Cogen for Africa – Full Size Project Brief Annexes Table of Contents

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Losing Ground.Pdf

The Unprecedented Shrinking of Public Spaces LOSING and Land in Ugandan GROUND? Municipalities A publication of the Cities Alliance Joint Work Programme for Equitable Economic Growth in Cities By Paul. I. Mukwaya, Dmitry Pozhidaev, Denis Tugume, and Peter Kasaija © UNCDF and Cities Alliance 2018 AUTHORS Paul. I. Mukwaya, Department of Geography, Geo-informatics and Climatic Sciences, Makerere University, Kampala, Uganda Dmitry Pozhidaev, United National Capital Development Fund, Kampala, Uganda Denis Tugume, Department of Geography, Geo-informatics and Climatic Sciences, Makerere University, Kampala, Uganda Peter Kasaija, Department of Geography, Geo-informatics and Climatic Sciences, Makerere University, Kampala, Uganda JWP MANAGEMENT AND COORDINATION Rene Peter Hohmann, Cities Alliance Fredrik Bruhn, Cities Alliance GRAPHIC DESIGN Creatrix Design Group This publication was produced by Cities Alliance and the United Nations Capital Development Fund (UNCDF) as part of the Cities Alliance Joint Work Programme (JWP) for Equitable Economic Growth in Cities. The U.K. Department for International Development (DFID) chairs the JWP, and its members are the United Nations Capital Development Fund (UNCDF), UN-Habitat, Women in Informal Employment: Globalizing and Organizing (WIEGO), Commonwealth Local Government Forum (CLGF), Ford Foundation, Institute for Housing and Development Studies (IHS) at Erasmus University Rotterdam and the World Bank. Disclaimer: The views expressed in this publication are those of the author(s) and do not necessarily represent those of the Cities Alliance, the United Nations, including UNCDF and UNOPS, or the UK Department for International Development (DFID). 2 Losing Ground? SUMMARY There is increasing importance being attached to is to promote economic growth that benefits ALL public spaces and other municipal assets, such as citizens. -

Mumbai's Kala Ghoda Gets a New Culinary Destination with The

July-September 2018 Mumbai's Kala Ghoda gets a New Culinary Destination with the launch of RUE DU LIBAN After delighting Mumbaikars with a hearty Italian menu served at their award winning restaurant – Gustoso, Indianapoli Hospitality is ready to take your palates on a journey through the Levant at their newly launched restaurant – Rue Du Liban. Housed in a heritage building in the heart of South Mumbai at the iconic Kala Ghoda, the restaurant is a visual delight. Brainchild of Mr. Jay Mehta, this gourmet destination has been launched in association with his partners Mr. Sam Malde and Ms. Arja Shridhar. COVER STORY July-September 2018 2 Luxury at its Best Rue Du Liban's menu is specially curated to bring you the taste of authentic Levantine cuisine. For those who do not know, Levantine cuisine has a strong multi-cultural influence that includes a delectable fare with traces that are century old, all amalgamated together – from Phoenicians, Turks, Lebanese, Jews and the French. Spread across a luxurious 3200 sq.ft. of space, the plush Art-Deco inspired interiors are accentuated by royal burgundy banquettes. Dale Atkinson, from the London-based designed firm Rosendale Design has given a royal touch to the ambiance with decorative elements like custom lamps, brass work, hand-painted olive leaves on green walls and bespoke glass leaves hanging from the ceiling. Not just the interiors, the crockery at the restaurant spells royalty as well. Specially handcrafted crockery commissioned by Pune-based Curators of Clay along with a range of glamorous brassware from Udaipur-based Baarique exhibit subtle designs that remains exclusive to Rue Du Liban. -

