Press Release KN Sindagi Solar Energy Private Limited

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Karnataka Name of Graduates' Constituency : Karnataka North West Graduates

Table of Content of Graduates' Constituency of Legislative Council Electoral Roll of the Year 2015 Name Of State: Karnataka Name of Graduates' Constituency : Karnataka North West Graduates DETAILS OF REVISION Year of revision : 2015 Type of revision : Summary Qualifying date : 01-11-2015 Date of publication : 18-01-2016 (a).Name of Graduates' Constituency : Karnataka North West Graduates Karnataka North West Graduates (b).Districts in which the aforesaid Constituency is located : Belgaum,Bagalkot,Bijapur. (c) No. and Name of Assembly Constituency Comprised within the All the Assembly Constituencies in the districts of aforesaid Graduates' Constituency : Belgaum,Bagalkot,Bijapur. TOTAL NO. OF PARTS IN THE CONSTITUENCY : 150. COMPONENTS OF THE ROLL. (A) Mother roll (B) Supplement-1 (C) Supplement-2 NET NUMBER OF ELECTORS : Male Female Others Total 141286 37801 11 179098 Part No : 111 Electoral Rolls,2015 of North West Graduates Constituency of Karnataka Legislative Council District : Bijapur Taluk/Town/City : Muddebihal Area : Muddebihal.Kuntoji,kolur,Tangadagi,Nebageri,Mudur,Kolur,L.T. Devur,Abbihal,Kavadimatii,Harindral.Geddalamari,Mudnal,Hadalageri,Handargal,Nagaral,Hadagali,Chirch ankal,Inchagal.Yargal,Gonal.S.H.Banoshi,Kamaladinni,Gangur,Chalmi,Alur,Kunchaganur,Kalagi,Amaragol, Shirol,Garasangi,Madari,Bailakur,Madinal,Gonal P.N Sl No Name of the Elector Name of Address (Place of Ordinary Qualification Business Age Sex EPIC Photo of Father/Mother/Husband Residence) Number the elector 1 2 3 4 5 6 7 8 9 10 1 L A Rajashekhar Em N A Maruthi Nagar Muddebihal M S C M Ed M Phila Lecturer 36 M Photo Not Available 2 PARAVIN AALAGUR Abdulakhadar AALAGUR .,Muddebihal, Muddebihal, B.A.,Bed. -

Muddebihal Assembly Karnataka Factbook

Editor & Director Dr. R.K. Thukral Research Editor Dr. Shafeeq Rahman Compiled, Researched and Published by Datanet India Pvt. Ltd. D-100, 1st Floor, Okhla Industrial Area, Phase-I, New Delhi- 110020. Ph.: 91-11- 43580781-84 Email : [email protected] Website : http://www.indiastatelections.com Online Book Store : www.indiastatpublications.com Report No. : AFB/KA-026-0121 ISBN : 978-93-87148-19-2 First Edition : January, 2018 Third Updated Edition : January, 2021 Price : Rs. 11500/- US$ 310/- © Datanet India Pvt. Ltd. All rights reserved. No part of this book may be reproduced, stored in a retrieval system or transmitted in any form or by any means, mechanical photocopying, photographing, scanning, recording or otherwise without the prior written permission of the publisher. Please refer to Disclaimer at page no. 183 for the use of this publication. Printed in India Contents No. Particulars Page No. Introduction 1 Assembly Constituency - (Vidhan Sabha) at a Glance | Features of Assembly 1-2 as per Delimitation Commission of India (2008) Location and Political Maps Location Map | Boundaries of Assembly Constituency - (Vidhan Sabha) in 2 District | Boundaries of Assembly Constituency under Parliamentary 3-10 Constituency - (Lok Sabha) | Town & Village-wise Winner Parties- 2019, 2018, 2014, 2013 and 2009 Administrative Setup 3 District | Sub-district | Towns | Villages | Inhabited Villages | Uninhabited 11-18 Villages | Village Panchayat | Intermediate Panchayat Demographics 4 Population | Households | Rural/Urban Population -

