View Annual Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

C:\Documents and Settings\All Users\Sean\Logos

C:\Documents and Settings\All Users\Sean\Logos 7 ELEVEN 1.eps 7 ELEVEN 2.eps 7UP 1.eps 7UP 2.eps 7UP CHERRY 1.eps 7UP CHERRY 2.eps 7UP DIET 1.eps 7UP DIET 2.eps 7UP DIET CHERR... 7UP DIET CHERR... S & H GREEN STA... SAA.eps SAAB AUTOMOBIL... SAAB AUTOMOBIL... SABENA AIR 1.eps SABENA AIR 2.eps SABENA WORLD ... SABRE BOATS.eps SACHS.eps SAFE PLACE.eps SAFECO.eps SAFEWAY 1.eps SAFEWAY 2.eps SAINSBURYS 1.eps SAINSBURYS 2.eps SAINSBURYS BAN... SAINSBURYS BAN... SAINSBURYS HO... SAINSBURYS HO... SAINSBURYS SAV... Page 1 C:\Documents and Settings\All Users\Sean\Logos SAINSBURYS SAV... SAKS 5TH AVENU... SAKS 5TH AVENU... SAKS 5TH AVENU... SALEM.eps SALOMON.eps SALON SELECTIV... SALTON.eps SALVATION ARMY... SAMS CLUB.eps SAMS NET.eps SAMS PUBLISHIN... SAMSONITE.eps SAMSUNG 1.eps SAMSUNG 2.eps SAN DIEGO STAT... SAN DIEGO UNIV ... SAN DIEGO UNIV ... SAN JOSE UNIV 1.... SAN JOSE UNIV 2.... SANDISK 1.eps SANDISK 2.eps SANFORD.eps SANKYO.eps SANSUI.eps SANYO.eps SAP.eps SARA LEE.eps SAS AIR 1.eps SAS AIR 2.eps Page 2 C:\Documents and Settings\All Users\Sean\Logos SASKATCHEWAN ... SASSOON.eps SAT MEX.eps SATELLITE DIREC... SATURDAY MATIN... SATURN 1.eps SATURN 2.eps SAUCONY.eps SAUDI AIR.eps SAVIN.eps SAW JAMMER PR... SBC COMMUNICA... SC JOHNSON WA... SCALA 1.eps SCALA 2.eps SCALES.eps SCCA.eps SCHLITZ BEER.eps SCHMIDT BEER.eps SCHWINN CYCLE... SCIFI CHANNEL.eps SCIOTS.eps SCO.eps SCORE INT'L.eps SCOTCH.eps SCOTIABANK 1.eps SCOTIABANK 2.eps SCOTT PAPER.eps SCOTT.eps SCOTTISH RITE 1... -

Quickar(PDF 8.49

7 September 2017 The Secretary, Economy and Infrastructure Committee Parliament House, Spring Street EAST MELBOURNE VIC 3002 Dear Secretary, Please accept this cover letter and attached report as a submission to the Committee’s Inquiry into Electric Vehicles. A mushrooming of Melbourne’s population over the next 20 years combined with the phenomena of significant population detachment from economic hubs driven by growing rates of car ownership and burgeoning investment by government in private car driver-driven infrastructure is a looming urban mobility crisis. We risk sleepwalking into a situation where our once “world’s most livable city” has insufficient public transport, overloaded infrastructures, a default logarithmic expansion of motorised means of transport, a vast rise in air and noise pollution and CO2 emissions, a concomitant parking capacity problem and increasing disparity in the social equity standards between communities of very near proximity. What should the Victorian Government do? The attached report assesses the opportunity for Free Floating Car Sharing in Zero Emission urban transport. This report concludes that Free Floating Car Sharing is an innovative technology with a smart operating model that improves cities. It offers cities a no-cost, scaleable transport alternative to supplement existing transport systems and reduce inner urban vehicle congestion. Moreover, Free Floating Car Sharing offers Melbourne’s best opportunity for a definitive, practical and evolutionary pathway into a sustainable Zero Emission urban mobility future through the accelerated uptake of Electric Vehicles. Quickar Pty Ltd (ABN 99 611 879 513) Melbourne, 3000 Victoria, Australia Page 1 of 66 In light of these conclusions, the Victorian Government should: • Enable Free Floating Car Sharing. -

