this report, whose support was critical to its production: The Economic Institute also wishes to acknowledge the valuable project support provided in India by: Global Reach Emerging Ties Between the San Francisco Bay Area and India A Bay Area Council Economic Institute Report by R. Sean Randolph President & CEO Bay Area Council Economic Institute and Niels Erich Global Business/Transportation Consulting November 2009 Bay Area Council Economic Institute 201 California Street, Suite 1450 San Francisco, CA 94111 (415) 981-7117 (415) 981-6408 Fax [email protected] www.bayareaeconomy.org Rangoli Designs Note The geometric drawings used in the pages of this report, as decorations at the beginnings of paragraphs and repeated in side panels, are grayscale examples of rangoli, an Indian folk art. Traditional rangoli designs are often created on the ground in front of the entrances to homes, using finely ground powders in vivid colors. This ancient art form is believed to have originated from the Indian state of Maharashtra, and it is known by different names, such as kolam or aripana, in other states. Rangoli de- signs are considered to be symbols of good luck and welcome, and are created, usually by women, for special occasions such as festivals (espe- cially Diwali), marriages, and birth ceremonies. Cover Note The cover photo collage depicts the view through a “doorway” defined by the section of a carved doorframe from a Hindu temple that appears on the left. -

Panacea Biotec Receives $24.32M Award from UN Agencies

Panacea Biotec receives $24.32M award from UN Agencies 23 December 2019 | News | By Manbeena Chawla Easyfive-TT (DTwP-HepB-Hib) was introduced by Panacea Biotec as world’s first fully liquid wP-based pentavalent vaccine in Indian market in 2005. New Delhi based biotechnology company Panacea Biotec has received Awards worth USD 24.32 Million (Over Rs.170 crores) from U.N. Agencies (UNICEF and PAHO) for supply of its Easyfive-TT, a fully liquid WHO prequalified Pentavalent Vaccine. UNICEF award is for year 2020 and award of PAHO is for three (3) years i.e. 2020-2022. Pediatric vaccination plays an important role to achieve Sustainable Development Goals set by the United Nations, in particular the target to reduce under-five mortality rate to less than 25 per 1000 live births. Pentavalent vaccine protects children against five deadly diseases; Diphtheria, Tetanus, Pertussis, Hepatitis B and invasive infections caused by Haemophilus Influenza Type b – becoming the foundation of paediatric immunization programs across the world. Easyfive-TT (DTwP-HepB-Hib) was introduced by Panacea Biotec as world’s first fully liquid wP-based pentavalent vaccine in Indian market in 2005. With WHO prequalification in 2008, over 100 million doses have been supplied to more than 50 countries globally. Easyfive-TT is ready for use without further preparation by healthcare workers in the field, which offers major healthcare advantages in countries with challenging infrastructure and hygiene problems. Panacea Biotec has contributed significantly for Children’s Health and has partnered with WHO, UNICEF & PAHO in their efforts to maximize coverage of vaccines under the Expanded Program on Immunization (EPI) in developing countries. -

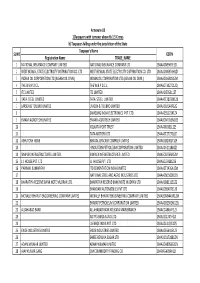

Manufacturing Permission of Human Vaccines Year 2021

Manufacturing Permission of Human Vaccines Year 2021 S. No. Name of Firm Name of Molecule Indication Date Approved 1 M/s Serum Institute ChAdOx1 nCoV-19 For Restricted use in emergency Permission No. of India Pvt. Ltd. Corona Virus Vaccine situation: MF/BIO/21/000001 dated 212/2, Off. Soli (Recombinant) For active immunization of 03.01.2021 Poonawalla Road, individuals of ≥18 years old for the Hadapsar Pune, prevention of corona virus disease Maharashtra, India. (COVID-19) when administered in two doses schedule. The second dose should be administered between 4 to 6 weeks after the first dose. However, there is data available for administration of the second dose up to 12 weeks after the first dose from the overseas studies. 2 M/s Bharat Biotech Whole Virion Inactivated For Restricted use in emergency Permission No. International Corona Virus Vaccine, situation in clinical trial mode: MF/BIO/21/000002 dated Limited, Sy. No. [BBV152] For active immunization against 03.01.2021 230, 231 & 235, Corona Virus Disease (COVID-19) Genome Valley, for age ≥12 years when Shameerpet administered in two doses interval Mandal, Medchal- of day 0 & day 28. Malkajgiri District, Telangana-500078, India. Manufacturing Permission of Human Vaccines Year 2020 S. No. Name of Firm Name of Molecule Indication Date Approved 1 M/s Biological E. Typhoid Vi Conjugate For active immunization against MF/BIO/20/000001 dated Limited, Plot No. 1, Vaccine, IP infection caused by Salmonella 28.01.2020 Phase II, Biotech typhi in infants, children, Park, Kolthur adolescents and adults aged ≥ 6 Village, Shameerpet months to ≤ 45 years. -

