Technical Analysis

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Copyrighted Material

INDEX Page numbers followed by n indicate note numbers. A Arnott, Robert, 391 Ascending triangle pattern, 140–141 AB model. See Abreu-Brunnermeier model Asks (offers), 8 Abreu-Brunnermeier (AB) model, 481–482 Aspray, Thomas, 223 Absolute breadth index, 327–328 ATM. See Automated teller machine Absolute difference, 327–328 ATR. See Average trading range; Average Accelerated trend lines, 65–66 true range Acceleration factor, 88, 89 At-the-money, 418 Accumulation, 213 Average range, 79–80 ACD method, 186 Average trading range (ATR), 113 Achelis, Steven B., 214n1 Average true range (ATR), 79–80 Active month, 401 Ayers-Hughes double negative divergence AD. See Chaikin Accumulation Distribution analysis, 11 Adaptive markets hypothesis, 12, 503 Ayres, Leonard P. (Colonel), 319–320 implications of, 504 ADRs. See American depository receipts ADSs. See American depository shares B 631 Advance, 316 Bachelier, Louis, 493 Advance-decline methods Bailout, 159 advance-decline line moving average, 322 Baltic Dry Index (BDI), 386 one-day change in, 322 Bands, 118–121 ratio, 328–329 trading strategies and, 120–121, 216, 559 that no longer are profitable, 322 Bandwidth indicator, 121 to its 32-week simple moving average, Bar chart patterns, 125–157. See also Patterns 322–324 behavioral finance and pattern recognition, ADX. See Directional Movement Index 129–130 Alexander, Sidney, 494 classic, 134–149, 156 Alexander’s filter technique, 494–495 computers and pattern recognition, 130–131 American Association of Individual Investors learning objective statements, 125 (AAII), 520–525 long-term, 155–156 American depository receipts (ADRs), 317 market structure and pattern American FinanceCOPYRIGHTED Association, 479, 493 MATERIALrecognition, 131 Amplitude, 348 overview, 125–126 Analysis pattern description, 126–128 description of, 300 profitability of, 133–134 fundamental, 473 Bar charts, 38–39 Andrews, Dr. -

Elliott Wave Principle

THE BASICS OF THE ELLIOTT WAVE PRINCIPLE by Robert R. Prechter, Jr. Published by NEW CLASSICS LIBRARY a division of Post Office Box 1618, Gainesville, GA 30503 USA 800-336-1618 or 770-536-0309 or fax 770-536-2514 THE BASICS OF THE ELLIOTT WAVE PRINCIPLE Copyright © 1995-2004 by Robert R. Prechter, Jr. Printed in the United States of America First Edition: August 1995 Second Edition: February 1996 Third Edition: April 2000 Fourth Edition: June 2004 August 2007 For information, address the publishers: New Classics Library a division of Elliott Wave International Post Office Box 1618 Gainesville, Georgia 30503 USA All rights reserved. The material in this volume may not be reprinted or reproduced in any manner whatsoever. Violators will be prosecuted to the fullest extent of the law. Cover design: Marc Benejan Production: Pamela Greenwood ISBN: 0-932750-63-X CONTENTS 7 The Basics 7 The Five Wave Pattern 8 Wave Mode 10 The Essential Design 11 Variations on the Basic Theme 12 Wave Degree 14 Motive Waves 14 Impulse 16 Extension 17 Truncation 18 Diagonal Triangles (Wedges) 19 Corrective Waves 19 Zigzags (5-3-5) 21 Flats (3-3-5) 22 Horizontal Triangles (Triangles) 24 Combinations (Double and Triple Threes) 26 Guidelines of Wave Formation 26 Alternation 26 Depth of Corrective Waves 27 Channeling Technique 28 Volume 29 Learning the Basics 32 The Fibonacci Sequence and its Application 35 Ratio Analysis 35 Retracements 36 Motive Wave Multiples 37 Corrective Wave Multiples 40 Perspective 41 Glossary FOREWORD By understanding the Wave Principle, you can antici- pate large and small shifts in the psychology driving any investment market and help yourself minimize the emo- tions that drive your own investment decisions. -

