Audited Financial Statements FY 2011 Through 2020

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

A Community Comes Together Superintendent

From the A Community Comes Together Superintendent... Parents, teachers and students share their Everyone here is so friendly Robert S. Monroe stories on how they are moving forward Junior high school student Kendyll Paul has Welcoming students during a global pandemic while working learned that self-reliance and time manage- together, developing different daily routines ment will be keys for her success. back for in-person and focusing on continued communication. “Being at home all day, every day is a big instruction Patience and grace are so important change,” she said. “I had to balance my time Over the past few weeks, we have been celebrating the return As a teacher and parent, Sara Jozefiak has between getting my schoolwork done and of students to our classrooms for in-person instruction. seen the remote learning environment from spending time with my family. I also learned Through a deliberate process, we have been welcoming back “both sides of the computer screen.” better self-reliance. I would say having the students in small groups using specific grades or programs. “Education looks extremely different and time by myself was a positive thing in the We began the year in a remote environment for all things are changing by the minute. Your long run.” students due to late summer surges in COVID-19 in our communities. As we were putting the remote plan teacher is working numerous hours to help The Eppler Junior High School student in place, we were already looking at how we could safely your child succeed. This is out of everyone’s believes the difference in succeeding this year bring students back to in-person instruction – our control. -

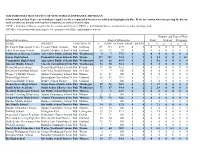

2020 Immunization Status of New School Entrants, Michigan

2020 IMMUNIZATION STATUS OF NEW SCHOOL ENTRANTS, MICHIGAN Schools with less than 95 percent of students complete for the recommended vaccines are bolded and highlighted in blue. Please use caution when interpreting the data in s small enrollments. Schools with less than 5 students are omitted from the data. COMP = # of student who are complete for the recommended vaccines; PROV = # of students who are provisional or in a dose waiting period; INCOM = # of students with an incomplete vaccination record; PHIL = philosophical waivers Number and Type of Waiv School Information Student Information Total Medical Religious NAME DISTRICT TYPECOUNTY N COMP %COMP PROV INCOM n % n % n % Tri County Educational Center Ferndale Public Schools Pub Oakland 199 194 97.5 0 5 0 0 0 0 0 0 Adler Elementary School Southfield Public School Di Pub Oakland 20 19 95 0 1 0 0 0 0 0 0 Pathways to Success AcademAnn Arbor Public Schools Pub Washtenaw 9 7 77.8 0 2 0 0 0 0 0 0 Salem High School Plymouth Canton Schools Pub Wayne 137 128 93.4 1 2 6 4.4 0 0 1 0.7 Community High School Ann Arbor Public Schools Pub Washtenaw 18 16 88.9 0 1 1 5.6 0 0 0 0 Lincoln Middle School Lincoln Consolidated SchoPub Washtenaw 53 50 94.3 0 3 0 0 0 0 0 0 Detroit Merit Academy Detroit Merit Charter AcadePub Detroit 57 56 98.2 1 0 0 0 0 0 0 0 Riverview East High School East China School District Pub St. -

F Cusfor the Community

Utica Community Schools Ray Washington Township December 2018 Township Shelby Township Macomb Township Utica Sterling for the Heights community A Publication for the Residents of Utica Community Schools FFrom the CUS Superintendent... From the youngest Christine M. Johns, Ed.D. members of our community Giving Thanks As 2018 nears its end, we look come the biggest hearts forward to the upcoming holidays Whether it is spreading holiday cheer, collecting food the pediatric and special gatherings with family and friends. items, securing toy donations or making sure neighbors department of Traditionally many of us reflect back on the year stay warm this winter, UCS students are showing their Beaumont Hospital in review and give thanks for the gifts we have extraordinary compassion in big ways. Students from all in Royal Oak. received, including gifts of support, from those 36 schools are involved in charitable giving this holiday around us. Giving back to the season to more than 200 separate service projects. With this in mind, I would like to share the community appreciation of the entire district to our residents for Giving back to its community is a noteworthy UCS is also important to students at Ebeling Elementary in the care and confidence that underlined the success- tradition that thousands of its students have embraced Macomb Township. They are busily decorating a giant ful passage of our recent safety and security bond throughout the years. Current student council president Christmas tree with brand new pairs of mittens, warm proposal. at West Utica Elementary, Ashley Mathews, said it winter hats and scarfs they have collected. -

