Ipl-63Rd-Annualreport-2017-2018.Pdf

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Acquirer : Indian Potash Limited (Ipl) Target Enterprise

SUMMARY - 500 WORDS A. NAME OF THE PARTIES TO THE COMBINATION: ACQUIRER : INDIAN POTASH LIMITED (IPL) TARGET ENTERPRISE: TITAWI SUGAR COMPLEX (TSC), UNIT OF MAWANA SUGARS LIMITED (MSL) B. TYPE OF THE COMBINATION IPL has entered into a Business Transfer Agreement dated 18.11.2016(BTA) with MSL. Pursuant to BTA, IPL shall, subject to all necessary consents and approvals acquire one sugar mill of MSL operating under the name and style of “ Titawi Sugar Complex”(TSC) located at Titawi, Muzaffarnagar, UP on “ AS IS WHERE IS WHAT IS “ basis as a going concern. C. AREA OF ACTIVITY OF THE PARTIES TO THE COMBINATION: The primary business of IPL is sale of fertilizer on pan India, the major fertilizer being MOP, DAP & SOP, Rock Phosphate. In addition to the sale of these 4 fertilizers & others the company has also ventured into production & sale of Cattle Feed, packing operations for Milk , production & selling of Ghee & SMP , production & selling of sulphitation sugar & trading of Gold & other precious metals. IPL is selling fertilizer on pan India basis & with negligible exports to Nepal & Sri Lanka, as regards to Milk the company is doing process & packing operations on behalf of Mother Dairy. The selling of ghee & SMP is in Uttar Pradesh & Haryana, Cattle Feed in states of Uttar Pradesh, Haryana, Punjab, Rajasthan & Madhya Pradesh through our Uttar Pradesh Plant & Tamil Nadu , Andhra Pradesh through our Andhra Pradesh Plant and the sale gold is in Delhi, Rajasthan, Uttar Pradesh & Madhya Pradesh . MSL has an installed capacity of 29500 TCD cane crush . MSL is engaged in the business of manufacture and sale of sugar, power, Bagasse, molasses, press mud, Caustic Lye, Chlorine, HCL, SBP. -

Research Findings

e-ifc No. 55, December 2018 Research Findings Paddy rice demonstration plot in Uttar Pradesh, India. The difference in the height and number of leaves between the plants on the left (with potash applied) and the plot on the right (without) is clear. Photo by Potash for Life. Fertilizing Indian Rice Plots with Potash: Results from Hundreds of Locations Across the States of Andhra Pradesh, Chhattisgarh, Madhya Pradesh, Telangana, Uttar Pradesh and West Bengal Bansal, S.K.(1)*, P. Imas(2), and J. Nachmansohn(3) Abstract Agriculture forms the backbone of India’s economy; however, (MOP), and to demonstrate to farmers the increased yield and declining soil fertility is directly impacting crop productivity. The profitability obtained when fertilizing rice plots with MOP, a appropriate application of fertilizer is a key factor in enhancing large-scale trial project was launched in 2013: Potash for Life soil fertility and productivity and for overcoming potassium (K) depletion, which has been shown to have clear negative effects on India’s rice production. (1)Indian Potash Research Institute, Gurgaon, Haryana, India (2)International Potash Institute (IPI), Zug, Switzerland (3)Fertilizer, Soil and Water Management Expert, Yeruham, Israel In order to evaluate the response of rice to muriate of potash *Corresponding author: [email protected] Note: From article published in Indian Journal of Fertilisers 14(10):30-35 with permission from Ind. J. Fert. 24/42 e-ifc No. 55, December 2018 (PFL). The methodology was straight forward - two identical rice from too low use, and soil quality deterioration from over-use or plots side by side, with the only difference being that one of them imbalanced use. -

ANSWERED ON:20.12.2012 SUPPLY of IMPORTED FERTILIZERS to STATES Shankar Alias Kushal Tiwari Shri Bhisma

