D-Zine Men's Apparel

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Simon & Authentic Brands to Buy Brooks Brothers

https://nyti.ms/2DCNl47 Bankrupt Brooks Brothers Finds a Buyer The retailer is seeking court approval of a $325 million sale to a group backed by the mall owner Simon Property Group and Authentic Brands Group, a licensing firm. By Sapna Maheshwari Aug. 12, 2020 Brooks Brothers, the venerable retailer that was founded in 1818 and filed for bankruptcy last month, said it would be sold to Simon Property Group, the biggest mall operator in the United States, and Authentic Brands Group, a licensing firm. The $325 million offer for Brooks Brothers, up from a $305 million bid last month from the same suitors, is subject to court approval this week, the companies said in a statement late on Tuesday. The buyers committed to continue operating at least 125 Brooks Brothers retail locations. Before the pandemic, the company operated 424 retail and outlet stores globally, including 236 in the United States, according to court documents. The offer for Brooks Brothers came from an entity known as the SPARC Group, a joint venture between Simon Property and Authentic Brands Group. The mall owner and A.B.G. have teamed up on deals to buy other bankrupt retailers in recent years, including the teen chain Aéropostale and the fast-fashion behemoth Forever 21. SPARC has also bid on Lucky Brand, the denim company that filed for bankruptcy last month. A.B.G. is known for acquiring the intellectual property of brands like Barneys New York and Sports Illustrated, then licensing their names to other companies and earning royalties from related products. The coronavirus outbreak has toppled several storied retail brands, especially those focused on apparel, as many stores were forced to temporarily close and demand for new clothing dropped in a remote, less social environment. -

SPYDER LAUNCHES in SOUTH KOREA with All New Performance Collection in 25 Retail Locations

For Immediate Release SPYDER LAUNCHES IN SOUTH KOREA With All New Performance Collection in 25 Retail Locations Seoul & Hong Kong – September 22, 2015 / New York – September 21, 2015 – Leading ski and sportswear brand, Spyder has launched in South Korea with an all-new product line available in freestanding stores and shop-in-shops. An accelerated retail rollout is planned with twenty-five Spyder stores opening across the country by the end of 2015. “We are excited to be working with Global Brands to bring Spyder to South Korea, one of the world’s most fashion-forward and trendsetting markets,” said Jamie Salter, Chairman and CEO of Authentic Brands Group and owner of the brand. “Spyder is highly regarded and we are confident that the brand will flourish in the country.” Designed for the style-seeking South Korean consumer, both the men’s and women’s collections draw from the core DNA of the brand, fusing elements of performance and fashion. "We see tremendous equity in the Spyder brand and its ability to translate across key markets in Asia," said Bruce Rockowitz, CEO and Vice Chairman, Global Brands Group Holding Limited. "We look forward to replicating the success we have achieved in other markets to South Korea, through the roll out of a number of exciting brand and category extensions." Spyder is featured in shop-in-shops at fashion hot spots including Galleria Department Store, Hyundai Department Store, Lotte Department Store and AK Department Store. The brand also launches with freestanding stores in Seoul, Daegu, Gumi, Incheon and Sokcho. Spyder will be promoted in a 360 degree campaign that includes national Print, Out of Home, Digital, Social, and TV promotion beginning this month. -

Consumer & Retail

CONSUMER & RETAIL Industry Snapshot | March 2021 Table of Contents 1. About Configure Partners 3 2. Industry Debrief 4 3. Macroeconomic Indicators 5 4. Subsector Performance 6 5. Public Comparables Analysis 7 6. Recent Bankruptcy Activity 8 This message and any attachment(s) is intended only for the use of the addressee(s) and may contain information that is PRIVILEGED and/or CONFIDENTIAL. If you are not the intended recipient(s), you are hereby notified that any dissemination of this communication is strictly prohibited. If you have received this communication in error, please erase all copies of the message and its attachments and notify us immediately. Although we attempt to sweep e-mail and attachments for viruses, we do not guarantee that either are virus-free and accept no liability for any damage sustained as a result of viruses. Securities transactions offered through our affiliate, Configure Partners Securities, LLC, member FINRA/SiPC. Principals of Configure Partners, LLC are registered representatives of Configure Partners Securities, LLC. Configure Partners, LLC and its affiliate are (a) not a law firm and do not provide legal advice and (b) not a CPA firm and do not provide audit or public accounting services. Configure Partners, LLC and its affiliate do not provide tax advice, and nothing contained in this communication (including any attachments) is intended or written to be used, and cannot be used, for the purpose of (a) avoiding penalties under applicable tax code or (b) promoting or otherwise recommending to another part any transaction of matter addressed of referenced herein. Copyright © Configure Partners, All rights reserved. -