The Future of Car Ownership August 2017 About the NRMA

Future mobility series The future of car ownership August 2017 About the NRMA Better road and transport infrastructure has been a core focus of the NRMA since 1920 when our founders lobbied for improvements to the condition of Parramatta Road in Sydney. Independent advocacy was our foundation activity, and it remains critical to who we are as we approach our first centenary. We’ve grown to represent over 2.4 million Australians, principally from New South Wales and the Australian Capital Territory. We provide motoring, mobility and tourism services to our Members and the community. Today, we work with policy makers and industry leaders, advocating for increased investment in road infrastructure and transport solutions to make mobility safer, provide access for all, and deliver sustainable communities. By working together with all levels of government to deliver integrated transport options, we give motorists real choice about how they get around. We firmly believe that integrated transport networks, including efficient roads, high-quality public transport and improved facilities for cyclists and pedestrians, are essential in addressing the challenge of growing congestion and providing for the future growth of our communities. The NRMA acknowledges the work of Sam Rutherford on this report. Comments and queries Ms Carlita Warren Senior Manager – Public Policy and Research NRMA PO Box 1026, Strathfield NSW 2135 Email: [email protected] Web: mynrma.com.au Cover Image: nadla – Getty Images Contents Executive summary 2 Challenges -

Women in the Redex Around Australia Reliability Trials of the 1950S

University of Wollongong Research Online Faculty of Arts - Papers (Archive) Faculty of Arts, Social Sciences & Humanities 1-1-2011 The flip side: women in the Redex Around Australia Reliability Trials of the 1950s Georgine W. Clarsen University of Wollongong, [email protected] Follow this and additional works at: https://ro.uow.edu.au/artspapers Part of the Arts and Humanities Commons, and the Social and Behavioral Sciences Commons Recommended Citation Clarsen, Georgine W., The flip side: women in the Redex Around Australia Reliability Trials of the 1950s 2011, 17-36. https://ro.uow.edu.au/artspapers/1166 Research Online is the open access institutional repository for the University of Wollongong. For further information contact the UOW Library: [email protected] The Flip Side: Women on the Redex Around Australia Reliability trials of the 1950s Georgine Clarsen In August 1953 almost 200 cars set off from the Sydney Showgrounds in what popular motoring histories have called the biggest, toughest, most ambitious, demanding, ‘no-holds-barred’ race, which ‘caught the public imagination’ and ‘fuelled the nation with excitement’.1 It was the first Redex Around Australia Reliability Trial and organisers claimed it would be more testing than the famous Monte Carlo Rally through Europe and was the longest and most challenging motoring event since the New York-to-Paris race of 1908.2 That 1953 field circuited the eastern half of the continent, travelling north via Brisbane, Mt Isa and Darwin, passing through Alice Springs to Adelaide and returning to the start point in Sydney via Melbourne. Two Redex trials followed, in 1954 and 1955, and each was longer and more demanding than the one before. -

For Personal Use Only Use Personal For

Caltex Australia Limited Australia Caltex 2018 Annual Report Annual 2018 2018 Annual Report Capability Scale For personal use only FUELS & INFRASTRUCTURE International sourcing and supply 0700 HRS Kurnell Fuel Import Terminal Caltex Australia Limited 2018 Annual Report Caltex Supply Chain 2 Refining 3 Integrated Australian fuel supply chain 5 Retail fuel and convenience 7 Network of Assets 8 2018 Highlights 10 Message from the Chairman and the Managing Director & CEO 12 Operations Reports 16 Fuels & Infrastructure 17 Convenience Retail 21 Our people taking us further 25 Our approach to sustainability 29 2018 Financial Report 33 On the Cover Ampol is Caltex’s international trading and shipping team based in Singapore. It sources petroleum products from global markets and connects their supply chains with our market leading infrastructure positions, such as our import terminal in Kurnell, New South Wales (pictured). This international supply capability underpins Caltex’s reputation for reliable supply to wholesale customers, while ensuring the competitiveness of our refining and retail operations. Ampol also manages supply to our first international acquisition, Gull New Zealand, our partner Seaoil in the Philippines, in which Caltex holds a 20% equity interest, and our other international wholesale customers. About this Report This 2018 Annual Report for Caltex Australia LimitedFor personal use only (ACN 004 201 307) has been prepared as at 26 February 2019. Please note that terms such as Caltex and Caltex Australia have the same meaning as Caltex Group, unless the context requires otherwise. An interactive version of the Annual Report is available on our website. Visit www.caltex.com.au to download or view a copy. -