GOVERNMENT OF INDIA CHEMICALS AND FERTILIZERS LOK SABHA UNSTARRED QUESTION NO:4559 ANSWERED ON:20.12.2012 SUPPLY OF IMPORTED FERTILIZERS TO STATES Shankar Alias Kushal Tiwari Shri Bhisma Will the Minister of CHEMICALS AND FERTILIZERS be pleased to state: (a) whether the fertilizers have been imported recently; and (b) If so, the names of the States which have been supplied the imported fertilizers from the ports during the current year and the name of such ports? Answer MINISTER OF STATE (INDEPENDENT CHARGE) IN THE MINISTRY OF STATISTICS AND PROGRAMME IMPLEMENTATION AND MINISTER OF STATE IN THE MINISTRY OF CHEMICALS AND FERTILIZERS (SHRI SRIKANT KUMAR JENA) (a): Yes, Madam. Urea is the only fertilizer under statutory price control and it is imported for direct agriculture use on Government account through State Trading Enterprises (STEs) i.e. Minerals and Metals Trading Corporation Limited (MMTC), State Trading Corporation Limited (STC) and Indian Potash Limited (IPL) to bridge the gap between assessed demand and indigenous production. Fertilizers other than Urea are imported under Open General Licence (OGL). Companies import these fertilizers as per their commercial judgement. (b): Details of states supplied imported fertilizer (Urea, DAP, MOP & NPK) is as below: Sr.No. Name of Port Name of State 1. KANDLA J&K, HIMACHAL PRADESH, UTTRAKHAND, 2. MUND PUNJAB, HARYANA, RARAJASTHAN, GUJARAT, 3. PIPAVAV CHHATTISGARH, DELHI, MAHARASHTRA, 4. ROZY MADHYA PRADESH & UTTAR PRADESH 5. NEW MANGALORE KARNATAKA, TAMIL NADU, KERALA, MAHARASHTRA, ANDHRA PRADESH & MADHYA PRADESH 6. TUTICORIN TAMIL NADU, KERALA, 7 COCHIN ANDHRA PRADESH & 8. KARAIKAL KARNATAKA 9. CHENNAI TAMIL NADU, ANDHRA PRADESH, KERALA & KARNATKA 10. -

Active Members As on 31.03.2020

FAI MEMBERS (AS ON 24.08.2021) ACTIVE MEMBERS 1 Asian Fertilizers Limited 8 DCM Shriram Limited P.W.D. Officers Colony, (Unit : Shriram Fertilizers & Chemicals) Near Rastriya Sahara Press, Park Road, 2nd Floor, (West Wing), World Mark 1, Aerocity, Gorakhpur New Delhi - 110 037 Uttar Pradesh - 273 001 2 BEC Fertilizers 9 Grasim Industries Limited (Unit of Bhillai Engg. Corp.Ltd.) (Unit : Indo Gulf Fertilisers) Sector A, Sirgetti Industrial Area, Sirgetti, P.O. Jagdishpur Industrial Area Bilaspur 495 004 District Amethi 227 817 Chattisgarh Uttar Pradesh 3 Bharat Agri Fert. & Realty Limited 10 Greenstar Fertilizers Limited 301, 3rd Floor, Hubtown Solaries, SPIC House N.S. Phadke Marg, Near East West Flyover, No. 88, Mount Road, Guindy Andheri (East) Chennai 600 032 Mumbai Tamil Nadu Maharashtra - 400 069 4 Brahmaputra Valley Fertilizer Corporation Limited 11 Gujarat Narmada Valley Fertilizers & Chemicals Limited Regd. Office Namrup P.O. Parbatpur P.O. Narmada Nagar District Dibrugarh 786 623 District Bharuch 392 015 Assam Gujarat 5 Chambal Fertilizers and Chemicals Limited 12 Gujarat State Fertilizers & Chemicals Limited Corporate One, First Floor, P.O. Fertilizernagar 5, Commercial Center, Jasola District Vadodara 391 750 New Delhi - 110 025 Gujarat 6 Coimbatore Pioneer Fertilizers Limited 13 Hindalco Industries Limited P.O.Muthugoundanpudur (Unit : Birla Copper) Via Sulur 3rd Floor, Aries House, Near Hotel Siddharth Palace, Old District Coimbatore 641 006 Padra Road Tamil Nadu Baroda 390 015 Gujarat 7 Coromandel International Limited 14 Indian Farmers Fertiliser Cooperative Limited 1-2-10, Sardar Patel Road IFFCO Sadan Post Box No. 1589 C-1, District Centre, Saket Place, Secunderabad 500 003 New Delhi - 110 017 Telangana 15 Indian Potash Limited 22 Madras Fertilizers Limited Potash Bhawan, Manali 10-B, Rajendra Park, Pusa Road, Chennai 600 068 New Delhi - 110 060 Tamil Nadu 16 Indorama India Private Limited 23 Mangalore Chemicals & Fertilizers Limited Ecocentre, EM-4, 12th Floor, Level-11, UB Towers, UB City Unit No. -