Report on the Implementation of the Investment Policy Review Uganda

Report on the Implementation of the Investment Policy Review Uganda United Nations Conference on Trade and Development REPORT ON THE IMPLEMENTATION OF THE INVESTMENT POLICY REVIEW UGANDA UNITED NATIONS New York and Geneva, 2007 Report on the Implementation of the Investment Policy Review Uganda Note UNCTAD serves as the focal point within the United Nations Secretariat for all matters related to foreign direct investment. This function was formerly carried out by the United Nations Centre on Transnational Corporations (1975-1992). UNCTAD's work is carried out through intergovernmental deliberations, research and analysis, technical assistance activities, seminars, workshops and conferences. The term "country" as used in this study also refers, as appropriate, to territories or areas; the designations employed and the presentation of the material do not imply the expression of any opinion whatsoever on the part of the Secretariat of the United Nations concerning the legal status of any country, territory, city or area or of its authorities, or concerning the delimitation of its frontiers or boundaries. In addition, the designations of country groups are intended solely for statistical or analytical convenience and do not necessarily express a judgement about the stage of develop- ment reached by a particular country or area in the development process. The following symbols have been used in the tables: • Two dots (..) indicate that date are not available or not separately re- ported. Rows in tables have been omitted in those cases where no data are available for any of the elements in the row. • A dash (-) indicates that the item is equal to zero or its value is negligible. -

Agent Banking Faqs

Agent Banking Frequently Asked Questions 1. What is agent banking? An arrangement that allows a retail outlet serve as representative of the agent offering transactional services to the bank customers as defined by agency banking guidelines. 2. Where can I conduct agent banking transactions? You can perform your banking transactions at any agent in Uganda which has Agent Banking Company handshake Logo (black & green) available at the agent premises. 3. Where do I find the Standard Chartered authorised agents? The authorised Standard Chartered agents can be found at the locations below. No AGENT OUTLET NAME PHYSICAL OUTLET ADDRESS 1 Shell Namugongo Along Namugongo Road formerly Super oil Petrol Station 2 Shell Rubaga Road Along Rubaga Road 3 Shell Makerere Makerere - Bwaise Road, Opposite Eastern Gate 4 Shell Makindye Makindye- Opposite Military Barracks 5 Shell Muyenga Muyenga - Kibuli Road Towards Kabalagala 6 Shell Kansanga Kansanga - Next to Former Didi's World 7 Shell Najjanakumbi Entebbe Road - Opposite Kenjoy Supermarket 8 Shell Kampala Road Kampala Road before Commercial Plaza 9 Shell Portbell Portbell Road Adjacent to Silver Springs Hotel 10 Shell Kabowa Ndeeba, Nyanama Road 4. What should I do to become a Standard Chartered Approved Agent Visit any of the Standard Chartered branches to be provided the details of the requirements to become an Agent. 5. What types of transactions can I perform? As a Standard Charted Bank Uganda customer, you can conduct the following; a) cash deposit b) cash withdrawal 6. In which currency can I transact? You will only be allowed to perform cash withdrawal and cash deposit transactions in Uganda Shillings. -

Improving Access to Finance

46994 Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized for SmallBusiness Creating Opportunities IFC, a member of the World Bank Group, fosters sustainable economic growth in developing countries by fi nancing private sector investment, mobilizing private capital in local and international fi nancial markets, and providing advisory and risk mitigation services to businesses and governments. IFC’s vision is that poor people have the opportunity to escape poverty and improve their lives. In FY07, IFC committed $8.2 billion and mobilized an additional $3.9 billion through loan participation and structured fi nance for 299 investments in 69 developing countries. IFC also provided advisory services in 97 countries. For more information, visit www.ifc.org. Creating Opportunities for Small Business Table of Contents 2 Foreword 3 Approach 5 IFC and SMEs 7 Improving the Business Environment 11 Improving Access to Finance 15 Providing Access to Markets, Business Skills, and Information 19 Creating New Opportunities Through Innovation 21 Measuring Results 22 Frequently Asked Questions 23 Contact Details 24 Donor Partners Creating Opportunities for Small Business 1 Foreword IFC’s vision is for people in emerging markets to have opportunities IFC plays a catalytic and innovative role in developing small to escape poverty and improve their lives. This vision drives all of businesses. We can tap the policy experience of the World Bank our work to develop the private sector. These efforts range from and mobilize the resources of a wide range of partners, including investing directly in businesses, to mobilizing private fi nancing governments, other multilateral and bilateral agencies, academic from other investors, to advising companies, governments, and institutions, foundations, nongovernmental and civil society other stakeholders in private enterprises. -

