Baron Large Cap Growth Strategy

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Servicenow Events 16:9 Powerpoint Template

Visibility to Multi-Cloud Measurable outcomes from CMDB Table of Contents Visibility into Multi-Cloud/Hybrid Cloud 3 Customer journey to Cloud Discovery 4 Visibility into TAGS 6 Deep-dive Discovery of cloud VMs 6 Event-driven Discovery 8 Discovering serverless workloads 9 New York Release enhancements 11 AWS—Identity and Access Management (IAM) roles 11 AssumeRole enhancements for AWS organizations 11 Cloud Discovery UI improvements 11 ITOM Visibility low-code framework—pattern engine and out-of-band patterns 13 For more information 14 Journey to Cloud starts with ServiceNow ITOM Multi-cloud is Cloud and DevOps are independent but mutually reinforcing strategies for quickly becoming delivering business value through IT. A hybrid or multi-cloud workload deploy- the de-facto ment offers the advantage of high resiliency, combined with the agility to adapt quickly to changing digital business requirements. Multi-cloud is quickly deployment becoming the de-facto deployment standard as organizations of all types leverage an ever-increasing variety of cloud computing services. standard as organizations Key factors that influence multi-cloud deployment strategies are: • “Best-of-breed” service offering of all types • Cost to IT Ops and enterprise licensing leverage an • Choice of technology stack for IaaS/PaaS/FaaS services ever-increasing • M&A and data sovereignty, which plays a vital role on the decision- making process variety of cloud computing Visibility into multi-cloud/hybrid cloud services. For many customers, migration to cloud is a transformational journey. Visibility to multi-cloud/hybrid cloud deployment data with on-premise infrastructure and application data is critical to solve the real-world challenges from IT Operations. -

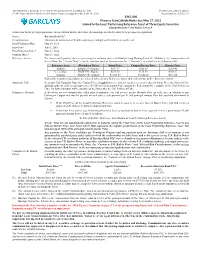

967000 Phoenix Autocallable Notes Due May 27, 2022 Linked to The

Amendment No. 1 dated July 25, 2018 to the Pricing Supplement dated May 24, 2018 Filed Pursuant to Rule 424(b)(2) (To the Prospectus dated March 30, 2018 and the Prospectus Supplement dated July 18, 2016) Registration No. 333–212571 $967,000 Phoenix AutoCallable Notes due May 27, 2022 Linked to the Least Performing Reference Asset of Three Equity Securities Global Medium-Term Notes, Series A Terms used in this pricing supplement, but not defined herein, shall have the meanings ascribed to them in the prospectus supplement. Issuer: Barclays Bank PLC Denominations: Minimum denomination of $1,000, and integral multiples of $1,000 in excess thereof Initial Valuation Date: May 24, 2018 Issue Date: June 1, 2018 Final Valuation Date:* May 24, 2022 Maturity Date:* May 27, 2022 Reference Assets: The American depositary shares representing the ordinary shares of Alibaba Group Holding Limited (“Alibaba”), the common stock of ServiceNow, Inc. (“ServiceNow”) and the common stock of Amazon.com, Inc. (“Amazon”), as set forth in the following table: Reference Asset Bloomberg Ticker Initial Price Coupon Barrier Price Barrier Price Alibaba BABA UN <Equity> $197.37 $128.29 $118.42 ServiceNow NOW UN <Equity> $175.52 $114.09 $105.31 Amazon AMZN UW <Equity> $1,603.07 $1,042.00 $961.84 Each of the securities noted above are referred to herein as a “Reference Asset” and, collectively, as the “Reference Assets.” Automatic Call: If, on any Call Valuation Date, the Closing Price of each Reference Asset is equal to or greater than its Initial Price, the Notes will be automatically called for a cash payment per $1,000 principal amount Note equal to the Redemption Price payable on the Call Settlement Date. -