In the Month of March 2020

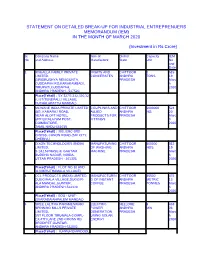

STATEMENT ON DETAILED BREAK-UP FOR INDUSTRIAL ENTREPRENUERS MEMORANDUM (IEM) IN THE MONTH OF MARCH 2020 (Investment in Rs Crore) Sl. Company Name Item of District Capacity IEM No and Address Manufacture State Unit No and Date 1 RNGALLA FAMILY PRIVATE FRUITS AND CHITTOOR 0 515 LIMITED. CONCERATES ANDHRA TONS 19 GIRIDRUSHYA RENIGUNTA, PRADESH Marc CUDDAPAH RO,KARAKAMBADI, h TIRUPATI,CUDDAPAH, 2020 ANDHRA PRADESH - 517520. Place(Tehsil) : SY.327/3,332,330,32 6,337(TENEPALLI VILLAGE, PUTHALAPATTU MANDAL) 2 MCWANE INDIA PRIVATE LIMITED COUPLINGS AND CHITTOOR 6000000 524 483, KAMARAJ ROAD, ALLIED ANDHRA NO. 20 NEAR ALOFT HOTEL, PRODUCTS FOR PRADESH Marc UPPILIPALAYAM POST, FITTINGS h COIMBATORE, 2020 TAMIL NADU-641015 Place(Tehsil) : 300, EMC-3RD CROSS, CANON ROAD,(SRI CITY, CHERIVI,) 3 DIXON TECHNOLOGIES (INDIA) MANUFATURING CHITTOOR 600000 512 LIMITED. OF WASHING ANDHRA NOS. 19 B-14,15,PHASE-II, GAUTAM MACHINE PRADESH Marc BUDDHA NAGAR, NOIDA, h UTTAR PRADESH - 201305. 2020 Place(Tehsil) : PLOT NO.30 AND 31(VIKRUTHAMALA VILLAGE) 4 CCL PRODUCTS (INDIA) LIMITED. MANUFACTURIN CHITTOOR 15500 472 DUGGIRALA VILLAGE,DUGGIR- G OF INSTANT ANDHRA METRIC 13 ALA MANDAL,GUNTUR, COFFEE PRADESH TONNES Marc ANDHRA PRADESH-522330. h 2020 Place(Tehsil) : EOU - UNIT- 2(VARADAIAHPALEM MANDAL) 5 SREE LALITHA PARAMESWARI ELECTRIC NELLORE 8 433 SPINNING MILLS PRIVATE POWER ANDHRA MW 06 LIMITED. GENERATION PRADESH Marc 1ST FLOOR TIRUMALA COMPL- USING SOLAR h EX,4TH LANE 2ND CROSS RD. ENERGY 2020 BRODIPET,GUNTUR, ANDHRA PRADESH-522002. Place(Tehsil) : TURPUROMPIDODL A VILLAGE(VINJAMURU) 6 GREENLAM SOUTH LIMITED. PLAIN PARTICLE NELLORE 214500 484 MAKUM ROAD,TINSUKIA, BOARD ANDHRA CBM 17 TINSUKIA, ASSAM-786125. -

Public Enterprises Survey 2017-18

Public Enterprises Survey 2017-18 Volume-II Government of India Ministry of Heavy Industries and Public Enterprises Department of Public Enterprises Public Enterprises Survey 2017-18: Vol-II i ii Contents CONTENTS Chapter Page Name of the Chapter No. No. A. 1-8 AGRICULTURE 1 3-8 AGRO BASED INDUSTRIES 1.1 6 ANDAMAN & NICOBAR ISL. FOREST & PLANT.DEV.CORP.LTD 1.2 7 HPCL BIOFUELS LTD. IND-AS 1.3 8 NATIONAL SEEDS CORPN. LTD. IND-AS B. 9-21 MINING AND EXPLORATION 2 11-21 COAL 2.1 14 BHARAT COKING COAL LTD. IND-AS 2.2 15 CENTRAL COALFIELDS LTD. IND-AS 2.3 16 COAL INDIA LTD. IND-AS 2.4 17 EASTERN COALFIELDS LTD. IND-AS 2.5 18 MAHANADI COALFIELDLS LTD. IND-AS 2.6 19 NORTHERN COALFIELDS LTD. IND-AS 2.7 20 SOUTH EASTERN COALFIELDS LTD. IND-AS 2.8 21 WESTERN COALFIELDS LTD. IND-AS 3 23-30 CRUDE OIL 3.1 26 BHARAT PETRO RESOURCES LTD. IND-AS 3.2 27 OIL & NATURAL GAS CORPORATION LTD. IND-AS 3.3 28 OIL INDIA LTD. IND-AS 3.4 29 ONGC VIDESH LTD. IND-AS 3.5 30 PRIZE PETROLEUM COMPANY LTD. IND-AS 4 31-44 OTHER MINERALS & METALS 4.1 34 FCI ARAVALI GYPSUM & MINERALS (INDIA) LTD. 4.2 35 HINDUSTAN COPPER LTD. IND-AS 4.3 36 INDIAN RARE EARTHS LTD. IND-AS 4.4 37 J & K MINERAL DEVELOPMENT CORPN. LTD. IND-AS 4.5 38 KIOCL LTD. IND-AS 4.6 39 MOIL LTD. IND-AS 4.7 40 NATIONAL ALUMINIUM COMPANY LTD. -