District Level Nodal Officers

DISTRICT LEVEL NODAL OFFICERS Sl. SUBJECT TO BE NAME OF NODAL DESIGNATION AND MOBILE NO.OFFICE TEL No DEALT BY NODAL OFFICER OFFICE ADDRESS FAX EMAIL ID OFFICER 1. Manpower Sri Shivanand District Office Phone No. Management Gugawad Informatic 08352-276577 Officer, NIC Mobile No. Vijaypura 9448917021 2. EVM Sri Manjunath Joint Director M.no.8277930601 management B Agriculture Vijayapur Office Phone No. Sri. Shanakar Deputy Director 08352- 251261 of Land Records Mobile No. Vijayapur 9242117114 3. FLC for EVMs H.Prasanna, KAS Additional 08352-250479 and VVPATS Deputy Commissioner Vijayapur 4. Transport Sri Manjunath Regional Mobile : 9449864028 management Transport Officer Vijayapur 5. Training Sri Sindhur Deputy Director Office Phone No. management of Public 08352-250151 Instructions Mobile No. Vijayapur 9448999331 6. Material Sri Pranesh Deputy Director Office Phone No. management Jahagirdhar of Animal 08352- Husbandry Mobile No. Vijayapur 9341610816 7. Modal Code of Sri Sundaresh Chief Executive Mobile: 9480857000 Conduct Babu. IAS Officer Zilla Panchayat, Vijayapur 8. Election Sri. Gangadhar Principla Chief Mobile: 9449306438 Expenditure Accounts Officers Monitoring KBJNL Almatti. Sri Vikram Senior Audit Mobile: 9908605083 Naik Deputy Director Assistant Controller Local Audit Circle Vijayapura Sri M.M Mirja Chief Account Mobile: 9902353188 Officer Mahanagar Palike Vijayapur 9. SVEEP Sri Sundaresh Chief Executive Mobile: 9480857000 Babu. IAS Officer Zilla Panchayat, Vijayapur 10. Law and Order Sri. ASP Vijayapur Office Phone No. R.Shivakumar 08352- Gunari. KSPS Mobile No. 9916865069 11. Ballot Sri. Mahadev Project Director Office Phone No. paper/dummy Muragi. KAS DUDC Vijayapur 08352- 222988 ballot Mobile No. 8050408576 12. Media Sri. Nadaf District Mobile: 9449926128 Information and Publicity Officer, Vijayapur 13. -

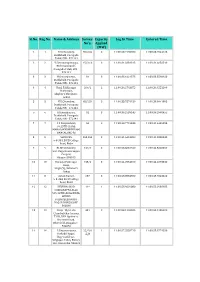

Sl.No. Reg.No. Name & Address Survey No's. Capacity Applied (MW

Sl.No. Reg.No. Name & Address Survey Capacity Log In Time Entered Time No's. Applied (MW) 1 1 H.V.Chowdary, 65/2,84 3 11:00:23.7195700 11:00:23.7544125 Doddahalli, Pavagada Taluk, PIN - 572141 2 2 Y.Satyanarayanappa, 15/2,16 3 11:00:31.3381315 11:00:31.6656510 Bheemunikunte, Pavagada Taluk, PIN - 572141 3 3 H.Ramanjaneya, 81 3 11:00:33.1021575 11:00:33.5590920 Doddahalli, Pavagada Taluk, PIN - 572141 4 4 Hanji Fakkirappa 209/2 2 11:00:36.2763875 11:00:36.4551190 Mariyappa, Shigli(V), Shirahatti, Gadag 5 5 H.V.Chowdary, 65/2,84 3 11:00:38.7876150 11:00:39.0641995 Doddahalli, Pavagada Taluk, PIN - 572141 6 6 H.Ramanjaneya, 81 3 11:00:39.2539145 11:00:39.2998455 Doddahalli, Pavagada Taluk, PIN - 572141 7 7 C S Nanjundaiah, 56 2 11:00:40.7716345 11:00:41.4406295 #6,15TH CROSS, MAHALAKHSMIPURAM, BANGALORE-86 8 8 SRINIVAS, 263,264 3 11:00:41.6413280 11:00:41.8300445 9-8-384, B.V.B College Road, Bidar 9 9 BLDE University, 139/1 3 11:00:23.8031920 11:00:42.5020350 Smt. Bagaramma Sajjan Campus, Bijapur-586103 10 10 Basappa Fakirappa 155/2 3 11:00:44.2554010 11:00:44.2873530 Hanji, Shigli (V), Shirahatti Gadag 11 11 Ashok Kumar, 287 3 11:00:48.8584860 11:00:48.9543420 9-8-384, B.V.B College Road, Bidar 12 12 DEVUBAI W/O 11* 1 11:00:53.9029080 11:00:55.2938185 SHARANAPPA ALLE, 549 12TH CROSS IDEAL HOMES RAJARAJESHWARI NAGAR BANGALORE 560098 13 13 Girija W/o Late 481 2 11:00:58.1295585 11:00:58.1285600 ChandraSekar kamma, T105, DNA Opulence, Borewell Road, Whitefield, Bangalore - 560066 14 14 P.Satyanarayana, 22/*/A 1 11:00:57.2558710 11:00:58.8774350 Seshadri Nagar, ¤ltĔ Bagewadi Post, Siriguppa Taluq, Bellary Dist, Karnataka-583121 Sl.No. -