Comprehensive Annual Financial Report for the Fiscal Year Ended June 30, 2019

Utica Community Schools Comprehensive Annual Financial Report For the Fiscal Year Ended June 30, 2019 Utica Community Schools 11303 Greendale Sterling Heights, Michigan 48312 COMPREHENSIVE ANNUAL FINANCIAL REPORT UTICA COMMUNITY SCHOOLS 11303 Greendale Sterling Heights, Michigan 48312 (586) 797-1000 For the Fiscal Year Ended June 30, 2019 BOARD OF EDUCATION Robert A Ross, Ph.D. President Mary K. Thomas, Ph.D Vice President Denyeal Nesovski, Secretary Michele Templeton, Treasurer Jennifer L. Prybys, Trustee Kimberly Becker, Trustee Kelli Rankin, Trustee SUPERINTENDENT OF SCHOOLS Christine M. Johns, Ed.D., Superintendent Report prepared by the Finance Department Utica Community Schools Contents Introductory Section Letter of Transmittal i-ix Organizational Chart x ASBO Certificate of Excellence in Financial Reporting xi Financial Section Independent Auditor's Report 1-2 Management's Discussion and Analysis 3-10 Basic Financial Statements Government-wide Financial Statements: Statement of Net Position 11 Statement of Activities 12 Fund Financial Statements: Governmental Funds: Balance Sheet 13 Reconciliation of the Balance Sheet to the Statement of Net Position 14 Statement of Revenue, Expenditures, and Changes in Fund Balances 15 Reconciliation of the Statement of Revenue, Expenditures, and Changes in Fund Balances to the Statement of Activities 16 Proprietary Fund - Internal Service Fund: Statement of Net Position 17 Statement of Revenue, Expenses, and Changes in Net Position 18 Statement of Cash Flows 19 Fiduciary Fund - Statement of Assets -

2018 September Edition

***********ECRWSSEDDM*********** NON-PROFIT ORG. US POSTAGE Residential Customer PAID Utica Community Schools ROYAL OAK, MI PERMIT NO. 618 Ray Washington Township September 2018 Township Shelby Township Macomb Township Utica for the Sterling Heights CUScommunity F A PPublication for the Residents of Utica Community Schools From the Superintendent... Back to School is fi lled with exciting Christine M. Johns, Ed.D. traditions for students and volunteers Welcome to another greateat Thanks to the generosity of one local service organization, The supplies are funded through a donation from Meijer school year in Utica one of those traditions – picking out a new backpack and Inc. and fundraisers held by the service club. Community Schools getting new school supplies – will be experienced by even One of the volunteers more students. The 2018-2019 school year is now offi cially stuffi ng the backpacks was under way with a renewed sense of energy and Recently, the Kiwanis senior citizen Joyce Decker. commitment. Club of Utica-Shelby “What we are doing is worked with area volun- Utica Community Schools remains a destination important because these district focused on success, thanks to an involved teers to stuff more than community, dedicated staff and a commitment 300 backpacks for stu- to making sure our students have a competitive dents throughout UCS advantage for college and career. who may need assistance. We create that advantage through four key strat- “We want to make sure egies: providing academic excellence, promoting they have the supplies student innovation, preparing positive digital they need to learn,” Photo credit: Linda-Ann Heldt citizens and ensuring accountability. -