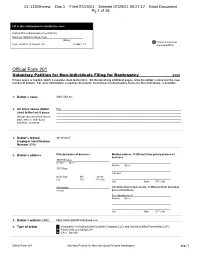

Petition for Non-Individuals Filing for Bankruptcy 04/20 If More Space Is Needed, Attach a Separate Sheet to This Form

21-11369-mew Doc 1 Filed 07/29/21 Entered 07/29/21 09:27:17 Main Document Pg 1 of 19 - Fill in this information to identify the case: United States Bankruptcy Court for the: Southern District of New York (State) Check if this is an Case number (if known): 21- Chapter 11 amended filing Official Form 201 Voluntary Petition for Non-Individuals Filing for Bankruptcy 04/20 If more space is needed, attach a separate sheet to this form. On the top of any additional pages, write the debtor’s name and the case number (if known). For more information, a separate document, Instructions for Bankruptcy Forms for Non-Individuals, is available. 1. Debtor’s name GBG USA Inc. 2. All other names debtor N/A used in the last 8 years Include any assumed names, trade names, and doing business as names 3. Debtor’s federal 94-3032467 Employer Identification Number (EIN) 4. Debtor’s address Principal place of business Mailing address, if different from principal place of business 350 Fifth Ave Number Street Number Street 10th Floor P.O. Box New York NY 10118 City State ZIP Code City State ZIP Code Manhattan Location of principal assets, if different from principal County place of business See Attachment A Number Street City State ZIP Code 5. Debtor’s website (URL) https://www.globalbrandsgroup.com 6. Type of debtor Corporation (including Limited Liability Company (LLC) and Limited Liability Partnership (LLP)) Partnership (excluding LLP) Other. Specify: Official Form 201 Voluntary Petition for Non-Individuals Filing for Bankruptcy page 1 21-11369-mew Doc 1 Filed 07/29/21 Entered 07/29/21 09:27:17 Main Document Debtor GBG USA Inc. -

Snap, Crackle

ALL JUSTICE’S DOLLED AFTERMATH 18 PEOPLE NAMED UP FOR THEIR ALLEGED INVOLVEMENT IN BARBIE GETS OUTFITTED… FRESH APPROACH HICKEY FREEMAN GETS A FACELIFT FOR SPRING. PAGE MW1 THE RANA PLAZA AS LAGERFELD. PAGE 7 TRAGEDY. PAGE 2 BACK ON THE TABLE Internet Sales Tax Bill Gets Push From Senate By KRISTI ELLIS WASHINGTON — Retailers’ efforts to close the Internet sales tax loophole just found new life on Capitol Hill. A group of senators, led by Sens. Dick Durbin (D., Ill.) and Mike Enzi (R., Wyoming), have introduced THURSDAY, JULY 17, 2014 ■ $3.00 ■ WOMEN’S WEAR DAILY legislation that combined their own bill enabling WWD states to collect sales taxes from out-of-state online sellers with a House-passed bill extending a perma- nent ban on states taxing Internet access. The new combined legislation is designed to equalize the ground rules for brick-and-mortar retailers. Retailers have led the fi ght to close the Internet sales-tax loophole for more than a decade without resolution, but the new legislation gives fresh mo- COLLECTIONS mentum to the effort. Retail groups in Washington lauded the revived legislative effort, which had been stalled this year. BERLIN “The National Retail Federation applauds the in- SPRING 2015 troduction of this bipartisan piece of legislation that seeks to level the playing fi eld between local, brick- and-mortar merchants and online retailers without Snap, creating or raising taxes,” said David French, senior vice president for government relations at the NRF. “The retail industry has rapidly evolved over the last two decades with e-commerce and mobile commerce, and it is time for Congress to eliminate the sales tax disparity, which disproportionately impacts commu- Crackle.. -