KARNATAKA BANK LTD.Pdf

STATE DISTRICT BRANCH ADDRESS CENTRE IFSC CONTACT1 CONTACT2 CONTACT3 MICR_CODE D.NO.13-3-304,IST FLOOR THAKAI TOWERS,RAILWAY FEEDER ROAD, ananthapur ANDHRA ANANTAPUR, ANANTAPU 08554 @ktkbank.c PRADESH ANANTAPUR Ananthapur PIN=515001 R KARB0000025 244226 9573764578 om 515052002 17-3-632/4,IST FLOOR,JEELANI COMPLEX,K L hindupur@ ANDHRA ROAD,HINDUPUR, 08556 ktkbank.co PRADESH ANANTAPUR Hindupur, A.P. PIN=515201 HINDUPUR KARB0000327 222242 9440683098 m 515052102 5-172,GUPTA'S BUILDING,TUMKUR BELLARY madakasira ANDHRA ROAD,MADAKASIRA, MADAKASIR 08493 @ktkbank.c PRADESH ANANTAPUR Madakshira PIN=515301 A KARB0000489 288424 9440888424 om 515052662 13/256,KANCHANI COMPLEX,C-B tadapathri ANDHRA ROAD,TADPATRI, 08558 @ktkbank.c PRADESH ANANTAPUR Tadapatri, AP PIN=515411 TADPATRI KARB0000760 226988 9490180175 om 515052402 OPP.PUSHPANJALI TALKIES MADAKASIRA ANDHRA ROAD,AGALI., 08493 agali@ktkb PRADESH ANANTAPUR AGALI PIN=515311 AGALI KARB0000014 284827 9014244685 ank.com 515052663 FIRST FLOOR,BELLARY KANEKAL ROAD,KANEKAL(S.O) bommanah ANDHRA ,BOMMANAHAL BOMMANHA 08495 al@ktkbank PRADESH ANANTAPUR BOMMANHAL POST., PIN=515871 L KARB0000092 258721 9449595572 .com 515052562 E B S R COMPLEX,GROUND FLOOR,19-8- 85,RAYALA- CHERUVU ANDHRA ROAD,TIRUPATI, 0877 tirupati@ktk PRADESH CHITTOOR Tirupati PIN=517501 TIRUPATI KARB0000765 2241356 9989136599 bank.com 517052002 D.NO.42/199-7,NGO’S COLONY, R.T.C.BUS STAND ROAD, CUDDAPAH -516001 cuddapah ANDHRA CUDDAPAH DIST. 08562 @ktkbank.c PRADESH CUDDAPAH Cuddapah, A.P. , PIN=516001 CUDDAPAH KARB0000151 241782 9491060570 om 516052002 D NO 34-1-13,IST FLOOR,SRI KRISHNA KIRTHI COMPLEX,TEMPLE kakinada@ ANDHRA EAST STREET,KAKINADA, 0884 ktkbank.co PRADESH GODAVARI Kakinada , AP PIN=533001 KAKINADA KARB0000429 2340257 9866499454 m 533052002 DOOR NO.46-11- 31,OPP.TOBACO BOARD OFFICE,DANAVAIPET rajahmundr ANDHRA EAST A,RAJAHMUNDRY, RAJAHMUN 0883 y@ktkbank. -