Car Sharing in the Byron Shire

Car Sharing in the Byron Shire Purpose: • To investigate the different types of car sharing models available in Australia and how they work. • To explore the potential for car sharing to alleviate car parking and traffic issues, reduce emissions and provide a more affordable transport option for the Byron Shire community. • Ascertain whether Council can participate in car sharing as an alternative to traditional fleet leasing arrangements, or in conjunction with these. Objectives: 1. Demonstrate leadership – contribute to Council and community behaviour changes about sustainable transport. 2. Introduce an alternative option to developers for site development including an option for no parking to deliver better design outcomes for sustainability. 3. Reduce on-street parking demand in the Shire. 4. Reduce traffic (even minimally) – relieve congestion and improve air quality, and the pedestrian environment. 5. Explore the use of car sharing for Council and whether it could compliment the traditional fleet leasing model (delivering on emissions reductions and cost efficiencies). 6. Encouragement of more sustainable models of transport for both locals and visitors in line with emissions reduction objectives. 7. Another transport option for locals that may deliver greater affordability, flexibility and environmental value for residents. Strategic links: Community Strategic Plan 2022 Council Resolution 17-005 Resolved that Council note the report Byron Bay Town Centre Local Environmental Plan and Development Control Plan controls review (Richardson/Hunter). -

2021 Shannons Autumn Timed Auction Results

2021 SHANNONS AUTUMN TIMED AUCTION RESULTS Please note: All prices listed are in Australian Dollars (AUD). Prices do not include the 5% buyers premium. LOT DESCRIPTION PRICE 1 TRICYCLE - c1950's Childs Cyclops Style Trike $435 2 DECANTER - set of 3 Grand Prix International Grill decanters - Ford, Mercedes, Jaguar ( 20.5 x 13cm) $405 3 BADGE BOARD - Assorted Veteran, Vintage & Classic Rally Badges Qty - 73 $850 4 OIL TINS ASSORTED - (1 x Caltex, 2 x Ampol) $300 5 4 x Assorted Small Oil Cans ( Castrol, Ampol, Bardahl, Laurel Kerosene) $200 6 PETROL TINS - 6 x Tins: Esso,Wakefield, Duckhams, Ampol, Plume, Lockheed $400 7 HI BOY - Castrol Highboy with pump Restored $680 8 HI BOY - SHELL Livery (Unrestored) $510 9 LUBE STAND - Shell Lubrications Guide on stand $600 10 Glass Barbershop Sign - Gents Hairdressing (45 x 110cm) $200 11 Railway Lamp $451 12 MOVIE POSTERS - Framed Mad Max One & Mad Max 2 Movie Posters (107 x 74cm) $1,450 13 PICNIC RADIO - Air Chief MN-CBE with Adaptor Fits EJ / EH Holden NACSO accessory $301 14 ENAMEL SIGN - Peter's Ice Cream Sign - Single sided Original (183 x 45cm) $1,350 15 RECORD PLAYER - ARC1000 Under Dash 12 Stacker Car Record Player for 45's - Universal $1,201 16 FRAMED BANNER - Vintage Texaco Calico Banner $200 17 GOLDEN FLEECE Aluminium Ram $800 18 CAST IRON - Michelin Man (58 x 12 wide) $2,100 19 LIGHT BOX - AMPOL PRODUCTS BAR $550 20 ENAMEL SIGN - Authorised Stockist of Perkins Diesel Spare Parts Sign (48 x 31 cm ) $1,500 21 ENAMEL SIGN - Ford Sales & Service Double sided - Original (76 x 30.5 cm) $2,200 22 SIGNS - Castrol Wakefield in enamel (Single Sided) & Castrol Masterpiece in Tin (Single sided) (76 x 30.5cm) $952 SCALEXTRICS SET VINTAGE - Slot Car Set Scale 1:25 with extra track in box, made in England (2amp) and power unit . -

