Assessment of Capital and Operating Expenditure Final

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Seqwater's 22 October Submission / Response To

SEQWATER’S 22 OCTOBER SUBMISSION / RESPONSE TO QCA REQUEST OF 12 OCTOBER 12 October 2012 I hereby provide Seqwater with a further information request. Seqwater’s detailed responses to each item would be appreciated by COB 19 October 2012, please. Happy to discuss at any time noting the proposed due date of COB 19 October 2012 From: Colin Nicolson [mailto:[email protected]] Sent: Friday, 19 October 2012 1:10 PM To: Angus MacDonald Cc: George Passmore; Damian Scholz Subject: FW: Information Request 12 October 2012 Hello Angus Here are our responses to the above information request. QCA Question 1 - Cedar Pocket Stakeholders (Issues Arising (IA) Cedar Pocket 2012) submitted that more details were required regarding Seqwater’s proposed renewals expenditure [outlined in the NSP] on “electricity supply assets” in 2025-26 at $30,000. Please provide more details regarding this proposed expenditure. Seqwater Response to Item 1 The Assets in question are a property pole, meter box (excluding the meters), cabling and a distribution board. The renewal is scheduled based on the Seqwater “standard asset life” of 20 years for this type of equipment. It was installed in 2005 and will be 20 years old when the work is scheduled. The cost estimate is drawn from the estimated replacement costs as set out in Section 5.2.2 and Section 9 of the Irrigation Infrastructure Renewal Projections - 2013/14 to 2046/47 Report on Methodology. The renewal timing, will be reviewed on an ongoing basis so that it is only delivered when condition warrants. The scope and cost estimate will be reviewed prior to commencement of work to ensure the delivery is efficient. -

Cedar Pocket Water Supply Scheme Annual Network Service Plan

Cedar Pocket Water Supply Scheme Annual Network Service Plan December 2013 Contents 1. Introduction ............................................................................................................................ 3 2. Scheme Details ...................................................................................................................... 3 2.1 Scheme background and context ............................................................................................ 3 2.2 Infrastructure details ................................................................................................................ 3 2.3 Customers and water entitlements serviced ........................................................................... 4 2.4 Water availability and use ........................................................................................................ 4 2.5 Water trading ........................................................................................................................... 5 2.6 Irrigation Customer Consultation ............................................................................................. 5 2.7 Customer service standards .................................................................................................... 5 3. Financial Performance .......................................................................................................... 5 3.1 Tariffs ...................................................................................................................................... -

Water for Life

SQWQ.001.002.0382 • se a er WATER FOR LIFE • Strategic Plan 2010-11 to 2014-15 Queensland Bulk Water Supply Authority (QBWSA) trading as Seqwater 1 SQWQ.001.002.0383 2010-11 to 2014-15 Strategic Plan Contents Foreword ........................................................................................................................................................... 3 Regional Water Grid ......................................................................................................................................... 4 . Seqwater's vision and mission ......................................................................................................................... 5 Our strategic planning framework ................................................................................................................... 5 Emerging strategic issues ................................................................................................................................ 7 Seqwater's goals and strategy for 2010-11 to 2014-15 ................................................................................... 8 • Budget outlook............................................................................................................................................... 10 Strategic performance management ................................................................................................................. 11 Key Performance Indicators .......................................................................................................................... -

Lower Lockyer Valley Water Supply Scheme Annual Network Service Plan

Lower Lockyer Valley Water Supply Scheme Annual Network Service Plan December 2013 Contents 1. Introduction ............................................................................................................................ 3 2. Scheme Details ...................................................................................................................... 3 2.1 Scheme background and context ............................................................................................ 3 2.2 Infrastructure details ................................................................................................................ 3 2.3 Customers and water entitlements serviced ........................................................................... 4 2.4 Water availability and use ........................................................................................................ 4 2.5 Water trading ........................................................................................................................... 5 2.6 Irrigation Customer Consultation ............................................................................................. 5 2.7 Customer service standards .................................................................................................... 6 3. Financial Performance .......................................................................................................... 6 3.1 Tariffs ...................................................................................................................................... -

Water for South East Queensland: Planning for Our Future ANNUAL REPORT 2020 This Report Is a Collaborative Effort by the Following Partners