High School Registration Summary

High School Registration Summary Participating in the Michigan e-Transcript Initiative will help ensure that schools may retain their federal stimulus dollars under the America Recovery and Reinvestment Act of 2009. During e-Transcript registration, a school staff member selected one of four phases to complete the installation, testing and training steps. The phases are depicted below: Installation Phases Phase Start End 1 December 1, 2009 February 28, 2010 2 March 1, 2010 May 31, 2010 3 June 1, 2010 August 31, 2010 4 September 1, 2010 November 30, 2010 When viewing this registration summary, you will notice that schools fall into one of nine statuses: Status Definition Installing The school received the installation instructions, is currently installing the software and sending test transcripts. Troubleshooting Docufide and/or the school are working on an issue regarding the student information system. Non-compliant The school sent the test transcripts, but is missing the student Unique Identification Code, building code and/or district code, labeled (format) as UIC, BCODE and DCODE, respectively. The school has been notified of these missing fields and Docufide is awaiting new test files to be sent. Non-compliant The school has not completed registration by the December 31, 2009 deadline or has not become "live" with the service in the selected phase. Pending training The school has completed the software installation and the transcripts contain the three required fields. The staff members at the school who will process transcripts still need to attend the online training. Unresponsive The school has received the installation instructions, but did not install the software and/or send test transcripts. -

Sterling Heights, MI | Detroit MSA PETCO CONSIDERING IPO in 2021

PETCO CONSIDERING IPO IN 2021 OFFERING MEMORANDUM Petco Sterling Heights, MI | Detroit MSA This property is listed in conjunction with Michigan-licensed real estate broker Kwekel Companies. www.preservewestcapital.com TABLE OF CONTENTS PROPERTY HIGHLIGHTS 1 AERIALS 5 PROPERTY INFORMATION 2 ABOUT THE AREA 7 TENANT INFORMATION 3 DEMOGRAPHICS 9 SITE PLAN 4 Disclaimer MGM Capital Corp dba Preserve West Capital (“Broker”) has been retained on an exclusive basis to market the property Putnam Daily described herein (“Property”). Broker has been authorized by the Seller of the Property (“Seller”) to prepare and distribute Partner the enclosed information (“Material”) for the purpose of soliciting offers to purchase from interested parties. More detailed financial, title and tenant lease information may be made available upon request following the mutual execution of a letter of 415.445.5107 intent or contract to purchase between the Seller and a prospective purchaser. You are invited to review this opportunity and [email protected] make an offer to purchase based upon your analysis. If your offer results in the Seller choosing to open negotiations with you, CA RE License #01750064 you will be asked to provide financial references. The eventual purchaser will be chosen based upon an assessment of price, terms, ability to close the transaction and such other matters as the Seller deems appropriate. Kevin Delehanty The Material is intended solely for the purpose of soliciting expressions of interest from qualified investors for the acquisition of the Property. The Material is not to be copied and/or used for any other purpose or made available to any other person Senior Managing Director without the express written consent of Broker or Seller. -

2019-2020 Utica Community Schools Continuity of Learning and COVID

2019-2020 Utica Community Schools Continuity of Learning and COVID-19 Response Plan April 2020 Utica Community Schools Board of Education Robert A. Ross, Ph.D., President Mary K. Thomas, Ph.D., Vice President Michele Templeton, Treasurer Denyeal Nesovski, Secretary Jennifer L. Prybys, Trustee Kimberly Becker, Trustee Kelli Rankin, Trustee Christine M. Johns, Ed.D. Superintendent of Schools Administration Executive Leadership Team Michael Bender, Ph.D., Chief of Staff John Graham, Assistant Superintendent for Auxiliary Services Robert Monroe, Assistant Superintendent for Teaching and Learning Michael Sturm, Assistant Superintendent for Human Resources and Transportation Services Michele VanDeKerkhove, Executive Administrator of Elementary Schools Steven Pfannes, Executive Administrator of Secondary Schools Jill Tomyn, Executive Director of Business and Finance Teaching and Learning Communications Sean Waymaster, Executive Director of Special Services Tim McAvoy, Director of School/Community Relations Kim Charland, Director of Secondary Programs Nancy Kort, Public Relations Coordinator Geoffrey Clark, Director of Assessment and Accountability Catherine Einhaus, Director of Elementary Programs Food Services Tumara Johnston, Supervisor of Special Services Mandy Sosnowski, Director of Food and Nutrition Services Karen Kennedy, Supervisor of Special Services Susan Towers, Supervisor of Special Services Information Technology Trapper Hallam, Instructional Technology Coach Sandro Silvestri, Executive Director of Information Technology Jacqueline Zawierucha, Instructional Technology Coach Todd Daniels, Director of Technology Mission We are committed to exemplary teaching and learning in order for our students to be prepared for success in the 21st Century. We will achieve this commitment by engaging the entire community to focus on each child’s achievement, with the expectation that every student will pursue some type of post-high school educational endeavor. -