EVC-State-Of-Evs-2020-Report.Pdf

STATE OF ELECTRIC VEHICLES AUGUST 2020 electricvehiclecouncil.com.au STATE OF ELECTRIC VEHICLES AUGUST 2020 electricvehiclecouncil.com.au 06 2020 HIGHLIGHTS 09 EXECUTIVE SUMMARY CONTENTS 13 CHAPTER 1: MARKET UPDATE 13 Electric vehicle sales 14 COVID-19 15 Consumer attitudes survey 22 Case study: Lane Cove development building now for the electrified future 24 CHAPTER 2: AUSTRALIA'S EV INDUSTRY 24 Passenger vehicles 28 Bikes and scooter 29 Commercial vehicles and buses 36 Case study: East waste makes haste, leading the way on electric garbage 38 CHAPTER 3: CHARGING INFRASTRUCTURE 38 Public charging 42 Home and workplace charging 44 Case study: Evie Networks, the Aussie company building a nation-wide ultra-fast charging network 46 CHAPTER 4: EV MINING AND MANUFACTURING 46 Battery value chain 51 Charger manufacturing 52 Electric vehicle manufacturing 58 Case study: Voltra and BHP break new ground underground CHAPTER 5: EVS, THE ENVIRONMENT, 60 AND THE ENERGY GRID 60 Emissions impact 61 Battery stewardship 64 Built environment 67 Integration with the grid 72 Case study: Realising electric vehicle-to-grid services CHAPTER 2: AUSTRALIA'S EV INDUSTRY 74 CHAPTER 6: EV POLICY 75 Policy progress and scorecard 77 Policy highlights 80 APPENDIX 80 Appendix 1: Carmakers' commitments to electric vehicles 84 Appendix 2: Electric vehicle model availability 90 Appendix 3: Carmakers' investments into secondary battery applications 90 Appendix 4: Bus partnerships in Australia 93 REFERENCES 6 ELECTRIC VEHICLE COUNCIL 2020 highlights In 2019, EV sales increased -

Dynamic Asset Allocation Balanced Fund Q3 Portfolio Holdings

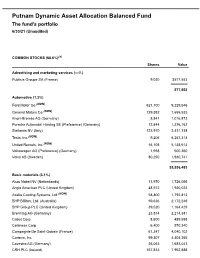

Putnam Dynamic Asset Allocation Balanced Fund The fund's portfolio 6/30/21 (Unaudited) COMMON STOCKS (68.6%)(a) Shares Value Advertising and marketing services (—%) Publicis Groupe SA (France) 9,030 $577,553 577,553 Automotive (1.3%) Ford Motor Co.(NON) 621,100 9,229,546 General Motors Co.(NON) 129,382 7,655,533 Knorr-Bremse AG (Germany) 8,841 1,016,872 Porsche Automobil Holding SE (Preference) (Germany) 12,844 1,376,162 Stellantis NV (Italy) 123,970 2,431,338 Tesla, Inc.(NON) 9,206 6,257,318 United Rentals, Inc.(NON) 16,108 5,138,613 Volkswagen AG (Preference) (Germany) 1,998 500,360 Volvo AB (Sweden) 80,250 1,930,741 35,536,483 Basic materials (3.1%) Akzo Nobel NV (Netherlands) 13,970 1,726,066 Anglo American PLC (United Kingdom) 48,572 1,930,023 Axalta Coating Systems, Ltd.(NON) 58,800 1,792,812 BHP Billiton, Ltd. (Australia) 59,636 2,172,246 BHP Group PLC (United Kingdom) 39,520 1,164,429 Brenntag AG (Germany) 23,814 2,214,381 Cabot Corp. 8,600 489,598 Celanese Corp. 6,400 970,240 Compagnie De Saint-Gobain (France) 61,347 4,040,102 Corteva, Inc. 99,307 4,404,265 Covestro AG (Germany) 26,063 1,683,043 CRH PLC (Ireland) 157,813 7,952,888 Dow, Inc. 93,022 5,886,432 DuPont de Nemours, Inc. 130,372 10,092,097 Eastman Chemical Co. 21,500 2,510,125 Eiffage SA (France) 8,245 838,825 FMC Corp. 4,000 432,800 Fortescue Metals Group, Ltd. -