Water for South East Queensland: Planning for our future ANNUAL REPORT 2020 This report is a collaborative effort by the following partners: CITY OF LOGAN Logo guidelines Logo formats 2.1 LOGO FORMATS 2.1.1 Primary logo Horizontal version The full colour, horizontal version of our logo is the preferred option across all Urban Utilities communications where a white background is used. The horizontal version is the preferred format, however due to design, space and layout restrictions, the vertical version can be used. Our logo needs to be produced from electronic files and should never be altered, redrawn or modified in any way. Clear space guidelines are to be followed at all times. In all cases, our logo needs to appear clearly and consistently. Minimum size 2.1.2 Primary logo minimum size Minimum size specifications ensure the Urban Utilities logo is reproduced effectively at a small size. The minimum size for the logo in a horizontal format is 50mm. Minimum size is defined by the width of our logo and size specifications need to be adhered to at all times. 50mm Urban Utilities Brand Guidelines 5 The SEQ Water Service Provider Partners work together to provide essential water and sewerage services now and into the future. 2 SEQ WATER SERVICE PROVIDERS PARTNERSHIP FOREWORD Water for SEQ – a simple In 2018, the SEQ Water Service Providers made a strategic and ambitious statement that represents decision to set out on a five-year journey to prepare a holistic and integrated a major milestone for the plan for water cycle management in South East Queensland (SEQ) titled “Water region. -

Lin-Et-Al-2018.Pdf

Received: 20 February 2017 Revised: 13 July 2017 Accepted: 17 July 2017 DOI: 10.1002/aqc.2831 RESEARCH ARTICLE Impacts of fishing, river flow and connectivity loss on the conservation of a migratory fish population Hsien‐Yung Lin1 | Christopher J. Brown2 | Ross G. Dwyer3 | Doug J. Harding4 | David T. Roberts5 | Richard A. Fuller1 | Simon Linke2 | Hugh P. Possingham1 1 Centre for Biodiversity and Conservation Science, School of Biological Sciences, The Abstract University of Queensland, St Lucia, QLD, 1. Migratory species depend on connected habitats and appropriate migratory cues to complete Australia their life cycles. Diadromous fish exemplify species with migratory life cycles by moving 2 The Australian Rivers Institute, Griffith between connected freshwater and saltwater habitats to reproduce. However, migration University, Nathan, QLD, Australia increases the exposure of fish to multiple threats and it is critical that managers integrate hab- 3 School of Biological Sciences, The University itat connectivity into resource management and conservation. of Queensland, St Lucia, QLD, Australia 4 Department of Natural Resources and Mines, 2. The benefit of alternative management actions was assessed for a diadromous fish, the Landcentre, Woolloongabba, Australia Australian bass Percalates novemaculeata, using a spatio‐temporal population model informed 5 Seqwater, Ipswich, QLD, Australia by individual‐based movement data. The management actions comprise seasonal closures Correspondence during the spawning season, and controlling fishing pressure by limiting catch or effort. Hsien‐Yung Lin, Centre for Biodiversity and Conservation Science, School of Biological 3. The benefits of implementing seasonal closures depend upon interactions among how fishing Sciences, The University of Queensland, St pressure is controlled, the response of anglers to fishery regulations and river flow regimes. -

Irrigation Infrastructure Renewal Projections - 2013/14 to 2046/47 Report - Cedar Pocket Tariff Group

Irrigation Infrastructure Renewal Projections - 2013/14 to 2046/47 Report - Cedar Pocket Tariff Group September 2012 Irrigation Infrastructure Renewal Projections - 2013/14 to 2046/47 Report - Cedar Pocket Tariff Group © Queensland Bulk Water Authority 2012 This document is and shall remain the property of Queensland Bulk Water Authority. The document may only be used for the purposes for which it was prepared. Unauthorised use of this document in any form whatsoever is prohibited. Document Status Version Date Author Reviewed PCG Approval 1 20/4/12 AL/GH MD 2 23/4/12 GH MD 3 19/9/12 GH MD Filename: Seqwater_IrrigRen_Tarrif Group Summary_CedarPkt_Ver 3_Sept12 Irrigation Infrastructure Renewal Projections - 2013/14 to 2046/47 Report - Cedar Pocket Tariff Group Contents 1. Introduction 4 2. Asset Information 5 2.1 Irrigation Infrastructure 5 2.2 Relevant Asset Information 5 3. Projections 6 3.1 Summary 6 3.2 Significant Projects 6 3.3 Additional Commentary 8 Table Index Table 1 Summary of Irrigation Infrastructure 5 Table 2 Significant Projects 6 Table 3 Summary of Renewal Projections 7 Appendices A Water Supply Scheme Schematic B Renewal Projections Filename: Seqwater_IrrigRen_Tarrif Group Summary_CedarPkt_Ver 3_Sept12 Irrigation Infrastructure Renewal Projections - 2013/14 to 2046/47 Report - Cedar Pocket Tariff Group 1. Introduction Seqwater owns and operates the following seven irrigation schemes: Central Lockyer WSS; Lower Lockyer WSS; Logan River WSS; Mary River WSS; Cedar Pocket WSS; Warrill Valley WSS; and Central-Brisbane WSS. Seqwater also owns and operates a distribution system, the Morton Vale Pipeline. There are nine tariff groups associated with these schemes. To assist with the determination of price paths, a forecast of future renewal expenditure is required at the individual tariff group level. -