Virtualwisdom App-Centric Hybrid IT Infrastructure Management Contents

VirtualWisdom App-centric Hybrid IT Infrastructure Management Contents Introduction 3 Operational Vulnerability 4 It’s Not Getting Easier 5 Expertise Required 6 What Expertise Is Required? 7 Traditional Monitoring Tools Don’t Cut It 9 VirtualWisdom Understands 10 Getting a Handle on Infrastructure 11 Getting a Handle on Applications 12 The Human Factor 13 VirtualWisdom Understands 14 HYBRID IT TECH BRIEF | BACK TO TOC | 2 Introduction Slow application performance and application outages cost money. As organizations have become more dependent on IT, the cost of outages has risen. Reducing the number of outages requires identifying their cause before the business is impacted. This is exactly what VirtualWisdom App-centric Hybrid IT Infrastructure Management excels at. Today, the cost of downtime for a single server can be punitive. According to Statista, 24 percent of respondents worldwide reported the average hourly downtime cost of their servers as being between $300,000 - $400,000, with more than 50 percent of respondents reporting costs in higher brackets. These statistics echo those released by Gartner, who cited $5,600 per minute as the cost of downtime: $5,600 per minute is $336,000 per hour. In today’s highly consolidated data centers, multiple individual virtualized hosts typically share a common infrastructure. A failure in any component of that infrastructure could result in multiple virtualized host failures. While it’s difficult to determine how much more a multiple-server outage would cost a given organization over a single server outage, the answer is certainly more than a single server outage would cost, and those costs are already far too high. -

Servicenow Cloud Success AWS 15MAR Webinar

Achieve Cloud Success with AWS Gain Cloud Service Oversight, Minimize Risks, and Reduce Costs – Simplified Through Self-Service Manisha Arora Deaddin Edris Douglas Lee Alliance Architect Senior Product Marketing Manager Head, Solution Architecture ServiceNow ServiceNow Strategic ISV Partners, AWS © 2017 ServiceNow All Rights Reserved 1 Agenda • Introduction • Why Organizations are Moving to the Cloud • The AWS Cloud • Manage Cloud Sprawl with ServiceNow • ServiceNow and AWS – Better Together • Demo • Q & A © 2017 ServiceNow All Rights Reserved 2 ServiceNow Is A Fast-Growing, Global Company ~4,800 Employees Strong Revenue & Growth Major Sites $1.391B San Diego, Silicon Valley, Seattle Amsterdam, London, Sydney, Israel, India $1B $683M $425M $244M $128M $28M $64M ‘09 ‘10 ‘11 ‘12 ‘13 ‘14 ‘15 ’16 ©© 2017 ServiceNow All 2017 ServiceNow All Rights Rights Reserved Reserved 3 Global Enterprises in Every Industry Rely on ServiceNow Construction Federal Financial Services Healthcare Higher Education Insurance IT Services Manufacturing Media MSPs Oil and Gas Retail Services Technology ©© 2017 ServiceNow All 2017 ServiceNow All Rights Rights Reserved Reserved 4 Providing Cloud Services Across the Enterprise © 2017 ServiceNow All Rights Reserved 5 IT SLAs Force Cloud Users to Look for Alternatives Manual IT processes can take weeks to months Cloud Service Needs Grow DIY on Public Clouds Creating Shadow IT Outside of Business Controls Compliance & Introduction Audit Issues of Security Risks Inability to Control Costs © 2017 ServiceNow All Rights Reserved 7 The AWS Cloud © 2017 ServiceNow All Rights Reserved 8 The AWS Cloud Eliminate costly technical debt and reallocate resources so you can deliver high-value, revenue-generating projects faster. Innovate faster and solidify your competitive advantage by merging startup agility with enterprise experience and resources. -

SERVICENOW, INC. (Exact Name of Registrant As Specified in Its Charter)

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, DC 20549 FORM 8-K CURRENT REPORT Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 Date of report (date of earliest event reported): February 22, 2017 SERVICENOW, INC. (Exact name of registrant as specified in its charter) Delaware 001-35580 20-2056195 (State or other jurisdiction of (Commission (I.R.S. Employer incorporation or organization) File Number) Identification Number) 2225 Lawson Lane Santa Clara, California 95054 (Address of Principal Executive Offices) (Zip Code) Registrant’s telephone number, including area code: (408) 501-8550 Not Applicable (Former Name or Former Address, if Changed Since Last Report) Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions (see General Instruction A.2 below): ☐ Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) ☐ Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) ☐ Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) ☐ Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) Item 5.02: Departure of Directors or Certain Officers; Election of Directors; Appointment of Certain Officers; Compensatory Arrangements of Certain Officers. (b) On February 24, 2017, Frank Slootman notified ServiceNow, Inc. (the “Company”) of his decision to resign from his position as the Company’s President and Chief Executive Officer, effective April 3, 2017. -