60Th Annual Report 2014 - 2015

60TH ANNUAL REPORT 2014 - 2015 INDIAN POTASH LIMITED REGISTERED OFFICE 1ST FLOOR, SEETHAKATHI BUSINESS CENTRE, 684-690, ANNA SALAI, CHENNAI - 600 006. TELEPHONE : 044 - 28297855 FAX : 044 - 28297407 INDIAN POTASH LIMITED BOARD OF DIRECTORS MS. VASUDHA MISHRA, IAS, Managing Director CHAIRPERSON National Cooperative Development Corporation DR. U.S. AWASTHI Managing Director Indian Farmers fertilizer Co-operative Limited SHRI PREM CHANDRA MUNSHI Director Indian Farmers fertilizer Co-operative Limited SHRI H.S. BAWA Director Zuari Global Limited SHRI BALVINDER SINGH NAKAI President Rampuraphul Co-operative Marketing cum Processing Society SHRI NATWARLAL Chairman PITAMBARDAS PATEL Gujarat State Co-operative Marketing Federation Limited DR. S K NANDA, IAS Chairman cum Managing Director Gujarat State Fertilisers and Chemicals Limited. SHRI DEVINDER KUMAR E.D. & Secretary Steel Authority of India Ltd. SHRI HEERALAL SAMARIYA, IAS Joint Secretary Department of Fertilisers, Government of India SHRI R G RAJAN Chairman cum Managing Director Rashtriya Chemicals & Fertilisers Limited DR. SUNIL KUMAR SINGH Chairman Bihar State Cooperative Marketing Union Limited SHRI SHYAMAL MISRA, IAS Managing Director The Haryana State Cooperative Supply & Marketing Federation Limited SHRI MANORANJAN PATNAIK, IAS Managing Director Odisha State Co-Op MKTG Federation Limited SHRI NAND KUMAR, IAS Managing Director The Maharashtra State Co-Op MKTG Federation Limited SHRI K.V.SATHYANARAYANA Director REDDY, Andhra Pradesh State Cooperative Marketing Federation Limited DR. P.S. GAHLAUT, Managing Director Indian Potash Limited 3 INDIAN POTASH LIMITED BANKERS STATE BANK OF INDIA STATE BANK OF HYDERABAD STATE BANK OF PATIALA CANARA BANK HDFC BANK LTD BANK OF BARODA PUNJAB NATIONAL BANK IDBI BANK LTD AXIS BANK LTD ALLAHABAD BANK INDUSIND BANK LTD DEUTSCHE BANK AG AUDITORS Messrs. -

Annual Report 2020 Final Page.Pmd

THE FERTILISERS AND CHEMICALS TRAVANCORE LIMITED Registered Office : Eloor, Udyogamandal, Kochi, Kerala CHAIRMAN’S MESSAGE of 3rd quarter of the financial year 2019-20, the outbreak of the COVID-19 in the fourth quarter has resulted in slow down of economic growth. On the external front, India continued to attract robust foreign direct investment. Foreign Portfolio investment inflows also rebounded in My dear shareholders, recent months. This reflect the unshaken belief of foreign investors A warm good morning to each and every one of you. I, as Chairman in India’s macro-economic fundamentals. & Managing Director of your Company, welcome all of you to the Agriculture, which contributes 15% of total gross value added is set 76th Annual General Meeting of FACT. to push in the shock of COVID-19 pandemic in Indian economy in As all of you are aware the 76th AGM is convened as a virtual meeting, the year 2020-21. due to the spread of pandemic COVID-19, the most disruptive event Comfortable Foreign Exchange Reserve, higher Foreign Direct in the modern human history. The world economy is facing an Investment, low oil prices coupled with the monetary policy of the unprecedented crisis and hardships due to the pandemic. Reserve Bank of India and stimulus package of the Government of The pandemic did not spare any sector including Fertilizer. Everyone India would stimulate the Indian Economy. has to respond with exceptional measures to maintain operation and Fertilizer Industry to continue to provide services to customers while ensuring the health During the financial year 2019-20, production of total fertilizer nutrients and safety. -