Lockyer Water Users Forum Inc

lockyer water LWUF users forum Lockyer Water Users Forum Inc. P.O. Box 77 Gatton Qld 4343 Chair Queensland Competition Authority GPO Box 2257 Brisbane Qld 4001 28th November 2018 Dear Sir, RE: CENTRAL AND LOWER LOCK.YER IRRIGATORS SUBMISSION UNDER SECTION 23 OF THE QUEENSLAND COMPETITION AUTHORITY ACT 1997 PRICE PATH PERIOD 2020-2024 This submission is on behalf of the Lockyer Valley Irrigators in the following water supply schemes constructed and owned by the State of Queensland and operated by SEQW being: • Atkinson Dam • Lake Clarendon • Mortonvale Pipeline • Bill Gunn Dam This submission is in regard to the yet to be introduced 4 year price path (2020 - 2024) and seeks to address maters of fact in the continual underlying poor performance of the schemes and argues that new policy is required when formulating a price path for schemes that will never be able to reach cost recovery or breakeven. Lockyer Valley Irrigators will also be providing a response when the Commission calls for submissions on the SEQW prici,ng proposals for the four years from July 2019 Current Situation: SEQW has advised customers under the pricing principles expected to be implemented by the QCA that the next price path will include the introduction of Part A (fixed cost) and Part B (variable cost) groundwater pricing for Central Lockyer Water Supply Schemes and that will result in the water charges being split at 95% Part A and 5% Part B. Mortonvale Pipeline Users will in addition pay Part C and Part D charges on the pipeline. The introduction of fixed Part A charges will occur with the introduction of water allocations in the Central Lockyer. -

Strategic Framework December 2019 CS9570 12/19

Department of Natural Resources, Mines and Energy Queensland bulk water opportunities statement Part A – Strategic framework December 2019 CS9570 12/19 Front cover image: Chinaman Creek Dam Back cover image: Copperlode Falls Dam © State of Queensland, 2019 The Queensland Government supports and encourages the dissemination and exchange of its information. The copyright in this publication is licensed under a Creative Commons Attribution 4.0 International (CC BY 4.0) licence. Under this licence you are free, without having to seek our permission, to use this publication in accordance with the licence terms. You must keep intact the copyright notice and attribute the State of Queensland as the source of the publication. For more information on this licence, visit https://creativecommons.org/licenses/by/4.0/. The information contained herein is subject to change without notice. The Queensland Government shall not be liable for technical or other errors or omissions contained herein. The reader/user accepts all risks and responsibility for losses, damages, costs and other consequences resulting directly or indirectly from using this information. Hinze Dam Queensland bulk water opportunities statement Contents Figures, insets and tables .....................................................................iv 1. Introduction .............................................................................1 1.1 Purpose 1 1.2 Context 1 1.3 Current scope 2 1.4 Objectives and principles 3 1.5 Objectives 3 1.6 Principles guiding Queensland Government investment 5 1.7 Summary of initiatives 9 2. Background and current considerations ....................................................11 2.1 History of bulk water in Queensland 11 2.2 Current policy environment 12 2.3 Planning complexity 13 2.4 Drivers of bulk water use 13 3. -