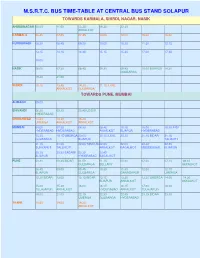

M.S.R.T.C. Bus Time-Table at Central Bus Stand Solapur

M.S.R.T.C. BUS TIME-TABLE AT CENTRAL BUS STAND SOLAPUR TOWARDS KARMALA, SHIRDI, NAGAR, NASIK AHMEDNAGAR 08.00 11.00 13.25 16.30 22.30 AKKALKOT KARMALA 06.45 07.00 07.45 10.00 12.00 15.30 16.00 KURDUWADI 08.30 08.45 09.20 10.00 10.30 11.30 12.15 13.15 14.15 14.45 15.15 15.30 17.00 17.45 18.00 NASIK 06.00 07.30 08.45 09.30 09.45 10.00 BIJAPUR 14.30 GULBARGA 19.30 21.00 SHIRDI 10.15 13.45 14.30 21.15 ILKAL AKKALKOT GULBARGA TOWARDS PUNE, MUMBAI ALIBAGH 09.00 BHIVANDI 06.30 09.30 20.45 UDGIR HYDERABAD CHINCHWAD 13.30 14.30 15.30 UMERGA AKKALKOT AKKALKOT MUMBAI 04.00 07.30 08.30 08.45 10.15 15.00 15.30 INDI HYDERABAD HYDERABAD AKKALKOT BIJAPUR HYDERABAD 15.30 19.15 UMERGA 20.00 20.15 ILKAL 20.30 21.15 BIDAR 21.15 GULBARGA BIJAPUR TALIKOTI 21.15 21.30 22.00 TANDUR 22.00 22.00 22.30 22.45 SURYAPET TALLIKOTI AKKALKOT BAGALKOT MUDDEBIHAL BIJAPUR 23.15 23.30 BADAMI 23.30 23.45 BIJAPUR HYDERABAD BAGALKOT PUNE 00.30 00.45 BIDAR 01.00 01.15 05.30 07.00 07.15 08.15 GULBARGA BELLARY AKKALKOT 08.45 09.00 09.45 10.30 11.30 12.00 12.15 BIJAPUR GULBARGA GANAGAPUR UMERGA 12.30 BIDAR 13.00 13.15 BIDAR 13.15 13.30 13.30 UMERGA 14.00 14.30 BIJAPUR AKKALKOT AKKALKOT 15.00 15.30 16.00 16.15 16.15 17.00 18.00 TULAJAPUR AKKALKOT HYDERABAD AKKALKOT TULAJAPUR 19.00 21.00 22.15 22.30 22.45 23.15 BIDAR 23.30 UMERGA GULBARGA HYDERABAD THANE 10.45 19.00 19.30 AKKALKOT TOWARDS AKKALKOT, GANAGAPUR, GULBARGA AKKALKOT 04.15 05.45 06.00 08.15 09.15 09.15 10.30 10.45 11.00 11.30 11.45 12.15 13.45 14.15 15.30 16.00 16.30 16.45 17.00 GULBARGA 02.00 PUNE 05.15 06.15 07.30 08.15 -