Comprehensive Annual Financial Report for the Fiscal Year Ended June 30, 2017

Utica Community Schools Comprehensive Annual Financial Report For the Fiscal Year Ended June 30, 2017 Utica Community Schools 11303 Greendale Sterling Heights, Michigan 48312 COMPREHENSIVE ANNUAL FINANCIAL REPORT UTICA COMMUNITY SCHOOLS 11303 Greendale Sterling Heights, Michigan 48312 (586) 797-1000 For the Fiscal Year Ended June 30, 2017 BOARD OF EDUCATION Gene L. Klida, President Michele Templeton, Vice President Jennifer L. Prybys, Secretary Robert A. Ross, Ph.D., Treasurer Ken Krolczyk, Trustee Mary K. Thomas, Ph.d, Trustee Denyeal Nesovski, Trustee SUPERINTENDENT OF SCHOOLS Christine M. Johns, Ed.D., Superintendent Report prepared by the Finance Department Utica Community Schools Financial Report with Supplemental Information June 30, 2017 Utica Community Schools Contents Introductory Section Letter of Transmittal i-viii Organizational Chart ix ASBO Certificate of Excellence in Financial Reporting x Financial Section Independent Auditor's Report 1-3 Management's Discussion and Analysis 4-13 Basic Financial Statements Government-wide Financial Statements: Statement of Net Position 14 Statement of Activities 15 Fund Financial Statements: Governmental Funds: Balance Sheet 16 Reconciliation of the Balance Sheet of Governmental Funds to the Statement of Net Position 17 Statement of Revenue, Expenditures, and Changes in Fund Balances 18 Reconciliation of the Statement of Revenue, Expenditures, and Changes in Fund Balances of Governmental Funds to the Statement of Activities 19 Proprietary Fund - Internal Service Fund: Statement of Net Position -

ED 060 506 TITLE INSTITUTION SPONS AGENCY PUB DATE EDRS PRICE DESCRIPTORS IDENTIFIERS ABSTRACT DOCUMENT RESUME EA 004 003 the Op

DOCUMENT RESUME ED 060 506 EA 004 003 TITLE The Optional Five-Term Year-Round Educational Plan. A Step Toward Implementing Plans for Extending the Regular School Year. 45 + 45 + 45 + 45 = 180(+ 45 = Fifth Term.) Phase II: The Communications Phase. INSTITUTION Utica Community Schools, Mich. SPONS AGENCY Michigan State Dept. of Education, Lansing. PUB DATE Jul 71 NOTE 243p. EDRS PRICE MF-$0.65 HC-$9.87 DESCRIPTORS Communications; *Community Attitudes; Community Schools; Directories; Educational Finance; Educational Research; Feasibility Studies; *Information Dissemination; Parent Attitudes; Pilot Projects; *School Community Relationship; *School Districts; School Schedules; Slides; *Year Round Schools IDENTIFIERS Michigan; Utica Community Schools ABSTRACT The Utica Community School District was one of several school districts in Michigan to receive a second grant from the State Legislature to continue research and communications on the year-round school concept during the 1970-71 fiscal year. This communications phase was designed to gather, investigate, analyze, and disseminate information concerning the possibilities of conducting a pilot, year-round school operation. The objectives of Phase II were to (1) develop an optional 3-year, 5-term, year-round educational plan; (2) communicate this educational plan to local residents;(3) develop a tooling-up Plan to move toward the optional 5-term, year-round educational concept including the cost analysis for Phases II and IV (1971-1976); and (4) the identification of a, possible level and a location for a pilot, year-round program. A related document is EA 004 002.(Autho31 U.S. DEPARTMENTOF HEALTH. EDUCATION & WELFARE OFFICE OF EDUCATION THIS DOCUMENT HASBEEN REPRO- DUCED EXACTLY ASRECEIVED FROM THE PERSON ORORGANIZATION ORIG- INATING IT. -

