Mortgage Lending Discrimination: Field

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Summary by Title

Summary NEWLAWS 2002 Summary by Title RESOLUTIONS No-fault automobile insurance full medical Resolution supporting personnel responding to expense benefits entitlement..................................................................................94 Sept. 11 terrorist attacks. ..............................................................................................89 Automobile insurance damaged window glass claims Resolution urging delayed termination of LTV pension plan. .........................89 payment basis modified. .............................................................................................94 Real estate industry licensee conduct regulated. ...................................................95 AGRICULTURE POLICY Fire insurance excess coverage prohibitions..............................................................95 Insurance provisions modification; medical malpractice insurance Biodiesel fuel mandate. ............................................................................................................89 Joint Underwriting Association issuance prohibition. .............................95 Phosphorus fertilizer use regulated. ................................................................................89 Cities additional liquor licenses; hotel rooms liquor cabinets Pesticides application prohibition exceptions (gypsy moth bill). .................90 hours of sale restrictions exemption. ..................................................................95 Omnibus agriculture policy bill. .........................................................................................90 -

Download the Transcript

BOOK-2020/02/24 1 THE BROOKINGS INSTITUTION FALK AUDITORIUM CODE RED: A BOOK EVENT WITH E.J. DIONNE JR. Washington, D.C. Monday, February 24, 2020 Conversation: E.J. DIONNE JR., W. Averell Harriman Chair and Senior Fellow, Governance Studies, The Brookings Institution ALEXANDRA PETRI Columnist The Washington Post * * * * * ANDERSON COURT REPORTING 1800 Diagonal Road, Suite 600 Alexandria, VA 22314 Phone (703) 519-7180 Fax (703) 519-7190 BOOK-2020/02/24 2 P R O C E E D I N G S MR. DIONNE: I want to welcome everybody here today. I’m E.J. Dionne. I’m a senior fellow here at Brookings. The views I am about to express are my own. I don’t want people here necessarily to hang on my views. There are so many people here. First, I want to thank Amber Hurley and Leti Davalos for organizing this event. I want to thank my agent, Gail Ross, for being here. You have probably already seen one of the 10,500,000 Mike Bloomberg ads; you know the tagline is “Mike Gets it Done.” No. Gail gets it done (laughter), so thank you for being here. One unusual person I want to -- also, another great book that you have to read, my friend, Melissa Rogers, who’s a visiting scholar here, we worked together for 20 years, her book, “Faith in American Public Life,” which has a nice double meaning, is a great book to read. And, I can't resist honoring my retired Dr. Mark Shepherd who came here today. -

Minn. GOP Wants Bachmann for Sen., Pawlenty for Pres

FOR IMMEDIATE RELEASE December 10, 2010 INTERVIEWS: DEAN DEBNAM 888-621-6988 / 919-880-4888 (serious media inquiries only please, other questions can be directed to Tom Jensen) QUESTIONS ABOUT THE POLL: TOM JENSEN 919-744-6312 Minn. GOP wants Bachmann for Sen., Pawlenty for Pres. Raleigh, N.C. – Despite getting no love from the state’s at-large electorate against President Obama in PPP’s Wednesday release, outgoing Minnesota Governor Tim Pawlenty is the slim favorite of his own party faithful to get the state’s Republican National Convention delegates. In the race to take on popular Senator Amy Klobuchar, however, he does less well despite coming closest to beating Klobuchar in Tuesday’s look at the general election. Instead, newly empowered Congresswoman Michele Bachman is overwhelmingly the darling of hardcore GOP voters. Bachmann pulls 36% support from usual GOP primary voters, with a wide margin over Pawlenty’s 20%, Norm Coleman’s 14%, and a host of prospective contenders bunched in single digits: 8th-District Congressman-elect Chip Cravaack at 7%, Tom Emmer at 6%, 2nd-District Congressman John Kline at 5%, state legislator Laura Brod at 4%, and Erik Paulsen at 2%, with 6% undecided or favoring someone else. Pawlenty trails Klobuchar by only ten points, versus Bachmann’s 18 and Coleman’s 14. There is a huge ideological divide at play. Bachmann, founder of the Congressional Tea Party Caucus, gets a whopping 42% from the conservative supermajority, which makes up almost three-quarters of the electorate. That puts her far ahead of second-place Pawlenty’s 19%. -