Census of India 2001 General Population Tables Karnataka

CENSUS OF INDIA 2001 GENERAL POPULATION TABLES KARNATAKA (Table A-1 to A-4) DIRECTORATE OF CENSUS OPERATIONS KARNATAKA Data Product Number 29-019-2001-Cen.Book (E) (ii) CONTENTS Page Preface v Acknowledgement Vll Figure at a Glance ]X Map relating to Administrative Divisions Xl SECTION -1 General Note 3 Census Concepts and Definitions 11-16 SECTION -2 Table A-I NUMBER OF VILLAGES, TOWNS, HOUSEHOLDS, POPULATION AND AREA Note 18 Diagram regarding Area and percentage to total Area State & District 2001 19 Map relating to Rural and Urban Population by Sex 2001 20 Map relating to Sex ratio 2001 21 Diagram regarding Area, India and States 2001 22 Diagram regarding Population, India and States 2001 23 Diagram regarding Population, State and Districts 2001 24 Map relating to Density of Population 25 Statements 27-68 Fly-Leaf 69 Table A-I (Part-I) 70- 82 Table A-I (Part-II) 83 - 98 Appendix A-I 99 -103 Annexure to Appendix A-I 104 Table A-2 : DECADAL VARIATION IN POPULATION SINCE 1901 Note 105 Statements 106 - 112 Fly-Leaf 113 Table A-2 114 - 120 Appendix A-2 121 - 122 Table A-3 : VILLAGES BY POPULATION SIZE CLASS Note 123 Statements 124 - 128 Fly-Leaf 129 Table A-3 130 - 149 Appendix A-3 150 - 154 (iii) Page Table A-4 TOWNS AND URBAN AGGLOMERATIONS CLASSIFIED BY POPULATION SIZE CLASS IN 2001 WITH VARIATION SINCE 1901 Note 155-156 Diagram regarding Growth of Urban Population showing percentage (1901-2001) 157- 158 Map showing Population of Towns in six size classes 2001 159 Map showing Urban Agglomerations 160 Statements 161-211 Alphabetical list of towns. -

Muddebihal Blk in Vijaypur SSA NOFN Works

Re-Tender for Trenching & Pipe Laying NOFN Project in Muddebihal BLK of Vijaypur SSA NIT. No.DET/OFP/BJP/NIT/XVII/2015-16/11 dated @ BJP the 13.08.2015 BHARAT SANCHAR NIGAM LIMITED (A GOVT. OF INDIA ENTERPRISE) OFFICE OF THE DIVISIONAL ENGINEER TELECOM OPTICAL FIBRE PROJECT DIVISION BIJAPUR PART-I QUALIFYING BID DOCUMENT Re-Tender for National Optical Fiber Network works in Muddebihal Blk in Vijaypur SSA NOFN Works SIGNATURE OF BIDDER 1 Re-Tender for Trenching & Pipe Laying NOFN Project in Muddebihal BLK of Vijaypur SSA NIT. No.DET/OFP/BJP/NIT/XVII/2015-16/11 dated @ BJP the 13.08.2015 TABLE OF CONTENTS Section Content Page No. QUALIFYING BID DOCUMENT (part-I) I Notice Inviting Tender 03 to 05 II Bid Form 06 III Bidder‟s Profile & Declaration 07 to 09 (part-II) IV Instruction to Bidders 11 to 19 V General (commercial) conditions of the contract 20 to 36 VI Special conditions of the contract 37 to 47 VII Scope of work and jurisdiction of Contract 48 to 49 VIII & IX OF Cable construction Specifications Manual 50 to 77 X Security Bond Form 78 to 79 XI Agreement 80 to 81 XII Letter of authorization for attending bid opening 82 XIII List of the documents to be submitted along with bid 83 XIV Rate of Empty Cable drums 84 SIGNATURE OF BIDDER 2 Re-Tender for Trenching & Pipe Laying NOFN Project in Muddebihal BLK of Vijaypur SSA NIT. No.DET/OFP/BJP/NIT/XVII/2015-16/11 dated @ BJP the 13.08.2015 BHARAT SANCHAR NIGAM LIMITED (A Government of India Enterprise) O/O. -

Environment Management Plan (EMP)