Annual Report 17-18 Initial Pages for Web.Cdr

Contents Safe Harbour Statement Corporate Information 01 This report contains forward-looking statements, which may be identied by their use of words like Tribute to Late Shri Ravinder Jain 02 ‘plans’, ‘expects’, ‘will’, ‘anticipates’, ‘believes’, Vision, Mission & Values 03 ‘intends’, ‘projects’, ‘estimates’, or other words of similar meaning. All statements that address Chairman's Message 04 expectations or projections about the future, Panacea Biotec at a Glance 06 including but not limited to statements about Company’s future growth drivers, product Financial Highlights 07 development, market position and expenditures Core Strengths 08 are forward looking statements. Forward looking statements are based on certain assumptions and Management Discussion & Analysis 10 expectations for future events. The Company may Directors' Report 25 not guarantee that these assumptions and expectations are accurate and will be realised. The Corporate Governance Report 49 Company’s actual results, performance or Auditors' Report on Standalone achievements could thus differ materially from Financial Statements 66 those projected in any forward-looking Standalone Financial Statements 72 s t ate m e nt s. Th e Co m p a ny a s s u m e s n o responsibility to publicly amend, modify, revise Auditors' Report on Consolidated any forward-looking statements, on the basis of Financial Statements 106 any subsequent developments, information and Consolidated Financial Statements 110 events. Mr. Soshil Kumar Jain, Chairman (Sitting) along with his colleagues on the Board and other officials (from left) Mr. Mahipat Singh, Mr. Vinod Goel, Mr. N. N. Khamitkar, Mr. O. P. Kelkar, Mr. Mukul Gupta, Mr. K. M. Lal, Dr. -

Panacea Biotec Limited (CIN: L33117PB1984PLC022350) Regd

Panacea Biotec Limited (CIN: L33117PB1984PLC022350) Regd. Office: Ambala - Chandigarh Highway, Lalru - 140 501, Punjab, India Corp. Office: B-1 Extn./G-3, Mohan Co-operative Indl. Estate, Mathura Road, New Delhi - 110 044, India Website: www.panaceabiotec.com E-mail: [email protected] Tel: +91 11 41679000 Fax: +91 11 41679070 NOTICE OF EXTRAORDINARY GENERAL MEETING NOTICE is hereby given that an Extraordinary General Meeting of the Members of Panacea Biotec Limited (“the Company”) will be held on Friday, June 25, 2021 at 11:30 A.M. through Video Conferencing (“VC”) / Other Audio-Visual Means (“OAVM”), to transact the following businesses: SPECIAL BUSINESS: 1. Raising of funds by way of issue of equity shares and / or other securities To consider and, if thought fit, to pass the following resolution, as a Special Resolution: “RESOLVED THAT pursuant to the provisions of Sections 23, 42, 62(1)(c) and all other applicable provisions, if any, of the Companies Act, 2013 read with the rules made thereunder including the Companies (Prospectus and Allotment of Securities) Rules, 2014 and the Companies (Share Capital and Debentures) Rules, 2014, (including any amendment(s), statutory modification(s) or re-enactment(s) thereof, for the time being in force) (“Act”), in accordance with the provisions of the Memorandum and Articles of Association of the Company and pursuant to the applicable provisions of the Securities and Exchange Board of India (Listing Obligations and Disclosure Requirements) Regulations, 2015, as amended (“SEBI LODR -

Panacea Biotec Partners with GAVI

Panacea Biotec partners with GAVI 11 July 2011 | News Image not found or type unknown New Delhi-based Panacea Biotec became the first company in the world to introduce a fully liquid pentavalent vaccine, EasyFive, in the year 2005. Panacea has pledged its support to the cause of GAVI alliance by deciding to reduce the cost of EasyFive to the tune of 10 to 15 percent in coming years. This effort would increase the access of vaccines to millions of children. After introduction of EasyFive in developing countries in the year 2008, the price of pentavalent vaccines have decreased by 18 percent in 2010. The new vaccine price reductions are expected to help in the donor support for GAVI & contribute towards reducing GAVI's funding challenge. Launched in 2000, the GAVI Alliance is a global health partnership representing stakeholders in immunization from both private and public sectors, developing world and donor governments, private sector philanthropists such as the Bill & Melinda Gates Foundation, the financial community, developed and developing country vaccine manufacturers, research and technical institutes, civil society organizations and multilateral organizations like the World Health Organization (WHO), the United Nations Children's Fund (UNICEF) and the World Bank. The combined demand of all pediatric vaccines worldwide is estimated to grow up toImage 7,200 not found crore or by type 2012. unknown The pentavalent vaccine market is estimated to cross a mark ofImage 4,500 not foundcrore, or outtype ofunknown which UN agencies are likely to procure vaccines worth more than Image1,912 not crorefound orby type the unknown end of 2011. -