New Elliott Wave Principle

History The Elliott Wave Theory is named after Ralph Nelson Elliott. In the 1930s, Ralph Nelson Elliott found that the markets exhibited certain repeated patterns. His primary research was with stock market data for the Dow Jones Industrial Average. This research identified patterns or waves that recur in the markets. Very simply, in the direction of the trend, expect five waves. Any corrections against the trend are in three waves. Three wave corrections are lettered as "a, b, c." These patterns can be seen in long-term as well as in short-term charts. In Elliott's model, market prices alternate between an impulsive, or motive phase, and a corrective phase on all time scales of trend, as the illustration shows. Impulses are always subdivided into a set of 5 lower-degree waves, alternating again between motive and corrective character, so that waves 1, 3, and 5 are impulses, and waves 2 and 4 are smaller retraces of waves 1 and 3. Corrective waves subdivide into 3 smaller-degree waves. In a bear market the dominant trend is downward, so the pattern is reversed—five waves down and three up. Motive waves always move with the trend, while corrective waves move against it and hence called corrective waves. Ideally, smaller patterns can be identified within bigger patterns. In this sense, Elliott Waves are like a piece of broccoli, where the smaller piece, if broken off from the bigger piece, does, in fact, look like the big piece. This information (about smaller patterns fitting into bigger patterns), coupled with the Fibonacci relationships between the waves, offers the trader a level of anticipation and/or prediction when searching for and identifying trading opportunities with solid reward/risk ratios. -

A STOCK MARKET CORRECTION SURVIVAL GUIDE What You Need to Do Now

Investment and Company Research Select Research SPECIAL REPORT A STOCK MARKET CORRECTION SURVIVAL GUIDE What You Need To Do Now Rob Goldman August 1, 2014 [email protected] CONCLUSION The start of a major correction rarely begins with one catalyst. Instead, they commence in response to multiple events, often within a week of one another. In my view, this has just happened in the past two trading sessions and investors must act quickly and decisively in the near term. The good news is that money can be made even in the throes of a corrective phase and we provide you with specific guidance in this special report. INTRODUCTION "The four most dangerous words in investing are: this time it's different." Sir John Templeton Mid-morning on Wednesday, July 30th, we viewed early economic and market events as a signal that the stock market rally was officially over and that we in fact entered into the start of a corrective phase a week earlier when the S&P 500 Index reached the 1991 mark. We issued a blog on our website and throughout cyberspace proclaiming the market top. The combination of Wednesday’s events (in the AM and PM) with Thursday’s economic news prompted the biggest stock selloff in months and only affirms the thesis made in the blog. Figure 1: S&P 200-Day Performance www.goldmanresearch.com Copyright © Goldman Small Cap Research, 2014 Page 1 of 9 Investment and Company Research Select Research SPECIAL REPORT While others may argue otherwise and trading on Friday may be a temporary return to a bullish stance, we deem the situation urgent enough to produce this special report with the intention of explaining the current correction and providing guidance on how to respond to it. -

Dow Theory for the 21St Century Schannep Timing Indicator COMPOSITE Indicator

st April 1 , 2015 Dow Theory for the 21st Century Schannep Timing Indicator COMPOSITE Indicator Charting a Course of Caution Dow Jones: 17,776.12 S&P 500: 2,067.88 OVERVIEW: There are many stock market and economic indicators ‘out NYSE: 11,062.79 there’, and we can’t follow them all. But every so often we see something that causes us to take a look. Recently a couple of lesser known, or followed, indicators have given us pause in our bullishness. A MarketWatch column by Mark Hulbert about an indicator described by Norman Fosback in his 1976 ‘classic’ Stock Market Logic is intriguing. In years prior to those shown in the chart below, Fosback states that from 1942 to 1975, the "tops of 1946, '56, '59, '61, '66, '68, and '73 were all accompanied or preceded by turns in margin debt". All but 1959 were major bull market tops, as you can see at the Historic Record on our website. The concept illustrated is that ‘sophisticated’ investors aggressively use margin in bull markets, but pull in their horns when stocks start going down. Fosback further stated that when the trend is down, there is a 59% chance a bear market is in progress (41% a bull market is in progress) - not good odds. That implies the bull market topped out earlier this last month on March 2nd at 18,288.63! How’s that for a cloudy outlook? On the other hand, when margin debt is rising there is an 85% probability that a bull market is in progress – as has been the case since 2011, until now. -