Download E-Ifc High Resolution (Pdf 4.9

No. 61 | September 2020 e-ifc No. 61, September 2020 Editorial Dear readers, Editorial 2 Population growth, urbanization, diets becoming more Research Findings diverse: all these are increasing demand for more vegetables and fruits. Response of Cabbage to Potash 3 Fertilization in Field Plot Trials Conducted However, consumers do not just want quantity, most of in Jammu & Kashmir, West Bengal and us want quality too. Quality is consistently rated higher Maharashtra in importance than price, brand name or freshness. Bansal, S.K., P. Imas, and J. Nachmansohn Of all essential plant nutrients, potassium is often referred to as the ‘quality element’ in crop production: grains are bigger; more protein, oil and vitamin C Polyhalite Effects on Coffee (Coffea 13 content in grains, fruits and vegetables; increased size robusta) Yield and Quality in Central of fruits and tubers; enhanced fruit color and flavor; and Highlands, Vietnam improved storage, ease of shipping and longer shelf life. Tien, T.M., T.T.M. Thu, H.C. Truc, and T.C. Tu Numerous on-farm trials within IPI projects have proved that balanced fertilization ticks all the quality criteria boxes. The farmer who practices balanced fertilization will have better market opportunities, get higher prices and increased income. Scale this up across Publications 27 a region and it is easy to see how the application of balanced fertilizer benefits the whole nation with better Scientific Abstracts 27 social stability, less migration and, last but not least, better export opportunities of competitive high-quality produce. Obituary 35 Professor Emeritus Joseph Hagin In October this year, again we celebrate FAO’s World Food Day to promote global awareness and action for those who suffer from hunger. -

Mushroom-Machinery.Pdf

Our Profile: We are the manufacturer of all kinds of Mushroom Farming Machinery and provides complete Mushroom Project Consultancy services which include our visit to their farm, project report formation which is prepared by our CA, Site Mapping, complete Farm Layout prepared by our Civil Engineer, Insulated Puff Panel rooms construction, Composting Unit Formation and installation of latest technology based fully and semiautomatic machinery under the supervision repudiated scientist and consultant. We also dealing in all type of shed constructions work which includes formation of Pre-Fabricated shed which are used for multipurpose. This shed work is completed under the guidance of our highly experienced & expertise team. We also provide our services to Old Mushroom Farm which needs automation. For this automation our expertise will visit to their farm and with their magnificent knowledge and matured experience suggest them the best possible way to atomized old methodology with the latest one. We work with an aim to provide customize solution to our customer as per there Project requirement as we are the manufacturer of wide range of Mushroom Farming Machinery. Our Machineries are fully Automatic, Computerized as well as semiautomatic based on customer need. Our machineries helpful to maintained control environmental condition inside growing room and composting tunnel so throughout the season customer received best quality of Compost and superior grade of Mushrooms in bulk amount without affecting by external temperature & Humidity. Our highly qualified and hard working team with their innovative ideas and technical mind working on the each & every challenging task faced in mushroom field and to grow this Mushroom field worldwide for the goodwill of humanity. -