Competition and Consumer Protection Scenario in Uganda

Competition and Consumer Protection Scenario in Uganda Consent Consumer Education Trust #0313 Competition and Consumer Protection Scenario in Uganda Consent CUTS Centre for Competition, Investment & Economic Regulation Consumer Education Trust Competition and Consumer Protection Scenario in Uganda Published by: CUTS Centre for Competition, Investment & Economic Regulation D-217, Bhaskar Marg, Bani Park, Jaipur 302 016, India Ph: +91.141.2207482, Fax: +91.141.2207486 Email: [email protected]/[email protected] Website: www.cuts.org Consent Consumer Education Trust Desai House, Plot 4 Parliament Avenue, GPO Box 1433, Kampala, Uganda Ph: +256.31.260431/2 Fax: +256.31.260432 Email: [email protected] Printed by: Jaipur Printers P. Ltd. Jaipur 302 001 ISBN 81-87222-85-9 © CUTS, 2003 #0313 SUGGESTED CONTRIBUTION Ush4000/INR100/US$5 Contents 1 General Background ........................................................... 5 1.1 UGANDA’S MACRO-ECONOMIC AND TRADE FRAMEWORK ................................................................... 5 1.2 STRUCTURE AND PERFORMANCE OF THE ECONOMY ............. 5 1.3 TRADE POLICY OVERVIEW ........................................................... 8 1.4 COMPETITION POLICY IN UGANDA .......................................... 10 2 Competition Policy and Law in Uganda ........................... 13 2.1 POWER SECTOR ........................................................................... 13 2.2 TELECOM ...................................................................................... 14 2.3 TRANSPORT ................................................................................. -

Portrait of a Resented Race

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by NORA - Norwegian Open Research Archives Portrait of a Resented Race Investigating how the Ugandan media covered the bitter sentiments against Asians expressed in April 2007 and what these sentiments say about the future of Asians in Uganda. Annet Kizza Rønningsbakk Thesis Submitted In Partial Fulfillment for the Master of Journalism Institute of Media and Communication University of Oslo Spring 2011 i ii iii Table of Contents LIST OF APPENDICES ............................................................................................................ v ABSTRACT ............................................................................................................................. vii ACKNOWLEDGEMENTS ...................................................................................................... ix LIST OF ABBREVIATIONS ................................................................................................... xi 1 INTRODUCTION AND BACKGROUND ............................................................................ 1 1.0 Introduction ...................................................................................................................... 1 1.1 Historical Background ...................................................................................................... 2 1.2 Statement of the problem ................................................................................................. 6 1.3 Research questions -

Annual Report of the Auditor General for the Year Ended 30Th June, 2007 Volume 4 Statutory Corporations

OFFICE OF THE AUDITOR GENERAL THE REPUBLIC OF UGANDA ANNUAL REPORT OF THE AUDITOR GENERAL FOR THE YEAR ENDED 30TH JUNE, 2007 VOLUME 4 STATUTORY CORPORATIONS TABLE OF CONTENTS 1.0 Introduction/Mandate .................................................................................... 1 2.0 Scope Of Auditor General‟s Work .................................................................... 1 3.0 Status Of Completion Of Audits ...................................................................... 3 4.0 Audit Opinions - (Certification Of Accounts) ..................................................... 8 4.1 Introduction ....................................................................................................................... 8 4.2 Financial Audit Opinions And Types Of Certification Of Accounts Issued During The Period 1st July 2006 To 30th June 2007 ................................................................. 8 4.3 Unqualified Audit Opinion ............................................................................................... 8 4.4 Unqualified Reports With Emphasis Of Matter ......................................................... 10 4.4.1 Uganda Coffee Development Authority (Year Ended 30th September 2005) ..... 11 4.4.2. National Youth Council Accounts – (Year Ended 30th June 2003) ...................... 11 4.4.3 Uganda Export Promotion Board (Uepb) (Year Ended 31st December 2002) .... 11 4.4.4 .Uganda Investment Authority (Year Ended 30th June 2005) ............................. 12 4.4.5 .Non-Performing Assets -