Charles Dow Desarrolla Lo Que Hoy Se Conoce Como El Dow Jones Industrial Average®

Hitos 1896 • Charles Dow desarrolla lo que hoy se conoce como el Dow Jones Industrial Average®. 1923 • Standard Statistics Company, antecesora de Standard & Poor’s, desarrolla su primer indicador del mercado accionario con cobertura a 233 empresas. 1926 • Standard Statistics Company lanza al mercado un índice compuesto de precios que incluía 90 acciones. 1941 • Standard Statistics se fusiona con Poor’s Publishing para formar Standard & Poor's. • El indicador del mercado accionario creado en 1923 aumenta su número de compañías de 233 a 416. 1946 • El Dow Jones Industrial Average cumple 50 años. 1957 • Standard & Poor’s publica por primera vez el S&P 500® como un índice de 500 acciones. 1972 • El S&P 500 se convierte en el primer índice bursátil con publicación diaria. 1975 • ExxonMobil se convierte en el primer fondo de pensiones vinculado al S&P 500 y la industria comienza a expandirse. • La calidad institucional llega al mercado general. Vanguard lanza el primer fondo mutuo de índices de consumo, el Vanguard 500, y utiliza el S&P 500 como benchmark. 1982 • CME Group comienza a operar los primeros índices de futuros ―S&P 500 index futures― en la Bolsa de Valores de Chicago (Chicago Mercantile Exchange). 1983 • El Mercado de Opciones de la Bolsa de Chicago (CBOE®) comienza a operar el primer índice de opciones. Estas opciones se basaban en el S&P 500 y el S&P 100. S&P Dow Jones Indices – Hitos 2016 1991 • Standard & Poor’s lanza al mercado el S&P MidCap 400®, el primer índice destacado de títulos de capitalización media en Estados Unidos. -

Results of the S&P Paris-Aligned & Climate Transition (PACT) Indices

INDEX ANNOUNCEMENT Results of the S&P Paris-Aligned & Climate Transition (PACT) Indices Consultation on Eligibility Requirements and Constraints AMSTERDAM, MAY 18, 2021: S&P Dow Jones Indices (“S&P DJI”) has conducted a consultation with market participants on potential changes to the S&P Paris-Aligned & Climate Transition (PACTTM) Indices. S&P DJI will make changes to the eligibility requirements and optimization constraints used in these indices. The changes are designed to ensure the indices continue to meet their objective, reflect evolving expectations for environmental, social and governance (ESG) business exclusions, while including additional stability to the turnover and stock counts following fluctuations caused by the existing rules. The table below summarizes the changes, and which indices they will impact. Index Family1 Methodology Change CT PA Current Updated Environmental X X CT: Weighted-average S&P DJI CT: Weighted-average S&P DJI ESG Score Score Environmental Score (waE) of the CT Index (waESG) of the CT Index should be ≥ the Constraint to should be ≥ the waE of the eligible universe. eligible waESG of the eligible universe. ESG Score Constraint PA: Weighted-average S&P DJI PA: Weighted-average S&P DJI ESG Score Environmental Score (waE) of the PA Index (waESG) of the PA Index should be ≥ the should be ≥ the waE of the eligible universe waESG of the universe after 20% of the + (20% × (max E score in eligible universe – worst ESG score performing companies by eligible universe’s waE)). count are removed and weight redistributed. Introduce X X No buffer, minimum stock weight lower Minimum stock weight threshold ≥1 buffer rule and threshold of 0.01%, maximum weight of 5%. -

Stock Market Efficiency Withstands Another Challenge: Solving the “Sell in May/Buy After Halloween” Puzzle