Servicenow Is on a Collision Course with Salesforce.Com…Here’S Why

Breaking Analysis: ServiceNow is on a Collision Course With Salesforce.com…Here’s Why Breaking Analysis: ServiceNow is on a Collision Course With Salesforce.com…Here’s Why by, David Vellante July 22nd, 2021 ServiceNow is a company that investors love to love. But there’s caution in the investor community right now as confusion about transitory inflation and higher interest rates looms. ServiceNow also suffers from perfection syndrome and elevated expectations. The company has seen that the slightest misstep, or not beating earnings by a wide enough margin, can […] © 2021 Wikibon Research | Page 1 Breaking Analysis: ServiceNow is on a Collision Course With Salesforce.com…Here’s Why ServiceNow is a company that investors love to love. But there’s caution in the investor community right now as confusion about transitory inflation and higher interest rates looms. ServiceNow also suffers from perfection syndrome and elevated expectations. The company has seen that the slightest misstep, or not beating earnings by a wide enough margin, can cause mini freakouts from the investor community. So it has architected a financial and communications model that allows it to marginally beat expectations and raise its outlook on a continuing basis. Regardless, ServiceNow appears to be on a track to vie for what its CEO Bill McDermott refers to as the next great enterprise software company. Wait, we thought that Marc Benioff had taken that crown already… In this Breaking Analysis we’ll dig into ServiceNow, one of the companies we began following almost ten years ago, and provide some thoughts on ServiceNow’s march to $15B by 2026. -

Servicenow Store

Benefits ServiceNow Store Faster Time to Value Deploy New Business Apps at Lightspeed. Store apps are developed and supported by ServiceNow The Challenge Technology Partners and certified IT and application development organizations are facing increasing demand for new by ServiceNow, so you can make and updated applications from users across the enterprise. This results in increasing the decision to buy versus build backlogs and cloud sprawl, with end users seeking out their own solutions from public apps and deploy faster. cloud services. Developing and testing apps from scratch either in-house or outsourced usually means more time, cost, and risk than a pre-built, pre-tested, ready-to-deploy app—resulting in end users waiting longer to start using the applications they need to Reduce Testing Time do their jobs better. and Resources Apps must successfully complete a set of ServiceNow certification The ServiceNow Solution tests focused on integration The ServiceNow® Store is the exclusive source for hundreds of NOW® Certified, interoperability, security, and ready to deploy apps and integrations from Technology Partners. performance. Deploy with Provide agility and innovation to drive business growth. Easily automate and confidence. integrate business processes across people, data, systems, and processes. Immediately deploy intuitive apps loved by users, increasing productivity, and Tap into Partner reducing time to resolution. Ecosystem Innovation The Store provides customers in IT, app dev, and service domains across the There are innovative apps for enterprise such as marketing, legal, HR, and purchasing with a buy verses build every department in the enterprise option and makes discovering, procuring and deploying applications fast, easy, from hundreds of Technology and secure. -