Daily Pricing Sheet

18th August, 2014 PAN AFRICA INDEX AND CURRENCY MOVEMENTS Country Index Name Index One Day MTD YTD 1 Year 1 Year FX Rate 1 Day MTD YTD Dollar Return % change Level % Chg % Chg % Chg High Low Current % Chg % Chg % Chg 1 Day MTD YTD Botswana BSE DCI 8,682.49 0.03 -0.07 15.61 22,116.00 7,255.90 1.00 761.87 761.87 678.51 762.10 761.27 800.03 Egypt EGX30 5,325.14 0.66 12.06 -2.51 5,969.39 4,523.32 1.00 600.98 600.98 536.39 605.63 685.49 520.40 Ghana GSE Composite 1,888.25 0.24 0.56 57.39 1,909.04 1,016.70 1.00 101.50 101.50 90.45 101.98 102.64 199.75 Ivory Coast IC COMP 208.77 0.91 -1.01 25.33 222.63 141.40 1.00 50,328.00 50,328.00 49,826.00 50,786.25 49,818.70 62,470.99 Kenya NSE 20 4,640.50 0.87 0.92 12.28 416,049.00 3,778.10 1.00 8,500.00 8,500.00 8,510.00 8,574.87 8,579.19 9,567.19 Malawi MSE AISI 6,999.98 0.06 1.24 16.37 6,999.98 5,874.77 1.00 32,600.00 32,600.00 33,369.50 32,620.57 33,004.49 38,846.96 Mauritius SEMDEX 1,869.06 -0.37 -2.38 7.91 1,956.29 1,653.98 1.00 3,000.00 3,000.00 2,955.00 2,988.48 2,926.20 3,196.64 Morocco MADEX 15,490.30 0.00 0.00 0.00 1.00 752.41 752.41 746.43 752.41 752.41 746.43 Namibia LOCAL 304.05 0.47 0.88 11.15 304.05 237.23 1.00 911.68 911.68 747.35 916.43 920.58 841.79 Nigeria NIG ALSI 37,128.40 0.31 2.67 32.23 40,012.66 20,025.93 1.00 15,950.00 15,950.00 15,515.00 15,999.55 16,377.88 20,547.60 South Africa JSE ALSI 39,638.54 -0.33 0.15 0.99 42,016.45 36,818.76 1.00 911.67 911.67 747.35 908.35 913.21 755.73 Swaziland SSX ALSI 289.42 0.00 0.00 1.31 289.42 284.32 1.00 911.67 911.67 747.35 911.67 911.67 758.47 -

I Large-Scale Land Acquisitions for Investment in Uganda

Large-Scale Land Acqusitions for Investment in Uganda Samuel B Mabikke Large-Scale Land Acquisitions for Investment in Uganda: Can it Yield Equitable Benefits for Smallholder Farmers? Presented at the Sixth Annual conference Theme: “Foreign Land Acquisitions in Africa: Implications for Trade, Investment and Development Policies” 24 – 25 November 2011 Arusha, Tanzania Samuel B Mabikke1 The views contained within do not necessarily represent those of trapca or its partners. 1 Chair of Land Management, Technische Universität München, Arcisstrasse 21, D-80333, Munich, GERMANY, E-mail: [email protected] i Large-Scale Land Acqusitions for Investment in Uganda Samuel B Mabikke Abstract By 2 Samuel B. Mabikke Technische Universität München, Germany Email: [email protected] In the wake of the increasing food prices and the subsequent Global Financial Crisis (GFC), with over one billion people going hungry, Large-Scale Land Acquisitions (LSLA) have attracted considerable interests in developing countries. The purchase or lease of land by wealthy, food-insecure nations and private investors from mostly poor, developing nations in order to produce food crops for export is gaining momentum. In the attempt of fighting poverty, create employment and transform agricultural development, many developing countries have attracted investors with promises of making big land offers or leases for investment. In turn, host countries are promised positive investment returns in agricultural development, infrastructure, education, and employment creation. However, evidence shows that little or none of these promises made by investors are fulfilled yet land and water rights, food security and livelihood of local people remain at stake. It is estimated that between 15 and 20 million hectares of farmland in developing countries have been subject to transactions or negotiations involving foreign investors since 2006. -