Econ Journal Watch, Volume 1, Number 1, April 2004, pp 29-46. Stock Market Efficiency Withstands another Challenge: Solving the “Sell in May/Buy after Halloween” Puzzle EDWIN D. MABERLY* AND RAYLENE M. PIERCE** A COMMENT ON: BOUMAN, SVEN AND BEN JACOBSEN. 2002. THE HALLOWEEN INDICATOR, ‘SELL IN MAY AND GO AWAY’: ANOTHER PUZZLE. AMERICAN ECONOMIC REVIEW 92(5): 1618-1635. ABSTRACT, KEYWORDS, JEL CODES OVER THE PAST TWENTY YEARS FINANCIAL ECONOMISTS HAVE documented numerous stock return patterns related to calendar time. The list includes patterns related to the month-of-the-year (January effect), day- of-the-week (Monday effect), day-of-the-month (turn-of-the-month effect), and market closures due to exchange holidays (the holiday effect) to name just a few.1 This research is cited as evidence of market inefficiencies (see, * University of Canterbury. Chiristchurch, New Zealand. ** Lincoln University. Canterbury, New Zealand. This paper benefited from editorial comments by Professor Tom Saving of Texas A&M University and encouraging comments by Professor Burton Malkiel of Princeton University. Additionally, constructive comments were provided by an anonymous referee. 1 The January effect is frequently misinterpreted as implying that stock returns, irrespective of market size, are unusually large in January. From Fama (1991, 1586-1587), the January effect refers to the phenomenon that “stock returns, especially returns on small stocks, are on average higher in January than in other months. Moreover, much of the higher January return on small stocks comes on the last trading day in December and the first 5 trading days in January.” 29 EDWIN D. -

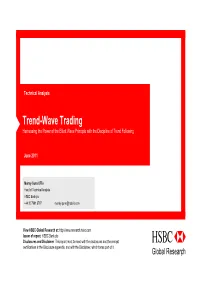

Trend-Wave Trading Harnessing the Power of the Elliott Wave Principle with the Discipline of Trend Following

Technical Analysis Trend-Wave Trading Harnessing the Power of the Elliott Wave Principle with the Discipline of Trend Following June 2011 Murray Gunn CFTe Head of Technical Analysis HSBC Bank plc +44 20 7991 6797 [email protected] View HSBC Global Research at: http://www.research.hsbc.com Issuer of report: HSBC Bank plc Disclosures and Disclaimer This report must be read with the disclosures and the analyst ABC certifications in the Disclosure appendix, and with the Disclaimer, which forms part of it Global Research1 The Elliott Wave Principle – A Basic Guide 1 Elliott Wave Principle A Fractal Design (5) Ralph Nelson Elliott (3) (B) Price action occurs in regular patterns Long 5 moves (or waves) in the direction of the primary Term 2 (4) 5 (A) trend 2 (1) 3 C 4 2 (C) 3 moves (or waves) when the price action is 1 A 4 correcting against the primary trend 5 1 3 B 1 4 (2) B 5 Repeat at every time frame or fractal Medium 3 Term 3 A 2 1 5 Mass human psychology is patterned C 1 4 5 B (5) Ratio analysis/natural mathematics (Phi, the golden 3 5 (B) 2 2 C ratio, 1.618, Leonardo Fibonacci) 1 4 A C 3 4 2 (3) 1 A 2 5 1 4 4 Elliott heavily influenced by Charles Dow Short B 3 B 1 Term 5 Wave Principle is the purest form of TA 3 A 2 (A) 3 (1) 5 The 1 C 5 4 (C) Full 3 B (4) Putting it all Cycle 1 A 2 together 2 4 C 2 (2) 2 Waves Are Self Similar in FORM… …but they do NOT have to be self similar in TIME or depth (AMPLITUDE) (5) Much more like REALITY 5 (3) 3 1 5 3 B 4 D 4 2 1 E (4) (1) 5 C 3 4 B 2 A 1 A 2 C 3 (2) Elliott’s Wave Principle is technical analysis Elliott heavily influenced by Charles Dow Empirical observations confirmed Dow’s Theory Refined Dow’s work into more detail Price and volume = pure technical analysis Edwards & Magee pattern recognition a derivative of Dow and Elliott 4 Dow Theory • Charles Dow’s editorials in his Wall Street Journal around 1900 • Analysis of price action of the market averages (Dow Industrials, Transports, Utilities) Distribution • Markets have 3 “movements” (value, primary and phase secondary movement). -