Karnataka Road Development Corporation Limited (A Government of Karnataka Enterprise) Design, Build, Finance, Operate, Maintain and Transfer (DBFOMT) of Existing State Highway Hungund – Muddebihal – Talikot in the state of Karnataka on DBFOMT Hybrid Annuity Basis (WCP-7) Environment Management Plan (EMP) Package No. : Road No. 7 - Hungund - Muddebihal -Talikota Employer : Karnataka Road Development Corporation Limited Concessionaire : Ashoka Hungund Talikot Road Limited Consultant : EGIS India Consulting Engineers Pvt.Ltd. EPC Contractor : Ashoka Hungund Talikot Road Limited R T Sateesha Babu SADASHIV BORADE ANIL SHIMPI KOTRESH Y.M DEVBRAT SINGH Rev.02 Prepared by Reviewed by Approved by Reviewed by Approved by Date Sadashiv Borade Anil Shimpi Projects In Independent IE 29thNovember HSE Officer Head-HSE charge Engineer (Env. Team Leder 2016 Concessionaire Concessionaire Concessionaire Specialist) Environment Management Plan (EMP)-Rev.2 Road No.7: Hungund - Muddebihal -Talikota Page 1 of 66 INDEX Sr. CHAPTER Page No. No. 1 BRIEF INTRODUCTION OF PROJECT 3 2 STATUTORY AND REGULATORY REQUIREMENTS 14 3 INSTITUTIONAL ARRANGEMENT 16 4 ENVIRONMENTAL MANAGEMENT PLAN AND REVIEW FRAMEWORK 23 5 ENVIRONMENTAL MANAGEMENT SYSTEM 36 ENVIRONMENTAL STIPULATION FROM THE COMPETENT AUTHORITY 6 SEIAA, MOEF, SPCB, FOREST DEPARTMENT AND CHECK LISTS OF 41 ENVIRONMENTAL REMIDIAL MEASURES 7 ENVIRONMENT MONITORING PLAN 42 8 HEALTH AND SAFETY 44 9 ENVIRONMENTAL REPORTING AND FREQUENCY 49 Tables: Table 1.4-1: Surface Water Resources along the Road Table 1.4-2: Ground/ -

Karnataka GIS City GIS Contents & Standards

CITY GIS STANDARDS VOLUME-I KARNATAKA STATE REMOTE SENSING APPLICATIONS CENTRE Dept. of Information Technology, Bio-Technology and Science & Technology “Doora Samvedi Bhavana”, Major Sandeep Unnikrishnan Road, Doddabettahalli, Bangalore- 560097. Ph No.: +91 80 29720557/58, Fax: +91 80 29720556 City GIS Contents & Standards – V 1.0 May- -2017 2 Contributors: Roopa Bhandiwad Chitra. R. N © Karnataka State Remote Sensing Applications Centre City GIS Contents & Standards – V 1.0 May- -2017 3 Document Control Sheet Document Number KSRSAC/K-GIS/STANDARDS/City GIS/volume 1 Title City GIS Contents & Standards Type of Document Technical Report Number of pages 86 Author(s) Roopa Bhandiwad Chitra. R. N Reviewed by Mission Director ,Chief Technical Officer & Technical Officer Approved by -- Abstract Karnataka State Remote Sensing and Application Centre is implementing Karnataka- GIS which envisions maintaining a State- wide, Standardized, seamless and most current GIS asset and providing GIS based decision support services for governance, private enterprise and citizen. In this connection a document on City GIS and its contents and standardization is prepared. Version Controlled by Roopa Bhandiwad Distribution Unrestricted Reproduction Rights This report and its contents are the property of KSRSAC under K-GIS City GIS Contents & Standards – V 1.0 May- -2017 4 This page is intentionally left blank City GIS Contents & Standards – V 1.0 May- -2017 5 Contents DOCUMENT CONTROL SHEET .................................................................................................... -

15/03/2021 Government of Karnataka Page:128 Department of Pre University Education List of Pu Colleges in Bijapur Distri