List of Participants

LIST OF PARTICIPANTS AT THE 11th ANNUAL GENERAL MEETING & CONFERENCE OF THE DEVELOPING COUNTRIES VACCINE MANUFACTURERS NETWORK ON 13 – 16 SEPTEMBER 2010, AT NOVOTEL CONVENTION CENTER, HYDERABAD, ANDHRA PRADESH, INDIA. MEMBERS OF THE DCVMN: Organization S.No. Name of the Member Organization No. 1 1 Dr. Ella, Krishna, M Bharat Biotech International Limited, Chairman & Managing Director Genome Valley, Shameerpet (M), Hyderabad, Andhra Pradesh, India. 500 078 2 Dr. Krishna Mohan, V Bharat Biotech International Limited President Genome Valley, Shameerpet (M), Hyderabad, Andhra Pradesh, India. 500 078 3 Mr. Prasad, Sai D. Bharat Biotech International Limited, Vice President Genome Valley, Shameerpet (M), Hyderabad, Andhra Pradesh, India. 500 078 4 Dr. Harshavardhan, G.V.J.A Bharat Biotech International Limited, Director - Rotavirus Vaccine Genome Valley, Shameerpet (M), Development Project Hyderabad, Andhra Pradesh, India. 500 078 5 Dr. Srinivas, V.K Bharat Biotech International Limited, Vice President Genome Valley, Shameerpet (M), Hyderabad, Andhra Pradesh, India. 500 078 6 Dr. Kamaraj, G Bharat Biotech International Limited, General Manager: Production Genome Valley, Shameerpet (M), Hyderabad, Andhra Pradesh, India. 500 078 7 Mr. Gopinathan, K Bharat Biotech International Limited, Assistant General Genome Valley, Shameerpet (M), Manager, Quality Control. Hyderabad, Andhra Pradesh, India. 500 078 8 Mr. Venkatesan, R Bharat Biotech International Limited, Assistant General Manager, Genome Valley, Shameerpet (M), Production. Hyderabad, Andhra Pradesh, India. 500 078 2 9 Ms. Datla, Mahima Biological E. Limited, Sr. Vice President 18/1&3, Azamabad, Hyderabad, India. 500 020 10 Mr. Mantena, Narender Dev Biological E. Limited, Sr. Vice President – SBD 18/1&3, Azamabad, Hyderabad, India. 500 020 11 Mr. -

Health Technology Innovation by Indigenous Enterprises in China, India and Brazil

Health Technology Innovation by Indigenous Enterprises in China, India and Brazil by Abdolrahim Rezaie A thesis submitted in conformity with the requirements for the degree of Doctor of Philosophy Institute of Medical Science University of Toronto © Copyright by Abdolrahim Rezaie, 2011 Health Technology Innovation by Indigenous Enterprises in China, India and Brazil Abdolrahim Rezaie Doctor of Philosophy Institute of Medical Science University of Toronto 2011 Abstract This thesis explores health technology innovation within indigenous enterprises in China, India, and Brazil. The main discussions are presented in five papers/manuscripts. The first is a case study of Brazil’s health biotechnology sector. It concludes that systemic tensions between the country’s public and private sectors may be detracting from its overall innovative success. The second paper gauges vaccine and medicinal innovation within enterprises in the stated countries by analyzing new technologies in their pipelines or on the market. It concludes that that a growing number of health enterprises in these countries are tackling more technologically challenging and costly innovations. The third paper explores how national institutions and industry globalization interact to shape commitments to new drug and vaccine innovations by enterprises in the three countries. It concludes that; a) the introduction of pharmaceutical product patent regimes has had a modest impact on entrepreneurial attempts to develop new technologies, b) key challenges that diminish patent incentives tend to be institutional in nature and, c) the increasingly globalized nature of health product innovation limits what countries can achieve independently. ii The fourth paper analyzes key issues and trends in health biotechnology firms’ transition to innovation in China, India, Brazil, and South Africa. -