Allsaints Selects the Island Pacific Smartplanning & Allocation

AllSaints selects the Island Pacific SmartPlanning & Allocation Manager Solution ● Island Pacific SmartPlanning & Allocation Manager chosen to support a leading and prestigious international brand operating a multi-channel business Island Pacific UK Ltd – 5th February 2018: Island Pacific, a division of 3Q Holdings Limited and a leading provider of global software solutions and services to the retail industry, announced it has signed a major deal with AllSaints for the deployment of its Island Pacific SmartPlanning & Allocation Manager solution. Island Pacific SmartPlanning will provide AllSaints with the tools to carry out strategic high- level pre-season and in-season plans across merchandise in all channels. Island Pacific SmartPlanning drives full planning lifecycle management, strategic budget planning, cross- channel and store planning, export capabilities, integrated reporting and much more. The tightly integrated Allocation Manager allows the distribution process to be streamlined across channels making the process faster and more efficient. Multiple allocation methods bring increased efficiency and greater inventory control. Nicole Smith, Global Trading Director at AllSaints said: “We feel the Island Pacific SmartPlanning & Allocation Manager solution has rich functional applications, which will enable us to strategically manage all aspects of planning and allocation within our business. It will provide the merchandising team with industry best practice that includes modern, flexible, and timely planning techniques. The integrated allocation module will make full use of our plans to create greater efficiency for my team as well as more effective management of stock across the business. This will be important to ensure the continued international success and growth of our brand.” Peter Wood, COO at AllSaints said: “Island Pacific's reputation for delivery and significant return on investment were key considerations in our decision. -

Sign up for Little League! Currently, the District Lion in Developer’S Fees the Three Officers, Chief Has $4.5 Million in Pri- for Debt Service

Home of The Huntington Library, Art Collections, and Botanical Gardens The Voice of Our Community Since 1929 Vol. 87 No. 51 San Marino, Friday, December 16, 2016 2650 Mission Street (626) 792-NEWS $1.75 a Copy, $89 per year ‘A Night of Choreography’ at SMHS Saturday DRC Deems Wallace Neff Community Invited to Watch Dance Students Take Their Final Exams House To Be Historically Significant to San Marino Decision Triggers Focused Environmental Impact Review For 1040 Oak Grove Avenue By Kev Kurdoghlian under CEQA, but that “the ASSISTANT EDITOR, NEWS exception to an exemp- tion is if the project would The San Marino De- significantly impact a his- sign Review Committee torical resource.” unanimously declared a See DRC page A-3 Wallace Neff-designed, California Ranch style home at 1040 Oak Grove City Will Begin Ave. to be historically sig- nificant for the City of San Search for New Marino. The committee’s action City Manager will require the home- owner, Hongbin Peng, to In the New Year CRAMMING FOR FINALS: Members of San Marino High School’s Dance Department rehearse the numbers they initiate an environmen- tal impact review, or EIR, By Kev Kurdoghlian will perform at Saturday’s ‘A Night of Choreography,’ which will take place in the Neher Auditorium at 7:00 p.m. ASSISTANT EDITOR, NEWS The dances are the students’ final exams. PICTURED ABOVE, left to right, are Queenie Qiu, Rinn Maldonado, which will examine the Serena Wang, Cortney Yue, Gwyneth Walla, Danielle Drake, Amber Chien, Grace Gambito, Alexis French, Serena impact of tearing down Cossu, Sofia Miera and Maya Puri. -

Sui Generis Protection for the Innovative Designer Linna T

Hastings Law Journal Volume 63 | Issue 1 Article 6 12-2011 Note – Fashioning a New Look in Intellectual Property: Sui Generis Protection for the Innovative Designer Linna T. Loangkote Follow this and additional works at: https://repository.uchastings.edu/hastings_law_journal Part of the Law Commons Recommended Citation Linna T. Loangkote, Note – Fashioning a New Look in Intellectual Property: Sui Generis Protection for the Innovative Designer, 63 Hastings L.J. 297 (2011). Available at: https://repository.uchastings.edu/hastings_law_journal/vol63/iss1/6 This Note is brought to you for free and open access by the Law Journals at UC Hastings Scholarship Repository. It has been accepted for inclusion in Hastings Law Journal by an authorized editor of UC Hastings Scholarship Repository. Loangkote_19 (J. Grantz) (Do Not Delete) 12/5/2011 11:35 PM Note Fashioning a New Look in Intellectual Property: Sui Generis Protection for the Innovative Designer Linna T. Loangkote* Fashion design is weaving its way through the fabric of American society by transforming how people think about fashion apparel. The $350 billion fashion industry not only puts the clothes on our backs, but gives individuals an outlet for individual expression as well. More and more, the fashion design process is recognized as a creative process where vision, raw materials, and skill meet to produce fashion apparel that should be worthy of sui generis protection. Current intellectual property regimes fail to adequately equip designers with legal remedies to guard against design piracy, and this affects both innovation and competition. Moreover, even though the U.S is a signatory to the Berne Convention, the U.S.’s lack of a protection scheme for fashion design is out of step with other signatory members, namely the European Union, and this mismatch could invite unintended reciprocity problems for American designers abroad. -