15/03/2021 GOVERNMENT OF KARNATAKA PAGE:128 DEPARTMENT OF PRE UNIVERSITY EDUCATION LIST OF PU COLLEGES IN BIJAPUR DISTRICT AS ON 15/03/2021 ******************************************************************************** SLNO COLCD NAME AND ADDRESS YEAR OF OPEN & COLL TYPE OPENING & AIDED GO NOS. WITH DATE ******************************************************************************** 1733 EE0001 SB ARTS & KCP SC PU COL 45-46 BIFUR PU COL SHOLAPUR ROAD BIJAPUR 586103 -------------------------------------------------------------------------------- 1734 EE0002 BLDEA'S NEW PU COLLEGE BIFUR PU COL UKKALI BASAVANBAGEWADI TQ BIJAPUR 586122 -------------------------------------------------------------------------------- 1735 EE0004 SECAB PU COL FOR WOMEN 72-73 AIDED PU COL 12 NAURASPUR BAGALKOT RD AFL CR-145 71-72 DT 03-06-1972 BIJAPUR 586101 PUE ACCTS E-3 GIA 72-73 19/03/1973 -------------------------------------------------------------------------------- 1736 EE0005 AS PATIL COMM PU COLLEGE 50-51 BIFUR PU COL SHOLAPUR ROAD BIJAPUR 586103 -------------------------------------------------------------------------------- 1737 EE0017 MGV CHINIWAR PU COLLEGE 68-69 BIFUR PU COL MUDDEBIHAL DCE OAG 31 68-69 DT 02-03-1972 BIJAPUR DT 586212 -------------------------------------------------------------------------------- 1738 EE0018 MH MEMORIAL PU COLLEGE AIDED PU COL ALMATTI DAMSITE BBWADI TQ BIJAPUR DT 586201 AFLR/736/71-72 DT 01/06/1971 -------------------------------------------------------------------------------- 1739 EE0021 PDJ PU COLLEGE 72-73 -

SENIOR CIVIL JUDGE and JMFC,INDI Hon

SENIOR CIVIL JUDGE AND JMFC,INDI Hon. Shri. ARAVIND SAIBANNA HAGARAGI SENIOR CIVIL JUDGE AND JMFC, INDI Cause List Date: 23-11-2020 Sr. No. Case Number Timing/Next Date Party Name Advocate 11.00 AM to 02.00 PM 1 O.S. 75/2019 Suresh Urf Suryakant S/o Y.S.Pujari (HEARING) Mahadev Halasangi IA/1/2019 Vs Gnagadhar S/o Chandram Halasangi 2 R.A. 13/2015 Ningappa So Prabhu Sarwad A.M.Biradar (ARGUMENTS) Vs Gunavati Wo Shashikant Metri 3 R.A. 29/2016 Shruti Wo Ramesh Sindagi S.S.Patil (ARGUMENTS) Vs IA/2/2016 Basavaraj So Mningappa S.V.Biradar IA/1/2016 Sindagi 4 R.A. 37/2016 Indirabai W/o Yallappa S P Patil (ARGUMENTS) Honnakatti IA/2/2016 Vs IA/1/2016 Revanasidda S/o Lagamanna Honnakatti 5 R.A. 51/2016 Ashok S/o Hanamant Alabagond I.S.Masali (ARGUMENTS) Vs IA/2/2016 Kamarati W/o Vithal Hugar Kulkarni Sameer Venkatesh 6 R.A. 49/2017 Uelappa S/o Sidalingappa S L (ARGUMENTS) Onkarashetti Nimbaragimath IA/1/2017 Vs Shivayogeppa S/o Sadashiva Onkarshetti 7 O.S. 62/2009 Nabeesab Gulekar S.G.Hattaraki (OBJECTION TO I.A) Vs Allabax Golekar I.S. Masali 8 O.S. 16/2015 Siddaram So Bhimaraya S.V.Kulkarni (CROSS EXAMINATION Hitanalli OF Vs PETITIONER/PLAINTIFF) Smt.Sonabai Wo Roopsingh IA/1/2015 Chavan 9 O.S. 90/2015 Shrishail So Shivalingappa S.G.Kulkarni (CROSS EXAMINATION Biradar, Ro.Ronihal, Tq- OF B.Bagewadi, Dist-Vijayapura PETITIONER/PLAINTIFF) Vs IA/1/2015 Hasandongrisab So Gaibusab Honyala, Ro.Kolhar, Tq- B.Bagewadi, Dist-Vijayapura 10 O.S.