FINAL DISTRIBUTION.Xlsx

Annexure-1B 1)Taxpayers with turnover above Rs 1.5 Crores b) Taxpayers falling under the jurisdiction of the State Taxpayer's Name SL NO GSTIN Registration Name TRADE_NAME 1 NATIONAL INSURANCE COMPANY LIMITED NATIONAL INSURANCE COMPANY LTD 19AAACN9967E1Z0 2 WEST BENGAL STATE ELECTRICITY DISTRIBUTION CO. LTD WEST BENGAL STATE ELECTRICITY DISTRIBUTION CO. LTD 19AAACW6953H1ZX 3 INDIAN OIL CORPORATION LTD.(ASSAM OIL DIVN.) INDIAN OIL CORPORATION LTD.(ASSAM OIL DIVN.) 19AAACI1681G1ZM 4 THE W.B.P.D.C.L. THE W.B.P.D.C.L. 19AABCT3027C1ZQ 5 ITC LIMITED ITC LIMITED 19AAACI5950L1Z7 6 TATA STEEL LIMITED TATA STEEL LIMITED 19AAACT2803M1Z8 7 LARSEN & TOUBRO LIMITED LARSEN & TOUBRO LIMITED 19AAACL0140P1ZG 8 SAMSUNG INDIA ELECTRONICS PVT. LTD. 19AAACS5123K1ZA 9 EMAMI AGROTECH LIMITED EMAMI AGROTECH LIMITED 19AABCN7953M1ZS 10 KOLKATA PORT TRUST 19AAAJK0361L1Z3 11 TATA MOTORS LTD 19AAACT2727Q1ZT 12 ASHUTOSH BOSE BENGAL CRACKER COMPLEX LIMITED 19AAGCB2001F1Z9 13 HINDUSTAN PETROLEUM CORPORATION LIMITED. 19AAACH1118B1Z9 14 SIMPLEX INFRASTRUCTURES LIMITED. SIMPLEX INFRASTRUCTURES LIMITED. 19AAECS0765R1ZM 15 J.J. HOUSE PVT. LTD J.J. HOUSE PVT. LTD 19AABCJ5928J2Z6 16 PARIMAL KUMAR RAY ITD CEMENTATION INDIA LIMITED 19AAACT1426A1ZW 17 NATIONAL STEEL AND AGRO INDUSTRIES LTD 19AAACN1500B1Z9 18 BHARATIYA RESERVE BANK NOTE MUDRAN LTD. BHARATIYA RESERVE BANK NOTE MUDRAN LTD. 19AAACB8111E1Z2 19 BHANDARI AUTOMOBILES PVT LTD 19AABCB5407E1Z0 20 MCNALLY BHARAT ENGGINEERING COMPANY LIMITED MCNALLY BHARAT ENGGINEERING COMPANY LIMITED 19AABCM9443R1ZM 21 BHARAT PETROLEUM CORPORATION LIMITED 19AAACB2902M1ZQ 22 ALLAHABAD BANK ALLAHABAD BANK KOLKATA MAIN BRANCH 19AACCA8464F1ZJ 23 ADITYA BIRLA NUVO LTD. 19AAACI1747H1ZL 24 LAFARGE INDIA PVT. LTD. 19AAACL4159L1Z5 25 EXIDE INDUSTRIES LIMITED EXIDE INDUSTRIES LIMITED 19AAACE6641E1ZS 26 SHREE RENUKA SUGAR LTD. 19AADCS1728B1ZN 27 ADANI WILMAR LIMITED ADANI WILMAR LIMITED 19AABCA8056G1ZM 28 AJAY KUMAR GARG OM COMMODITY TRADING CO. -

Indiarf Announces USD 144 Million Investment in Panacea Biotec Ltd

IndiaRF Announces USD 144 million Investment in Panacea Biotec Ltd. - Investment to be used for one-time settlement with existing lenders, working capital and growth requirements – Mumbai, India, April 08, 2019: India Resurgence Fund (“IndiaRF”), promoted by Piramal Enterprises Limited and Bain Capital Credit, along with its affiliates today announced an investment of up to INR 992 crores/ USD 144 million in New Delhi based Panacea Biotec Limited (“Company”). The investment proceeds will be used for a one-time settlement with existing lenders, general working capital and growth requirements of the Company. This investment is structured by way of Non-Convertible Debentures (NCDs) of up to INR 864 crores and subscription amount of INR 32 crores towards share warrants to be allotted on a preferential basis. The subscription amount represents 25% of total amount of INR 128 crores proposed to be raised upon issuance of equity shares against warrants as per SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2018. Subject to exercise of warrants, IndiaRF (along with its affiliates) will collectively end up owning 10.4% stake in the company on a fully diluted basis. Commenting on the investment, Shantanu Nalavadi, Managing Director, IndiaRF said, “We are pleased to partner with Panacea Biotec, as it embarks on an exciting journey to enhance its market position as a strong, research-focused pharmaceutical and biotechnology company. The purpose of this investment is to not only restructure the Company’s balance sheet, but more importantly, work closely with the promoters and management team, to drive rapid revenue growth and sustainable profitability improvement.