S4capital Investor Update July 2019

Investor Roadshows,Europe and North America July 2019 Contents 1_ Technological and geographic trends 2_ Core principles 3_ The story so far 4_ Strategy and structure 5_ Governance and leadership 6_ Financial performance 7_ MediaMonks 8_ MightyHive 9_ Current trading and outlook S4Capital Investor Update July 2019 !2 Technological and geographic trends The global advertising and marketing industry was worth $1.7tn in 2018 (including $400bn trade budgets – Redburn). Global internet users = 3.6bn people, or over 50% of the population, in 2018 (Kleiner Perkins). Digital media use 5.9 hours per day (Kleiner Perkins). Half of all advertising spend will be on digital media ad formats by 2019/2020, compared to 46% in 2018 (Magna). The market for internet advertising is expanding at over 20% year-on-year (Kleiner Perkins), compared to 3-4% for the overall advertising market (company estimate). Programmatic advertising spend is forecast by the Group to reach $84bn in 2019 growing at approximately 20 per cent year-on-year to reach $98bn in 2020 (company estimate). S4Capital Investor Update July 2019 !3 Technological and geographic trends Source: Company estimates Source: Kleiner Perkins Source: Kleiner Perkins Source: Kleiner Perkins S4Capital Investor Update July 2019 !4 Technological and geographic trends Source: Kleiner Perkins Source: Kleiner Perkins Source: Kleiner Perkins Source: Kleiner Perkins S4Capital Investor Update July 2019 !5 Technological and geographic trends Source: Kleiner Perkins Source: Kleiner Perkins Source: Polar State of Digital Media, Q1 2019 Source: Redburn S4Capital Investor Update July 2019 !6 Industry dynamics First party data Seven Digital creative Traditional creative Programmatic Sisters Zero-based budgeting In-housing Custom research Post-Lehman slower GDP Consultancy growth Walled gardens ‘growing’ ‘Take Back Control' S4Capital Investor Update July 2019 !7 Our four core principles S4Capital Investor Update July 2019 !8 The story so far Formation and initial funding of S4Capital plc in May 2018. -

BIOGRAPHY Hayri Tarhan Is the Director of Federal Civilian Solution Consulting for Servicenow

BIOGRAPHY Hayri Tarhan is the Director of Federal Civilian Solution Consulting for ServiceNow. He is responsible for pre-sales, go-to-market strategy, and overall growth for ServiceNow’s business in the US Federal Civilian markets. Hayri helps Federal agencies address their most important challenge - how to transform the future of government. He and his team work extensively with customers to help them design, evaluate, build, and secure digital workflows that create great experiences and unlock productivity. Prior to joining ServiceNow, Hayri was the VP of North American Public Sector Security Sales for Oracle. He earned a Bachelor of Science in Computer Science from Rensselaer Polytechnic Institute. About Servicenow ServiceNow, Inc. is a cloud computing company headquartered in Santa Clara, California. It was founded in 2003 by Fred Luddy, the previous CTO of software companies Peregrine Systems and Remedy Corporation. ServiceNow is listed on the New York Stock Exchange and is a constituent of the Russell 3000 index. ServiceNow makes work, work better for people by offering everything-as-a-service cloud computing, from including platform-as-a-service (PaaS) enterprise service management software for human resources, law, facilities management, finance, marketing, and field operations. ServiceNow specializes in ITSM applications and provides forms-based workflow application development. ServiceNow has integration options for platforms such as Salesforce, JIRA, SharePoint, and BMC Remedy Action Request System. The company is the fastest growing enterprise software company in the country, with 1000+ partners, 16 data centers worldwide and 290+ apps in the ServiceNow store. With 5600 employees, it has 73 global presence with operations in North America, South America, Asia, Europe and Africa. -

2018 Top 200 Employers for STEM OPT Students

2018 Top 200 Employers for OPT and STEM OPT Students Number of Students Number of Students Number of Students Participating in Top 200 Employer Names Participating in OPT or STEM OPT Participating in OPT in 2018 STEM OPT in 2018 in 2018 Amazon 2,911 851 2,395 Integra Technologies LLC 2,081 1,302 936 Intel Corporation 1,348 368 1,111 Google 1,193 308 996 Microsoft Corporation 867 243 690 AZTech Technologies LLC 854 705 188 Deloitte 747 216 579 Facebook 725 259 528 XCG Design Corporation 680 355 362 Tellon Trading, Inc 647 455 229 IBM 628 143 563 Veridic Solutions 558 332 307 Apple, Inc 538 166 433 CG Max Design Corp 521 224 326 Global IT Experts, Inc 467 442 28 Marlabs, Inc 448 166 311 Randstad 439 231 231 Ernst & Young 432 157 298 Qualcomm Technologies, Inc 416 118 351 PricewaterhouseCoopers 412 160 273 Cisco System, Inc 411 133 322 Populus Group 381 137 275 Cerner Corporation 380 94 313 Modis E&T LLC 374 120 281 Capgemini America 370 99 312 Insight Global 357 160 217 eBay or PayPal 350 116 274 JP Morgan Chase 348 68 295 Robert Half 346 260 96 University of Florida 335 224 118 Saibersys 330 144 203 Cloud Big Data 324 251 98 2018 Top 200 Employers for OPT and STEM OPT Students Walmart 320 124 224 Massachusetts Institute of Technology 315 119 220 Sinocontech 315 252 73 Cummins 312 90 241 Findream, LLC 312 112 209 Goldman Sachs 312 112 232 Stanford University 306 113 215 Oracle 305 73 256 Cognizant 301 54 258 Collabera 300 149 161 Arizona State University 298 258 59 Tesla, Inc 296 126 198 Elbum LLC 291 236 60 Apex Systems 282 115 182 Pioneer -