Lot# Description Qty Bid Amount 1 New Pegasus Neon Light up Sign (Working) 1100 X 800 1 130.00

Lot# Description Qty Bid Amount 1 New Pegasus Neon Light Up Sign (Working) 1100 x 800 1 130.00 2 New Pegasus Neon Light Up Sign (Working) 1100 x 800 1 100.00 3 2 x Modern Tin Shell Signs 550 x 390 1 70.00 4 2 x Modern Shell Tin Signs 350 x 520 1 100.00 5 Modern GTS Monaro Tin Sign 650 x 600 1 80.00 6 Modern Golden Fleece Tin Sign 730 x 400 1 70.00 7 Modern Shell Tin Sign 360 x 460 1 40.00 8 Modern Golden Fleece Tin Sign 300 x 470 1 50.00 9 2 x Modern Tin Signs Falcon and Valiant 600 x 400 1 30.00 10 Modern Tin Buick sign 600 x 300 1 15.00 11 Modern Tin Kombi sign 600 x 400 1 20.00 12 Modern Tin Atlantic Sign 550 x 430 1 60.00 13 Modern Tin Caltex Sign 390 x 570 1 50.00 14 Modern Tin Garage Sign 500 x 250 1 30.00 15 2 x Modern Tin Motor Bike Signs 440 x 300 1 30.00 16 Modern Tin Muscle Car Garage Sign 600 x 400 1 90.00 17 Modern Tin Garage Sign 600 x 400 1 40.00 18 Modern Tin Garage Local Dealer Sign 600 x 400 1 30.00 19 Castrol Tin Sign Reproduction 400mm 1 30.00 20 2 X Enamel Signs Golden Fleece & Red Indian 240mm Reproduction 1 100.00 21 2 x Enamel Signs inc Globe & Musgo 300mm Reproduction 1 100.00 22 Modern Tin Sign WB Ute 600 x 400 1 50.00 23 Modern Tin Sign FC Holden 600 x 400 1 50.00 24 Modern Tin Sign Torana 600 x 400 1 50.00 25 Modern Tin Sign Shell Motor Oil 600 x 400 1 40.00 26 Modern Shell Tin Sign EH Holden 600 x 400 1 40.00 27 Modern Tin Sign Shell Petrol and Oil 600 x 400 1 50.00 28 2 x Reproduction Tin and Enamel Signs inc Texaco and Mobilgas 320 x 400 1 30.00 29 2 x Modern Shell Tin Signs 600 x 400 1 110.00 30 Modern Tin -