Welcome to Eye Surgeons and Consultants! WE USE the MOST ADVANCED TECHNOLOGY and CUSTOMIZE OUR SERVICE to YOUR EYES!

Alan Mendelsohn, M.D. Nathan Klein, O.D. 954.894.1500 Welcome to Eye Surgeons and Consultants! WE USE THE MOST ADVANCED TECHNOLOGY AND CUSTOMIZE OUR SERVICE TO YOUR EYES! SERVICES For your convenience, we also have a full service optical dispensary Laser Cataract Surgery with the highest quality and huge selection of the latest styles of Laser Vision Correction eyeglasses and sunglasses, including: Glaucoma Laser Surgery Comprehensive Eye Exams Oliver Peoples • Michael Kors • Barton Perreira • Tom Ford • Burberry Macular Degeneration Marc Jacobs • Lily Pulitzer • Mont Blanc • Nike Flexon • Silhouette Diabetic Eye Exams Glaucoma Exams We provide personalized, professional care using Red Eye Evaluations a state-of-the-art computerized in-house laboratory. Dry Eye EXTENDED HOURS: MON: 7:30AM – 8:00PM Contact Lens Exams TUE – FRI: 7:30AM – 4:30PM • SUN: 7:30AM – 11:30AM Scleral Contact Lenses 4651 Sheridan Street, Suite 100, Hollywood, FL 33021 • 954.894.1500 PLEASE SEE OUR WEBSITE: www.myeyesurgeons.com for sight-saving suggestions! YOUNG ISRAEL OF HOLLYWOOD-FT. LAUDERDALE SEPTEMBER 2021 PAGE 3 FACTS I DISCOVERED WHILE LOOKING UP OTHER THINGS Rabbi Edward Davis JULIAN. On July 19, 362 CE, the new emperor, bath and to instruct the women about the rules of immersion. Constantine’s nephew, Julian, was in Antioch, on his way to When asked whether he was not afraid that his passion get invade Persia. He asked a Jewish delegation: “Why are you the better of him, he replied that to him the women looked not sacrificing?” The Jews answered, “We are not allowed. like so many white geese. -

The Abg Difference

“AS ABG CONTINUES TO BUILD OFF ITS SUCCESS AS AN INTELLECTUAL PROPERTY LICENSOR, THE COMPANY IS CHANGING THE FACE OF THE LICENSING GAME. WE’RE GOING BEYOND THE TRADITIONAL BRANDED PRODUCT APPROACH AND WE ARE CREATING EXPERIENCE BASED OUTLETS WHICH BUILD AUTHENTIC BRAND LOYALTY. ” THE WORLD IS FULL OF IDEAS. SOME ARE GROUND BREAKING, BUT HAVE Nick Woodhouse NO STRUCTURE. President & CMO WE ARE IDEA NAVIGATORS + WE TAKE BRILLIANCE AND POINT IT TOWARD SUCCESS COMPANY PROFILE WE ARE A BRAND DEVELOPMENT, We are backed by one of the nation’s preeminent private equity firms LICENSING AND ENTERTAINMENT with over $15 billion of private equity capital raised since inception. The COMPANY. IN CONJUNCTION WITH firm, founded in 1989, has invested in over 70 companies with aggregate value of over $88 billion. LEONARD GREEN & PARTNERS, OUR Leonard Green & Partners’ current and past portfolio includes numerous MANDATE IS TO ACQUIRE, MANAGE leading retailers such as Neiman Marcus, Whole Foods Market, Lucky Brand, Topshop/Topman, The Container Store, J.Crew, Bergdorf Goodman’s, AND ELEVATE THE LONG-TERM VALUE Equinox, PETCO Animal Supplies, The Sports Authority, Tourneau, David’s IN CONSUMER, CELEBRITY AND Bridal and Rite Aid. MEDIA BRANDS. ABG’s mission is to build a global portfolio of world-renowned brands and to further enhance brand equity by partnering with industry leading brand licensees. Our portfolio of brands span the celebrity, media and entertainment, luxury apparel, action sports, home and consumer electronics segments. This vast footprint enables us to develop partnerships with key accounts across retail channels from high-end department and specialty stores to mid-tier and mass retailers. -