Lesson 12 Technical Analysis

Lesson 12 Technical Analysis Instructor: Rick Phillips 702-575-6666 [email protected] Course Description and Learning Objectives Course Description Learn what technical analysis entails and the various ways to analyze the markets using this type of analysis Lessons and Learning Objectives ▪ Define technical analysis ▪ Explore the history of technical analysis ▪ Examine the accuracy of technical analysis ▪ Compare technical analysis to fundamental analysis ▪ Outline different types of technical studies ▪ Study tools and systems which provide technical analysis 2 What is Technical Analysis Short Description: Using the past to predict the future Long Description: A way to analyze securities price patterns, movements, and trends to extrapolate the ranges of potential future prices 3 History of Technical Analysis The principles of technical analysis are derived from hundreds of years of financial market data. Some aspects of technical analysis began to appear in Amsterdam-based merchant Joseph de la Vega's accounts of the Dutch financial markets in the 17th century. In Asia, technical analysis is said to be a method developed by Homma Munehisa during the early 18th century which evolved into the use of candlestick techniques, and is today a technical analysis charting tool. In the 1920s and 1930s, Richard W. Schabacker published several books which continued the work of Charles Dow and William Peter Hamilton in their books Stock Market Theory and Practice and Technical Market Analysis. In 1948, Robert D. Edwards and John Magee published Technical Analysis of Stock Trends which is widely considered to be one of the seminal works of the discipline. It is exclusively concerned with trend analysis and chart patterns and remains in use to the present. -

The First Stock Index Was Created in 1884 by Publishist Charles Dow As

TOOLS OF THE TRADE – INDEX FUNDS VS ASSET CLASS FUNDS The first stock index was created in 1884 by publicist Charles Dow as an indicator for investors of how the stock market was performing. Five years later, Dow established the Dow Jones Industrial Average, and in 1923 Standard & Poor’s instituted their first index, the S&P 90 Index. In the years that followed, many more indices were established and began to be utilized as tools, or benchmarks, for investors when evaluating their own portfolios’ performance. An index is simply a collection of investment types held constant, regardless of market conditions, until their governing body deems it appropriate to reconstitute. While useful as a view of the overall market or specific markets, indices themselves could not be bought or sold until the 1970s. The first index funds, established in 1973 by John McQuown and David Booth at Wells Fargo and Rex Sinquefield at American National Bank, were only available to institutional investors. In 1975, John Bogle at Vanguard changed that by establishing the First Index Investment Trust to track the S&P 500 Index and to be marketed to individuals and institutions. Passive investing was born. The fund, deemed “Bogle’s Folly”, was derided by professional money managers as “un- American”. Edward C. Johnson III, Chairman of Fidelity at that time, was quoted as saying “I can’t believe that the great mass of investors are going to be satisfied with just receiving average returns. The name of the game is to be the best.” (source: Bogle Financial markets Research Center, 2006) The fund was later re-named the Vanguard 500 Index Fund and by 2001 had more assets under management than Fidelity’s Magellan Fund. -

Harmonic Conditions How to Define Price and Time Cycles

Interview: Tim Hayes – A Class of its Own Your Personal Trading Coach Issue 03, April 2010 | www.traders-mag.com | www.tradersonline-mag.com Harmonic Conditions How to Define Price and Time Cycles Great Profi ts through When to Trade The Right Use of Failed Chart Patterns & When to Fade Cyclical Analysis We Show You How to Recognise Them Gaining an Edge in Forex Trading Timing Is Everything for Lasting Success TRADERS´EDITORIAL Harmonising Price with Time Harmonising price with time is one of the issues serious traders grapple with at one point in their careers. And how could this possibly be otherwise? After all, if you wish to predict the future you have to consider the past. And if you look back on the history of trading, you will automatically end up coming across some of the heroes who have written this history. Jesse Livermore is one of them, so is Ralph Nelson Elliott and, last but not least, William D. Gann. Among all the greats of the trade he certainly stands out as the enigma. Square of Nine, Gann Lines and Gann Angles, the law of vibration of the sphere of activity, i.e. the rate of internal vibration all of which you will come The harmony of price and time results in incredible forecasts across once you begin to study the trading hero. Gann’s forecasts are credited with 90% success rates and his trading results are said to have amounted to 50 million dollars. Considering that he lived from1878 to 1955, it is easy to imagine what an incredible fortune this would be today.