Annual Report 15-16

CENTRAL WAREHOUSING CORPORATION CENTRAL WAREHOUSING CORPORATION Annual Report 2015-16 i ii CENTRAL WAREHOUSING CORPORATION fo"k; lwph CONTENTS Page. No. 1 funs'kd e.My v Board of Directors 2 izcaèku vi Management 3 va'kèkkfj;ksa dks lwpuk xi Noce to Shareholders 4 y{;] nwjnf'kZrk ,oa mís'; xiv Mission, Vision, & Objecves 5 izeq[k fof'k"Vrk,a xv Highlights 6 funs'kd e.My dh fjiksVZ 1 Directors’ Report 7. fuxfer lkekftd nkf;Ro ,oa lqfLFkj fodkl xfrfofèk;ksa ij fjiksVZ 38 Report on Corporate Social Responsibility and Sustainable Development Acvies 8. uSxe vfèk'kklu fjiksVZ 42 Report on Corporate Governance 9. uSxe vfèk'kklu ij vuqikyu izek.k i= 57 Compliance Cerficate on Corporate Governance 10. dsUnzh; Hk.Mkjx`gksa dh lwph ,oa mudh Hk.Mkj.k {kerk 59 List of Central Warehouses and their Storage Capacity 11. lkekU; fufèk ys[ks dk fooj.k 91 12 lkekU; fufèk vuqlwfp;ka 98 13. Statement of Account of General Fund 133 14. General Fund Schedules 140 15. ys[kk ijh{kdksa dh fjiksVZ rFkk fuxe ds izR;qrj 174 Auditors’ Report and Replies of the Corporaon 16. Hkkjr ds fu;a=d ,oa egkys[kk ijh{kd dh fjiksVZ 181 Report of the C&AG of India 17. vè;{k dk vfHkHkk"k.k 183 Chairman’s Address Annual Report 2015-16 iii Jh gjizhr flag] izcaèk funs'kd] dsUnzh; Hk.Mkj.k fuxe dh 54oha okf"kZd lkèkkj.k cSBd ds volj ij fnukad 24 flrEcj -2016 dks va'kèkkfj;ksa dks lacksfèkr djrs gq,A Shri Harpreet Singh, Managing Director, CWC addressing the shareholders on the occasion of 54nd Annual General Meeng on 24th September 2016. -

LIST of IEM FILED from : 16/03/2020 to : 20/03/2020

LIST OF IEM FILED From : 16/03/2020 To : 20/03/2020 S No. IEM No & DATE Name and Address of the Party District & State Item of Manufacture 1 474/ RMM AGRO EXPORTS PVT.LTD., HOSHANGABAD, RICE 16/03/2020 C-1 TO C-7, E-12 TO E-17, MADHYA PRADESH FOOD PARK, NEAR JAIL PACHMARHI ROAD,KALLUKHAPA PIPARIYA, HOSHANGABAD, MADHYA PRADESH-461775. 2 475/ ROOTS MULTICLEAN LTD., COIMBATORE, MANUFACTURE OF 16/03/2020 RKG INDUSTRIAL ESTATE, TAMIL NADU MECHANIZED CLEANING GANAPATHY, COIMBATORE, EQUIPMENTS TAMIL NADU-641006. 3 476/ ROOTS INDUSTRIES INDIA LIMITED. COIMBATORE, COMPONENTS FOR 16/03/2020 SF NO.265,R.K.G.INDUSTRI- TAMIL NADU MEDICAL EQUIPMENTS AL ESTATE,GANAPATHY,COIM- BATORE,TAMIL NADU-641006. 4 477/ NIF PVT. LTD., KANPUR, ICE CREAM AND KULFI 16/03/2020 119-121(PART),BLOCK P & T UTTAR PRADESH MANUFACTURING WITH FAZALGANJ,KALPI ROAD, HELP OF MILK KALPI ROAD,KANPUR, UTTAR PRADESH-208012. 5 478/ GRAINSPAN NUTRIENTS PRIVATE SONIPAT, MAIZE GRITS 16/03/2020 LIMITED. HARYANA 504-505,SHAPATH V,OPP.KA- RNAVATI CLUB,S.G.HIGHWAY, AHMEDABAD,GUJARAT- 380058 6 479/ WESTERN REFRIGERATION PRIVATE VALSAD, MANUFACTURE OF 16/03/2020 LIMITED. GUJARAT REFRIGERATOR FOR SURVEY NO.174/1,KANADI COMMERCIAL USE ROAD,NAROLI VILLAGE,SILV- ASA,UNION TERRITORY OF DADRA & NAGAR HAVELI- SILVASA - 396235. 7 480/ EMPYREAN SKYVIEW PROJECTS UDHAMPUR, OTHER AMUSEMENT 16/03/2020 PVT.LTD., JAMMU AND AND RECREATION 411 B2, 4TH FLOOR,SOUTH KASHMIR ACTIVITIES BLOCK,BAHU PLAZA, JAMMU AND KASHMIR (UT)-180012. 8 481/ INDIAN POTASH LIMITED. MUZAFFAR NAGAR, COMPRESSED BIO GAS 16/03/2020 SEETHAKATHI BUSINESS CEN- UTTAR PRADESH TRE,1ST FLOOR,684-690, SEETHAKATHI BUSS.