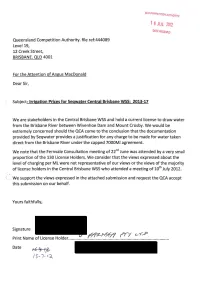

L Z012 Oalt Aegavcd

t 6 JUL Z012 OAlt AEGavcD Queensland Competition Authority. file ref:444089 Level19, 12 Creek Street, BRISBANE. QLD 4001 For the Attention of Angus MacDonald Dear Sir, Subject-Irrigation Prices for Seqwater Central Brisbane WSS: 2013-17 We are stakeholders in the Central Brisbane WSS and hold a current license to draw water from the Brisbane River between Wivenhoe Dam and Mount Crosby. We would be extremely concerned should the QCA come to the conclusion that the documentation provided by Seqwater provides a justification for any charge to be made for water taken direct from the Brisbane River under the capped 7000MI agreement. We note that the Fernvale Consultation meeting of 22"d June was attended by a very small proportion of the 130 license Holders. We consider that the views expressed about the level of charging per Ml were not representative of our views or the views of the majority of license holders in the Central Brisbane WSS who attended a meeting of 10th July 2012. We support the views expressed in the attached submission and request the QCA accept this submission on our behalf. Yours faithfully, Signature r/lrz-1'151§/1 rr-; L-~,P Print Name of l icense Holder... ............... :.................. .............................................. .. Date 16 ~: ~.... / 'j-l- ~~ MID a&Ua&JII£ A l 'f'EI. 1 &1.1&4..-e&l ~ Pt•omotin8 Effective Sustainable Catchment Manag=ent Submission to Queensland Competition Authority In relation to Seqwater Rural Water Supply Network Service Plan For the Central Brisbane River supply scheme On Behalf of The Members of Mid Brisbane River Irrigators Inc This submission is prepared under 3 main headings 1. -

Wyaralong Dam: Issues and Alternatives

Wyaralong Dam: issues and alternatives Issues associated with the proposed construction of a dam on the Teviot Brook, South East Queensland 2nd edition October 2006 Report prepared by Dr G Bradd Witt and Katherine Witt The proposed Wyaralong Dam: issues and alternatives 2nd edition October 2006 Wyaralong Dam: issues and alternatives Issues associated with the proposed construction of a dam on the Teviot Brook, South East Queensland 2nd Edition October 2006 Report prepared by Dr G Bradd Witt and Katherine Witt - 1 - The proposed Wyaralong Dam: issues and alternatives 2nd edition October 2006 Table of contents Table of contents ................................................................................. i 1.0 Executive summary ................................................................... 1 1.1 Purpose ............................................................................. 1 1.2 Key issues identified in this report ........................................ 2 1.3 Alternative proposition ........................................................ 3 2.0 Introduction and context............................................................ 5 2.1 The Wyaralong District ........................................................ 5 2.2 The Teviot Catchment ......................................................... 5 3.0 Key issues of concern ................................................................ 7 3.1 Catchment yield and dam yield ............................................ 7 3.2 Water quality................................................................... -

Disaster Management Plan Important Information

LOCAL DISASTER MANAGEMENT PLAN IMPORTANT INFORMATION Certain sections of this Scenic Rim Regional Local Disaster Management Plan are privileged and confidential and are not available for distribution to the general public. Scenic Rim Regional Council permits the use of material contained in the Scenic Rim Regional Local Disaster Management Plan being reproduced for research or planning purposes provided that any material used remains unaltered and due recognition of the source of the materials is recognised. Any party using the information for any purposes does so at their own risk and releases and indemnifies Scenic Rim Regional Council against all responsibility and liability (including negligence, negligent misstatement and pure economic loss) for all expenses, losses, damages and costs as a consequence of such use. All requests for additional or clarifying information regarding this document are to be referred to: The Local Disaster Coordinator Scenic Rim Local Disaster Management Group Scenic Rim Regional Council PO Box 25 BEAUDESERT QLD 4285 Ph. 07 5540 5111 Website: www.scenicrim.qld.gov.au ii Scenic Rim Regional Council Local Disaster Management Plan FOREWORD FROM THE CHAIRPERSON OF SCENIC RIM LOCAL DISASTER MANAGEMENT GROUP The Scenic Rim region is a dynamic area in South East Queensland which has a wide range of topography, changing demographic and diversified industries that may be occasionally subject to the impact of disasters, both natural and non-natural. To meet these challenges, Scenic Rim Regional Council annually review and maintain this Local Disaster Management Plan. The focus of the Plan, as required by the Disaster Management Act 2003, is to minimise the effects of disasters or significant emergencies within the Scenic Rim community by ensuring a coordinated, risk management approach involving Prevention, Preparedness, Response and Recovery strategies at Local, District, State and Federal Government levels, along with local emergency services.