Capitol Insurrection at Center of Conservative Movement

Capitol Insurrection At Center Of Conservative Movement: At Least 43 Governors, Senators And Members Of Congress Have Ties To Groups That Planned January 6th Rally And Riots. SUMMARY: On January 6, 2021, a rally in support of overturning the results of the 2020 presidential election “turned deadly” when thousands of people stormed the U.S. Capitol at Donald Trump’s urging. Even Senate Republican leader Mitch McConnell, who rarely broke with Trump, has explicitly said, “the mob was fed lies. They were provoked by the President and other powerful people.” These “other powerful people” include a vast array of conservative officials and Trump allies who perpetuated false claims of fraud in the 2020 election after enjoying critical support from the groups that fueled the Capitol riot. In fact, at least 43 current Governors or elected federal office holders have direct ties to the groups that helped plan the January 6th rally, along with at least 15 members of Donald Trump’s former administration. The links that these Trump-allied officials have to these groups are: Turning Point Action, an arm of right-wing Turning Point USA, claimed to send “80+ buses full of patriots” to the rally that led to the Capitol riot, claiming the event would be one of the most “consequential” in U.S. history. • The group spent over $1.5 million supporting Trump and his Georgia senate allies who claimed the election was fraudulent and supported efforts to overturn it. • The organization hosted Trump at an event where he claimed Democrats were trying to “rig the election,” which he said would be “the most corrupt election in the history of our country.” • At a Turning Point USA event, Rep. -

2018 BMS PAC Contributions

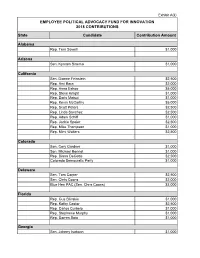

Exhibit A(ii) EMPLOYEE POLITICAL ADVOCACY FUND FOR INNOVATION 2018 CONTRIBUTIONS State Candidate Contribution Amount Alabama Rep. Terri Sewell $1,000 Arizona Sen. Kyrsten Sinema $1,000 California Sen. Dianne Feinstein $2,500 Rep. Ami Bera $2,000 Rep. Anna Eshoo $5,000 Rep. Steve Knight $1,000 Rep. Doris Matsui $1,000 Rep. Kevin McCarthy $5,000 Rep. Scott Peters $2,500 Rep. Linda Sanchez $2,500 Rep. Adam Schiff $1,000 Rep. Jackie Speier $2,500 Rep. Mike Thompson $1,000 Rep. Mimi Walters $2,500 Colorado Sen. Cory Gardner $1,000 Sen. Michael Bennet $1,000 Rep. Diana DeGette $2,500 Colorado Democratic Party $1,000 Delaware Sen. Tom Carper $2,500 Sen. Chris Coons $2,000 Blue Hen PAC (Sen. Chris Coons) $3,000 Florida Rep. Gus Bilirakis $1,000 Rep. Kathy Castor $2,500 Rep. Carlos Curbelo $1,000 Rep. Stephanie Murphy $1,000 Rep. Darren Soto $1,000 Georgia Sen. Johnny Isakson $1,000 Sen. David Perdue $2,000 Rep. Buddy Carter $2,500 Iowa Gov. Kim Reynolds $2,000 Sen. Chuck Grassley $2,500 State Sen. Charles Schneider $2,000 State Sen. Tom Shipley $500 Idaho Sen. Mike Crapo $5,000 Illinois Rep. Cheri Bustos $1,000 Rep. Bill Foster $1,000 Rep. Robin Kelly $1,000 Rep. Darin LaHood $1,000 Rep. Pete Roskam $1,000 Rep. Brad Schneider $1,000 Rep. John Shimkus $2,500 Indiana Sen. Mike Braun $1,000 Sen. Joe Donnelly $2,500 Rep. Larry Bucshon $2,500 Rep. Susan Brooks $2,000 Rep. Andre Carson $1,000 Rep. -