Building Mobile Apps White Paper

Building Mobile Apps with ServiceNow Quebec, March 2021 Building Mobile Apps with ServiceNow Table of Contents 1 Purpose of the document 4 2 How to use this document 4 3 Native mobile clients 4 3.1 Mobile Agent . 5 3.2 Now Mobile . 5 3.3 Onboarding . 5 4 Navigation tab bar 6 4.1 Naming conventions . 6 4.2 Ordering . 6 5 Applet launchers 7 5.1.1 Applet launcher concept . 7 5.1.2 Applet launcher structure . 7 5.1.3 Applet launcher header . 8 5.1.4 UI sections . 8 5.1.5 Icon section/Navigation UI section . 9 5.1.6 Item section . 9 5.1.7 Chart section . .11 5.1.8 Media section . 13 5.2.1 Campaigns . 14 5.2.2 Global search . 15 5.2.3 Applet launcher quick actions . 17 5.2.4 Applet launcher examples . 18 6 Applets 25 7 Lists applets 26 7.1 List . 26 7.2 Item stream segments on list . 27 7.3 Item streams on list . 27 7.4 Grouped list . .28 7.5 Employee Directory . 28 7.6 Calendar . 29 7.7 Map . 29 7.8 Filters . 30 7.9 Empty state . NEW. 31 8 Chart applet 32 9 URL applet 32 10 Form applet 33 10.1 Screen field types . 35 10.2 Activity stream . 37 10.3 Related list . 38 10.4 Embedded List . 38 10.5 Embedded browser .NEW . 38 March, 2021 2 Building Mobile Apps with ServiceNow Table of Contents (Continued) 10.6 Dynamic segments NEW. 39 11 Saved views NEW 40 12 Actions and functions 41 12.1 Action completion NEW . -

Final Servicenow Taps Artificial Intelligence With.Cdr

White Paper ServiceNow® Taps Artificial Intelligence with Kingston White Paper INTRODUCTION According to PwC's, “A Revolutionary Partnership: How AI Is Pushing Man and Machine Closer” survey of 2,500 U.S. consumers and business decision makers, 72% of the business leaders believe that AI will be extremely fundamental in the future and will be a “business advantage”.1 AI is here to stay. It has already started transforming enterprises and industries. Technology giants such as Google, Microsoft, Netflix, Amazon have not leveraged Al to create delightful customer experiences but have also invested heavily in its R & D. 4 Harley Davidson, a leading motorcycle manufacturer, improved its lead generation by 2930 percent in three months after the implementation of AI-based marketing system2 4 What used to take 360,000 hours for a team of lawyers is now done in seconds by an AI tool that is used by JP Morgan's legal team3 4 Enterprises such as KLM, China Merchants Bank have implemented AI-enabled catboats to help their customers get quick answers to their questions and thereby improve the overall customer satisfaction There are many more such use cases of successful AI implementations. Experts also believe that these applications still just scratch the surface and there is a lot more which can be achieved with these technologies like AI, machine learning, deep learning, and NLP. AI has the potential of stopping over 85% of cyber attacks4, AI- related technologies can increase the global GDP by 14% and drive GDP gains of $15.7 trillion5, AI can drive business growth through powerful insights, it can help in making the cities smarter, and much more.