Home | Bus./Industry | Ukraine | World | Health/Science | Opinion | Culture

Home | Bus./Industry | Ukraine | World | Health/Science | Opinion | Culture | Community | Art/Bks/Film | Travel | Sports | Today's photo EBRD increases UkrFarm Funding credit line to $40 mln 2011/7/4 12:12:51 UkrFarm belongs to the holding company Ukrainian Agrarian Investments, the main shareholder of which is Renaissance Group KYIV, July 4, 2011 (UBO) – The European Bank for Reconstruction and Development (EBRD) increases its credit line for UkrFarm Funding Limited (Cyprus), uniting more than 70 Ukrainian agricultural enterprises and an affiliate of Renaissance Group, to USD 40 million for the expansion of the company's activity, UkrInform reported. Authorization The credit line was opened in 2010 in the original amount of USD 20 million. It is assumed that the loan will help UkrFarm Funding increase the efficiency and productivity of arable land, as well as provide the expansion of land bank by 50,000 Username: he to 300,000 he before the end of 2013. Password: UkrFarm belongs to the holding company Ukrainian Agrarian Investments, the main shareholder of which is Renaissance Group. Remember me User Login Oldest First Refresh Post Comment Lost Password? Register now! Poster Thread Guest Posted: 2014/5/29 14:16 Search christian louboutin discount Search Cheap Christian Louboutin Shoes http://sophiadengo.com/cheap-christian-louboutin-shoes Web hosts are the hosts which allow us to make and design oNo Comments.. Do you own yours' cheap Louboutin shoes http://sophiadengo.com/cheap-louboutin-shoes insincere apology was unhelpful to the Government, the Tory Party and the reputation of MPs generally. Even if she thinks she has done nothing wrong, as she appears to do, she should surely know the importance of a show of contrition. -

Fashion Design Merchandising Strands and Standards

STRANDS AND STANDARDS FASHION DESIGN MERCHANDISING Course Description The Fashion Merchandising course is an introductory class that teaches the concepts of entry- level business and fashion fundamentals. The following list of skill strands prepares the student in fashion merchandising in the fundamentals of basic fashion concepts and marketing terminology, fashion cycles, key components of the fashion industry shuc a s fashion designers, fashion capitals and fashion week, retail merchandise categories, fashion promotion including advertising and social media, and fashion careers. Student leadership and competitive events (FCCLA and/or DECA) may be an integral part of the course. Intended Grade Level 10-12 Units of Credit .50 Core Code 34.01.00.00.145 Concurrent Enrollment Core Code NA Prerequisite Fashion Design Studio Skill Certification Test Number 405 Test Weight 0.5 License Type CTE and/or Secondary Education 6-12 Required Endorsement(s) Endorsement 1 Family & Consumer Sciences Endorsement 2 Fashion/Textiles/Apparel ADA Compliant: April 2021 FASHION DESIGN MERCHANDISING STRAND 1 Students will recognize basic fashion concepts and terminology. Standard 1 Review fashion terms. (Fashion Design Studio Standard 1) Accessories, apparel, avant-garde, classic, composite, design detail, draped, fad, fashion, fashion cycle, fit, garment type, haute couture, ready to wear, silhouette, style, tailored, trend, wardrobe. Standard 2 Identify fashion products. • Goods – tangible items that are made, manufactured, or grown. They include apparel, textiles, accessories, and other fashion products. • Services – intangible things that people do, such as tasks performed for customers. They include tailoring, cosmetology services, and stylist. STRAND 2 Students will examine the basics of fashion marketing and associated careers.