Feature Petrol, Oil, Advertising & Collectable

FEATURE PETROL, OIL, ADVERTISING & COLLECTABLE SALE RESULTS LOT # DESCRIPTION PRICE SOLD ($) 1 Grease Pump $30.00 2 AMPOL 4 Gallon Kerosene Drum $80.00 3 Wakefield Castrol 4 Gallon tin $200.00 4 Shell Blue Pennant Kerosene 4 Gallon tin $85.00 5 Mobilube GX 140 4 Gallon tin $90.00 6 AMPOL Home Kerosene 4 Gallon tin $175.00 7 AMPOL Home Kerosene 4 Gallon tin $85.00 8 NEPTUNE 1 Gallon tin $100.00 9 MOBILGAS and MOBILGAS Mower Fuel Can 1 Gallon $100.00 10 AMPOL 1 Gallon tin $50.00 11 AMPOL 1 Gallon tin $100.00 12 AMPOL 1 Gallon tin $110.00 13 2 x Caltex 1 Gallon tins $90.00 14 Golden Fleece 45lb Grease Tin $180.00 15 Golden Fleece 5 Gallon drum $125.00 16 Golden Fleece Supreme 5 Gallon drum $700.00 17 Golden Fleece 4 Gallon drum $300.00 18 Golden Fleece 4 Gallon drum $200.00 19 Texaco box $60.00 20 Texaco box $80.00 21 Texaco Box $60.00 22 Texaco Box $70.00 23 Golden Fleece box $180.00 24 2 x Shell running board tins $90.00 25 Golden Fleece running board tin $200.00 26 Big Tree Running board tin $110.00 27 Shell Running board tin $85.00 LOT # DESCRIPTION PRICE SOLD ($) 28 Golden Fleece 1 Gallon tin $100.00 29 Shell 1 Gallon tin $130.00 30 Shell 1 Gallon tin $150.00 31 Texaco 1 Gallon tin $150.00 32 3 x Shell tins Litres and Gallon $130.00 33 Neptune 4 Gallon drum $250.00 34 Caltex RPM 4 Gallon drum $75.00 35 AMPOL 4 Gallon drum $95.00 36 SHELL 4 Gallon drum $100.00 37 Laurel and Texaco box $120.00 38 Laurel box $250.00 39 Texaco box $35.00 40 Texaco box $50.00 41 Laurel box $300.00 42 Energol Bread bin inc 3 x hi-boys $875.00 43 Golden Fleece Bread bin inc 3 hi-boys $850.00 44 BP Motor Spirit running board tin $40.00 45 Shell running board tin $75.00 46 Mobil oil Running board tin $90.00 47 Esso Running board tin $150.00 48 Shelltox sprayer and oil can $40.00 49 2 x tins $30.00 50 Lister Sepoyle 1 Gallon tin $40.00 51 Golden Fleece 5 liter plastic $30.00 52 TOTAL and PENNZOIL 1 Gallon tins $45.00 53 2 x AMPOL Grease tins. -

The Collaborative Economy: Products, Services, and Market Relationships Have Changed As Sharing Startups Impact Business Models

A Market Definition Report The Collaborative Economy: Products, services, and market relationships have changed as sharing startups impact business models. To avoid disruption, companies must adopt the Collaborative Economy Value Chain. Altimeter Research Theme: Digital Economies June 4, 2013 By Jeremiah Owyang With Christine Tran and Chris Silva Includes input from 69 ecosystem contributors Executive Summary The Next Phase of Social Business Is the Collaborative Economy. Social technologies radically disrupted communications, marketing, and customer care. With these same technologies, customers now buy products once and share them with each other. Beyond business functions, the Collaborative Economy impacts core business models. Customers Are Sharing Goods and Services — Redefining the Buyer-Seller Relationship. Every car-sharing vehicle reduces car ownership by 9-13 vehicles; a revenue loss of at least $270,000 to an average auto manufacturer.1 The cascading impact to the ecosystem has far-reaching impacts to auto loans, car insurance, fuel, auto parts, and other services.2 For corporations, the direct impact is revenue loss that results from customers sharing products and services with each other. Innovative Companies Are Already Moving Into Collaborative Economy. Some companies have joined this movement. For instance, Toyota rents cars from dealership lots, and Patagonia partnered with eBay to encourage customers to buy and sell its used products. NBC has partnered with Yerdle, a startup founded by former Walmart executives to foster peer-to-peer sharing. This movement impacts every industry. Adopt the Collaborative Economy Value Chain. Companies risk becoming disintermediated by customers who connect with each other. The Collaborative Economy Value Chain illustrates how companies can rethink their business models by becoming a Company-as-a-Service, Motivating a Marketplace, or Providing a Platform.