Massachusetts 2012 Senate Poll

FOR IMMEDIATE RELEASE December 2, 2010 INTERVIEWS: DEAN DEBNAM 888-621-6988 / 919-880-4888 (serious media inquiries only please, other questions can be directed to Tom Jensen) QUESTIONS ABOUT THE POLL: TOM JENSEN 919-744-6312 Scott Brown looking good for 2012 re-election Raleigh, N.C. – In a look ahead to 2012, PPP tested five different Democrats against freshman Massachusetts Senator Scott Brown, who surprised the world by taking Ted Kennedy’s old seat in a January 2010 special election that was a precursor to November’s midterm drubbings. But Brown is still so popular even in a wider electorate that even in this heavily blue state, none of the five can come closer than a seven-point deficit. Brown tops recently re-elected Governor Deval Patrick, 49-42; Kennedy’s widow Vicki, 48-41; 34-year representative of the 7th congressional district, Ed Markey, 49-39; 8th- district Congressman Mike Capuano, 52-36; and 9th-district Congressman Stephen Lynch, 49-30. The varying deficits are largely a function of name recognition, but there is clearly a ceiling for a Democrat right now in an unlikely place. Brown gets 22-28% of Democrats, something usually only seen in Southern Democratic states like North Carolina. He maintains 85-89% of his own party, and holds 29- to 34-point leads with independents, who make up almost as much of the electorate (38%) as Democrats (42%). In a sign of how moderate and mainstream Brown’s image is, 53% say his views are “about right,” something only 32% say of the GOP as a whole. -

Summer 2012 Vol 17 • No

You could win something next! something win could You Summer 2012 Vol 17 • No. 2 Connected to the Community contest. Community the to Connected Mighty Red HD Radio Radio HD Red Mighty they won in the last MBA MBA last the in won they displays the the displays IN THIS ISSUE Ray Auger, Auger, Ray Multi Media Director from WMRC-AM in Milford Milford in WMRC-AM from Director Media Multi you” for the entry! the for you” Letter from the Editor We might even send you a little something to say “thank “thank say to something little a you send even might We some of the best entries in future Airwaves newsletters! newsletters! Airwaves future in entries best the of some Political Advertising Rules to share to [email protected]. We’ll feature feature We’ll [email protected]. to share to station success stories along with any photos you want want you photos any with along stories success station Continuing Education still buzzing about? We want to hear from you! Send your your Send you! from hear to want We about? buzzing still Or have you held a wicked cool contest that your station is is station your that contest cool wicked a held you have Or Reimbursement Program you and your team created a brag-worthy charity event? event? charity brag-worthy a created team your and you FROM THE EDITOR Have lately?” to up been station your has “What know, Sound Bites Annual Meeting The Massachusetts Broadcasters Association wants to to wants Association Broadcasters Massachusetts The & Mingling Request AIRWAVES Alec Baldwin’s character in Glengarry Glen Ross is famous for saying, “A-B-C. -

NRCC: MN-07 “Vegas, Baby”

NRCC: MN-07 “Vegas, Baby” Script Documentation AUDIO: Taxpayers pay for Colin Peterson’s Since 1991, Peterson Has Been Reimbursed At personal, private airplane when he’s in Minnesota. Least $280,000 For Plane Mileage. (Statement of Disbursements of House, Chief Administrative Officer, U.S. House of Representatives) (Receipts and Expenditures: Report of the Clerk of TEXT: Collin Peterson the House, U.S. House of Representatives) Taxpayers pay for Peterson’s private plane Statement of Disbursements of House AUDIO: But do you know where else he’s going? Peterson Went Las Vegas On Trip Sponsored By The Safari Club International From March AUDIO: That’s right. Vegas, Baby. Vegas. 22, 2002 To March 25, 2002 Costing, $1,614. (Collin Peterson, Legistorm, Accessed 3/17/14) Peterson Went Las Vegas On Trip Sponsored By The American Federation Of Musicians From June 23, 2001 To June 25, 2001, Costing $919. (Collin Peterson, Legistorm, Accessed 3/17/14) Peterson Went Las Vegas On Trip Sponsored By The Safari Club International From January 11, 2001 To January 14, 2001, Costing $918.33. (Collin Peterson, Legistorm, Accessed 3/17/14) AUDIO: Colin Peterson took 36 junkets. Vacation- Throughout His Time In Congress, Peterson like trips, paid for by special interest groups. Has Taken At Least 36 Privately Funded Trip Worth $57,942 (Collin Peterson, Legistorm, Accessed 3/17/14) TEXT: 36 Junkets paid for by special interest groups See backup below Legistorm AUDIO: In Washington, Peterson took $6 million in Collin Peterson Took $6.7 Million In Campaign campaign money from lobbyists and special Money From Special Interest Group PACs interests. -