Comprehensive Annual Financial Report for the Fiscal Year Ended June 30, 2016

Utica Community Schools Comprehensive Annual Financial Report For the Fiscal Year Ended June 30, 2016 Utica Community Schools 11303 Greendale Sterling Heights, Michigan 48312 COMPREHENSIVE ANNUAL FINANCIAL REPORT UTICA COMMUNITY SCHOOLS 11303 Greendale Sterling Heights, Michigan 48312 (586) 797-1000 For the Fiscal Year Ended June 30, 2016 BOARD OF EDUCATION Carol Klenow, Ed.D., President Gene L. Klida, Vice President Michele Templeton, Secretary Robert A. Ross, Ph.D., Treasurer Jennifer L. Prybys, Trustee Ken Krolczyk, Trustee Mary K. Thomas, Ph.d, Trustee SUPERINTENDENT OF SCHOOLS Christine M. Johns, Ed.D., Superintendent Report prepared by the Finance Department Utica Community Schools Financial Report with Supplemental Information June 30, 2016 Utica Community Schools Contents Introductory Section Letter of Transmittal i-vii Organizational Chart viii ASBO Certificate of Excellence in Financial Reporting ix Financial Section Independent Auditor's Report 1-3 Management's Discussion and Analysis 4-13 Basic Financial Statements Government-wide Financial Statements: Statement of Net Position 14 Statement of Activities 15 Fund Financial Statements: Governmental Funds: Balance Sheet 16 Reconciliation of the Balance Sheet of Governmental Funds to the Statement of Net Position 17 Statement of Revenue, Expenditures, and Changes in Fund Balances 18 Reconciliation of the Statement of Revenue, Expenditures, and Changes in Fund Balances of Governmental Funds to the Statement of Activities 19 Proprietary Fund - Internal Service Fund: Statement of -

Chief Connection Is the Official Newsletter of Utica High School

Utica High School Chief November 2016 Connection http://www.uticahigh.org See “About the Cover” on page 12 Utica High School Vision Statement: Empowering students to reach their full potential as members of a global community. Utica High School Mission Statement: The mission of Utica High School is to develop successful learners with the support of our community of educators, students, and parents. Our diverse student body will have an equitable, rigorous, and comprehensive education in a safe and supportive environment that promotes self-discipline, motivation, and excellence in learning. We aim to cul- tivate individual learners with active and creative minds, and a sense of understanding and compassion for others. Index is available on page 3 From the Principal’s Desk Dear Chieftain Families, It seems impossible, but we’ve reached November already and the end of Quarter 1. We are just a few weeks from our Parent Teacher Conferences and the Thanksgiving Holiday. In between now and then we have an election and a lot of work to do! Though we will be here for staff professional development, school will be closed on Tuesday, Nov. 8 for the General Election. Our conferences look a little different this year, with conferences being Tuesday, November 15 (4:30 - 7:30) and Thursday, No- vember 17 (12:00 – 3:00 and 4:30 – 7:30). Conferences will also be held in three locations, the Main Gym, the Cafeteria and the Media Center. Our Media Center will house our counseling department, Special Education teachers, and English as a Second Language teachers. All other teachers will be divided alphabetically between the Main Gym and the Cafeteria.