Innovation Systems and Development the Journey of a Beleaguered Nile Perch Fishery in Uganda

Innovation Systems and Development The Journey of a Beleaguered Nile Perch Fishery in Uganda Maastricht Economic and social Research and training centre on Innovation and Technology © Copyright Rose Kiggundu, Maastricht 2006 ISBN-13: 978-90-5278-580-6 ISBN-10: 90 5278-580-5 Productie: Datawyse / Universitaire Pers Maastricht Innovation Systems and Development The Journey of a Beleaguered Nile Perch Fishery in Uganda PROEFSCHRIFT ter verkrijging van de graad van doctor aan de Universiteit Maastricht, op gezag van de Rector Magnificus, Prof.mr G.P.M.F. Mols, volgens het besluit van het College van Decanen in het openbaar te verdedigen op donderdag 26 oktober 2006 om 12.00 uur door Rose Kiggundu UMP UNIVERSITAIRE PERS MAASTRICHT Promotor Prof. dr. Lynn K. Mytelka Co-promotor Prof. dr. Banji Oyelaran-Oyeyinka Beoordelingscommissie Prof. dr. Robin Cowan (voorzitter) Prof. dr. ir. Wiebe Bijker Prof. Joanna Chataway, The Open University, Walton Hall, Milton Keynes, UK Acknowledgement When I started this research and learning journey six years ago, I thought I was going to write some kind of report like I always did in my past working life with banks, non- government organizations and donor agencies. A couple of years and mentoring exer- cises later, not only did I find that the world of academia had a completely different set of principles defining its values and character but also that a dissertation had its own life. My children, family and I chose to adapt our lives to the many demands of this dissertation. The path was far from easy but we were all determined to keep going and I must say we enjoyed the rollercoaster ride. -

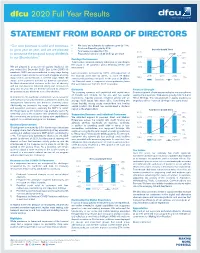

Dfcu 2020 Full Year Results

dfcu 2020 Full Year Results STATEMENT FROM BOARD OF DIRECTORS “Our core business is solid and continues • Net loans and advances to customers grew by 15%. • Customer Deposits grew by 27%. Deposits Growth Trend to grow year on year, and we are pleased • Total assets increased by 18%. 3,515 30% to announce the proposal to pay dividends • Proposed dividend of 50.33 Shillings per share. 27% 2,595 to our Shareholders.” 2,515 20% Earnings Performance 1,979 2,039 Total revenue remained relatively stable year on year despite 1,515 10% the impact of the pandemic and a declining interest rate 3% We are pleased to announce the audited results for the environment. 515 0% year ended 31st December 2020. Due to the COVID-19 0% pandemic, 2020 was unprecedented in many ways having Loan provisions increased by 107% and impairment of an adverse impact across the world and in Uganda affecting the financial asset rose by 400%, to reach 50 Billion 2018 2019 2020 many sectors and livelihoods in different ways. While the (485) -10% consequently posting a net profit for the year of 24 Billion. Deposits% Growth impact of the pandemic affected our business operations, The Financial asset is composed of non-performing loans the Bank demonstrated resilience in the face of adversity that were taken over from the 2017 transaction. and our core business remained strong and continued to grow year on year. We are therefore pleased to announce Dividends Financial Strength the proposal to pay dividends to our Shareholders. The company remained well capitalized with capital ratios Sustained growth of total assets underpins the strength and of 19.34% and 20.94% for tier one and two capital viability of our business.