Politicians and Their Professors the Discrepancy Between Climate Science and Climate Policy

Better Future Project 30 Bow Street Cambridge, MA. 02138 Politicians and Their Professors The Discrepancy between Climate Science and Climate Policy By Craig S. Altemose and Hayley Browdy Massachusetts Edition Better Future Project 1 Politicians and Their Professors: The Discrepancy between Climate Science and Climate Policy By Craig Altemose and Hayley Browdy With research and editing assistance provided by Elana Sulakshana, Alli Welton, and Kristen Wraith © 2012, Better Future Project 30 Bow Street, Cambridge, MA 02138 About This Report This report seeks to highlight the discrepancy between the overwhelming consensus on climate change that exists among the nation’s scientific community and the lack of action by federal leaders. Past studies have shown that 97-98% of climate scientists who publish in peer-reviewed journals agree with the consensus that climate change is real, happening now, and man-made. Since many politicians seem to disregard the views of such scientific “elites” as a whole, we decided to compare politicians’ views on climate change to those of the climate experts at their alma maters. These politicians clearly valued the expertise of the academics at their schools enough that they chose to (usually) spend tens of thousands of dollars and up to four years of their lives absorbing knowledge from these institutions’ experts. We thought that even if these politicians choose to disregard the consensus of national experts, they might be persuaded by the consensus of the higher education institutions in which they trusted enough to invest great amounts of their time and money. This report and the research supporting it are available online at www.betterfutureproject.org/resources. -

Freshman Class of the 110Th Congress at a Glance

Freshman Class of the 110th Congress at a Glance NEW HOUSE MEMBERS BY DISTRICT Position on Position on District Republican Democrat1 Winner Immigration Immigration Border security with AZ-05 J.D. Hayworth Enforcement first Harry E. Mitchell Mitchell • guest worker program Employer sanctions; Randy Graf AZ-08 Enforcement first Gabrielle Giffords “comprehensive Giffords (Jim Kolbe) reform” “Comprehensive CA-11 Richard W. Pombo• Enforcement first Jerry McNerney reform” and “path to McNerney citizenship” Kevin McCarthy Enforcement and tighter CA-22 Sharon M. Beery No clear position McCarthy (Bill Thomas) border security Doug Lamborn Tighter security; CO-05 Jay Fawcett Enforcement first Lamborn (Joel Hefley) opposes amnesty “Comprehensive Rick O’Donnell Enforcement first; CO-07 Ed Perlmutter reform” and “path to Perlmutter (Bob Beauprez) employer sanctions citizenship” CT-02 Bob Simmons• Enforcement first Joe Courtney Employer Sanctions Courtney Supports tighter border CT-05 Nancy L. Johnson Christopher S. Murphy “Path to citizenship” Murphy • security 1For simplification, this column also includes Independents. Incumbent Retiring incumbent Vacating to run for higher office Resigning Lost in the primary Position on Position on District Republican Democrat1 Winner Immigration Immigration Gus Bilirakis FL-09 Enforcement first Phyllis Busansky Supports border security Bilirakis (Michael Bilirakis) Kathy Castor “Comprehensive FL-11 Eddie Adams Opposes amnesty Castor (Jim Davis) reform” Supports enforcement, Vern Buchanan Employer sanctions; FL-13 tighter security; Christine Jennings Buchanan (Katherine Harris) “path to citizenship” opposes amnesty Supports border Joe Negron FL-16 Tighter border security Tim Mahoney security; “path to Mahoney (Mark Foley) citizenship” “Comprehensive reform”; FL-22 E. Clay Shaw Ron Klein Employer sanctions Klein • guest worker program Hank Johnson “Comprehensive GA-04 Catherine Davis Enforcement first; removal (Cynthia A. -

Donald Trump, Twitter, and Islamophobia: the End of Dignity in Presidential Rhetoric About Terrorism

Montclair State University Montclair State University Digital Commons Department of Justice Studies Faculty Scholarship and Creative Works Department of Justice Studies Spring 3-22-2020 Donald Trump, Twitter, and Islamophobia: The End of Dignity in Presidential Rhetoric about Terrorism Gabriel Rubin Follow this and additional works at: https://digitalcommons.montclair.edu/justice-studies-facpubs Part of the Administrative Law Commons, International Humanitarian Law Commons, International Law Commons, Legal Ethics and Professional Responsibility Commons, Legal Profession Commons, Near and Middle Eastern Studies Commons, Peace and Conflict Studies Commons, Place and Environment Commons, President/Executive Department Commons, Public Administration Commons, Public Affairs Commons, Public Policy Commons, Social Justice Commons, and the Terrorism Studies Commons Chapter Four Donald Trump, Twitter, and Islamophobia: The End of Dignity in Presidential Rhetoric about Terrorism Presidential rhetoric is critically important in guiding American foreign and domestic policy as well as in determining which threats are pursued by the U.S. government1. After the September 11 attacks, terrorism was touted as a threat that would “never again” be ignored. This threat was repeatedly harped on by Presidents George W. Bush and Barack Obama. After Bush set the agenda for an expansive terror war and a presidential rhetoric replete with fear, Obama attempted to recalibrate and narrow the war on terror but ended up largely maintaining Bush’s policies and falling into some of Bush’s rhetoric regarding the terror threat. President Donald Trump, who campaigned viciously against Obama’s legacy, also did not change much in terms of terrorism policy. Even so, the rhetoric adopted by Trump has upended decades of presidential decorum and dignity in the way he speaks about terrorists and the brazen way he links terrorism to the negatives he attaches to immigration. -

June 26, 2011 Transcript

© 2011, CBS Broadcasting Inc. All Rights Reserved. PLEASE CREDIT ANY QUOTES OR EXCERPTS FROM THIS CBS TELEVISION PROGRAM TO "CBS NEWS' FACE THE NATION." June 26, 2011 Transcript GUEST: REPRESENTATIVE MICHELE BACHMANN R-Minnesota; Republican Presidential Candidate MODERATOR/ PANELIST: Bob Schieffer, CBS News Political Analyst This is a rush transcript provided for the information and convenience of the press. Accuracy is not guaranteed. In case of doubt, please check with FACE THE NATION - CBS NEWS (202) 457-4481 TRANSCRIPT BOB SCHIEFFER: Today on FACE THE NATION, who is Michele Bachmann and why does she want to be President. Critics had dismissed her as a religious zealot and a shoot from the hip extremist. But the conservative journal Weekly Standard puts her on the cover this week and calls her Queen of the Tea Party. And the poll out this morning shows that she and Mitt Romney have a big lead over the other Republican candidates in Iowa. That after rave reviews in the first campaign debate in New Hampshire. REPRESENTATIVE MICHELE BACHMANN (R-Minnesota/Republican Presidential Candidate): President Obama is a one-term President. BOB SCHIEFFER: So how broad is her appeal? Tomorrow in Iowa, she announces officially that she’s running for the Republican nomination. Today, she’s in our studio to tell us how and why she is doing. It’s all ahead on FACE THE NATION. ANNOUNCER: FACE THE NATION with CBS News chief Washington correspondent Bob Schieffer. And now from Washington, Bob Schieffer. BOB SCHIEFFER: And good morning again and welcome to FACE THE NATION. Well, Congresswoman, your day is off to-- I would say to a very good start.